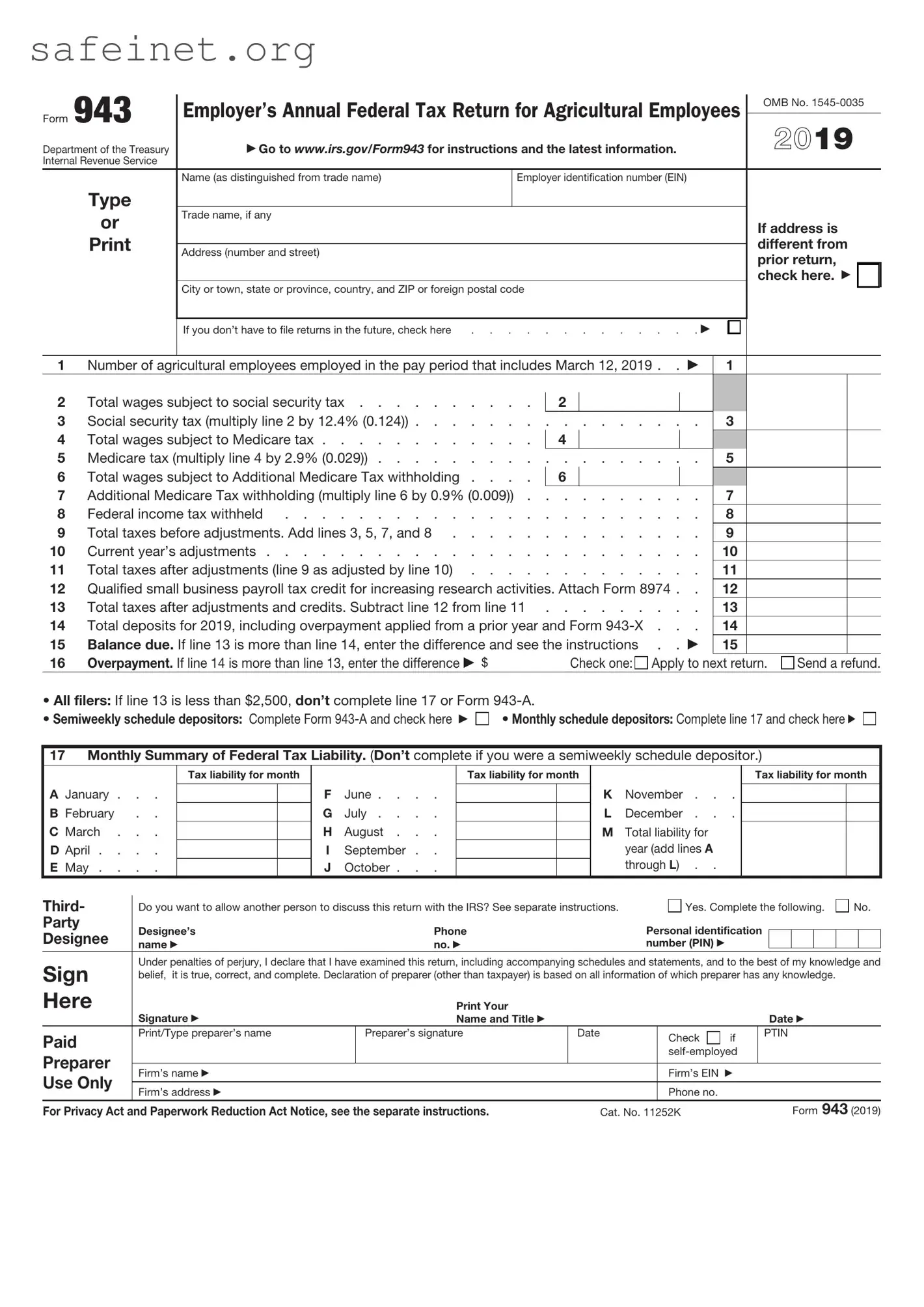

The IRS 943 form plays a crucial role in the realm of agriculture and farming-related businesses. Designed specifically for employers in these sectors, it is used to report annual federal income tax withheld from wages and the corresponding social security and Medicare taxes. Instead of being a burden, this form provides farmers and agricultural businesses with a streamlined process for fulfilling their tax obligations, ensuring compliance while allowing them to focus more on their operations. As an annual filing, the IRS 943 form must be submitted by January 31 of the following year, and it often leads to questions surrounding due dates, filing requirements, and the information needed to complete it accurately. Understanding how to properly use the form, while recognizing its importance in maintaining proper tax records, can bring peace of mind to agricultural employers. By submitting the IRS 943 form, farmers can also contribute to vital social programs that benefit their workers and the community at large.

Form 943 |

Employer’s Annual Federal Tax Return for Agricultural Employees |

OMB No. |

|||||||||||

|

|

|

|

||||||||||

|

2019 |

|

|||||||||||

Department of the Treasury |

Go to www.irs.gov/Form943 for instructions and the latest information. |

|

|

|

|||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (as distinguished from trade name) |

|

Employer identification number (EIN) |

|

|

|

|

|

||||

|

Type |

|

|

|

|

|

|

|

|

|

|

|

|

|

or |

Trade name, if any |

|

|

|

|

|

|

|

If address is |

|||

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

different from |

||||

|

Address (number and street) |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

prior return, |

|

||

|

|

|

|

|

|

|

|

|

|

check here. |

|

||

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

If you don’t have to file returns in the future, check here |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||

1 |

Number of agricultural employees employed in the pay period that includes March 12, 2019 . . |

1 |

|

|

|

|

|||||||

2 |

Total wages subject to social security tax |

. . |

|

2 |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||||

3 |

Social security tax (multiply line 2 by 12.4% (0.124)) |

3 |

|

|

|

|

|||||||

4 |

Total wages subject to Medicare tax |

. . |

|

4 |

|

|

|

|

|

|

|

||

5 |

Medicare tax (multiply line 4 by 2.9% (0.029)) |

5 |

|

|

|

|

|||||||

6 |

Total wages subject to Additional Medicare Tax withholding . . |

. . |

|

6 |

|

|

|

|

|

|

|

||

7 |

Additional Medicare Tax withholding (multiply line 6 by 0.9% (0.009)) |

7 |

|

|

|

|

|||||||

8 |

Federal income tax withheld |

8 |

|

|

|

|

|||||||

9 |

Total taxes before adjustments. Add lines 3, 5, 7, and 8 |

9 |

|

|

|

|

|||||||

10 |

Current year’s adjustments |

10 |

|

|

|

|

|||||||

11 |

Total taxes after adjustments (line 9 as adjusted by line 10) |

11 |

|

|

|

|

|||||||

12 |

Qualified small business payroll tax credit for increasing research activities. Attach Form 8974 . . |

12 |

|

|

|

|

|||||||

13 |

Total taxes after adjustments and credits. Subtract line 12 from line 11 |

13 |

|

|

|

|

|||||||

14 |

Total deposits for 2019, including overpayment applied from a prior year and Form |

14 |

|

|

|

|

|||||||

15 |

Balance due. If line 13 is more than line 14, enter the difference and see the instructions . . |

15 |

|

|

|

|

|||||||

16 |

Overpayment. If line 14 is more than line 13, enter the difference $ |

|

|

|

Check one: Apply to next return. |

Send a refund. |

|||||||

• All filers: If line 13 is less than $2,500, don’t complete line 17 or Form |

|

|

|

|

|

|

|

|

|

||||

• Semiweekly schedule depositors: Complete Form |

• Monthly schedule depositors: Complete line 17 and check here |

||||||||||||

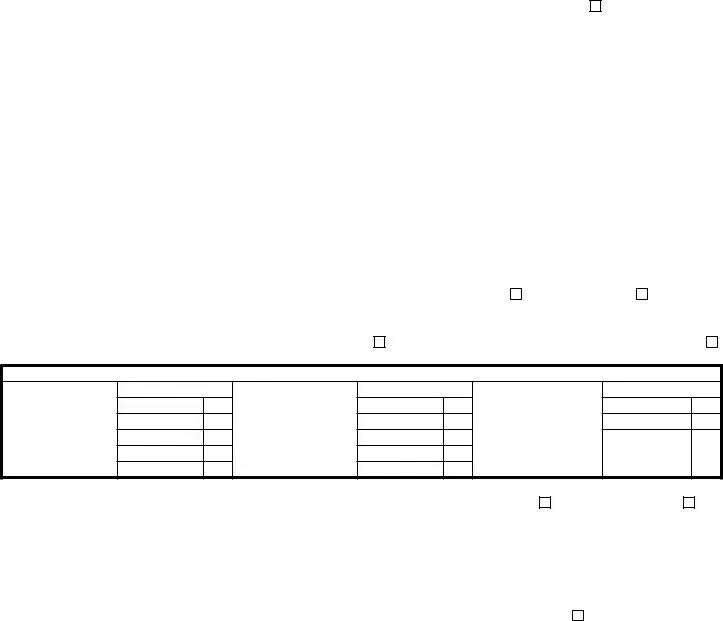

17Monthly Summary of Federal Tax Liability. (Don’t complete if you were a semiweekly schedule depositor.)

A January . . .

B February . . C March . . .

D April . . . .

E May . . . .

Tax liability for month

F |

June . . . . |

G |

July . . . . |

H |

August . . . |

I |

September . . |

J |

October . . . |

Tax liability for month

K November . . .

L December . . .

MTotal liability for year (add lines A

through L) . .

Tax liability for month

Third- |

Do you want to allow another person to discuss this return with the IRS? See separate instructions. |

|

Yes. Complete the following. |

No. |

|||||||||

Party |

Designee’s |

Phone |

|

Personal identification |

|

|

|

|

|

|

|||

Designee |

name |

no. |

|

number (PIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Sign |

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and |

||||||||||||

belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|||||||||||

Here |

Signature |

Print Your |

|

|

|

|

|

|

|

|

|

|

|

|

Name and Title |

|

|

|

|

|

|

Date |

|

|

|||

Paid |

Print/Type preparer’s name |

Preparer’s signature |

Date |

|

Check |

if |

|

PTIN |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

|

|

|

|

|

|

Use Only |

|

|

|

|

|

|

|

|

|

|

|

||

Firm’s address |

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11252K |

|

|

|

|

Form 943 (2019) |

|||||||

Form

Purpose of Form

Complete Form

Making Payments With Form 943

To avoid a penalty, make your payment with your 2019 Form 943 only if:

•Your total taxes for the year (Form 943, line 13) are less than $2,500 and you’re paying in full with a timely filed return, or

Specific Instructions

Box

Box

Box

•You’re a monthly schedule depositor making a payment in accordance with the Accuracy of Deposits Rule. See section 7 of Pub. 51 for details. In this case, the amount of your payment may be $2,500 or more.

Otherwise, you must make deposits by electronic funds transfer. See section 7 of Pub. 51 for deposit instructions. Don’t use Form

FUse Form

CAUTION Form 943 that should’ve been deposited, you may be subject to a penalty. See Deposit Penalties in section 7 of Pub. 51.

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your EIN, “Form 943,” and “2019” on your check or money order. Don’t send cash. Don’t staple Form

•Detach Form

Note: You must also complete the entity information above line 1 on Form 943.

Detach Here and Mail With Your Payment and Form 943. |

||||||||||

Form |

|

|

|

|

Payment Voucher |

|

OMB No. |

|||

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Department of the Treasury |

|

|

|

Don’t staple this voucher or your payment to Form 943. |

|

|

2019 |

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

||

1 Enter your employer identification number (EIN). |

2 |

|

Enter the amount of your payment . . . |

|

|

Dollars |

|

Cents |

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

Make your check or money order payable to “United States Treasury” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

Enter your business name (individual name if sole proprietor). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter your address. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter your city or town, state or province, country, and ZIP or foreign postal code. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS Form 943 is designed for agricultural employers to report annual wages and taxes for farm workers. |

| Filing Frequency | Form 943 must be filed annually by employers who pay agricultural workers. |

| Filing Deadline | Employers must submit Form 943 by January 31 of the year following the tax year. |

| Wages Covered | This form covers wages paid to farm employees, including those who work on a contract basis. |

| Form Availability | IRS Form 943 can be obtained from the IRS website or local IRS offices. |

| State-Specific Forms | Some states require additional forms to comply with state labor laws; regulations vary by state. |

| Penalties | Failure to file Form 943 on time can result in penalties, including fines for the employer. |

| Record Keeping | Employers are required to maintain payroll records for at least four years to substantiate claims on Form 943. |

| Guidance | The IRS provides instructions for completing Form 943, which helps ensure correct and complete filings. |

Completing your IRS 943 form is an important step in ensuring compliance with federal tax regulations related to agricultural employers. By carefully following the instructions, you can accurately report employment taxes for your agricultural workers. With your information ready, you can proceed with filling out the form.

What is the IRS Form 943?

The IRS Form 943, Employer's Annual Federal Tax Return for Agricultural Employees, is used by employers in the agricultural industry to report wages paid to their employees. This form also includes details about federal income tax withheld, Social Security taxes, and Medicare taxes. Employers must file this form annually if they pay agricultural employees $150 or more in wages during the year, or if they are required to withhold federal income tax for any employee.

Who needs to file Form 943?

Form 943 must be filed by agricultural employers who meet specific criteria. If an employer pays agricultural employees wages of $150 or more, or if they have a significant amount of federal income tax withheld from any employee's wages, they are required to file this form. This requirement applies regardless of whether the employer operates as an individual, corporation, or partnership.

When is Form 943 due?

The filing deadline for Form 943 is typically January 31 of the year following the end of the calendar year. However, if January 31 falls on a weekend or holiday, the due date may be extended to the next business day. Employers must ensure they submit their form on time to avoid any potential penalties associated with late filing.

How do I file Form 943?

Incorrect employer identification number (EIN): Many people enter an incorrect or invalid EIN, leading to processing delays and potential penalties.

Missing signatures: Failing to sign the form can result in the IRS rejecting your submission. Both the responsible official and the preparer must provide their signatures.

Calculation errors: Simple arithmetic mistakes in total taxes due or related fields can lead to inaccurate submissions and unexpected liabilities.

Wrong tax year indicated: Submitting for the wrong tax year can complicate compliance. Make sure the tax year matches the year for which you are reporting.

Not including supporting documentation: Some filers forget to attach necessary schedules or documentation, which could delay processing.

Omitting employee information: Missing details about employees, such as Social Security numbers or names, can hinder the accuracy of the form and lead to complications.

Failure to follow specific instructions: Not adhering to the detailed guidelines provided by the IRS can lead to incorrect submissions. Each line has specific instructions that must be followed.

Neglecting to review the form: Skipping a final review can result in overlooked errors. It's important to double-check all entries before submission.

The IRS 943 form is used by agricultural employers to report and pay payroll taxes for farmworkers. Along with this form, several other documents may be necessary to ensure compliance with tax regulations. Here are some commonly associated forms and documents that you might encounter:

Understanding these forms and their purposes can help ensure that agricultural businesses remain compliant with federal tax obligations. Each document plays a part in the bigger picture of payroll and tax reporting, making it important to keep them organized and accessible.

The IRS 941 form is a quarterly tax return used by employers to report income taxes withheld from employees' paychecks, along with Medicare and Social Security taxes. This form, like IRS 943, is important for ensuring compliance with tax regulations. While IRS 943 is specifically for agricultural employers reporting annual taxes, IRS 941 caters to a broader range of employers and is submitted more frequently throughout the year.

The IRS W-2 form summarizes an employee's annual wages and the amount of taxes withheld. Employers use this document to provide employees with a comprehensive overview of their earnings and taxes for the year. Similar to the IRS 943, the W-2 is essential for tax filing, but it focuses on individual employee information rather than the tax liabilities of the employer.

The IRS W-3 form is a transmittal form that accompanies the W-2 filings. It aggregates the total earnings and tax withheld for all employees. Like IRS 943, which aggregates annual tax information for agricultural employers, the W-3 provides a summary to the IRS, ensuring accurate reporting of total wages and tax contributions.

The IRS 1099 form is used to report various types of income other than wages, salaries, or tips. This form is crucial for independent contractors and other non-employees. While IRS 943 applies to employers in the agriculture sector and focuses on employment taxes, the 1099 series serves a different purpose in reporting payments made to individuals who are not classified as employees.

The IRS 940 form serves as an annual report for federal unemployment taxes. Similar to IRS 943, which addresses specific taxes related to agricultural payroll, the 940 form helps employers report their contributions towards federal unemployment insurance. Both forms are pivotal for compliance with federal tax regulations, albeit for different funding purposes.

The IRS Schedule H is an attachment for filers who employ household employees and need to report taxes on their wages. While both Schedule H and IRS 943 involve reporting employment taxes, Schedule H is targeted towards domestic staff, while 943 caters to agricultural workers, highlighting the different employment contexts addressed by these documents.

The IRS 1065 form is filed by partnerships to report income, deductions, and credits. This form does not focus primarily on employment taxes like IRS 943 but is important for tax compliance among partnerships. Both forms share the objective of ensuring accurate reporting to the IRS, but they cover different types of business structures and tax obligations.

The IRS 1120 form is utilized by corporations to report their income, gains, losses, deductions, and credits. Like IRS 943, it is essential for tax compliance; however, the 1120 form pertains to corporate entities rather than agricultural employers. Both documents play a vital role in the broader context of tax reporting and obligation fulfillment.

The IRS Form 5558 is used to apply for an extension of time to file certain employee benefit plan returns. This form is similar to IRS 943 in that both involve deadlines and filings concerning certain fiscal responsibilities. However, Form 5558 specifically addresses retirement and employee benefit plans, while IRS 943 is focused on agricultural employment taxes.

When filling out the IRS Form 943, there are several important considerations to ensure accuracy and compliance. The following list outlines key dos and don’ts that will help guide you through the process.

The IRS Form 943 is crucial for agricultural employers, yet many misconceptions surround it. Understanding these misconceptions can prevent mistakes and ensure compliance with tax obligations. Here are eight common misunderstandings about Form 943:

By clarifying these misconceptions, employers can better navigate their tax responsibilities and ensure that they comply with IRS regulations regarding agricultural employment.

When dealing with the IRS 943 form, individuals and organizations involved in agricultural employment must pay close attention to specific details to ensure compliance with federal regulations. Below are some key takeaways that encapsulate the essentials of filling out and using this form.

By keeping these key points in mind, employers can navigate the complexities of the IRS 943 form more effectively, ensuring compliance and promoting good financial practices within their agricultural business.