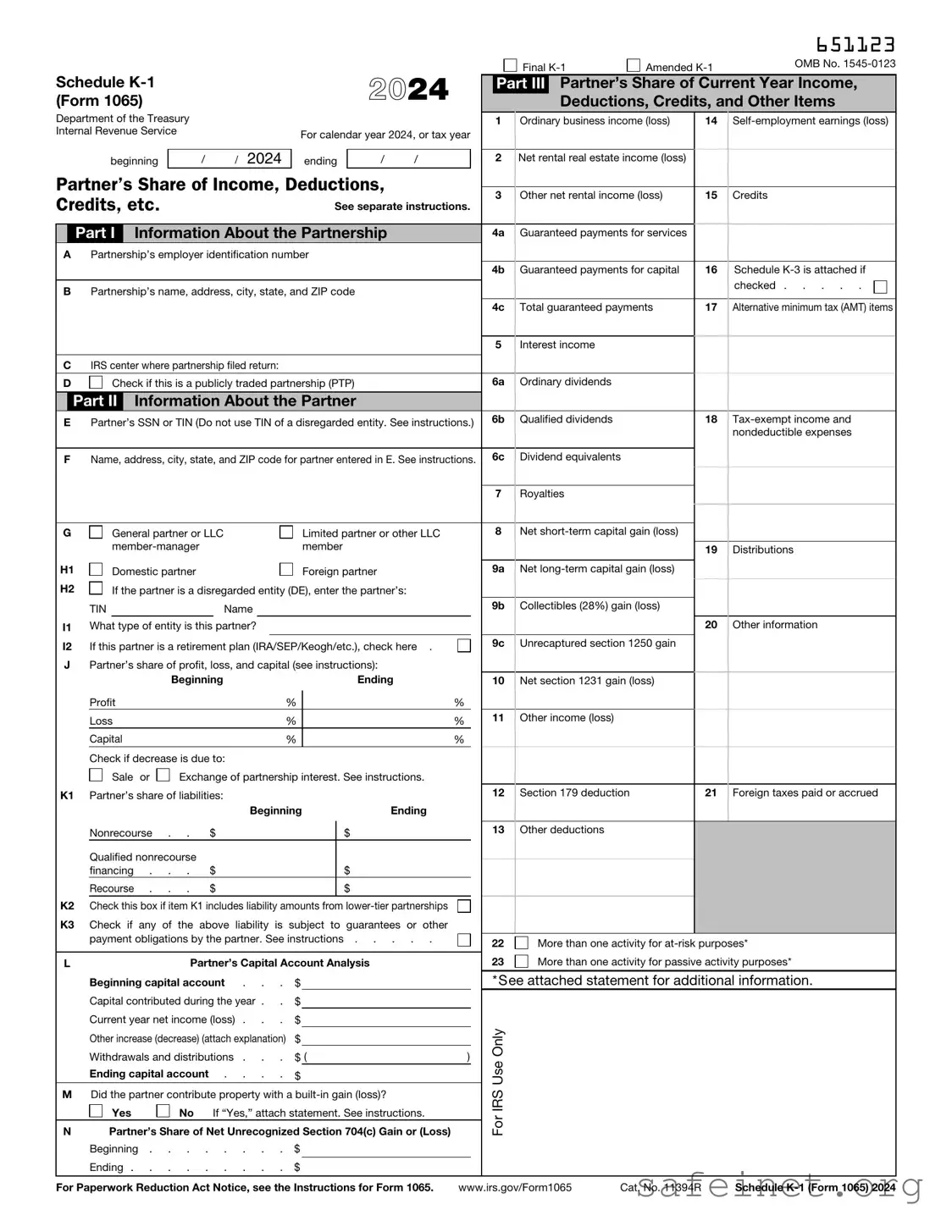

The IRS Schedule K-1 (Form 1065) plays a crucial role for partnerships and their partners in the world of taxation. This form is used to report each partner's share of income, deductions, credits, and other important tax items from the partnership. When a partnership files its tax return, it must provide a K-1 to each partner, detailing their specific financial stake in the business. This information is essential for partners, as they need it to accurately report their earnings on their individual tax returns. The K-1 breaks down various components, including ordinary business income, rental income, and capital gains, ensuring that partners understand their tax obligations. Furthermore, the form also addresses any losses that can be claimed, which can significantly impact a partner's tax situation. Understanding the intricacies of the K-1 is vital for anyone involved in a partnership, as it directly affects their tax liabilities and overall financial planning.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

651123 |

|

|

|

|

|

|

|

2024 |

|

|

|

Final |

Amended |

OMB No. |

|||

Schedule |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

Part III |

Partner’s Share of Current Year Income, |

||||||||||

(Form 1065) |

|

|

|

|

|

|

|

Deductions, Credits, and Other Items |

||||||||

Department of the Treasury |

|

|

|

|

|

|

1 |

Ordinary business income (loss) |

14 |

|||||||

Internal Revenue Service |

|

|

For calendar year 2024, or tax year |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

ending |

|

|

|

|

|

|

|

|

|

|

|

beginning |

|

/ |

/ 2024 |

/ |

/ |

2 |

Net rental real estate income (loss) |

|

|

||||||

Partner’s Share of Income, Deductions, |

|

|

|

|

|

|

|

|

|

|||||||

|

3 |

Other net rental income (loss) |

15 |

Credits |

||||||||||||

Credits, etc. |

|

|

See separate instructions. |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

Part I |

Information About the Partnership |

|

|

4a Guaranteed payments for services |

|

|

|||||||||

APartnership’s employer identification number

|

|

|

4b |

Guaranteed payments for capital |

16 |

Schedule |

|

|

|

|

|

|

checked |

B |

Partnership’s name, address, city, state, and ZIP code |

|

|

|||

|

|

|

||||

|

|

|

4c |

Total guaranteed payments |

17 |

Alternative minimum tax (AMT) items |

|

|

|

|

|

|

|

|

5 |

Interest income |

|

|

||

CIRS center where partnership filed return:

D |

|

Check if this is a publicly traded partnership (PTP) |

6a |

Ordinary dividends |

|

|

||||||||

|

Part II |

Information About the Partner |

|

|

|

|

|

|||||||

E |

Partner’s SSN or TIN (Do not use TIN of a disregarded entity. See instructions.) |

6b |

Qualified dividends |

18 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

nondeductible expenses |

|

|

|

|

|

|

|

||||||||

F |

Name, address, city, state, and ZIP code for partner entered in E. See instructions. |

6c |

Dividend equivalents |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Royalties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G |

|

General partner or LLC |

|

|

Limited partner or other LLC |

8 |

Net |

|

|

|||||

|

|

|

|

|

member |

|

|

|

19 |

Distributions |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

H1 |

|

Domestic partner |

|

|

Foreign partner |

9a |

Net |

|

|

|||||

H2 |

|

If the partner is a disregarded entity (DE), enter the partner’s: |

|

|

|

|

|

|||||||

|

|

TIN |

|

|

Name |

|

|

9b |

Collectibles (28%) gain (loss) |

|

|

|

||

I1 |

What type of entity is this partner? |

|

|

|

|

|

20 |

Other information |

||||||

I2 |

If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here . |

9c |

Unrecaptured section 1250 gain |

|

|

|||||||||

JPartner’s share of profit, loss, and capital (see instructions):

|

|

Beginning |

|

|

Ending |

|

|

|

|

10 Net section 1231 gain (loss) |

|

|||||

|

Profit |

|

|

% |

|

|

|

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Loss |

|

|

% |

|

|

|

% |

|

11 |

Other income (loss) |

|

|

|

||

|

Capital |

|

|

% |

|

|

|

% |

|

|

|

|

|

|

|

|

|

Check if decrease is due to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Sale or |

Exchange of partnership interest. See instructions. |

|

|

|

|

|

|

|

|

|

|||||

K1 Partner’s share of liabilities: |

|

|

|

|

|

|

12 |

Section 179 deduction |

21 Foreign taxes paid or accrued |

|||||||

|

|

|

Beginning |

Ending |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonrecourse |

. . |

$ |

|

|

$ |

|

|

|

13 |

Other deductions |

|

|

|

||

|

Qualified nonrecourse |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

financing . |

. . |

$ |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

Recourse . |

. . |

$ |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

K2 Check this box if item K1 includes liability amounts from |

|

|

|

|

|

|

|

|

|

|||||||

K3 Check if any of the above liability is subject to guarantees or other |

|

|

|

|

|

|

|

|

|

|||||||

|

payment obligations by the partner. See instructions |

|

|

|

22 |

More than one activity for |

||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

L |

|

Partner’s Capital Account Analysis |

|

|

|

23 |

More than one activity for passive activity purposes* |

|||||||||

|

Beginning capital account . . . |

$ |

|

|

|

|

|

|

|

*See attached statement for additional information. |

||||||

|

Capital contributed during the year . . |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Current year net income (loss) . . . |

$ |

|

|

|

|

|

|

|

Only |

|

|

|

|

||

|

Other increase (decrease) (attach explanation) |

$ |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Withdrawals and distributions . . . |

$ ( |

|

|

|

) |

|

|

Use |

|

|

|

|

|||

|

Ending capital account . . . . |

$ |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

M |

Did the partner contribute property with a |

|

|

|

|

|

IRS |

|

|

|

|

|||||

|

Yes |

No |

If “Yes,” attach statement. See instructions. |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

For |

|

|

|

|

|||||||

N |

Partner’s Share of Net Unrecognized Section 704(c) Gain or (Loss) |

|

|

|

|

|

|

|

|

|||||||

|

Beginning . . . . . . . . $ |

|

|

|

|

|

|

|

|

|

|

|||||

|

Ending |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

For Paperwork Reduction Act Notice, see the Instructions for Form 1065. |

www.irs.gov/Form1065 |

Cat. No. 11394R |

Schedule |

|||||||||||||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule K-1 (Form 1065) is used to report income, deductions, and credits from partnerships to the IRS and to the partners. |

| Who Files | Partnerships must file this form annually to report the financial activity of the partnership. |

| Partner Information | Each partner receives a K-1 that details their share of the partnership's income, losses, and other tax-related items. |

| Filing Deadline | The K-1 must be filed with the IRS by March 15 of the year following the tax year, unless an extension is granted. |

| State-Specific Forms | Some states require their own K-1 forms, governed by state laws. For example, California has Form 565 for partnerships. |

| Impact on Taxes | Partners must report the information from the K-1 on their individual tax returns, which can affect their overall tax liability. |

| Amendments | If changes occur after the K-1 is issued, amended forms must be filed to correct any discrepancies in reported income or deductions. |

Once you have gathered all necessary information, you can begin filling out the IRS Schedule K-1 (Form 1065). This form is essential for reporting income, deductions, and credits from partnerships. Completing it accurately is crucial for ensuring compliance with tax regulations.

After completing the form, ensure that all information is correct and submit it along with the partnership's tax return. Each partner should receive their copy for personal tax filing. Be sure to keep a copy for your records as well.

What is the IRS Schedule K-1 1065 form?

The IRS Schedule K-1 1065 form is used to report income, deductions, and credits from partnerships. It provides detailed information about each partner's share of the partnership's income, losses, and other tax-related items. Each partner receives a K-1 form, which they use to report their share on their individual tax returns.

Who needs to file a Schedule K-1 1065?

Partnerships must file a Schedule K-1 1065 for each partner. This includes general partnerships, limited partnerships, and limited liability companies (LLCs) that are treated as partnerships for tax purposes. Each partner then uses the K-1 to report their income and deductions on their personal tax returns.

When is the Schedule K-1 1065 due?

The Schedule K-1 1065 is typically due on the same date as the partnership's tax return, which is usually March 15 for calendar-year partnerships. However, if the partnership files for an extension, the K-1 may be submitted later, but it is important to ensure partners receive their K-1s in time to file their own returns.

How do I report the information from a Schedule K-1 1065 on my tax return?

To report the information from a Schedule K-1 1065, you will need to transfer the amounts listed on the K-1 to the appropriate sections of your individual tax return, typically on Form 1040. Each item on the K-1 corresponds to specific lines on your tax return, so it’s essential to follow the instructions carefully.

What should I do if my Schedule K-1 is incorrect?

If you find that your Schedule K-1 contains errors, you should contact the partnership for a corrected version. The partnership can issue a new K-1 if they made a mistake. It’s crucial to ensure that the information is accurate before you file your tax return, as discrepancies can lead to delays or issues with the IRS.

Can I e-file my tax return if I have a Schedule K-1?

Yes, you can e-file your tax return even if you have a Schedule K-1. Most tax preparation software supports the entry of K-1 information. Just make sure to enter the amounts correctly to ensure your tax return is accurate and complete.

What happens if I don’t receive my Schedule K-1 in time?

If you do not receive your Schedule K-1 in time to file your tax return, you have a few options. You can file your return without the K-1 and report the income when you receive it later, or you can file for an extension. However, be aware that if you owe taxes, you may still be liable for penalties and interest if you do not pay by the original due date.

Is the income reported on a Schedule K-1 subject to self-employment tax?

Yes, certain types of income reported on a Schedule K-1 may be subject to self-employment tax. This typically applies to income from partnerships where you are actively involved in the business. It’s important to review the K-1 carefully and consult a tax professional if you have questions about your specific situation.

What types of income are reported on a Schedule K-1 1065?

Schedule K-1 1065 reports various types of income, including ordinary business income, rental income, interest income, and capital gains. It may also include deductions, credits, and other tax-related items. Each partner's share of these items is reported separately, reflecting their ownership interest in the partnership.

Where can I find more information about Schedule K-1 1065?

For more information about Schedule K-1 1065, you can visit the IRS website. The IRS provides detailed instructions and resources that can help you understand how to complete the form and report the information correctly on your tax return. Additionally, consulting a tax professional can provide personalized guidance based on your circumstances.

Failing to report all income accurately. It is essential to include all sources of income, as missing any can lead to discrepancies.

Incorrectly entering partnership information. Ensure that the partnership's name, address, and tax identification number are accurate.

Not including the correct tax year. The K-1 form should reflect the tax year for which the income is being reported.

Neglecting to check the box for the appropriate partnership type. This can affect how income is taxed.

Misreporting the distribution amounts. Double-check that the amounts reported match the partnership's records.

Forgetting to sign and date the form. A signature is required to validate the information provided.

Failing to provide a copy to the IRS and the partners. Each partner should receive their copy for accurate reporting on their individual tax returns.

Not keeping copies of the submitted forms. Retaining a copy for personal records can be helpful for future reference or audits.

The IRS Schedule K-1 (Form 1065) is a critical document for partnerships, providing detailed information about each partner's share of income, deductions, and credits. When preparing taxes, several other forms and documents may accompany the K-1. Below is a list of commonly used forms that often work in conjunction with the Schedule K-1.

Understanding these forms and their purposes can streamline the tax preparation process for partnerships and their individual partners. Each document plays a role in ensuring accurate reporting and compliance with IRS regulations.

The IRS Schedule K-1 (Form 1065) is similar to the Schedule K-1 (Form 1120S) used for S corporations. Both documents report income, deductions, and credits allocated to shareholders or partners. While Schedule K-1 (1065) is specifically for partnerships, the S corporation version serves a similar purpose for shareholders. Each form provides a breakdown of an individual's share of the entity's income, which is essential for accurate tax reporting. The information on both forms helps recipients complete their individual tax returns, ensuring they account for their share of the business's financial activities.

Another document comparable to the IRS Schedule K-1 (Form 1065) is the Schedule C (Form 1040), which is used by sole proprietors. Schedule C details the income and expenses of a business operated by an individual. While Schedule K-1 (1065) allocates income from a partnership, Schedule C reflects the sole proprietor's income directly. Both documents help taxpayers report business earnings and determine their tax liability. They serve as critical tools for individuals to transparently report their financial activities to the IRS.

The IRS Form 1065 itself is another related document. This form is filed by partnerships to report their overall income, deductions, and other tax-related information. While Schedule K-1 (1065) provides individual partners with their specific share of the partnership's income, Form 1065 summarizes the partnership's financial situation as a whole. Together, they ensure that both the entity and its partners fulfill their tax obligations accurately and transparently.

The IRS Schedule K-1 (Form 1041) is also similar, as it pertains to estates and trusts. This form reports income distributed to beneficiaries from an estate or trust. Like the K-1 (1065), it allocates income, deductions, and credits, allowing beneficiaries to report their share on their individual tax returns. Both forms ensure that income is reported correctly and that beneficiaries understand their tax responsibilities regarding distributions received.

Lastly, the IRS Schedule E (Form 1040) is another document that shares similarities with the Schedule K-1 (Form 1065). Schedule E is used to report income or loss from rental real estate, partnerships, S corporations, estates, trusts, and more. While Schedule K-1 (1065) specifically details a partner's share of partnership income, Schedule E serves as a broader reporting tool for various income sources. Both documents help taxpayers accurately report their earnings and ensure compliance with tax regulations.

When filling out the IRS Schedule K-1 (Form 1065), it's essential to navigate the process carefully. This form is crucial for partnerships, as it reports each partner's share of income, deductions, and credits. Here’s a list of things to do and avoid:

Understanding the IRS Schedule K-1 (Form 1065) can be challenging. Here are ten common misconceptions about this form and the realities behind them.

In reality, each partner receives a K-1 that reflects their individual share of income, deductions, and credits based on the partnership agreement.

This is incorrect. The K-1 is primarily used by partnerships to report income, deductions, and credits to individual partners, regardless of their tax status.

False. Partners must report the income or loss shown on their K-1 on their personal tax returns, as it affects their overall tax liability.

This is misleading. The K-1 is not submitted with your personal tax return but should be kept for your records and used to complete your tax return accurately.

Not necessarily. Some items reported on the K-1 may be tax-exempt or subject to special treatment, depending on the nature of the income.

Many partnerships may not provide K-1s until later in the tax season, often after the April deadline, which can complicate filing your taxes on time.

Both general and limited partners receive a K-1, as all partners share in the income and losses of the partnership.

This is incorrect. Partnerships must still issue K-1s even if there are no profits, as they must report each partner's share of losses and other items.

Not necessarily. The K-1 reflects your share of the partnership's income, but actual tax liability depends on your overall financial situation and deductions.

This is a misconception. Partnerships are legally required to file Form 1065 and issue K-1s to report income and expenses to the IRS and partners.

Clearing up these misconceptions can help partners better understand their tax obligations and avoid potential issues with the IRS.

When filling out and using the IRS Schedule K-1 (Form 1065), it is essential to understand its purpose and how it impacts both partnerships and individual partners. Here are some key takeaways: