The IRS Schedule D is a crucial component of the tax filing process for many individuals, particularly those engaging in the buying and selling of stocks, bonds, and other investments. It allows taxpayers to report capital gains and losses from their investment activities, helping to determine their overall tax liability. This form is typically filed alongside the main 1040 or 1040-SR income tax forms, ensuring that the income from investments is accurately reflected in one's tax calculations. Various sections of Schedule D guide individuals through reporting short-term versus long-term capital gains, with distinctions made based on how long an asset was held before selling. Deductions and credits can also be claimed here, potentially reducing the amount of taxable income. Importantly, correctly completing this form helps ensure compliance with IRS regulations and can even affect future investment decisions. For those navigating the complexities of investments and taxes, understanding Schedule D is essential for making informed financial choices.

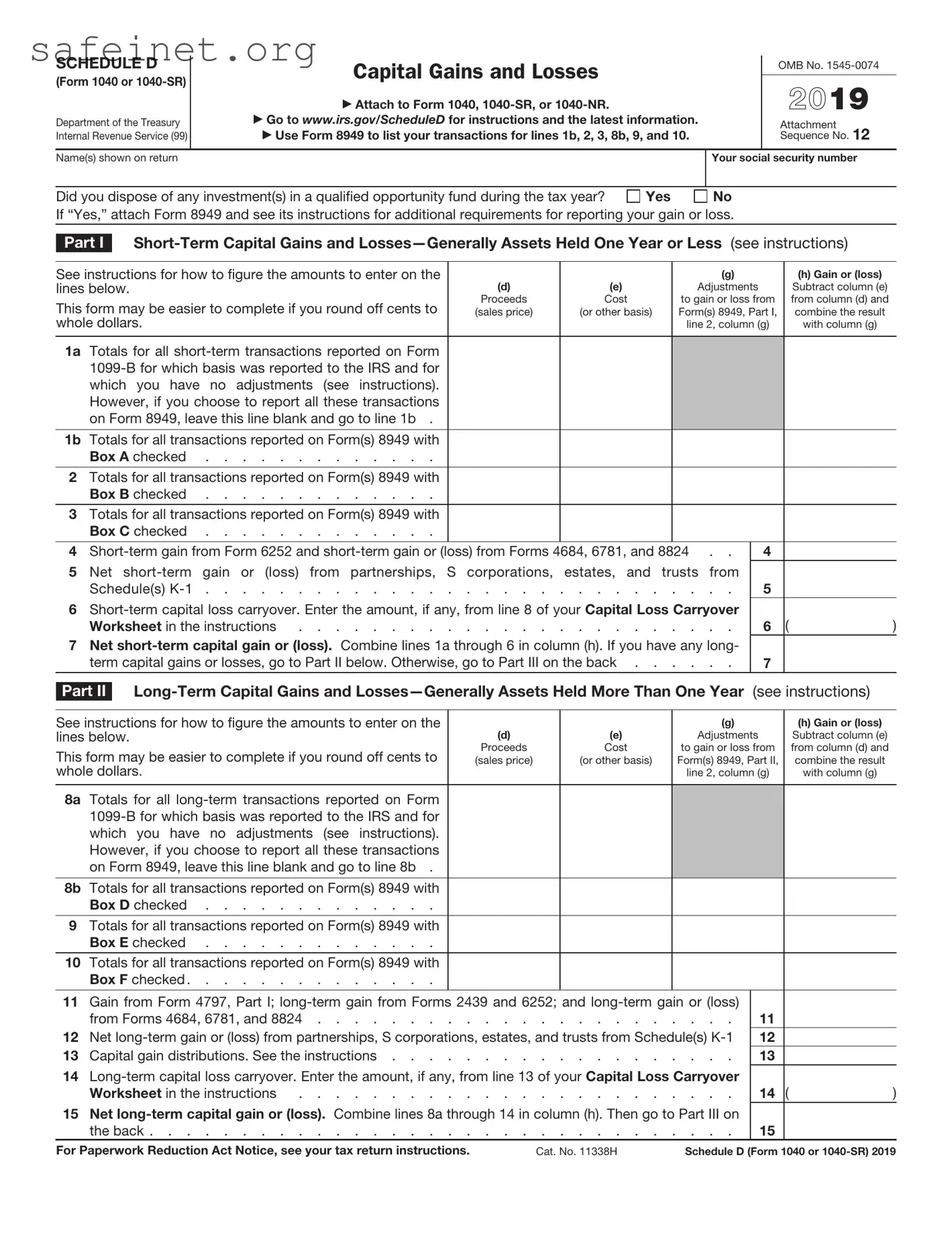

SCHEDULE D |

Capital Gains and Losses |

|

|

|

|

OMB No. |

|||||||

(Form 1040 or |

|

|

|

|

|

2019 |

|||||||

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Attach to Form 1040, |

|

|

|

|

|

||||

Department of the Treasury |

Go to www.irs.gov/ScheduleD for instructions and the latest information. |

|

|

|

Attachment |

12 |

|||||||

Internal Revenue Service (99) |

Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10. |

|

|

|

Sequence No. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||

Name(s) shown on return |

|

|

|

|

|

Your social security number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||

Did you dispose of any investment(s) in a qualified opportunity fund during the tax year? |

Yes |

|

No |

|

|

|

|||||||

If “Yes,” attach Form 8949 and see its instructions for additional requirements for reporting your gain or loss. |

|

|

|

||||||||||

|

|

|

|

|

|

||||||||

Part I |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions for how to figure the amounts to enter on the |

|

|

|

|

(g) |

|

(h) Gain or (loss) |

||||||

lines below. |

|

|

(d) |

(e) |

|

Adjustments |

|

Subtract column (e) |

|||||

This form may be easier to complete if you round off cents to |

Proceeds |

Cost |

|

to gain or loss from |

from column (d) and |

||||||||

(sales price) |

(or other basis) |

Form(s) 8949, Part I, |

combine the result |

||||||||||

whole dollars. |

|

|

|

|

line 2, column (g) |

with column (g) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

1a |

Totals for all |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

which you have no adjustments (see instructions). |

|

|

|

|

|

|

|

|

|

|||

|

However, if you choose to report all these transactions |

|

|

|

|

|

|

|

|

|

|||

|

on Form 8949, leave this line blank and go to line 1b . |

|

|

|

|

|

|

|

|

|

|||

1b |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box A checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

2 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box B checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box C checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

4 |

. . |

|

4 |

|

|

||||||||

5 |

Net |

from |

|

|

|

|

|||||||

|

Schedule(s) |

. |

. . |

|

5 |

|

|

||||||

6 |

|

|

( |

) |

|||||||||

|

Worksheet in the instructions |

. |

. . |

|

6 |

||||||||

7 |

Net |

|

|

|

|

||||||||

|

term capital gains or losses, go to Part II below. Otherwise, go to Part III on the back . . . |

. |

. . |

|

7 |

|

|

||||||

|

|

|

|||||||||||

Part II |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions for how to figure the amounts to enter on the |

|

|

|

|

(g) |

|

(h) Gain or (loss) |

||||||

lines below. |

|

|

(d) |

(e) |

|

Adjustments |

|

Subtract column (e) |

|||||

This form may be easier to complete if you round off cents to |

Proceeds |

Cost |

|

to gain or loss from |

from column (d) and |

||||||||

(sales price) |

(or other basis) |

Form(s) 8949, Part II, |

combine the result |

||||||||||

whole dollars. |

|

|

|

|

line 2, column (g) |

with column (g) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

8a |

Totals for all |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

which you have no adjustments (see instructions). |

|

|

|

|

|

|

|

|

|

|||

|

However, if you choose to report all these transactions |

|

|

|

|

|

|

|

|

|

|||

|

on Form 8949, leave this line blank and go to line 8b . |

|

|

|

|

|

|

|

|

|

|||

8b |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box D checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

9 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box E checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

10 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box F checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11Gain from Form 4797, Part I;

|

from Forms 4684, 6781, and 8824 |

11 |

12 |

Net |

12 |

13 |

Capital gain distributions. See the instructions |

13 |

14

Worksheet in the instructions |

14 ( |

) |

15Net

the back |

15 |

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 11338H |

Schedule D (Form 1040 or |

Schedule D (Form 1040 or |

Page 2 |

|

|

Summary |

|

Part III |

|

|

16 Combine lines 7 and 15 and enter the result . . . . . . . . . . . . . . . . . .

•If line 16 is a gain, enter the amount from line 16 on Form 1040 or

•If line 16 is a loss, skip lines 17 through 20 below. Then go to line 21. Also be sure to complete line 22.

•If line 16 is zero, skip lines 17 through 21 below and enter

17Are lines 15 and 16 both gains?

Yes. Go to line 18.

No. Skip lines 18 through 21, and go to line 22.

18If you are required to complete the 28% Rate Gain Worksheet (see instructions), enter the

amount, if any, from line 7 of that worksheet . . . . . . . . . . . . . . . . .

19 If you are required to complete the Unrecaptured Section 1250 Gain Worksheet (see instructions), enter the amount, if any, from line 18 of that worksheet . . . . . . . . .

20Are lines 18 and 19 both zero or blank?

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

No. Complete the Schedule D Tax Worksheet in the instructions. Don’t complete lines 21 and 22 below.

No. Complete the Schedule D Tax Worksheet in the instructions. Don’t complete lines 21 and 22 below.

21If line 16 is a loss, enter here and on Form 1040 or

• The loss on line 16; or |

} |

• ($3,000), or if married filing separately, ($1,500) |

Note: When figuring which amount is smaller, treat both amounts as positive numbers.

22Do you have qualified dividends on Form 1040 or

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

16

18

19

21 ( |

) |

No. Complete the rest of Form 1040,

Schedule D (Form 1040 or

| Fact Name | Description |

|---|---|

| Purpose of Schedule D | Schedule D is used to report capital gains and losses from the sale of assets, such as stocks and real estate. |

| Who should file | Any taxpayer who has sold assets during the tax year must complete Schedule D to report their capital transactions. |

| Long-Term vs. Short-Term | Schedule D differentiates between long-term and short-term capital gains and losses, depending on how long the asset was held. |

| Tax Rate Changes | Capital gains are taxed differently based on the asset's holding period, with long-term gains typically enjoying lower tax rates. |

| Carryover Losses | Taxpayers can carry over any unused capital losses to future years, which may help offset gains in those years. |

| Filing Mechanism | Schedule D must be attached to Form 1040 or Form 1040-SR when filed with the IRS, providing a complete overview of capital transactions. |

| State Tax Implications | Many states also require the reporting of capital gains on state tax returns, governed by individual state laws. |

| Electronic Filing | Schedule D can be filed electronically using tax preparation software, which simplifies calculations and the filing process. |

| Form Updates | Schedule D may be updated annually; it’s essential to use the correct version corresponding to the tax year being filed. |

| Special Situations | Some transactions, such as those related to cryptocurrency or collectibles, have specific reporting requirements on Schedule D. |

After gathering all necessary information about your capital gains and losses, it’s time to fill out the IRS Schedule D form. This form is essential for reporting how much you owe or are entitled to receive back from the IRS. Completing it accurately ensures that you are in good standing with the IRS and that you take advantage of any eligible deductions.

What is IRS Schedule D?

IRS Schedule D is a form used to report capital gains and losses from the sale of assets such as stocks, bonds, and real estate. The information on this schedule helps to determine your overall tax liability on these transactions. Both Form 1040 and Form 1040-SR can include Schedule D when applicable. Completing this form accurately is crucial because it affects your taxable income due to the nature of capital gains and losses.

Who needs to file Schedule D?

Individuals who have sold capital assets or received capital gains must file Schedule D. This includes those who made money from the sale of stocks, bonds, or real estate. Even if a taxpayer has losses, it is important to report them, as they can offset gains and potentially reduce taxable income. Anyone who has sold assets during the tax year should review their situation to determine if filing Schedule D is necessary.

How do I report capital gains and losses on Schedule D?

To report capital gains and losses on Schedule D, start by listing each transaction on a worksheet. Gather information such as the date of acquisition, the date of sale, the sale price, the cost basis, and any related expenses. Once you have compiled this information, fill out the relevant sections of Schedule D, including Part I for short-term transactions and Part II for long-term transactions. After completing these sections, transfer the totals to Form 1040 or 1040-SR. If applicable, you may also include Form 8949 for detailed transaction reporting.

What are the tax implications of capital gains reported on Schedule D?

Capital gains can be subject to different tax rates based on how long the asset was held. Short-term gains, for assets held one year or less, are taxed at ordinary income tax rates. Long-term gains, for assets held longer than one year, benefit from lower rates, typically ranging from 0% to 20%, depending on your income level. Properly reporting capital gains and losses on Schedule D ensures compliance with tax laws and can help optimize your tax situation, potentially reducing your overall tax burden.

Failure to report all sales. Omitting any stock or asset sales can lead to discrepancies with the IRS. Ensure every transaction is documented.

Incorrectly calculating gains and losses. Miscalculations can occur especially with adjustments for costs like commissions or fees.

Neglecting to account for wash sales. If you sell a stock and repurchase it within 30 days, you may have a wash sale, affecting your reported gains or losses.

Using outdated cost basis information. Ensure you have the correct historical purchase price for assets to calculate accurate gains and losses.

Not utilizing the proper form. Schedule D is typically used with Form 1040 and should not be confused with other forms.

Overlooking foreign transactions. If you've sold foreign investments or assets, ensure those transactions are reported correctly to avoid legal issues.

Failing to report cryptocurrency transactions. As cryptocurrency gains and losses need to be reported, do not forget these when filling out Schedule D.

Inconsistent reporting. Make sure that the gains and losses reported on Schedule D match those on your brokerage statements. Discrepancies may raise red flags.

Ignoring state requirements. Some states have specific forms or requirements for reporting sales, which should not be overlooked.

Substituting taxpayer identification numbers. Use the correct Social Security number for accuracy. An error here can lead to complications with your tax return.

The IRS Schedule D is an important form for reporting capital gains and losses. Individuals who have sold investments, such as stocks or real estate, will need to utilize this form to accurately report their earnings or losses from these transactions. Often, other supporting documents are required to provide a comprehensive view of a taxpayer's financial situation. Here are four commonly used forms that may accompany Schedule D.

Understanding these accompanying documents can greatly benefit taxpayers by ensuring a complete and accurate depiction of their financial activities. Proper documentation aids in minimizing audit risks and maximizing potential tax benefits. If you're navigating capital gains and losses, familiarizing yourself with these forms will help you stay organized and informed throughout the tax filing process.

The Schedule D of Form 1040 or 1040-SR is akin to a personal financial statement, which is often prepared to provide a snapshot of an individual’s financial position. Like Schedule D, a personal financial statement includes details about assets and liabilities, allowing individuals to gauge their financial health. Both documents require individuals to compile information about investments, reflecting gains and losses that may influence overall financial stability.

Investment income tax forms, such as the 1099-DIV, share similarities with Schedule D because they report specific types of income derived from investments. The 1099-DIV provides information about dividends and distributions, which directly ties into the capital gains and losses reported on Schedule D. This relationship helps taxpayers consolidate their investment income and assess their overall tax liability related to investments.

Another document comparable to Schedule D is the IRS Form 8949, which is used to report sales and other dispositions of capital assets. Taxpayers list individual transactions on Form 8949, detailing proceeds and costs associated with sales of assets. Schedule D summarizes these transactions, often incorporating totals from Form 8949, to present the overall capital gain or loss for the tax year.

In terms of reporting stocks and securities, the IRS Form 4797 is relevant as it addresses the sale of business property, including stocks held by business owners. Like Schedule D, Form 4797 demands accurate reporting of gains and losses from the sale of assets. Both forms involve recognizing the financial implications of asset sales for the purpose of tax reporting.

The IRS Form 8862 can also be compared to Schedule D in that both documents involve claiming entitlements related to past tax events. While Form 8862 is necessary for taxpayers trying to reclaim the Earned Income Tax Credit after it was denied previously, the Schedule D may also be used by taxpayers who have held onto capital assets for extended periods, impacting the credit they might access based on prior losses or gains.

Likewise, the tax credit forms, such as the Child and Dependent Care Expenses Credit form (Form 2441), could be seen as somewhat comparable to Schedule D. While not directly related to capital assets, both involve compiling and reporting financial information relevant for tax credits. They each require individuals to consider different aspects of their financial circumstances that may lead to reduced tax liability.

Scholarship applications can resemble Schedule D, as both documents require careful and thoughtful reporting of income sources. When applying for scholarships, students often need to disclose information about their family's financial situation. Similarly, Schedule D requires taxpayers to report their financial activities, revealing insights that might impact eligibility for financial aid or other programs.

Additionally, the annual income tax return Form W-2 has a similarity with Schedule D, given that both contribute to the overall understanding of taxable income. Form W-2 reports earnings from employment, while Schedule D accounts for capital gains or losses. The accurate aggregation of both forms helps ensure that individuals meet their tax obligations effectively.

Lastly, the IRS Form 1040-X, used for amending tax returns, can be related to Schedule D, as it can be utilized to correct any errors involving capital gain or loss reporting. Individuals must ensure that all financial transactions are accurately reported, and any adjustments made on Form 1040-X will often stem from discrepancies identified on the Schedule D, making both essential for providing a true and accurate representation of one’s tax situation.

When completing the IRS Schedule D (Form 1040 or 1040-SR), it is essential to adhere to certain guidelines to ensure accuracy and compliance. Below is a list of things to do and not do when filling out this form.

Things You Should Do:

Things You Shouldn't Do:

Understanding IRS forms can be challenging, and misconceptions abound regarding the Schedule D of the 1040 or 1040-SR forms. Here are six common misunderstandings:

Understanding these misconceptions can help taxpayers navigate their reporting obligations more effectively, ensuring compliance with IRS regulations and potentially optimizing tax liabilities.

When it comes to reporting capital gains and losses on your individual income tax return, IRS Schedule D (Form 1040 or 1040-SR) is essential. Here are some key takeaways to help you understand how to fill it out and use it effectively:

By keeping these points in mind, taxpayers can navigate the complexities of Schedule D with greater confidence, ensuring compliance and potentially reducing their tax burden.