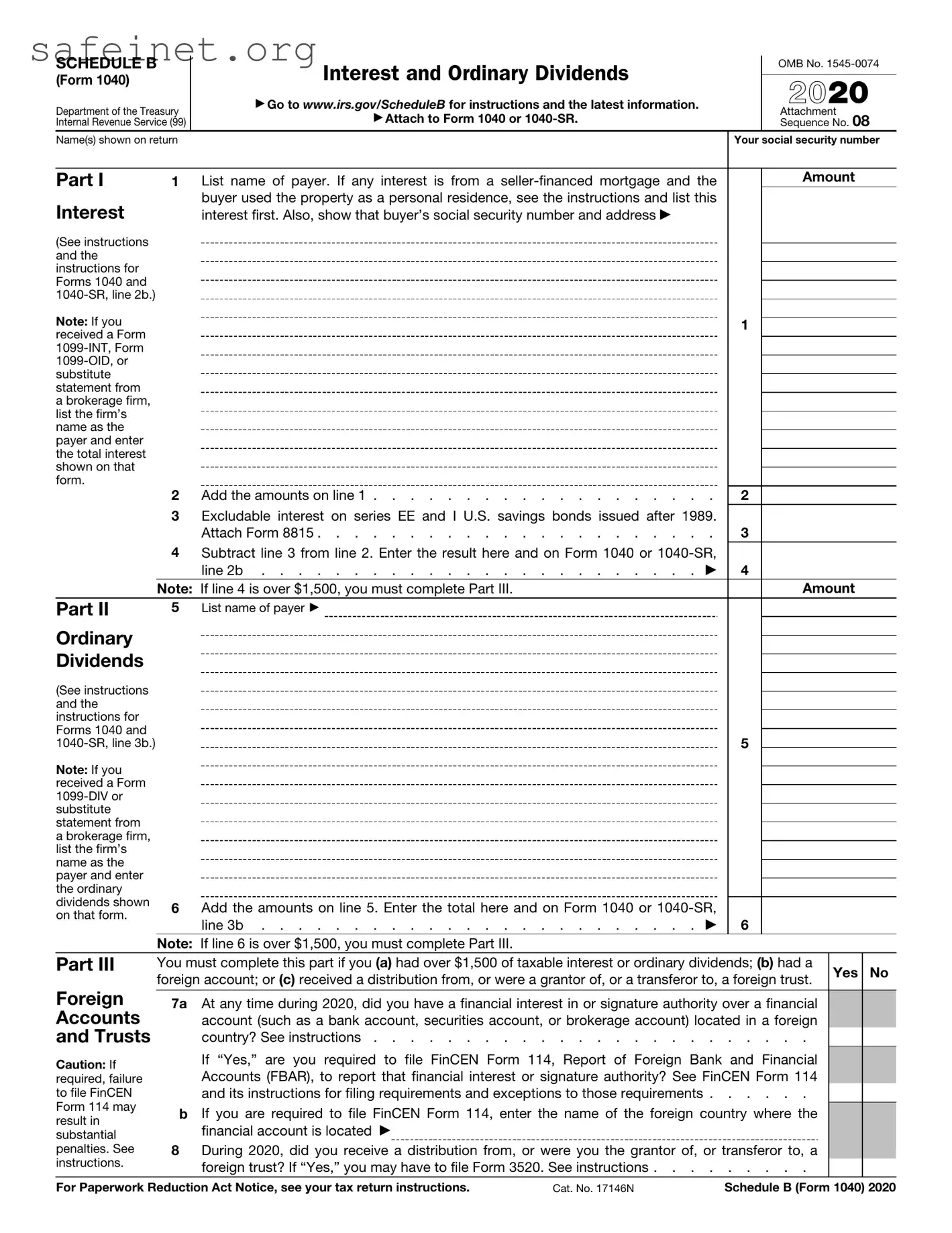

The IRS Schedule B form is an essential part of the 1040 tax return for many individuals. It primarily deals with interest and dividend income, providing a clear overview of your earnings from these sources. If you have received taxable interest or dividends during the tax year, completing Schedule B is often necessary. This form helps the IRS understand your financial activities, ensuring that all income is accurately reported. Additionally, it requires you to disclose any foreign accounts you may hold, which is crucial for compliance with U.S. tax laws. By detailing this information, you not only comply with regulations but also help streamline your overall tax process. Understanding Schedule B can simplify filing and may assist in avoiding potential errors or audits down the line.

SCHEDULE B |

|

Interest and Ordinary Dividends |

|

OMB No. |

|

|

|||

(Form 1040) |

|

|

|

|

|

|

2020 |

||

Department of the Treasury |

▶ Go to www.irs.gov/ScheduleB for instructions and the latest information. |

|

||

▶ Attach to Form 1040 or |

|

Attachment |

||

Internal Revenue Service (99) |

|

Sequence No. 08 |

||

Name(s) shown on return |

|

Your social security number |

||

|

|

|

|

|

Part I |

1 |

List name of payer. If any interest is from a |

|

Amount |

Interest |

|

buyer used the property as a personal residence, see the instructions and list this |

|

|

|

interest first. Also, show that buyer’s social security number and address ▶ |

|

|

|

(See instructions |

|

|

|

|

|

|

|

|

|

and the |

|

|

|

|

instructions for |

|

|

|

|

Forms 1040 and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: If you |

|

|

1 |

|

|

|

|

||

received a Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

substitute |

|

|

|

|

|

|

|

|

|

statement from |

|

|

|

|

a brokerage firm, |

|

|

|

|

list the firm’s |

|

|

|

|

|

|

|

|

|

name as the |

|

|

|

|

|

|

|

|

|

payer and enter |

|

|

|

|

the total interest |

|

|

|

|

shown on that |

|

|

|

|

|

|

|

|

|

form. |

|

|

|

|

|

2 |

Add the amounts on line 1 |

2 |

|

3Excludable interest on series EE and I U.S. savings bonds issued after 1989.

Attach Form 8815 |

3 |

4Subtract line 3 from line 2. Enter the result here and on Form 1040 or

|

|

line 2b |

. . . . . . . . . . . . . |

. . . |

. ▶ |

4 |

|

|

|

|

Note: If line 4 is over $1,500, you must complete Part III. |

|

|

|

Amount |

||||

Part II |

5 |

List name of payer ▶ |

|

|

|

|

|

|

|

Ordinary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(See instructions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and the |

|

|

|

|

|

|

|

|

|

instructions for |

|

|

|

|

|

|

|

|

|

Forms 1040 and |

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

Note: If you |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

received a Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

substitute |

|

|

|

|

|

|

|

|

|

statement from |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a brokerage firm, |

|

|

|

|

|

|

|

|

|

list the firm’s |

|

|

|

|

|

|

|

|

|

name as the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

payer and enter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

the ordinary |

|

|

|

|

|

|

|

|

|

dividends shown |

6 |

Add the amounts on line 5. Enter the total here and on Form 1040 or |

|

|

|

|

|||

on that form. |

|

|

|

|

|||||

|

line 3b |

. . . . . . . . . . . . . |

. . . |

. ▶ |

6 |

|

|

|

|

|

|

|

|

|

|||||

|

Note: If line 6 is over $1,500, you must complete Part III. |

|

|

|

|

|

|

||

Part III |

You must complete this part if you (a) had over $1,500 of taxable interest or ordinary dividends; (b) had a |

Yes |

No |

||||||

|

foreign account; or (c) received a distribution from, or were a grantor of, or a transferor to, a foreign trust. |

||||||||

Foreign |

|

|

|||||||

7a |

At any time during 2020, did you have a financial interest in or signature authority over a financial |

|

|

||||||

Accounts |

|

account (such as a bank account, securities account, or brokerage account) located in a foreign |

|

|

|||||

and Trusts |

|

country? See instructions |

|

|

|||||

Caution: If |

|

If “Yes,” are you required |

to file FinCEN Form 114, Report of |

Foreign |

Bank |

and Financial |

|

|

|

|

Accounts (FBAR), to report that financial interest or signature authority? See FinCEN Form 114 |

|

|

||||||

required, failure |

|

|

|

||||||

to file FinCEN |

|

and its instructions for filing requirements and exceptions to those requirements |

|

|

|||||

Form 114 may |

b |

If you are required to file FinCEN Form 114, enter the name of the foreign country where the |

|

|

|||||

|

|

||||||||

result in |

|

|

|||||||

|

financial account is located |

▶ |

|

|

|

|

|

|

|

substantial |

|

|

|

|

|

|

|

||

penalties. See |

8 |

During 2020, did you receive a distribution from, or were you the grantor of, or transferor to, a |

|

|

|||||

instructions. |

|

foreign trust? If “Yes,” you may have to file Form 3520. See instructions |

|

|

|||||

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 17146N |

Schedule B (Form 1040) 2020 |

| Fact Name | Description |

|---|---|

| Purpose | Schedule B of Form 1040 is used to report interest and ordinary dividends earned during the tax year. |

| Filing Requirement | Taxpayers must complete Schedule B if they have more than $1,500 of interest or ordinary dividends or if they received interest from a foreign account. |

| Signature Requirement | Unlike other forms, Schedule B does not require a separate signature. Signing the Form 1040 serves as an acknowledgment of the information on Schedule B. |

| Foreign Accounts | Those with foreign bank accounts must disclose this information on Schedule B and may also need to comply with additional reporting requirements under the Foreign Account Tax Compliance Act (FATCA). |

| State-Specific Requirements | While Schedule B itself is a federal form, some states may have similar requirements. It's important to check the specific regulations in your state, as state tax laws vary widely. |

Filling out the IRS Schedule B 1040 form is an essential step in your tax return preparation, especially if you have certain types of income. After completing this form, you will provide additional details about your income sources on your main tax return. Below are the steps you need to follow to accurately complete the form.

What is the IRS Schedule B 1040 form?

The IRS Schedule B is a supplemental form that taxpayers use to report interest and ordinary dividends. It accompanies Form 1040, which is the main individual income tax return. If you have more than $1,500 in interest or dividends, or if you received these payments from a foreign source, you will need to complete Schedule B to provide the IRS with details. The purpose of this form is to ensure accurate reporting of income to ensure compliance with tax laws.

Who needs to fill out Schedule B?

You must complete Schedule B if your taxable interest or dividends exceed $1,500, or if you have foreign bank accounts or other foreign financial assets. Additionally, if you have received interest payments from a seller-financed mortgage, you will need to include them on this schedule. It’s important to review your financial records for any interest income that might require reporting, as failing to do so can lead to penalties.

How do I complete Schedule B?

Completing Schedule B involves providing details about your interest and dividends. Start by listing each source of interest income and the amount received in the appropriate sections. Then, similarly list each source of dividends. If you have foreign accounts, you’ll need to indicate this, as it may require additional disclosures or forms. Pay careful attention to accuracy. Errors can delay processing and result in penalties.

Where do I submit Schedule B?

Once you have completed Schedule B, you will attach it to your completed Form 1040 when you file your tax return. If you are filing electronically, the software you use will guide you through including Schedule B. Be sure to keep a copy for your records, as it contains important information that may be needed for future reference or audits.

What happens if I don’t file Schedule B when required?

If you are required to file Schedule B but neglect to do so, the IRS may impose penalties. Not reporting interest and dividends can lead to under-reported income, which might trigger an audit. Additionally, substantial penalties might accrue for each year you fail to file accurately. To avoid these complications, always check if your financial situation necessitates the inclusion of this form and file it accordingly.

Completing the IRS Schedule B (Form 1040) can be a straightforward task, but there are common pitfalls that many individuals encounter. Here is a list of five mistakes to avoid:

Every penny earned from interest and dividends must be reported. This includes amounts from bank accounts, investments, and other sources. Missing even a small amount can raise questions from the IRS.

The IRS requires disclosure of foreign bank accounts if the balance exceeds certain limits. Failing to accurately report these accounts can lead to significant penalties.

Interest income and qualified dividends are taxed differently. Ensure that each is reported correctly to avoid potential underpayment of taxes.

Any Form 1099 received must be carefully reviewed. Information on these forms should be transferred accurately to Schedule B. Omitting any details can cause discrepancies.

It might seem minor, but failing to sign and date the Schedule B can delay the processing of your tax return. Always double-check that this step is completed.

Taking the time to review these common mistakes can lead to a smoother filing process and peace of mind as you navigate your tax responsibilities.

The IRS Schedule B (Form 1040) is used to report interest and ordinary dividends. It helps taxpayers disclose income from these sources to the IRS. However, several other forms and documents frequently accompany this schedule, ensuring accurate reporting of all income and tax obligations. Below is a list of commonly associated documents.

Understanding these forms can help streamline the tax filing process and ensure that all income is accurately reported. Keeping these documents organized will ultimately lead to clearer reporting and may even prevent potential issues with the IRS in the future.

The IRS Form 1040 Schedule B is similar to the 1099 form series. Both documents are used to report income from sources other than traditional employment. For instance, if an individual receives interest, dividends, or any other type of income, they would typically report this on a 1099 form as well as on Schedule B. This helps ensure that all income is accounted for when filing taxes.

The W-2 form is another document related to income reporting. Unlike Schedule B, which focuses on income from investments, the W-2 is used to report wages and salaries earned from an employer. However, both forms are essential for accurately reporting an individual’s overall income. Workers use the W-2 to show their earnings, while Schedule B allows them to disclose additional income generated through investments.

The IRS Form 8889 is similar in that it deals with reporting income but is specifically used for Health Savings Accounts (HSAs). Individuals must report contributions and distributions related to their HSAs on this form, and if they earn any interest on those accounts, it would also be reported on Schedule B. Both forms play a role in ensuring transparency in financial matters related to health care.

The Schedule D form, which reports capital gains and losses, also shares similarities with Schedule B. Investors use both forms to report different types of income derived from investments. While Schedule B focuses on dividends and interest, Schedule D handles the sale of assets, emphasizing the comprehensive nature of reporting various income sources.

The Form 8606 is another document that resonates with Schedule B, particularly regarding certain tax-deferred accounts. Individuals report their non-deductible contributions to traditional IRAs with Form 8606. If a taxpayer earns interest or dividends on IRA investments, they would include that information on Schedule B. This connection helps clarify how various types of income relate to retirement accounts.

Form 4562, which deals with depreciation and amortization, has a connection to Schedule B when discussing rental income. If a taxpayer owns rental property and earns interest on security deposits, they are required to report this on Schedule B. The depreciation aspect reported on Form 4562 can also affect the overall tax calculations resulting from that rental income.

The IRS Form 8814, the Parents' Election to Report Child's Interest and Dividends, shares a link with Schedule B. Parents can opt to report their child's unearned income, such as interest or dividends, on their own tax returns instead of having the child file separately. Thus, if a child has investment income, it will also need to be included on Schedule B for accurate reporting.

Form 5329, which addresses additional taxes on qualified plans, aligns with Schedule B in addressing tax implications surrounding retirement income. For example, if a taxpayer has taken early distributions from retirement plans, the income would be reported on Schedule B. Understanding both forms is crucial for comprehensively handling tax responsibilities related to retirement savings.

Lastly, Form 8862, which is used to claim the Earned Income Tax Credit after disallowance, can intersect with Schedule B when income qualifies or disqualifies a taxpayer for the credit. If a taxpayer’s additional income is reported on Schedule B, it might influence their ability to claim the credit, emphasizing the interconnectedness of various tax documents.

Filling out the IRS Schedule B (Form 1040) can seem daunting, but it can be managed effectively with attention to detail. Below is a list of things you should and shouldn't do when completing this form.

Everyone has questions about the IRS Schedule B (Form 1040), but some common misconceptions might lead to confusion. Here are seven misconceptions clarified:

This is incorrect. You must file Schedule B if your total interest or dividends exceed $1,500, regardless of the amount. It’s required for anyone who has foreign accounts, as well.

Actually, if your interest or dividend income meets certain thresholds, using Schedule B becomes mandatory. Ignoring this can lead to issues with the IRS.

It's a misconception that banks are the only source of interest income. Other sources, like credit unions or online savings accounts, also contribute to taxable interest.

This is misleading. Different types of interest income (like tax-exempt bonds) have different reporting requirements. Make sure to categorize them properly.

On the contrary, if you have foreign bank accounts or financial assets, you must disclose this on Schedule B, and there can be significant penalties for not doing so.

This is not true. Even if you report interest directly, Schedule B must still be completed to provide details about the sources of that income.

This misconception assumes that reporting more income will automatically lead to a refund. In reality, whether you owe taxes or receive a refund depends on your overall tax situation.

Understanding these misconceptions about Schedule B can help ensure accurate tax filing and avoid complications. If in doubt, consulting with a tax professional is always a reliable option.

Here are some key takeaways about filling out and using the IRS Schedule B 1040 form:

By understanding these key points, you can navigate filling out Schedule B with greater confidence and accuracy.