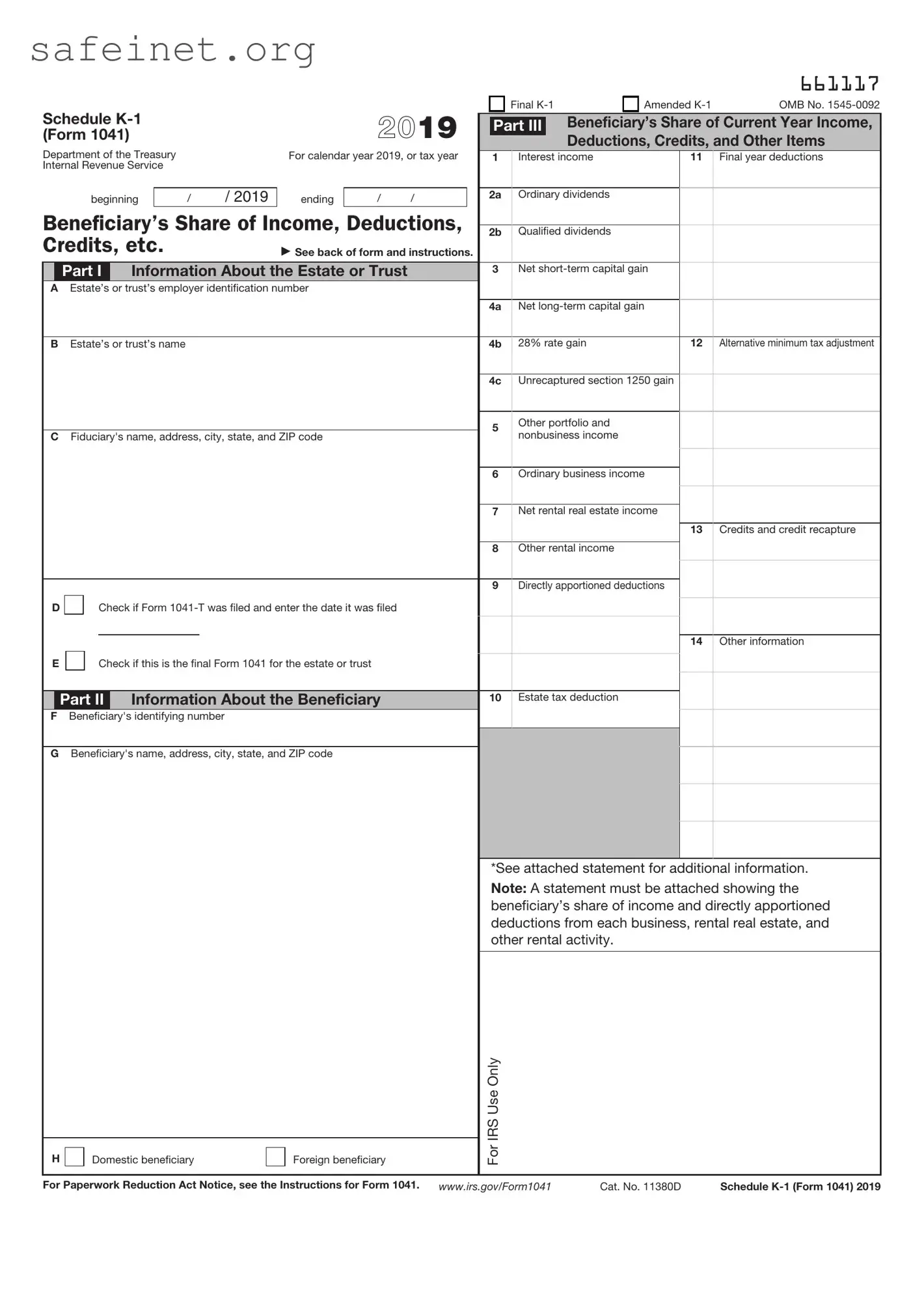

The IRS Schedule K-1 (Form 1041) serves a pivotal role in the realm of estate and trust taxation, providing essential information about the income earned by a trust or estate that is passed on to beneficiaries. This form details each beneficiary's share of income, deductions, and credits, thus influencing their individual tax return submissions. When a trust or estate generates income, expenses, or gains, it must report those figures on its tax return using Form 1041. The K-1 then breaks down how much of that income, whether it be from rental properties, dividends, or capital gains, is allocated to each beneficiary. Additionally, it allows for transparency in reporting tax distributions, which are crucial for tax compliance. Beneficiaries must carefully review their K-1s to understand their tax obligations, as accurate reporting can significantly affect their overall tax liabilities. Furthermore, the deadlines for filing these forms align closely with those for Form 1041, underscoring the importance of timely and accurate documentation in the estate and trust administration process.

Schedule |

|

|

|

2019 |

||

(Form 1041) |

|

|

|

|||

Department of the Treasury |

|

|

For calendar year 2019, or tax year |

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

beginning |

|

/ |

/ 2019 |

ending |

/ |

/ |

Beneficiary’s Share of Income, Deductions, Credits, etc.

Part I Information About the Estate or Trust

AEstate’s or trust’s employer identification number

BEstate’s or trust’s name

CFiduciary's name, address, city, state, and ZIP code

D |

|

|

Check if Form |

|

E |

|

|

|

|

|

|

Check if this is the final Form 1041 for the estate or trust |

||

|

|

|||

Part II Information About the Beneficiary

FBeneficiary's identifying number

GBeneficiary's name, address, city, state, and ZIP code

H |

|

Domestic beneficiary |

|

Foreign beneficiary |

|

|

|

|

|

|

|

661117 |

|

|

Final |

|

Amended |

OMB No. |

||

|

Part III |

|

Beneficiary’s Share of Current Year Income, |

||||

|

|

|

|

Deductions, Credits, and Other Items |

|||

1 |

Interest income |

11 |

Final year deductions |

||||

|

|

|

|

|

|||

2a |

Ordinary dividends |

|

|

|

|||

|

|

|

|

|

|||

2b |

Qualified dividends |

|

|

|

|||

3Net

4a |

Net |

|

4b |

28% rate gain |

12 Alternative minimum tax adjustment |

|

|

|

4c |

Unrecaptured section 1250 gain |

|

5Other portfolio and nonbusiness income

6Ordinary business income

7Net rental real estate income

13 Credits and credit recapture

8Other rental income

9Directly apportioned deductions

14 Other information

10Estate tax deduction

*See attached statement for additional information.

Note: A statement must be attached showing the beneficiary’s share of income and directly apportioned deductions from each business, rental real estate, and other rental activity.

For IRS Use Only

For Paperwork Reduction Act Notice, see the Instructions for Form 1041. |

www.irs.gov/Form1041 |

Cat. No. 11380D |

Schedule |

Schedule |

Page 2 |

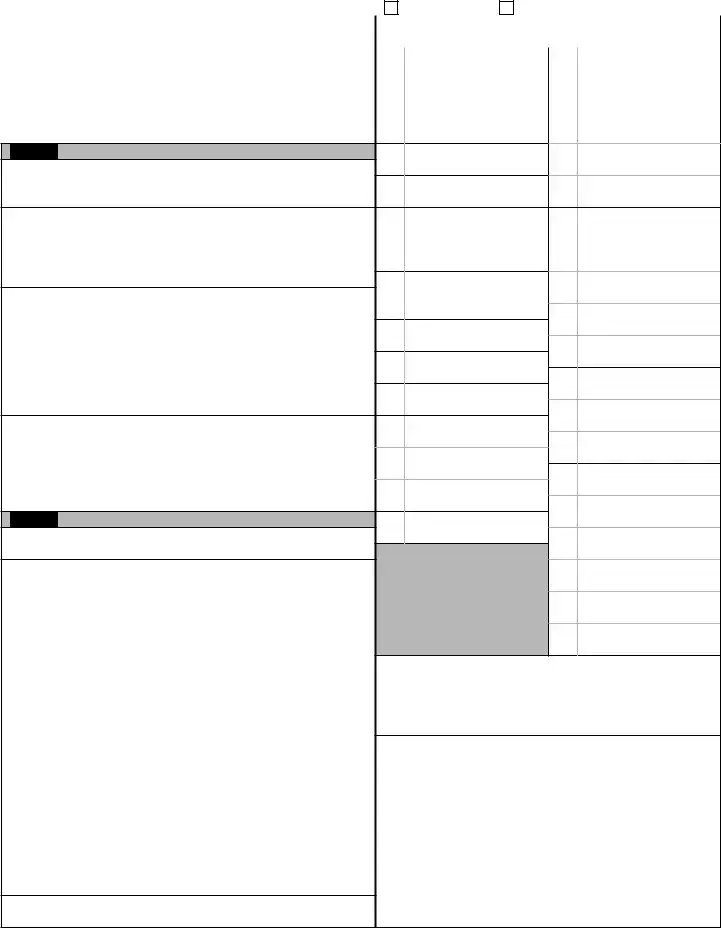

This list identifies the codes used on Schedule

Report on

Form 1040 or

Form 1040 or

Form 1040 or

Schedule D, line 5

Schedule D, line 12

28% Rate Gain Worksheet, line 4 (Schedule D Instructions)

Unrecaptured Section 1250 Gain

Worksheet, line 11 (Schedule D

Instructions)

Schedule E, line 33, column (f)

Schedule E, line 33, column (d) or (f)

Schedule E, line 33, column (d) or (f)

Schedule E, line 33, column (d) or (f)

9. Directly apportioned deductions |

|

|

Code |

|

|

A Depreciation |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

B Depletion |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

C Amortization |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

10. Estate tax deduction |

Schedule A, line 16 |

|

11. Final year deductions |

|

|

A Excess deductions |

See the beneficiary's instructions |

|

B |

Schedule D, line 5 |

|

C |

Schedule D, line 12; line 5 of the |

|

|

wksht. for Sch. D, line 18; and |

|

|

line 16 of the wksht. for Sch. D, |

|

|

line 19 |

|

D Net operating loss carryover — |

Form 1040 or |

|

regular tax |

1, line 8 |

|

E Net operating loss carryover — |

Form 6251, line 2f |

|

minimum tax |

} |

|

12. Alternative minimum tax (AMT) items |

|

|

A Adjustment for minimum tax purposes |

Form 6251, line 2j |

|

B AMT adjustment attributable to |

|

|

qualified dividends |

|

|

C AMT adjustment attributable to |

|

|

net |

|

|

D AMT adjustment attributable to |

|

|

net |

|

See the beneficiary’s |

|

|

|

E AMT adjustment attributable to |

|

instructions and the |

unrecaptured section 1250 gain |

|

Instructions for Form 6251 |

F AMT adjustment attributable to 28% rate gain

G Accelerated depreciation

HDepletion

IAmortization

J Exclusion items |

2020 Form 8801 |

|

Code |

|

|

Report on |

|

A Credit for estimated taxes |

|

|

Form 1040 or |

|

|

|

|

3, line 8 |

|

B Credit for backup withholding |

|

|

Form 1040 or |

|

C |

|

|

|

|

D Rehabilitation credit and energy credit |

|

|

|

|

E Other qualifying investment credit |

|

|

|

|

F Work opportunity credit |

|

|

|

|

G Credit for small employer health |

|

|

|

|

insurance premiums |

|

|

|

|

H Biofuel producer credit |

|

|

|

|

I Credit for increasing research activities |

|

|

|

|

J Renewable electricity, refined coal, |

|

|

|

|

and Indian coal production credit |

|

|

|

|

K Empowerment zone employment credit |

See the beneficiary’s instructions |

||

|

L Indian employment credit |

|

}Form 1040 or |

|

|

M Orphan drug credit |

|

||

|

N Credit for |

|||

|

care and facilities |

|

||

|

O Biodiesel and renewable diesel |

fuels |

||

|

credit |

|

||

|

P Credit to holders of tax credit bonds |

|||

|

Q Credit for employer differential wage |

|||

|

payments |

|

||

|

R Recapture of credits |

|

||

|

Z Other credits |

|

||

14. |

Other information |

|

||

A |

|

|||

|

B Foreign taxes |

|

|

Form 1040 or |

|

|

|

|

3, line 1 or Sch. A, line 6 |

|

C Reserved |

|

|

|

|

D Reserved |

|

|

|

|

E Net investment income |

|

|

Form 4952, line 4a |

|

F Gross farm and fishing income |

|

|

Schedule E, line 42 |

|

G Foreign trading gross receipts |

|

|

See the Instructions for |

|

(IRC 942(a)) |

|

|

Form 8873 |

|

H Adjustment for section 1411 net |

|

|

Form 8960, line 7 (also see the |

|

investment income or deductions |

|

beneficiary's instructions) |

|

|

I Section 199A information |

|

|

See the beneficiary’s instructions |

|

Z Other information |

|

|

See the beneficiary’s instructions |

|

|

|

|

|

Note: If you are a beneficiary who does not file a Form 1040 or 1040- SR, see instructions for the type of income tax return you are filing.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule K-1 (Form 1041) is used to report income, deductions, and credits from an estate or trust to its beneficiaries. |

| Filing Requirement | Estates and trusts must complete Schedule K-1 if they have distributions to beneficiaries during the tax year. |

| Beneficiary Information | Each beneficiary receives their own K-1 detailing their share of the estate's or trust's income and deductions. |

| Tax Implications | The income reported on a K-1 is taxed at the beneficiary's individual tax rate, which may vary based on their overall income. |

After receiving your IRS Schedule K-1 (Form 1041), it’s essential to complete it accurately to ensure compliance with tax regulations. This form reports income, deductions, and credits from estates or trusts that you may have been a beneficiary of. Completing this form may seem daunting, but following these detailed steps can streamline the process.

What is the IRS Schedule K-1 (Form 1041)?

The IRS Schedule K-1 (Form 1041) is a tax document used by estates and trusts to report income, deductions, and credits to beneficiaries. Each beneficiary receives a K-1 form that details their share of the estate's or trust's taxable income and other relevant tax information. This form is essential for beneficiaries to accurately report their income on their personal tax returns.

Who needs to file the Schedule K-1 (Form 1041)?

The fiduciary of an estate or trust must file the Schedule K-1 (Form 1041) for each beneficiary receiving distributions. The form provides the IRS with information about the beneficiary’s portion of the estate's or trust's income, ensuring that beneficiaries report their share on their tax returns.

When is the Schedule K-1 (Form 1041) due?

The completed Schedule K-1 (Form 1041) is due to beneficiaries when the fiduciary files the Form 1041 for the estate or trust. Typically, Form 1041 must be filed by the 15th day of the fourth month following the end of the tax year, which aligns with the due date for the K-1 forms.

How do beneficiaries report income from Schedule K-1 (Form 1041)?

Beneficiaries report the income, deductions, and credits listed on the Schedule K-1 (Form 1041) on their personal tax returns, usually on IRS Form 1040. Specific line items on the K-1 correspond to certain parts of the 1040 form, assisting beneficiaries in properly claiming their share of the estate's or trust's income.

What types of income are reported on Schedule K-1 (Form 1041)?

Common types of income reported on Schedule K-1 (Form 1041) include interest income, dividends, capital gains, and ordinary income. Each type is distinguished to help beneficiaries understand how it affects their overall tax liability. Different types of income may also be subject to varying tax rates.

What should I do if I believe the K-1 information is incorrect?

If you believe the information on your Schedule K-1 (Form 1041) is incorrect, contact the fiduciary or the person responsible for filing the estate or trust's taxes. It is crucial to address any discrepancies promptly, as incorrect information may lead to errors on your tax return.

What if I do not receive a Schedule K-1 (Form 1041) but should have?

If you believe you should receive a Schedule K-1 (Form 1041) but do not receive it, reach out to the fiduciary or trustee for clarification. Beneficiaries have a right to receive this document to accurately report their income and ensure compliance with tax laws.

Are there any special tax implications for receiving income through Schedule K-1 (Form 1041)?

Yes, beneficiaries may have special tax implications for income received via Schedule K-1 (Form 1041). This income may affect your overall taxable income and potentially push you into a higher tax bracket. It’s important to consult with a tax professional to understand the full impact and any strategies for tax planning.

Can I e-file my tax return if I receive a Schedule K-1 (Form 1041)?

Yes, you can e-file your tax return while including the income reported on your Schedule K-1 (Form 1041). Most e-filing software accommodates K-1 forms, making it easier for beneficiaries to accurately report their income. Just ensure the figures from the K-1 are correctly entered into the appropriate fields during the e-filing process.

Omitting Necessary Information: One common mistake is failing to include all required information on the Schedule K-1. This can include missing names, addresses, or Social Security numbers. Each detail is critical, and an incomplete form may lead to delays or issues with the IRS.

Incorrect Tax Year: Another error is using the wrong tax year. Schedule K-1 is specific to the tax year in which the income or deduction occurs. Double-checking the year before submitting can prevent complications.

Misclassifying Income: People sometimes misclassify the type of income received. For example, different types of income, like dividends or capital gains, may have varying tax implications. Take time to accurately categorize each income source.

Failing to Distribute Income Accurately: Distributing income among beneficiaries can lead to errors if not done correctly. Each beneficiary must report their share accurately. Failing to do this may result in discrepancies that could raise red flags with the IRS.

Not Keeping Copies of the Form: Lastly, neglecting to keep a copy of the completed form for personal records is a mistake many make. Retaining a copy is essential for future reference or if any questions arise from the IRS.

The IRS Schedule K-1 (Form 1041) is used to report income, deductions, and credits from estates and trusts. When dealing with this form, there are several other documents that may be needed to provide a complete picture of the estate or trust’s financial situation. Below is a list of relevant forms and documents often associated with Schedule K-1.

Understanding these forms and documents can help clarify the financial landscape surrounding estates and trusts. Proper documentation ensures that all parties fulfill their tax obligations accurately and efficiently.

The IRS Schedule K-1 (Form 1041) is similar to the Schedule K-1 (Form 1065). Both documents report income, deductions, and credits from partnerships or trusts to their beneficiaries. The Schedule K-1 (Form 1065) is used specifically for partnerships, detailing each partner's share of the income, deductions, and credits. Meanwhile, the Schedule K-1 (Form 1041) serves the same purpose but in the context of estates and trusts. Both forms are essential for beneficiaries who need to report that income on their personal tax returns.

Another similar document is the Schedule K-1 (Form 1120S). This form provides information on the income and deductions passed on to shareholders of an S corporation. Similar to the K-1 from a trust, the S corporation version ensures that shareholders report their share of the corporation's income, credits, and deductions accurately. Both K-1 forms serve to pass through tax implications to the beneficiaries or shareholders, allowing them to account for their respective portions on their tax returns.

The IRS Form 1099-DIV also parallels the K-1 forms by reporting distributions to shareholders. While the Schedule K-1 outlines income and losses from trusts and partnerships, the 1099-DIV focuses explicitly on dividends from stocks and mutual funds. Investors receive this form when they earn dividends, helping them incorporate those amounts when filing their tax returns. Both documents fulfill the function of detailing income that taxpayers must report, but they apply to different financial contexts.

Form 1099-INT is another document that bears similarity to the K-1. This form is issued by banks and financial institutions to report interest income paid to account holders. Just like the K-1, the 1099-INT informs taxpayers about income they need to report to the IRS. While the K-1 relates primarily to entities like estates or partnerships, the 1099-INT strictly pertains to interest earned, but both forms enable taxpayers to accurately report their income.

Additionally, the Schedule A (Form 1040) can also be seen as somewhat similar. While it is not a K-1, it allows taxpayers to itemize deductions on their personal income tax returns. Beneficiaries receiving a Schedule K-1 may also find deductions that they can utilize on their Schedule A. Both documents play crucial roles in the overall tax return process, with K-1 detailing income and Schedule A focusing on allowable deductions, contributing to the taxpayer’s financial picture.

Last, the W-2 form is comparable to the Schedule K-1 in that both serve to declare income earned. Employers issue W-2 forms to employees to report wages, salaries, and other compensation, while the Schedule K-1 details income passed through from partnerships, S corporations, estates, or trusts. Both of these forms help ensure that individuals fulfill their tax obligations by accurately reporting income received during the tax year.

When filling out the IRS Schedule K-1 (Form 1041), careful attention to detail is essential. This form, used to report income, deductions, and credits for beneficiaries of estates or trusts, can be tricky. Here’s a guide on key dos and don’ts to ensure compliance and accuracy.

Following these guidelines can significantly reduce the likelihood of errors and ensure a smoother tax filing process. Take the time necessary to complete the Schedule K-1 accurately and responsibly.

Understanding the IRS Schedule K-1 (Form 1041) can be challenging, and several misconceptions can lead to confusion. Here are six common misunderstandings about this financial document:

This form is often associated with estates and trusts, which may lead to the belief that only affluent individuals deal with it. However, anyone who has received income from a partnership, trust, or estate must be aware of this form.

While income reported on a K-1 is taxable, it doesn't necessarily require immediate payment; tax liability depends on overall financial circumstances and other reported income. It's best to consult with a tax professional.

This is not entirely accurate. In addition to beneficiaries, partners in a partnership also receive K-1 forms reflecting their share of the earnings or losses.

In fact, the K-1 is prepared by the entity, whether it’s a partnership or fiduciary, that is responsible for issuing it. The recipient’s role is to review the form and ensure they report it correctly on their tax return.

While it is possible to amend a return, it can be tedious and may even incur penalties if tax liability changes. It's crucial to ensure the K-1 is accurate before filing.

This can be misleading. While it’s true that K-1 forms typically do not have tax withheld, partners or beneficiaries may still need to make estimated tax payments if the income reported significantly affects their tax liability.

Understanding the IRS Schedule K-1 (Form 1041) is essential for beneficiaries and fiduciaries alike. Here are some key takeaways about this important tax form:

Being familiar with the Schedule K-1 process can ease the tax filing experience for everyone involved. It is a good practice to seek assistance from a tax professional if you find any part of the process confusing.