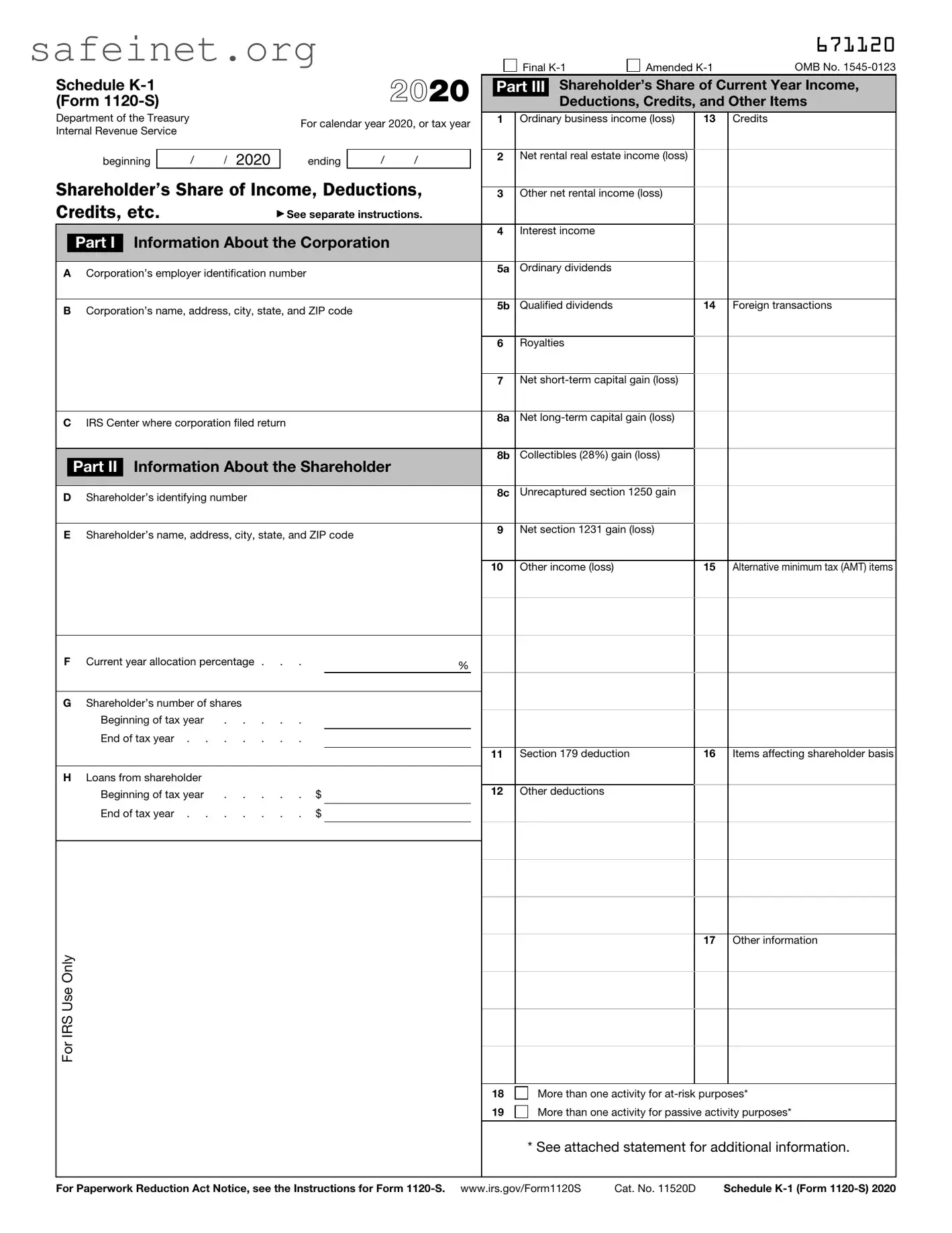

The IRS Schedule K-1 (Form 1120-S) serves a crucial role in the tax reporting process for S corporations and their shareholders. This form provides a lifetime record of a shareholder's share of the corporation’s income, deductions, and credits. When an S corporation completes its yearly taxes, it uses the K-1 to communicate each shareholder's portion of profits or losses, which ultimately influences their personal tax obligations. Shareholders receive this information to report on their individual tax returns, guiding them through the sometimes-complex world of pass-through taxation. Additionally, the Schedule K-1 form tracks various financial elements, including dividends paid and capital gains, ensuring that transparency is maintained between the corporation and its stakeholders. Understanding this form is essential for any shareholder, as it impacts financial reporting and influences how taxes are calculated at the individual level. Overall, the Schedule K-1 1120-S is a pivotal document that aligns the financial interests of S corporations with the tax responsibilities of their shareholders.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

671120 |

|

|

|

|

|

|

|

|

|

|

2020 |

|

|

|

Final |

Amended |

OMB No. |

|||

Schedule |

|

|

|

|

|

|

|

Part III |

Shareholder’s Share of Current Year Income, |

||||||||||

(Form |

|

|

|

|

|

|

|

Deductions, Credits, and Other Items |

|||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

Department of the Treasury |

|

|

|

For calendar year 2020, or tax year |

|

1 |

Ordinary business income (loss) |

13 |

Credits |

||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

beginning |

|

/ |

/ 2020 |

|

ending |

|

/ |

/ |

|

2 |

Net rental real estate income (loss) |

|

|

||||

Shareholder’s Share of Income, Deductions, |

|

|

|

|

|||||||||||||||

|

3 |

Other net rental income (loss) |

|

|

|||||||||||||||

Credits, etc. |

|

|

▶ See separate instructions. |

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Interest income |

|

|

|

||

|

|

Part I |

Information About the Corporation |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

Corporation’s employer identification number |

|

|

|

|

5a |

Ordinary dividends |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

Corporation’s name, address, city, state, and ZIP code |

|

|

|

|

5b |

Qualified dividends |

|

14 |

Foreign transactions |

|||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Royalties |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Net |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

C |

IRS Center where corporation filed return |

|

|

|

|

8a |

Net |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8b |

Collectibles (28%) gain (loss) |

|

|

||

|

|

Part II |

Information About the Shareholder |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

D |

Shareholder’s identifying number |

|

|

|

|

|

|

|

8c |

Unrecaptured section 1250 gain |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

E |

Shareholder’s name, address, city, state, and ZIP code |

|

|

9 |

Net section 1231 gain (loss) |

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

10 |

Other income (loss) |

|

15 |

Alternative minimum tax (AMT) items |

|||

F Current year allocation percentage . . . |

% |

|

GShareholder’s number of shares

Beginning of tax year |

. . . . . |

|

|

|

|

|

|

|

End of tax year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Section 179 deduction |

16 Items affecting shareholder basis |

|

|

|

|

|

|

|

|

|

|

H Loans from shareholder |

|

|

|

|

|

|

|

|

Beginning of tax year |

. . . . . |

$ |

|

12 |

Other deductions |

|

||

|

|

|

|

|

|

|||

End of tax year . . |

. . . . . |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

17 Other information

For IRS Use Only

18 More than one activity for

19 More than one activity for passive activity purposes*

* See attached statement for additional information.

For Paperwork Reduction Act Notice, see the Instructions for Form |

Cat. No. 11520D |

Schedule |

| Fact Name | Details |

|---|---|

| Purpose | The IRS Schedule K-1 (Form 1120-S) is used to report income, deductions, and credits from S corporations. |

| Filing Requirement | Shareholders receive a K-1 to report their share of the corporation's income on their personal tax returns. |

| Deadline | The form is generally due to shareholders by March 15, following the end of the tax year. |

| Information Included | The K-1 contains information about the taxpayer’s share of income, losses, deductions, and credits. |

| Box Categories | Different boxes on the form categorize various types of income, including ordinary business income and rental income. |

| State Filing | Many states require their own Schedule K-1 forms, potentially governed by laws specific to each state. |

| Taxation | S corporation income is generally passed through to shareholders, meaning the corporation itself typically does not pay federal income tax. |

| Importance for Shareholders | Shareholders must ensure they correctly report the K-1 information to avoid issues with the IRS. |

| Amendments | If changes occur, the corporation must issue amended K-1s to shareholders to reflect updated information. |

Filling out the IRS Schedule K-1 (Form 1120-S) is an important part of reporting income from an S corporation. After completing this form, you will provide it to each shareholder, who will use the information for their personal tax filings. Below are the steps to ensure you fill out the form accurately.

What is the IRS Schedule K-1 1120-S form?

The Schedule K-1 1120-S form is a tax document issued by S corporations to report each shareholder’s share of income, deductions, and credits. It serves as a pass-through entity, meaning that the corporation itself does not pay taxes at the corporate level; instead, shareholders report their share of the company's income on their personal tax returns.

Who needs to file Schedule K-1 1120-S?

Only S corporations are required to file Schedule K-1 1120-S. Each shareholder of the S corporation receives a K-1 that details their specific financial information. Shareholders must file this form with their individual tax returns.

When is the Schedule K-1 1120-S due?

The Schedule K-1 must be issued by the S corporation to its shareholders by March 15 of each year. This aligns with the deadline for the S corporation's return (Form 1120-S). Shareholders should ensure they receive their K-1 in a timely manner to meet their filing obligations.

How is the information on Schedule K-1 1120-S used?

Shareholders use the information reported on Schedule K-1 to complete their personal income tax returns. The income, deductions, and credits reported inform their overall tax liability and are included on Form 1040 and associated schedules.

Can I get my Schedule K-1 electronically?

Yes, many S corporations provide Schedule K-1 electronically. Shareholders may receive it via email or through a secure online portal. Ensure that you keep a copy for your records and for filing your taxes.

What should I do if I don’t receive my Schedule K-1?

If you haven’t received your K-1 by the filing deadline, you should contact the S corporation directly. Sometimes delays occur due to administrative issues. It is essential to resolve this promptly, as you may need the information to file your tax return accurately.

What happens if I receive an incorrect Schedule K-1?

If the information on your K-1 is incorrect, contact the S corporation for a corrected version. The corporation is responsible for providing accurate information, and you will need the revised K-1 to ensure correct reporting on your tax return.

Aren’t all S corporations required to file a Schedule K-1?

Yes, all S corporations must file a Schedule K-1 for each shareholder. This requirement applies regardless of whether the corporation had income, deductions, or credits. It ensures that all shareholders receive the necessary information for their tax filings.

What if I have multiple K-1 forms from different S corporations?

In the event you receive K-1 forms from multiple S corporations, it is important to report each one on your tax return. Each K-1 includes information specific to that corporation, and combining this information helps determine your overall tax situation.

Are there any penalties for not filing Schedule K-1?

Yes, failing to file or incorrectly filing a Schedule K-1 can result in penalties for both the S corporation and the shareholder. The IRS can impose fines for late filings, and shareholders may face issues during audits or when correcting their returns.

Incomplete Information: One common mistake involves not providing all required information. Individuals often omit details such as the taxpayer's name, identification number, or business details. Each section of the form needs careful attention to ensure completeness.

Incorrect Tax Year: Another frequent error relates to entering the wrong tax year. The Schedule K-1 must reflect the appropriate year based on when the income or loss was earned. Failing to match the form with the right year can lead to discrepancies in tax reporting.

Misreporting Income: Mistakes can also occur when reporting income, deductions, or credits. Shareholders may unintentionally misclassify types of income, leading to understating or overstating tax liability. Accurate categorization is essential for compliance with IRS regulations.

Neglecting to File: Some individuals mistakenly believe that if they are not receiving a K-1 for the current tax year, they do not need to file anything at all. However, each partner or shareholder in an S Corporation must report their share of income and losses, regardless of whether they received a K-1 form.

The IRS Schedule K-1 1120-S form plays a vital role in the tax reporting process for S corporations. Alongside this form, there are several other key documents that often accompany it. Each of these documents serves a unique purpose in ensuring accurate tax reporting and compliance with IRS requirements.

Completing these forms accurately is essential for compliance with IRS regulations. They each contribute to a clear picture of the S corporation's earnings and tax obligations. Careful attention to detail in preparing these documents can help avoid problems or delays during the tax process.

The IRS Schedule K-1 (Form 1120-S) is similar to the Schedule K-1 (Form 1065) used by partnerships. Both forms report the share of income, deductions, and credits passed through to the partners or shareholders from the entity. While Schedule K-1 (Form 1120-S) focuses on S corporations, the partnership version captures details for partnerships, detailing how each partner's income and tax obligations are determined based on their share of the partnership's profits or losses.

Another similar document is the Schedule K-1 (Form 1041) for estates and trusts. This form outlines the distributions made to beneficiaries from an estate or trust. Much like the S corporation version, it conveys how much taxable income each beneficiary should report on their personal tax returns. The process of reporting distributed income ensures consistency in tax treatment across different forms of business and estate distributions.

The IRS Form 8804 is another relevant document when discussing income reporting for partnerships. This form reports the annual tax liability of a partnership that is subject to the Foreign Partners U.S. Tax Compliance regulations. While it primarily focuses on foreign partners, like Schedule K-1, it helps ensure all partners are informed of their tax responsibilities and it aligns with the flow-through nature of income reporting.

Form 1120, which is the U.S. Corporation Income Tax Return, serves as another counterpart to the K-1. Unlike the K-1 forms, which are used to report income to shareholders and partners, Form 1120 is used by C corporations to report their total income, gains, losses, deductions, and credits directly to the IRS. Both forms, however, ultimately seek to provide clarity on the income and tax situation of different entity types.

Further along the same lines, the Schedule C (Form 1040) is often used by sole proprietors to report income and expenses from their business. While it provides an overview of the business owner’s finances and taxes owed, Schedule C also emphasizes how individual business owners report profits directly on their own tax returns, mirroring the way S corporations pass income to their shareholders.

The IRS Form 5471 is relevant in terms of international operations and foreign income reporting. Primarily used by U.S. citizens and residents who are shareholders of certain foreign corporations, it details ownership interests and income similar to a K-1. Both forms play a crucial role in ensuring taxation is appropriately reported for income generated both domestically and internationally.

Form 1065 is another important document that works in a similar capacity to the Schedule K-1 (Form 1120-S). This is the U.S. Return of Partnership Income, which provides a summary of the partnership's income, deductions, and credits. Each partner receives a Schedule K-1 from the 1065, similar to how shareholders of an S corporation receive the K-1, illustrating that both forms provide essential information for individual income tax calculations.

The 1099-MISC form also shares similarities with the K-1 in that it reports various types of income other than wages, salaries, or tips. This form is often issued to independent contractors or freelancers and conveys the earnings these individuals need to report. Both K-1 and 1099-MISC serve the vital purpose of reporting income generated through various means outside of traditional employment.

Form 990, filed by most tax-exempt organizations, also follows the spirit of transparency found within the K-1 forms. This form provides insight into the financial health and activities of non-profit organizations. While not directly comparable, both the K-1 and Form 990 illustrate the importance of financial disclosures in shaping tax obligations and benefitting stakeholders.

Finally, Form 1120-SF, or the U.S. Income Tax Return for Settlement Funds, also bears similarities with the K-1. This form is used by settlement funds established under specific legal and tax regulations. Shareholders of these funds may receive K-1 equivalents detailing their income share, showing the variety of scenarios in which income can be reported through pass-through mechanisms similar to those in the Schedule K-1.

When filling out the IRS Schedule K-1 (Form 1120-S), clarity and accuracy are key. Here are important dos and don’ts to keep in mind:

Attention to detail is crucial. Following these guidelines can help ensure that your filing process goes smoothly and without unnecessary complications. By doing your best to follow these practices, you will be better positioned to address any questions or issues that may arise from the IRS.

Understanding the IRS Schedule K-1 1120-S form can be tricky. Here are four common misconceptions people often have about this form.

Many people think that only businesses receive a Schedule K-1. In reality, this form is issued to shareholders of S corporations, which are a type of business entity. However, individuals can also receive K-1s if they have invested in partnerships or limited liability companies (LLCs) that file a K-1.

Another misconception is that a K-1 is issued only when there are profits. A K-1 can be issued even if your share of the business resulted in a loss. This loss can often be used to offset other income, which is beneficial for tax purposes.

Some believe that receiving a K-1 means they don’t need to report any income on their tax return. In fact, any income, losses, or deductions listed on the K-1 need to be included in your personal tax filing. Failure to report this can lead to complications with the IRS.

It's a common thought that all K-1 forms are identical. However, each K-1 can differ based on the type of entity issuing it. The information required on a K-1 for a partnership is different from that on one from an S corporation or an LLC, so it’s important to understand the specifics of the K-1 you receive.

Clarifying these misconceptions can help ensure that you handle your taxes correctly. Understanding the Schedule K-1 is an important part of accurately managing your tax obligations.

When dealing with the IRS Schedule K-1 (Form 1120-S), it's important to understand its purpose and how to fill it out correctly. This form is crucial for reporting income, deductions, and credits from an S corporation to its shareholders. Here are some essential takeaways: