The IRS Schedule B (Form 941) plays a crucial role in the payroll tax reporting process for employers in the United States. This form is specifically designed to report the employer's share of Social Security and Medicare taxes, as well as federal income tax withheld from employee wages. Employers must file this form quarterly, alongside Form 941, to ensure compliance with federal tax regulations. Schedule B requires detailed information regarding the total wages paid, the number of employees, and the amount of taxes withheld during the reporting period. Additionally, it includes a section for employers to report any adjustments to their tax liabilities. Accurate completion of Schedule B is essential, as it helps the IRS track payroll tax obligations and prevents potential penalties for underreporting or misreporting. Understanding the nuances of this form is vital for employers to maintain good standing with tax authorities and to ensure proper tax management within their organizations.

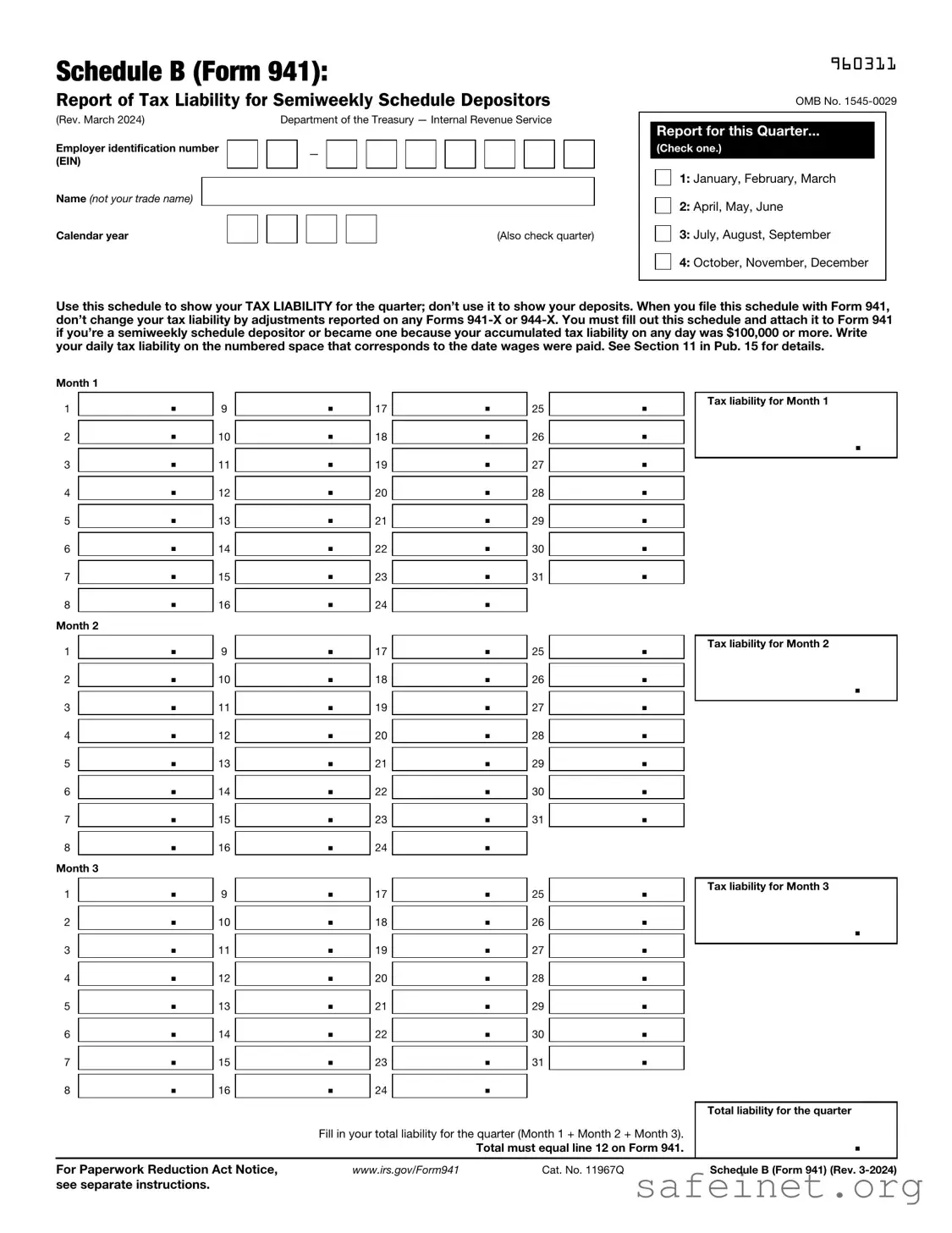

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. March 2024) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don’t use it to show your deposits. When you file this schedule with Form 941, don’t change your tax liability by adjustments reported on any Forms

Month 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 1 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 2 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3). |

|

. |

|||||||

|

|

|

|

|

|

|

|

|

Total must equal line 12 on Form 941. |

|

||||

For Paperwork Reduction Act Notice, |

|

www.irs.gov/Form941 |

|

Cat. No. 11967Q |

|

|

Schedule B (Form 941) (Rev. |

|||||||

see separate instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule B (Form 941) is used to report the amount of federal income tax withheld from employees' wages. |

| Filing Frequency | This form is typically filed quarterly, along with Form 941. |

| Who Must File | Employers who withhold federal income tax from employees must file this form. |

| State-Specific Forms | Some states have their own versions of this form, governed by state tax laws. |

| Due Dates | Forms are due on the last day of the month following the end of the quarter. |

| Penalties | Failure to file can result in penalties, including fines and interest on unpaid taxes. |

| Record Keeping | Employers must keep records for at least four years to support the information reported on the form. |

| Electronic Filing | Employers can file electronically, which is often faster and more efficient. |

Filling out the IRS Schedule B (Form 941) is an important task for employers. This form helps report the tax withheld from employees’ wages and the employer's share of Social Security and Medicare taxes. After completing the form, you will need to file it with the IRS as part of your quarterly tax obligations.

What is the IRS Schedule B (Form 941)?

The IRS Schedule B (Form 941) is a supplemental form that employers use to report their tax liabilities related to federal income tax withholding and Social Security and Medicare taxes. It's specifically designed for employers who have a payroll tax liability that exceeds $100,000 during a specific period. This form provides the IRS with detailed information about the employer's tax liabilities and helps ensure compliance with federal tax laws.

Who needs to file Schedule B (Form 941)?

Employers who meet certain criteria must file Schedule B. If your business has a payroll tax liability that exceeds $100,000 during a pay period, you are required to complete and submit this form along with your Form 941. This includes employers who have accumulated this liability in a calendar month. If your liability is below this threshold, you generally do not need to file Schedule B.

When is Schedule B (Form 941) due?

Schedule B must be filed at the same time as your Form 941. Typically, Form 941 is due on the last day of the month following the end of the quarter. For example, if you are reporting for the first quarter (January to March), your Form 941, along with Schedule B, is due by April 30. It’s important to keep these deadlines in mind to avoid penalties for late filing.

How do I fill out Schedule B (Form 941)?

Filling out Schedule B involves reporting your payroll tax liabilities for each pay period within the quarter. You’ll need to provide information such as the dates of your pay periods and the total taxes withheld for each period. Make sure to double-check your calculations to ensure accuracy. If you're unsure about any part of the form, consider consulting a tax professional for assistance.

Incorrect Employer Identification Number (EIN): Failing to enter the correct EIN can lead to processing delays and potential penalties.

Missing Signature: Not signing the form can result in the IRS rejecting the submission. Always ensure the form is signed by an authorized individual.

Incorrect Tax Period: Filling in the wrong tax period can cause confusion and may lead to incorrect tax calculations. Double-check the dates before submission.

Failure to Report All Employees: Omitting any employees from the report can lead to underreporting and possible penalties. Include all eligible employees.

Errors in Calculating Tax Liability: Miscalculating the amounts owed can result in either underpayment or overpayment. Review calculations carefully.

Not Keeping a Copy: Failing to retain a copy of the submitted form can complicate future inquiries or audits. Always keep a copy for your records.

The IRS Schedule B (Form 941) is a crucial document for employers to report their payroll tax liabilities. Along with this form, there are several other documents that play an important role in ensuring compliance with tax regulations. Below is a list of commonly used forms and documents that accompany the Schedule B.

These documents collectively ensure that employers meet their tax obligations and maintain accurate records. Proper management of these forms helps avoid penalties and fosters a transparent relationship with tax authorities.

The IRS Schedule B (Form 941) is closely related to Form 940, which is the Employer's Annual Federal Unemployment (FUTA) Tax Return. Both forms are essential for employers, but they serve different purposes. While Form 941 is used to report income taxes, Social Security tax, and Medicare tax withheld from employee wages, Form 940 focuses solely on unemployment taxes. Employers must file both forms to ensure compliance with federal tax obligations, especially regarding employee wages and unemployment insurance.

Another document similar to Schedule B is Form 944. This form is the Employer's Annual Federal Tax Return for Small Businesses. Like Schedule B, Form 944 is used by employers to report withheld taxes, but it is designed for smaller businesses with lower payroll amounts. Instead of filing quarterly like Form 941, eligible employers can file Form 944 once a year, simplifying the reporting process for those with less frequent payroll.

Form W-2 is another important document in the realm of employee tax reporting. Employers use this form to report wages paid to employees and the taxes withheld from those wages. While Schedule B focuses on the employer's responsibilities for federal tax reporting, Form W-2 provides a summary of the employee's earnings and tax contributions for the year. Both documents are vital for ensuring accurate tax reporting to the IRS.

Form W-3, the Transmittal of Wage and Tax Statements, complements Form W-2. Employers submit Form W-3 to summarize all W-2 forms they have issued for a given year. This document provides the IRS with a consolidated view of the total wages and taxes withheld, similar to how Schedule B summarizes the employer's tax liabilities for each quarter.

Form 1099-MISC is another document that shares similarities with Schedule B. While Schedule B deals with employee wages, Form 1099-MISC is used to report payments made to independent contractors and other non-employee compensation. Both forms are crucial for tax reporting, ensuring that all types of income are accurately reported to the IRS, although they apply to different categories of workers.

Form 1096 is a summary form that accompanies certain information returns, including Form 1099-MISC. Similar to Schedule B, which summarizes tax liabilities, Form 1096 provides the IRS with a summary of all 1099 forms submitted by an employer. This helps the IRS track payments made to non-employees and ensures proper reporting of income.

Lastly, Form 720 is the Quarterly Federal Excise Tax Return. While it serves a different purpose—reporting excise taxes on specific goods and services—its quarterly nature aligns it with Schedule B. Both forms require regular filing, ensuring that the IRS receives timely information regarding the taxes owed by businesses, whether they pertain to employee wages or specific excise taxes.

When filling out the IRS Schedule B 941 form, it's important to be careful and thorough. Here are some dos and don'ts to keep in mind:

Understanding IRS forms can be challenging. Schedule B (Form 941) is no exception. Here are six common misconceptions about this form:

Being informed about these misconceptions can help you navigate your tax responsibilities more effectively. Always consult a tax professional for personalized advice.

Here are key takeaways regarding the IRS Schedule B 941 form: