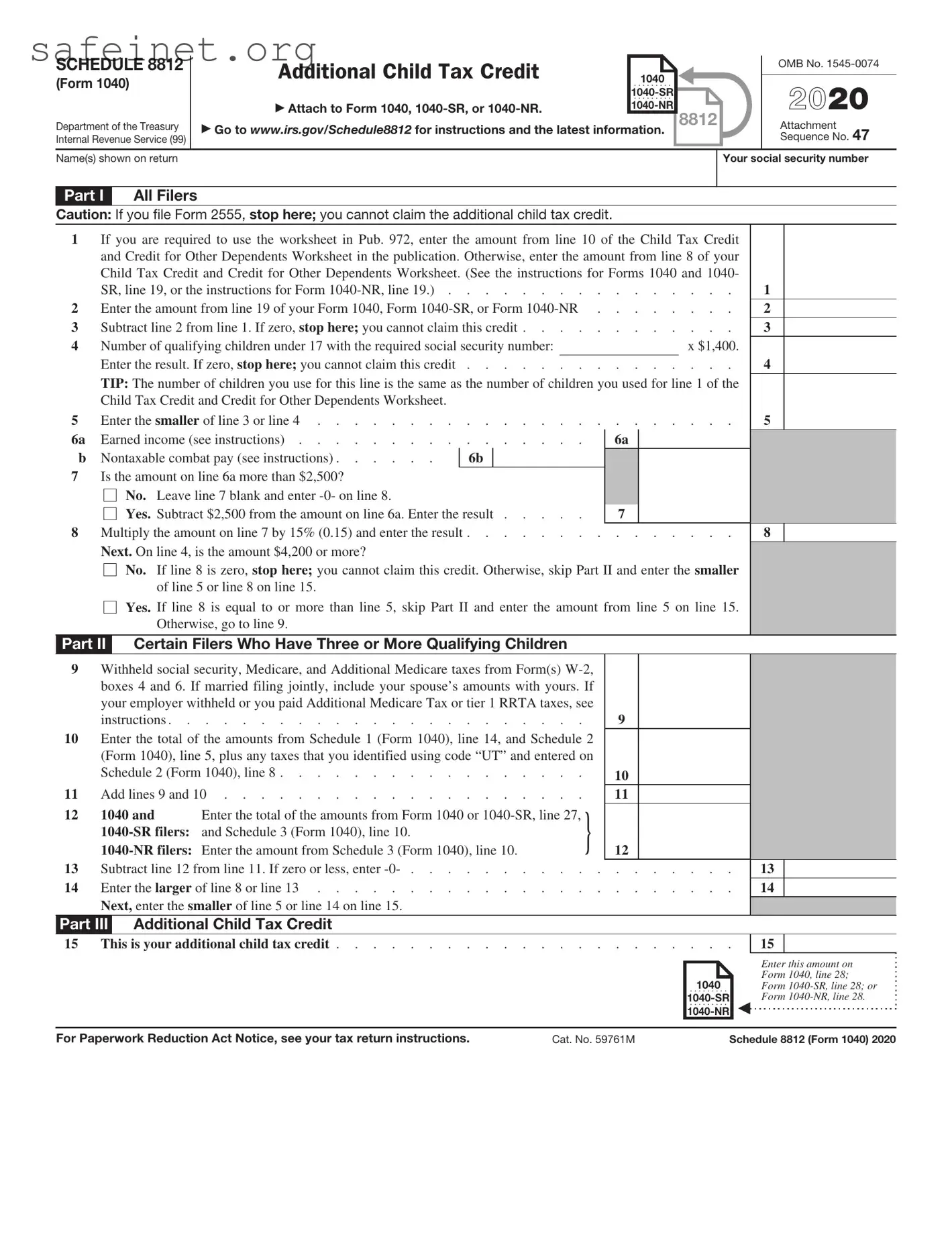

The IRS Schedule 8812, also known as the Additional Child Tax Credit, is an essential component for families seeking to maximize their tax benefits. This form is designed to help eligible taxpayers claim a credit for qualifying children under the age of 17, enhancing financial relief for parents and guardians. Not only does Schedule 8812 allow for the calculation of the Additional Child Tax Credit, but it also provides a pathway for taxpayers who may not qualify for the standard Child Tax Credit due to their income levels. It includes specific criteria, such as residency requirements and income thresholds, which help determine eligibility. Moreover, the form requires detailed information about dependents, ensuring that all necessary data is reported accurately. Filling out the Schedule 8812 can lead to significant savings, especially for lower to moderate-income families. Thus, understanding its intricacies is crucial for those aiming to benefit from this tax provision.

SCHEDULE 8812 |

Additional Child Tax Credit |

1040 |

|

OMB No. |

(Form 1040) |

|

2020 |

||

|

. . . . . . . . . |

|

||

|

|

|

||

|

|

. . . . . . . . . |

|

|

|

Attach to Form 1040, |

8812 |

||

Department of the Treasury |

Go to www.irs.gov/Schedule8812 for instructions and the latest information. |

Attachment |

||

Internal Revenue Service (99) |

|

|

|

Sequence No. 47 |

Name(s) shown on return |

|

|

|

Your social security number |

Part I |

All Filers |

Caution: If you file Form 2555, stop here; you cannot claim the additional child tax credit.

1If you are required to use the worksheet in Pub. 972, enter the amount from line 10 of the Child Tax Credit

|

and Credit for Other Dependents Worksheet in the publication. Otherwise, enter the amount from line 8 of your |

|

|

|||||||

|

Child Tax Credit and Credit for Other Dependents Worksheet. (See the instructions for Forms 1040 and 1040- |

|

|

|||||||

|

SR, line 19, or the instructions for Form |

. . . . . . . . |

1 |

|||||||

2 |

Enter the amount from line 19 of your Form 1040, Form |

. . . . . . . . |

2 |

|||||||

3 |

Subtract line 2 from line 1. If zero, stop here; you cannot claim this credit . . . . |

. . . . . . . . |

3 |

|||||||

4 |

Number of qualifying children under 17 with the required social security number: |

|

|

|

|

x $1,400. |

|

|

||

|

Enter the result. If zero, stop here; you cannot claim this credit |

. . . . . . . . |

4 |

|||||||

|

TIP: The number of children you use for this line is the same as the number of children you used for line 1 of the |

|

|

|||||||

|

Child Tax Credit and Credit for Other Dependents Worksheet. |

|

|

|

|

|

|

|

|

|

5 |

Enter the smaller of line 3 or line 4 |

. . . . . . . . |

5 |

|||||||

6a |

Earned income (see instructions) |

|

|

6a |

|

|

||||

b |

Nontaxable combat pay (see instructions) |

6b |

|

|

|

|

|

|

|

|

7Is the amount on line 6a more than $2,500?

|

No. Leave line 7 blank and enter |

|

|

|

|

|

Yes. Subtract $2,500 from the amount on line 6a. Enter the result |

|

7 |

|

|

8 |

Multiply the amount on line 7 by 15% (0.15) and enter the result |

. . . . . . . . |

8 |

|

|

Next. On line 4, is the amount $4,200 or more?

No. If line 8 is zero, stop here; you cannot claim this credit. Otherwise, skip Part II and enter the smaller of line 5 or line 8 on line 15.

Yes. If line 8 is equal to or more than line 5, skip Part II and enter the amount from line 5 on line 15.

Otherwise, go to line 9.

Part II Certain Filers Who Have Three or More Qualifying Children

9Withheld social security, Medicare, and Additional Medicare taxes from Form(s)

|

instructions |

|

9 |

|

|

||

10 |

Enter the total of the amounts from Schedule 1 (Form 1040), line 14, and Schedule 2 |

|

|

|

|||

|

(Form 1040), line 5, plus any taxes that you identified using code “UT” and entered on |

|

|

|

|||

|

Schedule 2 (Form 1040), line 8 |

|

10 |

|

|

||

11 |

Add lines 9 and 10 |

} |

11 |

|

|

||

12 |

1040 and |

Enter the total of the amounts from Form 1040 or |

|

|

|

||

|

|

|

|

||||

|

12 |

|

|

||||

13 |

Subtract line 12 from line 11. If zero or less, enter |

. . . . . . . |

13 |

|

|||

14 |

Enter the larger of line 8 or line 13 |

. . . . . . . |

14 |

|

|||

|

Next, enter the smaller of line 5 or line 14 on line 15. |

|

|

|

|

||

Part III |

Additional Child Tax Credit |

|

|

|

|

||

15 |

This is your additional child tax credit |

. . . . . . . |

15 |

|

|||

1040 |

. . . . . . . . . |

. . . . . . . . . |

Enter this amount on Form 1040, line 28; Form

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 59761M |

Schedule 8812 (Form 1040) 2020 |

| Fact Name | Description |

|---|---|

| Purpose | IRS Schedule 8812 is used to claim the Child Tax Credit and the Additional Child Tax Credit on your federal tax return. |

| Eligibility | To qualify, you must have dependent children under the age of 17 and meet specific income thresholds. |

| Form Requirements | This schedule must be attached to your Form 1040, 1040-SR, or 1040-NR when filing your tax return. |

| Income Limits | For tax year 2023, the benefit begins to phase out for single filers with income over $200,000 and married couples over $400,000. |

| State Law Reference | The state income tax treatment of child tax credits varies. It’s advisable to check state-specific laws for additional benefits. |

After gathering your tax documents and confirming your eligibility for child tax benefits, you can begin filling out IRS Schedule 8812. This form will help you calculate and claim various tax credits for your qualifying children on your tax return. Follow these steps carefully to ensure all information is accurate.

What is IRS Schedule 8812, and why do I need to file it?

IRS Schedule 8812, also known as the "Credits for Qualifying Children and Other Dependents," is an additional form you may need to file with your Form 1040. This form is specifically used to calculate your eligibility for various tax credits related to your qualifying children. If you have dependent children under the age of 17 or other qualifying dependents, completing this schedule can help you claim the Child Tax Credit or the Credit for Other Dependents, which may reduce your overall tax liability. Ensuring accuracy in this form can lead to significant tax savings.

Who qualifies as a ‘qualifying child’ for the purpose of Schedule 8812?

To be considered a qualifying child, a dependent must meet several criteria set by the IRS. Firstly, they must be under the age of 17 at the end of the tax year. Secondly, they must live with you for more than half of the year and be related to you in specific ways: they can be your child, stepchild, foster child, sibling, or descendant of any of these. Additionally, they must not provide more than half of their own support for the year. Meeting all these requirements is crucial to ensure your eligibility for the relevant credits.

How do I fill out Schedule 8812?

Filling out Schedule 8812 is a straightforward process if you follow the instructions carefully. First, start by entering your personal information and the names and Social Security numbers of your qualifying children. Next, navigate through the sections to determine the amount of the child tax credit and any other applicable credits for your dependents. The form includes a worksheet that helps you calculate the credits step by step. Make sure to provide accurate figures as errors may affect your refund or tax owed.

What should I do if I made a mistake on Schedule 8812?

If you realize that you made a mistake on Schedule 8812 after submitting your tax return, don’t panic. You can correct this by filing an amended return using Form 1040-X, "Amended U.S. Individual Income Tax Return." When completing Form 1040-X, you can provide the corrected information as well as an explanation for the changes made. It’s important to file this amendment promptly, particularly if the error results in a change to your tax liability, as this could also impact any refund you might be due or might affect future tax filings.

Incorrect Calculation of the Credit: Many people miscalculate the Child Tax Credit amount they're eligible for. It's essential to review your income and number of qualifying children carefully. Using the wrong income figures can significantly impact your credit.

Not Following Instructions Closely: The IRS provides specific guidance on how to fill out Schedule 8812. Skipping over important instructions can lead to errors. For example, overlooking the requirement to report your child’s Social Security number will cause delays or even disqualification from the credit.

Inaccurate Information: Entering wrong information about your dependents is a common mistake. This may include names, birthdays, or Social Security numbers. Such inaccuracies can result in audits or the denial of credits.

Missing Signatures: After completing the form, many taxpayers forget to sign it. An unsigned form is considered incomplete, and the IRS will reject it. Always double-check that you’ve signed and dated the form before submission.

The IRS Schedule 8812 is used to calculate the Additional Child Tax Credit. This document is often accompanied by several other forms that provide necessary information for accurately completing a tax return. Below are some of the key forms and documents commonly used alongside Schedule 8812.

Each of these forms plays an essential role in the tax filing process. They enable taxpayers to claim the deductions and credits for which they are eligible. Accurate completion ensures compliance with IRS regulations and maximizes potential tax benefits.

The IRS Schedule EIC (Form 1040) is a document related to the Earned Income Tax Credit, much like Schedule 8812, which also deals with credits for families. Both forms are designed to help lower-income families receive refunds or reduce tax liability. While Schedule EIC focuses on earned income and qualifying children, Schedule 8812 expands its scope to include the Child Tax Credit, allowing taxpayers to claim additional benefits for eligible dependents.

Form 8862 is another relevant document because it is used to claim the Earned Income Tax Credit (EITC) after a prior disallowance. Similar to Schedule 8812, it addresses eligibility and qualifying criteria for credits. Anyone whose EITC claim was denied in previous years must complete Form 8862 to prove they indeed qualify for the credit in the current tax year.

Form 2441 connects to Schedule 8812, as it addresses the Child and Dependent Care Credit. Both forms consider the financial burden of raising children. However, while Schedule 8812 is focused on the Child Tax Credit primarily, Form 2441 provides credits for child care expenses that allow parents to work or attend school, thus promoting work among families.

Also similar is Form 8863, which is used for education credits like the American Opportunity and Lifetime Learning Credits. Much like Schedule 8812, this form is aimed at benefiting taxpayers with dependents, but it focuses on their education expenses. Families can potentially reduce their tax burden by claiming credits for tuition and related costs through Form 8863.

Form 8880 offers another avenue for families, as it deals with the Retirement Savings Contributions Credit. Similar to Schedule 8812, this document is aimed at lower and moderate-income families. It incentivizes saving for retirement while acknowledging the importance of financial support for dependents, in the same way that Schedule 8812 acknowledges financial pressures from raising children.

Form 8889, utilized for Health Savings Accounts (HSAs), shares thematic similarities with Schedule 8812. Both documents underscore significant financial commitments faced by families, though the focus is distinctly different. While Schedule 8812 highlights the support for children, Form 8889 promotes saving for healthcare expenses, enabling families to navigate rising medical costs more effectively.

Form 5329 pertains to Additional Taxes on Qualified Plans (including IRAs) and can complement discussions found in Schedule 8812. Although they serve different purposes, both documents demonstrate an understanding of budget constraints faced by families. While Schedule 8812 is concerned with credits for children, Form 5329 ensures that families adhere to tax laws related to retirement savings, an essential part of long-term financial planning.

The Federal Form 1040 itself is essential in this context, acting as the overarching tax return document. Schedule 8812 supplements this form by allowing taxpayers to claim additional credits specific to families with dependent children. Essentially, Schedule 8812 is an add-on to the 1040, narrowing down some aspects of the taxpayer’s financial situation and providing further avenues for savings or refunds.

The IRS Publication 972, while not a form, functions as an important resource akin to Schedule 8812. This publication elaborates on the Child Tax Credit and other credits for families. It serves as a guide and educational tool, helping taxpayers understand the ins and outs of claiming these credits while Schedule 8812 offers the mechanism to claim them on the tax return.

Lastly, Form 8886 might be considered somewhat similar, despite its focus on reportable transactions. While it doesn’t directly relate to credits for families, the form emphasizes compliance and transparency for complex financial arrangements. Like Schedule 8812, which aids in proper tax reporting for families, Form 8886 ensures taxpayers are aware of their reporting requirements, promoting responsible financial behavior.

Filing IRS Schedule 8812 can be straightforward if you keep a few key points in mind. Here’s a helpful guide on what to do and what to avoid.

By following these guidelines, you can help ensure a smoother filing process for your Schedule 8812 form.

When dealing with the IRS Schedule 8812 form, misunderstandings can create confusion for taxpayers. Here are four common misconceptions:

Understanding these misconceptions can lead to more accurate tax filings and ensure taxpayers maximize their available credits.