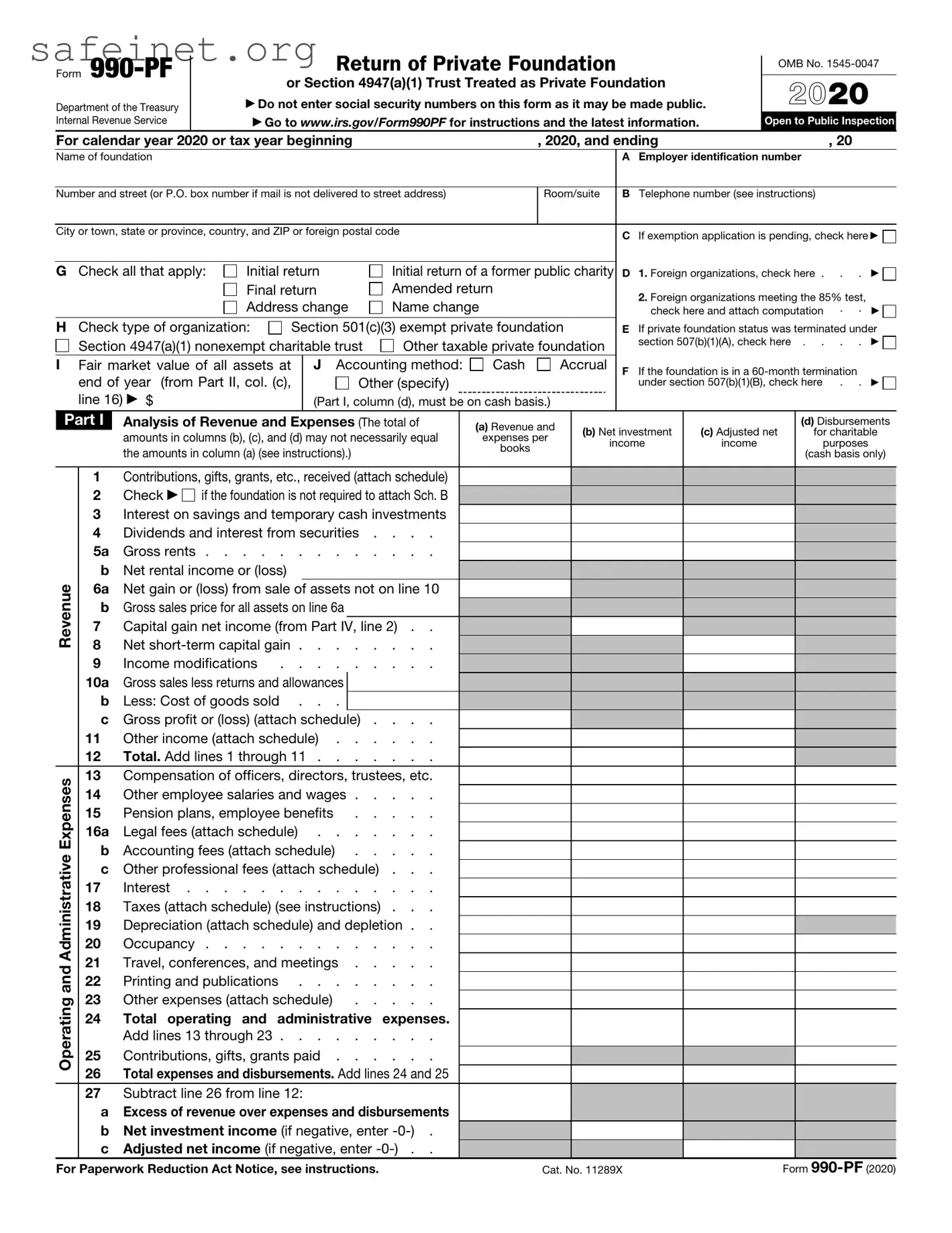

The IRS 990-PF form plays a critical role in the financial transparency and accountability of private foundations in the United States. This form provides a comprehensive overview of a foundation's financial activities throughout the tax year, detailing essential information such as revenue, expenses, and grantmaking activities. It also captures data on the foundation's investments, ensuring compliance with federal regulations while promoting philanthropic missions. Foundations utilize the 990-PF to report their financial position, including assets, liabilities, and net worth, which in turn helps inform both the IRS and the public about the foundation’s operations. Additionally, it includes information on the foundation's board members and key employees, shedding light on those who guide its activities. By requiring this detailed reporting, the IRS aims to enhance the public’s trust in charitable organizations and ensure that donations are directed toward legitimate purposes that align with the foundation's stated goals.

Form

Department of the Treasury Internal Revenue Service

Return of Private Foundation

or Section 4947(a)(1) Trust Treated as Private Foundation

▶Do not enter social security numbers on this form as it may be made public.

▶Go to www.irs.gov/Form990PF for instructions and the latest information.

OMB No.

2020

Open to Public Inspection

|

For calendar year 2020 or tax year beginning |

|

|

|

, 2020, and ending |

|

|

|

, 20 |

|

||||||||||||

|

Name of foundation |

|

|

|

|

|

|

|

|

|

|

|

|

A |

Employer identification number |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Number and street (or P.O. box number if mail is not delivered to street address) |

|

Room/suite |

|

B |

Telephone number (see instructions) |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

|

|

C If exemption application is pending, check here ▶ |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

G Check all that apply: |

Initial return |

Initial return of a former public charity |

D |

1. Foreign organizations, check here . |

. . |

▶ |

|||||||||||||||

|

|

|

|

|

Final return |

Amended return |

|

|

|

|

|

2. Foreign organizations meeting the 85% test, |

|

|||||||||

|

|

|

|

|

Address change |

Name change |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

check here and attach computation |

. . |

▶ |

||||||||||

|

H Check type of organization: |

Section 501(c)(3) exempt private foundation |

|

E |

If private foundation status was terminated under |

|||||||||||||||||

|

|

Section 4947(a)(1) nonexempt charitable trust |

Other taxable private foundation |

|

|

section 507(b)(1)(A), check here . . |

. . |

▶ |

||||||||||||||

|

I Fair market value of all assets at |

|

J Accounting method: |

Cash |

|

Accrual |

|

F |

If the foundation is in a |

|

||||||||||||

|

|

end of year (from Part II, col. (c), |

|

|

Other (specify) |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

under section 507(b)(1)(B), check here |

. . |

▶ |

||||||||||

|

|

line 16) ▶ $ |

|

|

|

(Part I, column (d), must be on cash basis.) |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Part I |

Analysis of Revenue and Expenses (The total of |

|

(a) Revenue and |

|

(b) Net investment |

(c) Adjusted net |

|

(d) Disbursements |

|||||||||||||

|

|

|

amounts in columns (b), (c), and (d) may not necessarily equal |

|

expenses per |

|

|

for charitable |

||||||||||||||

|

|

|

|

|

|

income |

income |

|

purposes |

|

||||||||||||

|

|

|

the amounts in column (a) (see instructions).) |

|

|

books |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

(cash basis only) |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

1 |

Contributions, gifts, grants, etc., received (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

2 |

Check ▶ |

if the foundation is not required to attach Sch. B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

3 |

Interest on savings and temporary cash investments |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

4 |

Dividends and interest from securities . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

5a |

Gross rents |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

b |

Net rental income or (loss) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Revenue |

6a |

Net gain or (loss) from sale of assets not on line 10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

b |

Gross sales price for all assets on line 6a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

Capital gain net income (from Part IV, line 2) . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

8 |

Net |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

9 |

Income modifications |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

10a |

Gross sales less returns and allowances |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

b |

Less: Cost of goods sold . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

c |

Gross profit or (loss) (attach schedule) . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

11 |

Other income (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

12 |

Total. Add lines 1 through 11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Expenses |

13 |

Compensation of officers, directors, trustees, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

14 |

Other employee salaries and wages |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

15 |

Pension plans, employee benefits |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

16a |

Legal fees (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Administrative |

b |

Accounting fees (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

c |

Other professional fees (attach schedule) . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

17 |

Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

18 |

Taxes (attach schedule) (see instructions) . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

19 |

Depreciation (attach schedule) and depletion . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

20 |

Occupancy |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

and |

21 |

Travel, conferences, and meetings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

22 |

Printing and publications |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Operating |

23 |

Other expenses (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

24 |

Total operating and administrative expenses. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Add lines 13 through 23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

25 |

Contributions, gifts, grants paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

26 |

Total expenses and disbursements. Add lines 24 and 25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

27 |

Subtract line 26 from line 12: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

a |

Excess of revenue over expenses and disbursements |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

b |

Net investment income (if negative, enter |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

c |

Adjusted net income (if negative, enter |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

For Paperwork Reduction Act Notice, see instructions. |

|

|

|

Cat. No. 11289X |

|

|

Form |

||||||||||||||

Form |

|

|

Page 2 |

|

Part II |

Balance Sheets Attached schedules and amounts in the description column |

Beginning of year |

End of year |

|

|

should be for |

(a) Book Value |

(b) Book Value |

(c) Fair Market Value |

|

|

|

|

|

1 |

|

|

|

|

2 |

Savings and temporary cash investments |

|

|

|

3 |

Accounts receivable ▶ |

|

|

|

|

Less: allowance for doubtful accounts ▶ |

|

|

|

4 |

Pledges receivable ▶ |

|

|

|

|

Less: allowance for doubtful accounts ▶ |

|

|

|

5 |

Grants receivable |

|

|

|

6Receivables due from officers, directors, trustees, and other

|

|

disqualified persons (attach schedule) (see instructions) . . |

|

7 |

Other notes and loans receivable (attach schedule) ▶ |

|

|

Less: allowance for doubtful accounts ▶ |

Assets |

8 |

Inventories for sale or use |

9 |

Prepaid expenses and deferred charges |

|

10a |

b

c |

|

11 |

|

|

Less: accumulated depreciation (attach schedule) ▶ |

12

13 |

|

|

14 |

Land, buildings, and equipment: basis ▶ |

|

|

Less: accumulated depreciation (attach schedule) ▶ |

|

15 |

Other assets (describe ▶ |

) |

16Total assets (to be completed by all

|

|

instructions. Also, see page 1, item I) |

||

|

|

|

|

|

|

17 |

Accounts payable and accrued expenses |

|

|

Liabilities |

18 |

Grants payable |

|

|

19 |

Deferred revenue |

|

||

|

|

|||

|

20 |

Loans from officers, directors, trustees, and other disqualified persons |

|

|

|

21 |

Mortgages and other notes payable (attach schedule) . . . |

|

|

|

22 |

Other liabilities (describe ▶ |

) |

|

|

23 |

Total liabilities (add lines 17 through 22) |

|

|

Balances |

25 |

Foundations that follow FASB ASC 958, check here |

▶ |

|

Net assets with donor restrictions |

|

|||

|

|

and complete lines 24, 25, 29, and 30. |

|

|

|

24 |

Net assets without donor restrictions |

|

|

Fund |

|

Foundations that do not follow FASB ASC 958, check here ▶ |

|

|

|

|

|

||

|

|

and complete lines 26 through 30. |

|

|

or |

26 |

Capital stock, trust principal, or current funds |

|

|

27 |

|

|||

Assets |

|

|||

28 |

Retained earnings, accumulated income, endowment, or other funds |

|

||

|

29 |

Total net assets or fund balances (see instructions) . . . |

|

|

Net |

30 |

Total liabilities and net assets/fund balances (see |

|

|

|

instructions) |

|

||

Part III |

Analysis of Changes in Net Assets or Fund Balances |

|

||

1Total net assets or fund balances at beginning of

|

1 |

|

2 |

Enter amount from Part I, line 27a |

2 |

3 |

Other increases not included in line 2 (itemize) ▶ |

3 |

4 |

Add lines 1, 2, and 3 |

4 |

5 |

Decreases not included in line 2 (itemize) ▶ |

5 |

6 |

Total net assets or fund balances at end of year (line 4 minus line |

6 |

Form

Form |

|

|

|

|

|

|

|

|

|

|

|

|

Page 3 |

||

Part IV |

Capital Gains and Losses for Tax on Investment Income |

|

|

|

|

|

|

||||||||

|

|

(a) List and describe the kind(s) of property sold (for example, real estate, |

|

(b) How acquired |

(c) Date acquired |

(d) Date sold |

|||||||||

|

|

|

|||||||||||||

|

|

|

|

(mo., day, yr.) |

(mo., day, yr.) |

||||||||||

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(e) Gross sales price |

|

|

(f) Depreciation allowed |

|

(g) Cost or other basis |

|

|

|

|

(h) Gain or (loss) |

||||

|

|

|

(or allowable) |

|

|

plus expense of sale |

|

|

|

|

((e) plus (f) minus (g)) |

||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete only for assets showing gain in column (h) and owned by the foundation on 12/31/69. |

|

|

|

(l) Gains (Col. (h) gain minus |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

(i) FMV as of 12/31/69 |

|

|

(j) Adjusted basis |

|

|

(k) Excess of col. (i) |

|

|

|

col. (k), but not less than |

||||

|

|

|

|

|

|

|

|

|

Losses (from col. (h)) |

||||||

|

|

|

as of 12/31/69 |

|

|

over col. (j), if any |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Capital gain net income or (net capital loss) { |

If gain, also enter in Part I, line 7 |

} |

|

|

|

|

|

|||||||

If (loss), enter |

2 |

|

|

|

|

||||||||||

3 Net |

} |

|

|

|

|

|

|||||||||

|

If gain, also enter in Part I, line 8, column (c). See instructions. If (loss), enter |

|

|

|

|

|

|||||||||

|

Part I, line 8 |

. . . . . . . |

3 |

|

|

|

|

||||||||

Part V |

Qualification Under Section 4940(e) for Reduced Tax on Net Investment Income |

|

|||||||||||||

|

|

|

SECTION 4940(e) REPEALED ON DECEMBER 20, 2019 – DO NOT COMPLETE. |

|

|||||||||||

1 |

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

|

(b) |

|

|

|

(c) |

|

|

|

|

|

(d) |

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|||

|

|

Reserved |

|

|

Reserved |

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserved |

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Reserved |

. . . . . . . . . |

. |

|

2 |

|

|

||||||||

|

|

|

|||||||||||||

3 |

Reserved |

. . . . . . . . . |

. |

|

3 |

|

|

||||||||

|

|

|

|||||||||||||

4 |

Reserved |

. . . . . . . . . |

. |

|

4 |

|

|

||||||||

|

|

|

|||||||||||||

5 |

Reserved |

. . . . . . . . . |

. |

|

5 |

|

|

||||||||

|

|

|

|||||||||||||

6 |

Reserved |

. . . . . . . . . |

. |

|

6 |

|

|

||||||||

|

|

|

|||||||||||||

7 |

Reserved |

. . . . . . . . . |

. |

|

7 |

|

|

||||||||

|

|

|

|||||||||||||

8 |

Reserved |

. . . . . . . . . |

. |

|

8 |

|

|

||||||||

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Form |

|

|

|

|

Page 4 |

|

Part VI |

Excise Tax Based on Investment Income (Section 4940(a), 4940(b), or |

|||||

1a Exempt operating foundations described in section 4940(d)(2), check here ▶ |

and enter “N/A” on line 1. |

} |

|

|

||

|

|

|

||||

Date of ruling or determination letter: |

(attach copy of letter if |

|

|

|

||

b Reserved |

. . . . . . . . . . |

. . . . . . . . . |

|

1 |

|

|

cAll other domestic foundations enter 1.39% of line 27b. Exempt foreign organizations, enter 4% of

|

Part I, line 12, col. (b) |

|

2 |

Tax under section 511 (domestic section 4947(a)(1) trusts and taxable foundations only; others, enter |

2 |

3 |

Add lines 1 and 2 |

3 |

4 |

Subtitle A (income) tax (domestic section 4947(a)(1) trusts and taxable foundations only; others, enter |

4 |

5 |

Tax based on investment income. Subtract line 4 from line 3. If zero or less, enter |

5 |

6Credits/Payments:

a |

2020 estimated tax payments and 2019 overpayment credited to 2020 . . |

|

6a |

|

|

|

|

|

|

|

||

b |

Exempt foreign |

|

6b |

|

|

|

|

|

|

|

||

c |

Tax paid with application for extension of time to file (Form 8868) . . . . |

|

6c |

|

|

|

|

|

|

|

||

d |

Backup withholding erroneously withheld |

|

6d |

|

|

|

|

|

|

|

||

7 |

Total credits and payments. Add lines 6a through 6d |

. . . . . . . . |

|

7 |

|

|

|

|||||

8 |

Enter any penalty for underpayment of estimated tax. Check here |

if Form 2220 is attached |

|

|

8 |

|

|

|

||||

9 |

Tax due. If the total of lines 5 and 8 is more than line 7, enter amount owed |

. . . . . . . ▶ |

|

9 |

|

|

|

|||||

10 |

Overpayment. If line 7 is more than the total of lines 5 and 8, enter the amount overpaid . . . |

▶ |

|

10 |

|

|

|

|||||

11 |

Enter the amount of line 10 to be: Credited to 2021 estimated tax ▶ |

|

|

|

Refunded |

▶ |

11 |

|

|

|

||

Part |

Statements Regarding Activities |

|

|

|

|

|

|

|

|

|

|

|

1a |

During the tax year, did the foundation attempt to influence any national, state, or local legislation or did it |

|

Yes No |

|||||||||

|

participate or intervene in any political campaign? |

. . . . . . . . . |

. |

|

1a |

|||||||

bDid it spend more than $100 during the year (either directly or indirectly) for political purposes? See the

instructions for the definition |

1b |

||

If the answer is “Yes” to 1a or 1b, attach a detailed description of the activities and copies of any materials |

|

|

|

published or distributed by the foundation in connection with the activities. |

|

||

c Did the foundation file Form |

|

1c |

|

d Enter the amount (if any) of tax on political expenditures (section 4955) imposed during the year: |

|

||

(1) On the foundation. ▶ $ |

(2) On foundation managers. ▶ $ |

|

|

eEnter the reimbursement (if any) paid by the foundation during the year for political expenditure tax imposed

on foundation managers. ▶ $ |

|

|

|

2 Has the foundation engaged in any activities that have not previously been reported to the IRS? . . . . |

2 |

||

If “Yes,” attach a detailed description of the activities. |

|

||

3Has the foundation made any changes, not previously reported to the IRS, in its governing instrument, articles

|

of incorporation, or bylaws, or other similar instruments? If “Yes,” attach a conformed copy of the changes . |

3 |

4a |

Did the foundation have unrelated business gross income of $1,000 or more during the year? |

4a |

b |

If “Yes,” has it filed a tax return on Form |

4b |

5 |

Was there a liquidation, termination, dissolution, or substantial contraction during the year? |

5 |

|

If “Yes,” attach the statement required by General Instruction T. |

|

6Are the requirements of section 508(e) (relating to sections 4941 through 4945) satisfied either:

•By language in the governing instrument, or

•By state legislation that effectively amends the governing instrument so that no mandatory directions that

|

conflict with the state law remain in the governing instrument? |

6 |

7 |

Did the foundation have at least $5,000 in assets at any time during the year? If “Yes,” complete Part II, col. (c), and Part XV |

7 |

8a |

Enter the states to which the foundation reports or with which it is registered. See instructions. ▶ |

|

bIf the answer is “Yes” to line 7, has the foundation furnished a copy of Form

(or designate) of each state as required by General Instruction G? If “No,” attach explanation |

8b |

9Is the foundation claiming status as a private operating foundation within the meaning of section 4942(j)(3) or 4942(j)(5) for calendar year 2020 or the tax year beginning in 2020? See the instructions for Part XIV. If “Yes,”

complete Part XIV |

9 |

10Did any persons become substantial contributors during the tax year? If “Yes,” attach a schedule listing their

names and addresses |

10 |

|

Form |

Form |

Page 5 |

|

Part |

|

Statements Regarding Activities (continued) |

11At any time during the year, did the foundation, directly or indirectly, own a controlled entity within the

meaning of section 512(b)(13)? If “Yes,” attach schedule. See instructions . . . . . . . . . . .

12Did the foundation make a distribution to a donor advised fund over which the foundation or a disqualified

person had advisory privileges? If “Yes,” attach statement. See instructions . . . . . . . . . . .

13Did the foundation comply with the public inspection requirements for its annual returns and exemption application?

Website address ▶ |

|

14 The books are in care of ▶ |

Telephone no. ▶ |

Located at ▶ |

ZIP+4 ▶ |

Yes No

Yes No

11

12

13

15Section 4947(a)(1) nonexempt charitable trusts filing Form

and enter the amount of |

15 |

|

|

|

16 At any time during calendar year 2020, did the foundation have an interest in or a signature or other |

authority |

|

Yes No |

|

over a bank, securities, or other financial account in a foreign country? |

|

|

||

16 |

|

|||

See the instructions for exceptions and filing requirements for FinCEN Form 114. If “Yes,” enter the name of |

|

|

||

the foreign country ▶ |

|

|

||

Part |

Statements Regarding Activities for Which Form 4720 May Be Required |

|

|

|

|

File Form 4720 if any item is checked in the “Yes” column, unless an exception applies. |

|

|

|

Yes No |

|

1a During the year, did the foundation (either directly or indirectly): |

|

|

|

|

|

(1) Engage in the sale or exchange, or leasing of property with a disqualified person? . . |

Yes |

No |

|||

(2)Borrow money from, lend money to, or otherwise extend credit to (or accept it from) a

|

disqualified person? |

Yes |

No |

(3) |

Furnish goods, services, or facilities to (or accept them from) a disqualified person? . . |

Yes |

No |

(4) |

Pay compensation to, or pay or reimburse the expenses of, a disqualified person? . . |

Yes |

No |

(5)Transfer any income or assets to a disqualified person (or make any of either available for

the benefit or use of a disqualified person)? |

Yes |

No |

(6)Agree to pay money or property to a government official? (Exception. Check “No” if the

foundation agreed to make a grant to or to employ the official for |

a period |

after |

|

|

termination of government service, if terminating within 90 days.) . . . |

. . . |

. . |

Yes |

No |

bIf any answer is “Yes” to

Regulations section |

. |

1b |

Organizations relying on a current notice regarding disaster assistance, check here |

▶ |

|

cDid the foundation engage in a prior year in any of the acts described in 1a, other than excepted acts, that

were not corrected before the first day of the tax year beginning in 2020? |

1c |

2Taxes on failure to distribute income (section 4942) (does not apply for years the foundation was a private operating foundation defined in section 4942(j)(3) or 4942(j)(5)):

aAt the end of tax year 2020, did the foundation have any undistributed income (Part XIII, lines

6d and 6e) for tax year(s) beginning before 2020? |

. . . . . . . . . . . . . . |

Yes |

No |

|||

If “Yes,” list the years ▶ |

20 |

, 20 |

, 20 |

, 20 |

|

|

bAre there any years listed in 2a for which the foundation is not applying the provisions of section 4942(a)(2) (relating to incorrect valuation of assets) to the year’s undistributed income? (If applying section 4942(a)(2) to

all years listed, answer “No” and attach |

2b |

cIf the provisions of section 4942(a)(2) are being applied to any of the years listed in 2a, list the years here.

▶ 20 |

, 20 |

, 20 |

, 20 |

|

|

3a Did the foundation hold more than a 2% direct or indirect interest in any business enterprise |

|

|

|||

at any time during the year? . |

. . . . . . . . . . . . . . . . . . . . . |

Yes |

No |

||

bIf “Yes,” did it have excess business holdings in 2020 as a result of (1) any purchase by the foundation or disqualified persons after May 26, 1969; (2) the lapse of the

foundation had excess business holdings in 2020.) |

3b |

4a Did the foundation invest during the year any amount in a manner that would jeopardize its charitable purposes? |

4a |

bDid the foundation make any investment in a prior year (but after December 31, 1969) that could jeopardize its charitable purpose that had not been removed from jeopardy before the first day of the tax year beginning in 2020? 4b

Form

Form |

Page 6 |

|

Part |

|

Statements Regarding Activities for Which Form 4720 May Be Required (continued) |

5a During the year, did the foundation pay or incur any amount to: |

|

|

|

Yes No |

(1) Carry on propaganda, or otherwise attempt to influence legislation (section 4945(e))? . |

Yes |

No |

||

(2)Influence the outcome of any specific public election (see section 4955); or to carry on,

directly or indirectly, any voter registration drive? |

Yes |

No |

(3) Provide a grant to an individual for travel, study, or other similar purposes? |

Yes |

No |

(4)Provide a grant to an organization other than a charitable, etc., organization described in

section 4945(d)(4)(A)? See instructions |

Yes |

No |

(5)Provide for any purpose other than religious, charitable, scientific, literary, or educational

purposes, or for the prevention of cruelty to children or animals? |

Yes |

No |

bIf any answer is “Yes” to

|

in Regulations section 53.4945 or in a current notice regarding disaster assistance? See instructions . |

. |

|

5b |

|

|

Organizations relying on a current notice regarding disaster assistance, check here |

▶ |

|

||

c |

If the answer is “Yes” to question 5a(4), does the foundation claim exemption from the tax |

|

|

|

|

|

because it maintained expenditure responsibility for the grant? |

Yes |

No |

|

|

|

If “Yes,” attach the statement required by Regulations section |

|

|

|

|

6a |

Did the foundation, during the year, receive any funds, directly or indirectly, to pay premiums |

|

|

|

|

|

on a personal benefit contract? |

Yes |

No |

|

|

b Did the foundation, during the year, pay premiums, directly or indirectly, on a personal benefit contract? |

. |

|

6b |

||

|

If “Yes” to 6b, file Form 8870. |

|

|

|

|

7a |

At any time during the tax year, was the foundation a party to a prohibited tax shelter transaction? |

Yes |

No |

|

|

b If “Yes,” did the foundation receive any proceeds or have any net income attributable to the transaction? |

. |

|

7b |

||

8Is the foundation subject to the section 4960 tax on payment(s) of more than $1,000,000 in

remuneration or excess parachute payment(s) during the year? |

Yes |

No |

|

Part VIII |

Information About Officers, Directors, Trustees, Foundation Managers, Highly Paid Employees, |

||

|

and Contractors |

|

|

1 List all officers, directors, trustees, and foundation managers and their compensation. See instructions.

(a)Name and address

(b)Title, and average hours per week

devoted to position

(c)Compensation

(If not paid,

enter

(d)Contributions to employee benefit plans

and deferred compensation

(e)Expense account, other allowances

2Compensation of five

(a)Name and address of each employee paid more than $50,000

(b)Title, and average hours per week

devoted to position

(c)Compensation

(d)Contributions to employee benefit

plans and deferred

compensation

(e)Expense account, other allowances

Total number of other employees paid over $50,000 . . . . . . . . . . . . . . . . . . . . ▶

Form

Form |

Page 7 |

|

Part VIII |

Information About Officers, Directors, Trustees, Foundation Managers, Highly Paid Employees, |

|

|

and Contractors (continued) |

|

3 Five

(a)Name and address of each person paid more than $50,000

(b)Type of service

(c)Compensation

Total number of others receiving over $50,000 for professional services |

. |

. . |

. |

. ▶ |

|

||

Part |

Summary of Direct Charitable Activities |

|

|

|

|

|

|

List the foundation’s four largest direct charitable activities during the tax year. Include relevant statistical information such as the number of |

Expenses |

||||||

organizations and other beneficiaries served, conferences convened, research papers produced, etc. |

|

|

|

|

|||

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part |

Summary of |

|

|

|

|

|

|

Describe the two largest |

|

|

|

|

Amount |

||

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

All other |

|

|

|

|

|

||

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Total. Add lines 1 through 3 |

. |

. . |

. |

. ▶ |

|

||

Form

Form |

Page 8 |

|

Part X |

Minimum Investment Return (All domestic foundations must complete this part. Foreign foundations, |

|

|

see instructions.) |

|

1Fair market value of assets not used (or held for use) directly in carrying out charitable, etc., purposes:

a |

Average monthly fair market value of securities |

1a |

b |

Average of monthly cash balances |

1b |

c |

Fair market value of all other assets (see instructions) |

1c |

d |

Total (add lines 1a, b, and c) |

1d |

eReduction claimed for blockage or other factors reported on lines 1a and

|

1c (attach detailed explanation) |

1e |

|

|

|

2 |

Acquisition indebtedness applicable to line 1 assets |

. . . . . . . |

|

2 |

|

3 |

Subtract line 2 from line 1d |

. . . . . . . |

|

3 |

|

4Cash deemed held for charitable activities. Enter 11/2% of line 3 (for greater amount, see

|

instructions) |

4 |

||

5 |

Net value of |

5 |

||

6 |

Minimum investment return. Enter 5% of line 5 |

6 |

||

Part XI |

Distributable Amount (see instructions) (Section 4942(j)(3) and (j)(5) private operating foundations |

|||

|

|

and certain foreign organizations, check here ▶ |

and do not complete this part.) |

|

1 |

Minimum investment return from Part X, line 6 |

||

2a |

Tax on investment income for 2020 from Part VI, line 5 |

2a |

|

b |

Income tax for 2020. (This does not include the tax from Part VI.) . . . |

2b |

|

c |

Add lines 2a and 2b |

||

3 |

Distributable amount before adjustments. Subtract line 2c from line 1 |

||

4 |

Recoveries of amounts treated as qualifying distributions |

||

5 |

Add lines 3 and 4 |

||

6 |

Deduction from distributable amount (see instructions) |

||

7Distributable amount as adjusted. Subtract line 6 from line 5. Enter here and on Part XIII, line 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part XII Qualifying Distributions (see instructions)

1

2c

3

4

5

6

7

1Amounts paid (including administrative expenses) to accomplish charitable, etc., purposes:

a |

Expenses, contributions, gifts, |

b |

2Amounts paid to acquire assets used (or held for use) directly in carrying out charitable, etc.,

purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3Amounts set aside for specific charitable projects that satisfy the:

a |

Suitability test (prior IRS approval required) |

b |

Cash distribution test (attach the required schedule) |

4Qualifying distributions. Add lines 1a through 3b. Enter here and on Part V, line 8; and Part XIII, line 4

5Foundations that qualify under section 4940(e) for the reduced rate of tax on net investment income.

|

Enter 1% of Part I, line 27b. See instructions |

6 |

Adjusted qualifying distributions. Subtract line 5 from line 4 |

1a

1b

2

3a

3b

4

5

6

Note: The amount on line 6 will be used in Part V, column (b), in subsequent years when calculating whether the foundation qualifies for the section 4940(e) reduction of tax in those years.

Form

Form |

|

|

Page 9 |

|

Part XIII |

Undistributed Income (see instructions) |

|

|

|

|

(a) |

(b) |

(c) |

(d) |

|

Corpus |

Years prior to 2019 |

2019 |

2020 |

1Distributable amount for 2020 from Part XI,

line 7 . . . . . . . . . . . . .

2 Undistributed income, if any, as of the end of 2020:

a |

Enter amount for 2019 only |

||

b |

Total for prior years: 20 |

, 20 |

, 20 |

3 Excess distributions carryover, if any, to 2020:

a |

From 2015 |

|

b |

From 2016 |

|

c |

From 2017 |

|

d |

From 2018 |

|

e |

From 2019 |

|

f |

Total of lines 3a through e |

|

4Qualifying distributions for 2020 from Part XII, line 4: ▶ $

a Applied to 2019, but not more than line 2a .

bApplied to undistributed income of prior years (Election

cTreated as distributions out of corpus (Election

d Applied to 2020 distributable amount . . e Remaining amount distributed out of corpus

5Excess distributions carryover applied to 2020 (If an amount appears in column (d), the same

amount must be shown in column (a).) . .

6Enter the net total of each column as indicated below:

a Corpus. Add lines 3f, 4c, and 4e. Subtract line 5

bPrior years’ undistributed income. Subtract

line 4b from line 2b . . . . . . . .

cEnter the amount of prior years’ undistributed income for which a notice of deficiency has been issued, or on which the section 4942(a) tax has been previously assessed . . . .

dSubtract line 6c from line 6b. Taxable

eUndistributed income for 2019. Subtract line 4a from line 2a. Taxable

instructions . . . . . . . . . . .

fUndistributed income for 2020. Subtract lines 4d and 5 from line 1. This amount must be

distributed in 2021 . . . . . . . . .

7Amounts treated as distributions out of corpus to satisfy requirements imposed by section 170(b)(1)(F) or 4942(g)(3) (Election may be

8Excess distributions carryover from 2015 not applied on line 5 or line 7 (see instructions) .

9Excess distributions carryover to 2021.

|

Subtract lines 7 and 8 from line 6a . . . |

|

10 Analysis of line 9: |

||

a |

Excess from 2016 . . . . |

|

b |

Excess from 2017 . . . . |

|

c |

Excess from 2018 . . . . |

|

d |

Excess from 2019 . . . . |

|

e |

Excess from 2020 . . . . |

|

Form

Form |

|

|

|

|

|

|

Page 10 |

||

Part XIV |

Private Operating Foundations (see instructions and Part |

|

|

|

|||||

1a If the foundation has received a ruling or determination letter that it is a private operating |

|

|

|

|

|||||

|

foundation, and the ruling is effective for 2020, enter the date of the ruling . |

. . . . . ▶ |

|

|

|

|

|||

|

|

|

|

|

|||||

b Check box to indicate whether the foundation is a private operating foundation described in section |

4942(j)(3) or |

4942(j)(5) |

|||||||

2a |

Enter the lesser of the adjusted net |

Tax year |

|

Prior 3 years |

|

|

(e) Total |

||

|

income from Part I or the minimum |

|

|

|

|

|

|

||

|

(a) 2020 |

(b) 2019 |

(c) 2018 |

(d) 2017 |

|||||

|

investment return from Part X for |

|

|||||||

|

|

|

|

|

|

|

|

||

|

each year listed |

|

|

|

|

|

|

|

|

b |

85% of line 2a |

|

|

|

|

|

|

|

|

cQualifying distributions from Part XII, line 4, for each year listed . . . .

dAmounts included in line 2c not used directly for active conduct of exempt activities . .

eQualifying distributions made directly for active conduct of exempt activities.

Subtract line 2d from line 2c . . .

3Complete 3a, b, or c for the alternative test relied upon:

a“Assets” alternative

(1) Value of all assets . . . . .

(2)Value of assets qualifying under

section 4942(j)(3)(B)(i) . . . .

b“Endowment” alternative

Part X, line 6, for each year listed |

. . |

c“Support” alternative

(1)Total support other than gross investment income (interest, dividends, rents, payments on

securities loans (section 512(a)(5)), or royalties) . . . .

(2)Support from general public and 5 or more exempt organizations as provided in section 4942(j)(3)(B)(iii) . . . .

(3)Largest amount of support from

an exempt organization . . .

(4)Gross investment income . . .

Part XV |

Supplementary Information (Complete this part only if the foundation had $5,000 or more in assets at |

|

any time during the |

1 Information Regarding Foundation Managers:

aList any managers of the foundation who have contributed more than 2% of the total contributions received by the foundation before the close of any tax year (but only if they have contributed more than $5,000). (See section 507(d)(2).)

bList any managers of the foundation who own 10% or more of the stock of a corporation (or an equally large portion of the ownership of a partnership or other entity) of which the foundation has a 10% or greater interest.

2Information Regarding Contribution, Grant, Gift, Loan, Scholarship, etc., Programs:

Check here ▶  if the foundation only makes contributions to preselected charitable organizations and does not accept unsolicited requests for funds. If the foundation makes gifts, grants, etc., to individuals or organizations under other conditions, complete items 2a, b, c, and d. See instructions.

if the foundation only makes contributions to preselected charitable organizations and does not accept unsolicited requests for funds. If the foundation makes gifts, grants, etc., to individuals or organizations under other conditions, complete items 2a, b, c, and d. See instructions.

aThe name, address, and telephone number or email address of the person to whom applications should be addressed:

bThe form in which applications should be submitted and information and materials they should include:

cAny submission deadlines:

dAny restrictions or limitations on awards, such as by geographical areas, charitable fields, kinds of institutions, or other factors:

Form

| Fact | Description |

|---|---|

| Purpose | The IRS Form 990-PF is used primarily by private foundations to report financial information to the IRS. |

| Filing Requirement | Private foundations must file Form 990-PF annually, regardless of their income levels. |

| Deadline | Form 990-PF is typically due on the 15th day of the 5th month after the end of the foundation's tax year. |

| Public Disclosure | This form is public information. Anyone can request to see it, which promotes transparency. |

| State Requirements | Some states require a copy of Form 990-PF to be filed with their state agencies. Check specific state laws for details. |

| Part I Overview | Part I provides basic information about the foundation, including its name, address, and type of foundation. |

| Investment Income | Part II and Part III detail the foundation's revenues, including contributions and investment income, showcasing its financial health. |

| Grants and Expenses | Part IV explains how the foundation distributed its income through grants and operational expenses, underscoring its mission-driven work. |

| Penalties for Non-filing | Failure to file Form 990-PF can result in financial penalties and can jeopardize the foundation's tax-exempt status. |

Completing the IRS 990-PF form requires attention to detail and accurate financial reporting. Preparing your information ahead of time will ensure the process goes smoothly. Here are the steps to fill out the form:

What is IRS Form 990-PF?

IRS Form 990-PF is an annual tax return required for private foundations in the United States. It provides the IRS with detailed information about the foundation's finances, including income, expenses, and activities. This form helps ensure transparency and compliance with federal tax regulations.

Who is required to file Form 990-PF?

Any private foundation with gross receipts exceeding $100,000 or total assets of over $250,000 at the end of the year must file Form 990-PF. This requirement also applies if the foundation is controlled by a corporation, partnership, or other entity that qualifies as a private foundation.

What information is included on Form 990-PF?

The form includes various sections covering the foundation’s revenue, expenses, and net assets. It also requires a detailed report on grants made, investments, and administrative costs. Additionally, it contains schedules to provide supplementary information, such as compensation for officers and directors.

When is Form 990-PF due?

Form 990-PF is due on the 15th day of the 5th month after the end of the foundation's tax year. For most private foundations operating on a calendar year, the form must be submitted by May 15. Extensions may be requested, but they are not automatic.

What are the penalties for not filing Form 990-PF?

Failure to file Form 990-PF can result in significant penalties. Private foundations may incur fines of up to $20 per day for each day the form is late, with a maximum penalty of $10,000. Additionally, if the foundation continues to neglect its filing obligations, it may risk losing its tax-exempt status.

Can Form 990-PF be filed electronically?

Yes, Form 990-PF can be filed electronically using the IRS's e-file system. Electronic filing can simplify the submission process and provide immediate confirmation of receipt. Many foundations prefer this method for its efficiency and ease of use.

What resources are available for assistance with Form 990-PF?

The IRS provides numerous resources on their website, including instructions, FAQs, and contact information for support. Additionally, many accountants and tax professionals have experience in preparing and filing Form 990-PF and can offer valuable assistance.

What happens after Form 990-PF is filed?

Once Form 990-PF is filed, the IRS reviews it for compliance. The foundation must retain a copy of the filed form along with its supporting documentation. This information should be readily available in case of an audit or further inquiries from the IRS.

Omitting basic information: Many filers forget to include essential details such as the organization's name, address, and EIN. Missing these can lead to delays in processing.

Incorrect financial data: Accurate reporting of income, expenses, and assets is critical. Mistakes in these numbers can create issues with compliance and reporting.

Neglecting to report contributions: Filers often overlook reporting grants and contributions received. This omission can misrepresent the organization's financial health.

Failing to disclose related organizations: Many people do not reference affiliated entities. This can raise red flags and produce questions from the IRS.

Ignoring deadline requirements: Some individuals miss the filing deadline. Timely submission is essential to avoid penalties.

Not providing complete descriptions: When detailing activities, incomplete descriptions may hinder understanding of the organization's mission and operations.

Errors in calculations: Simple arithmetic mistakes can lead to significant discrepancies in reported figures. Double-check all calculations before submission.

Misunderstanding compliance obligations: Failing to recognize or comply with state-specific requirements can lead to unnecessary complications.

Disregarding public support tests: Many organizations overlook the requirement to provide public support information, which is vital for maintaining tax-exempt status.

Failing to review before submission: A final review is often neglected. Poor proofreading can lead to inaccuracies and future scrutiny from the IRS.

The IRS Form 990-PF is a critical document for private foundations, detailing their financial activities and compliance with tax regulations. However, it is not the only form needed to ensure adherence to IRS guidelines. A variety of other forms and documents are often required alongside the 990-PF for comprehensive compliance and transparency. Below is a list of other essential forms and documents utilized by private foundations.

In summary, these forms and documents complement the IRS 990-PF by covering various aspects of a foundation’s operations, ensuring compliance, transparency, and accountability. Being organized and thorough with all required paperwork not only aids in regulatory adherence but also promotes trust with stakeholders and the public.

The IRS Form 990 is one of the most well-known forms for nonprofit organizations. Like Form 990-PF, it provides transparency about financial activities. Both forms require organizations to disclose information about their revenue, expenses, and governance. However, while Form 990 is used by public charities, Form 990-PF specifically applies to private foundations. This distinction reflects the different regulatory frameworks surrounding these two types of organizations.

Form 990-EZ serves as a shorter version of Form 990 for smaller organizations. It shares many similarities with Form 990-PF, particularly in the financial reporting requirements. Like Form 990-PF, it includes sections for revenue, expenses, and program activities. The main difference lies in the size and type of organizations that typically use it, as it is designed for those with less complex operations.

Form 1023 is the application for tax-exempt status for charitable organizations. It is similar to Form 990-PF in that it requires detailed information about the organization’s purpose, activities, and structure. Both forms aim to demonstrate that the organization adheres to tax rules and operates in a manner consistent with charitable purposes. However, Form 1023 is more focused on the initial approval process for charitable organizations, while Form 990-PF is an annual informational return.

Form 1024 is another application form, but it’s used for organizations seeking tax-exempt status under specific IRS codes other than 501(c)(3). Similar in nature to Form 1023, it requires organizations to provide detailed information about their structure and activities. While Form 990-PF deals with private foundations after they have been established, Form 1024 helps with the approval process for various other tax-exempt organizations.

The IRS Form 990-T is used to report unrelated business income tax (UBIT). Organizations that file Form 990-PF may also need to file Form 990-T if they earn income from business activities not related to their charitable purpose. Both forms require financial disclosures, but Form 990-T focuses specifically on income and expenses related to those unrelated trade or business activities.

Form 990-PF and Schedule B are closely linked. Schedule B is used to report contributions received by the organization. Form 990-PF requires similar information regarding grants and donations, thus ensuring transparency about funding sources. While Form 990-PF covers a broader range of financial details, Schedule B dives deep into the specifics of contributions, enhancing the overall picture of the foundation's finances.

The IRS Form 5500 provides information about employee benefit plans. Like Form 990-PF, it aims to promote transparency about financial matters, but relates to retirement and health plans instead of charitable activities. Both forms require detailed financial information, although the context and focus differ significantly. Form 5500 is essential for ensuring that organizations comply with employee benefit regulations.

Finally, Form 1065 is used by partnerships to report income, deductions, gains, and losses. Although it serves a different type of entity, both Form 990-PF and Form 1065 emphasize the importance of reporting financial health and operational details to relevant authorities. Just like Form 990-PF, which ensures that private foundations fulfill their charitable missions, Form 1065 ensures that partnerships adhere to tax regulations regarding their shared income and expenses.

When filling out the IRS 990-PF form, it's important to be careful and informed. Here are some helpful dos and don'ts to consider.

Following these tips will help ensure your IRS 990-PF form is filled out correctly and submitted on time.

The IRS Form 990-PF is an important document for private foundations, yet there are several misconceptions surrounding it. These misunderstandings can lead to confusion and mismanagement. Below is a list that aims to clarify these misconceptions:

This is incorrect. All private foundations, regardless of size, must file Form 990-PF annually. This requirement helps ensure transparency and accountability.

While it does serve a tax-related function, Form 990-PF also provides vital information to the public about a foundation's financial status and charitable activities.

This misconception overlooks the requirement. A foundation must file the form even if it did not distribute any grants in the reporting year.

In fact, Form 990-PF is a public document. Anyone can access it, making transparency crucial for building public trust.

This is misleading. While the IRS may not review every form in detail, they do conduct audits. Accuracy and clarity are essential to avoid potential issues.

Filing does not guarantee exemption. Foundations must meet specific criteria, and compliance with regulations is continually evaluated by the IRS.

This is not necessarily true. While the form has standardized sections, each foundation's finances and activities differ. Customization is often required to accurately represent unique circumstances.

This assumption is false. If a foundation’s activities or financial situation change, it is critical to reflect those changes accurately in future filings.

Turning a blind eye to deadlines can lead to penalties and legal issues. Timely filing is essential for maintaining good standing.

While some may feel confident to complete the form independently, seeking professional guidance can help avoid errors that may have serious consequences.

Understanding these misconceptions can aid in the proper management of private foundations and ensure compliance with regulatory requirements. By demystifying Form 990-PF, foundations can better fulfill their commitments to transparency and philanthropy.

Filing the IRS 990-PF form is a crucial task for private foundations. It provides transparency and ensures compliance with federal regulations. Here are some key takeaways to consider when filling it out:

By keeping these takeaways in mind, filling out the IRS 990-PF form can become a more straightforward process. Staying organized and attentive can significantly ease the filing experience.