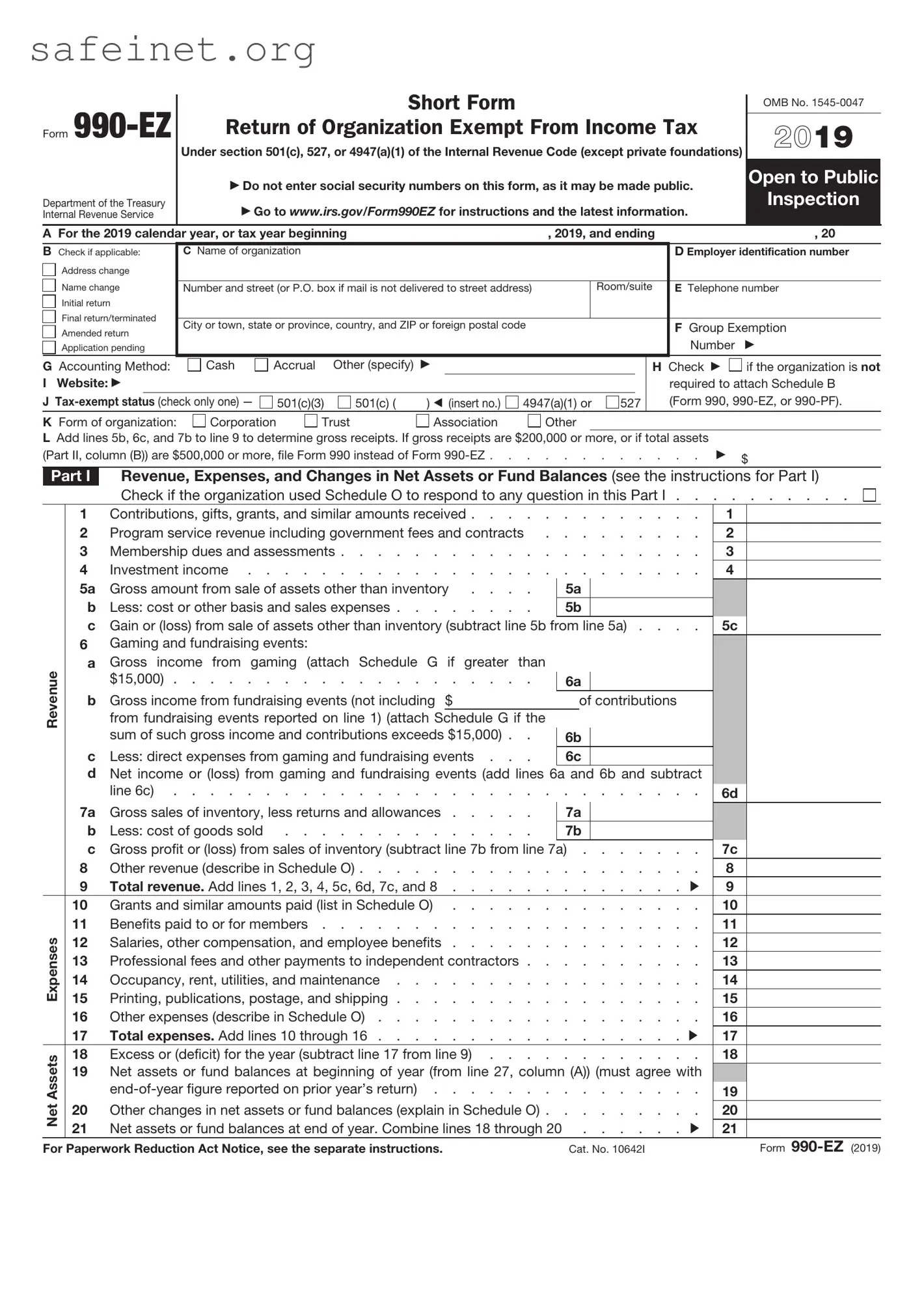

The IRS 990-EZ form serves as a vital tool for many small to medium-sized tax-exempt organizations, providing a streamlined method to report their financial activities. This form is typically used by organizations that have annual gross receipts between $200,000 and $500,000, or total assets of less than $500,000 at the end of the year. In essence, it offers a simplified alternative to the more complex 990 form, enabling organizations to showcase their financial health, activities, and governance practices in a straightforward manner. The 990-EZ requires detailed information about the organization's revenue, expenses, and net assets, reflecting its overall financial position. Moreover, it mandates disclosures about key personnel, public support, and program activities, ensuring transparency and accountability. As tax-exempt organizations play a significant role in addressing community needs, understanding and accurately completing the 990-EZ is essential for compliance. Not only does it fulfill legal obligations, but it also aids in building trust with stakeholders, donors, and the public alike.

Form

Department of the Treasury Internal Revenue Service

Short Form

Return of Organization Exempt From Income Tax

Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Do not enter social security numbers on this form, as it may be made public. Go to www.irs.gov/Form990EZ for instructions and the latest information.

OMB No.

2019

Open to Public

Inspection

A For the 2019 calendar year, or tax year beginning |

, 2019, and ending |

, 20 |

||

B Check if applicable: |

C Name of organization |

|

|

D Employer identification number |

Address change |

|

|

|

|

|

|

|

|

|

Name change |

Number and street (or P.O. box if mail is not delivered to street address) |

|

Room/suite |

E Telephone number |

Initial return |

|

|

|

|

Final return/terminated |

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

F Group Exemption |

|

Amended return |

|

|

||

|

|

|

Number |

|

Application pending |

|

|

|

|

G Accounting Method: |

Cash |

Accrual |

Other (specify) |

|

|

|

|

|

|

I Website: |

|

|

|

|

|

|

|

|

|

J |

501(c)(3) |

501(c) ( |

) (insert no.) |

4947(a)(1) or |

527 |

||||

H Check |

if the organization is not |

required to attach Schedule B (Form 990,

K Form of organization: |

Corporation |

Trust |

Association |

Other |

LAdd lines 5b, 6c, and 7b to line 9 to determine gross receipts. If gross receipts are $200,000 or more, or if total assets

(Part II, column (B)) are $500,000 or more, file Form 990 instead of Form |

$ |

|

Part I Revenue, Expenses, and Changes in Net Assets or Fund Balances (see the instructions for Part I)

Check if the organization used Schedule O to respond to any question in this Part I . . . . . . . . . .

Revenue

Net Assets Expenses

1 |

Contributions, gifts, grants, and similar amounts received . . . . |

. . . . . . . . . |

1 |

|

||

2 |

Program service revenue including government fees and contracts |

. . . . . . . . . |

2 |

|

||

3 |

Membership dues and assessments |

. . . . . . . . . |

3 |

|

||

4 |

Investment income |

. . . . . . . . . |

4 |

|

||

5a |

Gross amount from sale of assets other than inventory . . . . |

|

5a |

|

|

|

b |

Less: cost or other basis and sales expenses |

|

5b |

|

|

|

c |

Gain or (loss) from sale of assets other than inventory (subtract line 5b from line 5a) . . . . |

5c |

||||

6Gaming and fundraising events:

aGross income from gaming (attach Schedule G if greater than

|

$15,000) |

6a |

|

||

b |

Gross income from fundraising events (not including $ |

of contributions |

|||

|

from fundraising events reported on line 1) (attach |

Schedule G if the |

|

|

|

|

sum of such gross income and contributions exceeds $15,000) . . |

6b |

|

||

c |

Less: direct expenses from gaming and fundraising events . . . |

6c |

|

||

dNet income or (loss) from gaming and fundraising events (add lines 6a and 6b and subtract

|

line 6c) |

. . . . . . . . |

|

6d |

|

|

7a |

Gross sales of inventory, less returns and allowances |

7a |

|

|

|

|

b |

Less: cost of goods sold |

7b |

|

|

|

|

c |

Gross profit or (loss) from sales of inventory (subtract line 7b from line 7a) |

7c |

|

|||

8 |

Other revenue (describe in Schedule O) |

. . . . . . . . |

|

8 |

|

|

9 |

Total revenue. Add lines 1, 2, 3, 4, 5c, 6d, 7c, and 8 |

. . . . . . . |

|

9 |

|

|

10 |

Grants and similar amounts paid (list in Schedule O) |

. . . . . . . . |

|

10 |

|

|

11 |

Benefits paid to or for members |

. . . . . . . . |

|

11 |

|

|

12 |

Salaries, other compensation, and employee benefits |

. . . . . . . . |

|

12 |

|

|

13 |

Professional fees and other payments to independent contractors . . |

. . . . . . . . |

|

13 |

|

|

14 |

Occupancy, rent, utilities, and maintenance |

. . . . . . . . |

|

14 |

|

|

15 |

Printing, publications, postage, and shipping |

. . . . . . . . |

|

15 |

|

|

16 |

Other expenses (describe in Schedule O) |

. . . . . . . . |

|

16 |

|

|

17 |

Total expenses. Add lines 10 through 16 |

. . . . . . . |

|

17 |

|

|

18 |

Excess or (deficit) for the year (subtract line 17 from line 9) . . . . |

. . . . . . . . |

|

18 |

|

|

19Net assets or fund balances at beginning of year (from line 27, column (A)) (must agree with

|

19 |

|

20 |

Other changes in net assets or fund balances (explain in Schedule O) |

20 |

21 |

Net assets or fund balances at end of year. Combine lines 18 through 20 |

21 |

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 10642I |

Form |

Form |

|

Page 2 |

||||

Part II |

Balance Sheets (see the instructions for Part II) |

|

|

|

||

|

|

Check if the organization used Schedule O to respond to any question in this Part II |

|

|||

|

|

|

(A) Beginning of year |

|

(B) End of year |

|

|

|

|

|

|

|

|

22 |

Cash, savings, and investments |

|

22 |

|

|

|

23 |

Land and buildings |

|

23 |

|

|

|

24 |

Other assets (describe in Schedule O) |

|

24 |

|

|

|

25 |

Total assets |

|

25 |

|

|

|

26 |

Total liabilities (describe in Schedule O) |

|

26 |

|

|

|

27 |

Net assets or fund balances (line 27 of column (B) must agree with line 21) . . |

|

27 |

|

|

|

Part III Statement of Program Service Accomplishments (see the instructions for Part III)

|

|

Check if the organization used Schedule O to respond to any question in this Part III . . |

|

Expenses |

|||||

|

|

|

|

|

|

|

(Required for section |

||

What is the organization’s primary exempt purpose? |

|||||||||

501(c)(3) and 501(c)(4) |

|||||||||

|

|

|

|

|

|

|

|||

Describe the organization’s program service accomplishments for each of its three largest program services, |

organizations; optional for |

||||||||

as measured by expenses. In a clear and concise manner, describe the services provided, the number of |

others.) |

||||||||

persons benefited, and other relevant information for each program title. |

|

|

|||||||

28 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

28a |

|

|||

29 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

29a |

|

|||

30 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

30a |

|

|||

31 |

|

Other program services (describe in Schedule O) |

|

|

|||||

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

31a |

|

||||

32 |

|

Total program service expenses (add lines 28a through 31a) |

32 |

|

|||||

Part IV List of Officers, Directors, Trustees, and Key Employees (list each one even if not

Check if the organization used Schedule O to respond to any question in this Part IV . . . . . . . . .

(a)Name and title

(b)Average hours per week

devoted to position

(c) Reportable |

(d) Health benefits, |

(e) Estimated amount of |

compensation |

contributions to employee |

|

(Forms |

benefit plans, and |

other compensation |

(if not paid, enter |

deferred compensation |

|

|

|

|

Form

Form |

Page 3 |

||

Part V |

Other Information (Note the Schedule A and personal benefit contract statement requirements in the |

||

|

instructions for Part V.) Check if the organization used Schedule O to respond to any question in this Part V . |

|

|

|

|

Yes No |

|

33Did the organization engage in any significant activity not previously reported to the IRS? If “Yes,” provide a

detailed description of each activity in Schedule O |

33 |

34Were any significant changes made to the organizing or governing documents? If “Yes,” attach a conformed copy of the amended documents if they reflect a change to the organization’s name. Otherwise, explain the

change on Schedule O. See instructions |

34 |

35a Did the organization have unrelated business gross income of $1,000 or more during the year from business |

|

activities (such as those reported on lines 2, 6a, and 7a, among others)? |

35a |

b If “Yes” to line 35a, has the organization filed a Form |

35b |

cWas the organization a section 501(c)(4), 501(c)(5), or 501(c)(6) organization subject to section 6033(e) notice,

reporting, and proxy tax requirements during the year? If “Yes,” complete Schedule C, Part III |

35c |

36Did the organization undergo a liquidation, dissolution, termination, or significant disposition of net assets

|

during the year? If “Yes,” |

complete applicable parts of Schedule N |

. . . . . . |

|

|

36 |

|

||||||

37a |

Enter amount of political expenditures, direct or indirect, as described in the instructions |

37a |

|

|

|

|

|

||||||

b |

Did the organization file Form |

. . . . . . |

|

|

37b |

|

|||||||

38a |

Did the organization borrow from, or make any loans to, any officer, director, trustee, or key employee; or were |

|

|

|

|||||||||

|

any such loans made in a prior year and still outstanding at the end of the tax year covered by this return? . |

38a |

|

||||||||||

b |

If “Yes,” complete Schedule L, Part II, and enter the total amount involved . . . . |

38b |

|

|

|

|

|

||||||

39 |

Section 501(c)(7) organizations. Enter: |

|

|

|

|

|

|

|

|

|

|||

a |

Initiation fees and capital contributions included on line 9 |

39a |

|

|

|

|

|||||||

b |

Gross receipts, included on line 9, for public use of club facilities |

39b |

|

|

|

|

|||||||

40a |

Section 501(c)(3) organizations. Enter amount of tax imposed on the organization during the year under: |

|

|

||||||||||

|

section 4911 |

|

; section 4912 |

|

; section 4955 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

bSection 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Did the organization engage in any section 4958

excess benefit transaction during the year, or did it engage in an excess benefit transaction in a prior year |

|

|

|

that has not been reported on any of its prior Forms 990 or |

|

40b |

|

c Section 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Enter amount of tax imposed |

|

|

|

on organization managers or disqualified persons during the year under sections 4912, |

|

|

|

4955, and 4958 |

|

|

|

|

|

|

|

d Section 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Enter amount of tax on line |

|

|

|

40c reimbursed by the organization |

|

|

|

eAll organizations. At any time during the tax year, was the organization a party to a prohibited tax shelter

|

transaction? If “Yes,” complete Form |

|

40e |

|

|||||

41 |

List the states with which a copy of this return is filed |

|

|

|

|

|

|

|

|

42a |

The organization’s books are in care of |

Telephone no. |

|

|

|

|

|

||

b |

Located at |

ZIP + 4 |

|

|

|

|

|

||

At any time during the calendar year, did the organization have an interest in or a signature or other authority |

over |

|

|

Yes |

No |

||||

|

a financial account in a foreign country (such as a bank account, securities account, or other financial account)? |

|

42b |

|

|

||||

|

If “Yes,” enter the name of the foreign country |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

See the instructions for exceptions and filing requirements for FinCEN Form 114, Report of Foreign Bank and |

|

|

|

|

||||

|

Financial Accounts (FBAR). |

|

|

|

|

|

|

||

c |

At any time during the calendar year, did the organization maintain an office outside the United States? . |

|

42c |

|

|

||||

|

If “Yes,” enter the name of the foreign country |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

43 |

Section 4947(a)(1) nonexempt charitable trusts filing Form |

|

|||||||

|

and enter the amount of |

. . . . |

43 |

|

|

|

|

||

|

|

|

|

|

|

|

|

Yes |

No |

44a |

Did the organization maintain any donor advised funds during the year? If “Yes,” Form 990 must be |

|

|

|

|

||||

|

completed instead of Form |

|

44a |

|

|||||

bDid the organization operate one or more hospital facilities during the year? If “Yes,” Form 990 must be

completed instead of Form |

44b |

c Did the organization receive any payments for indoor tanning services during the year? |

44c |

dIf “Yes” to line 44c, has the organization filed a Form 720 to report these payments? If “No,” provide an

explanation in Schedule O |

44d |

45a Did the organization have a controlled entity within the meaning of section 512(b)(13)? |

45a |

bDid the organization receive any payment from or engage in any transaction with a controlled entity within the meaning of section 512(b)(13)? If “Yes,” Form 990 and Schedule R may need to be completed instead of

Form |

45b |

Form

Form |

Page 4 |

46Did the organization engage, directly or indirectly, in political campaign activities on behalf of or in opposition to candidates for public office? If “Yes,” complete Schedule C, Part I . . . . . . . . . . . . .

Yes No

46

Part VI Section 501(c)(3) Organizations Only

All section 501(c)(3) organizations must answer questions

Check if the organization used Schedule O to respond to any question in this Part VI . . . . . . . . .

Yes No

47Did the organization engage in lobbying activities or have a section 501(h) election in effect during the tax

|

year? If “Yes,” complete Schedule C, Part II |

47 |

48 |

Is the organization a school as described in section 170(b)(1)(A)(ii)? If “Yes,” complete Schedule E . . . . |

48 |

49a |

Did the organization make any transfers to an exempt |

49a |

b |

If “Yes,” was the related organization a section 527 organization? |

49b |

50Complete this table for the organization’s five highest compensated employees (other than officers, directors, trustees, and key employees) who each received more than $100,000 of compensation from the organization. If there is none, enter “None.”

|

(b) Average |

(c) Reportable |

(d) Health benefits, |

(e) Estimated amount of |

|

(a) Name and title of each employee |

contributions to employee |

||||

hours per week |

compensation |

||||

benefit plans, and deferred |

other compensation |

||||

|

devoted to position |

(Forms |

|||

|

|

|

compensation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f Total number of other employees paid over $100,000 . . . .

51Complete this table for the organization’s five highest compensated independent contractors who each received more than $100,000 of compensation from the organization. If there is none, enter “None.”

(a)Name and business address of each independent contractor

(b)Type of service

(c)Compensation

d Total number of other independent contractors each receiving over $100,000 . .

52Did the organization complete Schedule A? Note: All section 501(c)(3) organizations must attach a completed Schedule A . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Yes

No

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than officer) is based on all information of which preparer has any knowledge.

Sign

Here

Paid

Preparer

Use Only

|

F |

|

|

|

|

|

|

|

|

|

|

|

Signature of officer |

|

|

|

|

Date |

|

|

|

||||

|

F |

|

|

|

|

|

|

|

|

|

|

|

Type or print name and title |

|

|

|

|

|

|

|

|

|

|

||

|

Print/Type preparer’s name |

|

Preparer’s signature |

|

Date |

|

Check |

if |

|

PTIN |

||

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

Firm’s EIN |

|

|

|

|||

|

Firm’s address |

|

|

|

|

Phone no. |

|

|

|

|||

May the IRS discuss this return with the preparer shown above? See instructions . . . . . . . . . .

Yes

No

Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS 990-EZ form is used by tax-exempt organizations to report their financial activities. |

| Eligibility | Organizations with gross receipts less than $200,000 and total assets under $500,000 can file this form. |

| Filing Deadline | The 990-EZ must be filed by the 15th day of the 5th month after the end of the organization’s fiscal year. |

| Extensions | Organizations can apply for a 6-month extension using Form 8868. |

| State Requirements | Some states require a copy of the 990-EZ for state income tax filings; check your specific state's requirements. |

| Public Disclosure | The completed 990-EZ form is publicly available and should be disclosed upon request. |

| Penalty for Not Filing | Organizations that fail to file the form may face penalties and risk losing their tax-exempt status. |

| Schedule A Attachment | If the organization is a charity, it must attach Schedule A to the 990-EZ to maintain its tax-exempt status. |

| Tax Identification Number | Every organization must provide its Employer Identification Number (EIN) on the form. |

Filling out the IRS 990-EZ form requires careful attention to detail and accuracy. Ensuring all necessary information is provided will ease the submission process. Here are the steps to effectively fill out the form.

What is the IRS 990-EZ form?

The IRS 990-EZ form is a short version of the IRS Form 990, which is used by tax-exempt organizations to report their annual financial information. It is specifically designed for organizations with gross receipts under a certain threshold, making it easier to file than the full Form 990.

Who needs to file the 990-EZ form?

What is the deadline for filing the IRS 990-EZ form?

The IRS 990-EZ form is due on the 15th day of the 5th month after the end of the organization's tax year. For most organizations that operate on a calendar basis, this means the form is typically due on May 15th. Extensions may be requested using Form 8868.

What information is required on the 990-EZ form?

The form requires information such as the organization's mission, a summary of revenue and expenses, a detailed list of assets, and a report on contributions and grants. It also includes questions about the governance, management, and any changes that occurred during the tax year.

Can electronic filing be done for the 990-EZ form?

What are the penalties for not filing the 990-EZ?

What can organizations do if they miss the filing deadline?

Is there a difference between the 990-EZ and 990-N forms?

How can an organization find assistance with completing the 990-EZ form?

Omitting Financial Information: Many organizations fail to include comprehensive financial data. This omission can lead to discrepancies in reporting income and expenses.

Incorrect or Missing Employer Identification Number (EIN): Some filers do not accurately enter their EIN. This error can cause complications with the IRS and may delay processing.

Inaccurate Description of Activities: A vague or incorrect description of the organization's mission and activities can mislead the IRS. Clarity is crucial for accurately representing your nonprofit's purpose.

Failure to Report Changes in Leadership: Changes in officers or board members must be reported on the form. Failing to do so may raise questions about governance and compliance.

Neglecting to Sign and Date the Return: A common oversight is forgetting to sign and date the form. An unsigned form is considered incomplete and may be rejected.

Forgetting to Attach Required Schedules: Certain organizations need to include additional schedules along with Form 990-EZ. Not providing these attachments can lead to an incomplete filing.

Misclassifying Income or Expenses: Misunderstanding what qualifies as income or an expense can result in incorrect reporting. This misclassification potentially affects the organization's tax status.

The IRS 990-EZ form is a crucial document for many organizations, primarily those classified as tax-exempt by the IRS. Alongside this form, several other documents are frequently utilized to provide a comprehensive overview of an organization’s financial health and compliance status. Below is a list of commonly associated forms and documents.

Accurate completion and submission of these documents ensure compliance with IRS regulations and demonstrate transparency in financial activities. Organizations should understand the necessity of each form and ensure they are filed correctly and on time to maintain their tax-exempt status.

The IRS 990 form is the standard annual reporting document that tax-exempt organizations use to provide information about their financial activities. Similar to the 990-EZ, the 990 is a more detailed form that larger organizations must file. Both forms require organizations to report income, expenses, and program services, helping to maintain transparency and accountability. While the 990-EZ is tailored for smaller organizations, the 990 captures a comprehensive view of an organization's financial standing.

The IRS 990-PF form serves as an annual return for private foundations. Like the 990-EZ, it includes financial information and details on grants made during the year. The commonality lies in the objective of maintaining public trust through disclosure of financial activities. Private foundations use the 990-PF to comply with tax regulations, while smaller non-profits use the 990-EZ, ensuring both are committed to public accountability.

The IRS 501(c)(3) application is crucial for organizations seeking tax-exempt status. It is similar to the 990-EZ because it outlines essential financial and operational information. While the 501(c)(3) application is the initial step for obtaining tax-exempt status, the 990-EZ acts as a follow-up, providing ongoing financial transparency. Both documents encourage organizations to uphold their mission and remain accountable to the public.

The state-level charity registration forms are required for organizations soliciting donations within specific states. These forms resemble the 990-EZ in that they require financial data and descriptions of programs. They serve the same purpose: ensuring that organizations are transparent about their use of funds and that they adhere to state regulations regarding fundraising activities. Both types of documents help protect the interests of donors and the public.

The IRS Form 1023 is the application for recognition of exemption from federal income tax for 501(c)(3) organizations. The 1023 and the 990-EZ share a focus on the organization's finances and programs. The 1023 establishes the organization's eligibility for tax-exempt status, while the 990-EZ ensures continued compliance by providing a financial snapshot of the organization’s operations annually. Both forms contribute to maintaining a clear public record of nonprofit activities.

The IRS Schedule A is an attachment for the 990 and 990-EZ forms that provides additional information about the organization’s public charity status and financial activities. It complements the 990-EZ by detailing the sources of funding and how they are utilized. Like the 990-EZ, Schedule A’s purpose is to ensure transparency and proper classification of the organization’s charitable status, reinforcing the commitment to integrity in operations.

The IRS Form 990-T is used by tax-exempt organizations to report unrelated business income (UBI). Similar to the 990-EZ, it requires financial disclosures, but focuses specifically on income that does not directly relate to the organization’s tax-exempt purpose. By filing both forms, an organization demonstrates its adherence to tax rules while maintaining transparency in its overall financial reporting.

The IRS Form 8872 is required for organizations engaged in political activities and is similar to the 990-EZ in that both require transparency regarding funding sources and expenditures. While the 990-EZ focuses on nonprofit activities, the 8872 ensures organizations involved in political spending disclose their activities to the public, thus promoting accountability and ethical fundraising practices.

The IRS Form 990-N, also known as the e-Postcard, is a simplified version for small tax-exempt organizations with gross receipts under a certain threshold. Like the 990-EZ, the 990-N keeps organizations accountable by requiring them to report basic financial information annually. Although it is less detailed, both forms aim to promote transparency and maintain a public record of each organization’s financial health.

The IRS Annual Information Return for Non-Profits (Form 990-Short Form) has been developed for certain organizations that qualify for a streamlined reporting process. Much like the 990-EZ, the short form requires essential information about the organization’s finances while relieving smaller entities from the burden of cumbersome reporting. Both forms reflect a commitment to transparency and responsible management within the nonprofit sector.

Filling out the IRS 990-EZ form can seem daunting, but keeping a few simple guidelines in mind can make the process smoother. Below are some essential dos and don'ts to consider.

This form is designed for smaller tax-exempt organizations. If your gross receipts are under $200,000 and total assets are below $500,000, you can file the 990-EZ.

Most nonprofits are required to file either a 990 or 990-EZ every year. Failure to file can lead to penalties or loss of tax-exempt status.

While it includes some financial information, the 990-EZ is simpler than the full IRS Form 990. It has streamlined reporting requirements.

Even if there was no income, organizations must still file the 990-EZ or another appropriate form to maintain compliance with IRS rules.

Nonprofits must file the 990-EZ by the 15th day of the fifth month after their fiscal year ends. Extensions may be available, but deadlines are crucial.

While many charities use it, other types of tax-exempt organizations, like social clubs and certain educational entities, may also file the 990-EZ.

All 990-EZ forms are publicly available. Interested individuals can view them online through various nonprofit databases for transparency.

The IRS 990-EZ form is an important document for small tax-exempt organizations. Here are some key takeaways to consider when filling it out and using it:

Filling out the IRS 990-EZ form can seem daunting, but paying close attention to these key areas will help ensure compliance and proper reporting for your organization.