The IRS 941-X form is an essential tool for employers seeking to correct errors on their previously filed IRS Form 941, which reports payroll taxes withheld from employee wages, as well as the employer’s portion of Social Security and Medicare taxes. This form is particularly beneficial for businesses that have discovered inaccuracies in their tax filings, whether those errors pertain to the amount of wages reported, tax payments submitted, or eligibility for certain tax credits. By allowing for amendments to prior quarterly tax returns, the 941-X not only safeguards employers from potential penalties but also ensures compliance with federal tax obligations. Completing this form requires attention to detail, as it involves providing specific information regarding the original errors and the corrections needed. Moreover, understanding the timeline for making these amendments is crucial; employers must file the 941-X within a specific period to ensure adjustments are accepted by the IRS. This guide will walk you through the intricacies of the IRS 941-X form, from its purpose and significance to practical tips for its completion, thus empowering you to navigate the correction process with confidence.

Form

(Rev. October 2020) |

Department of the Treasury — Internal Revenue Service |

OMB No. |

Employer identification number |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Number |

Street |

|

|

|

Suite or room number |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign country name |

Foreign province/county |

Foreign postal code |

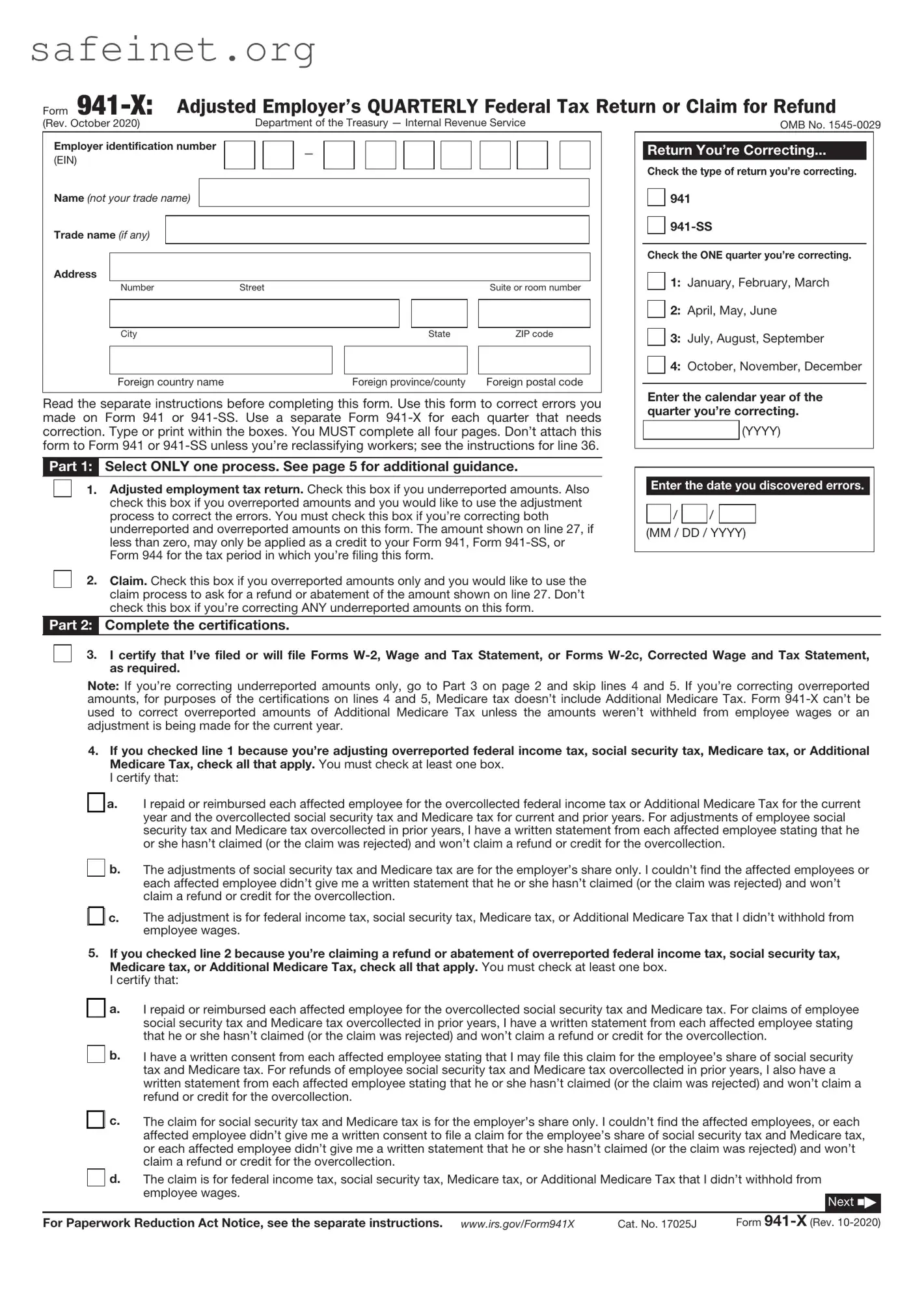

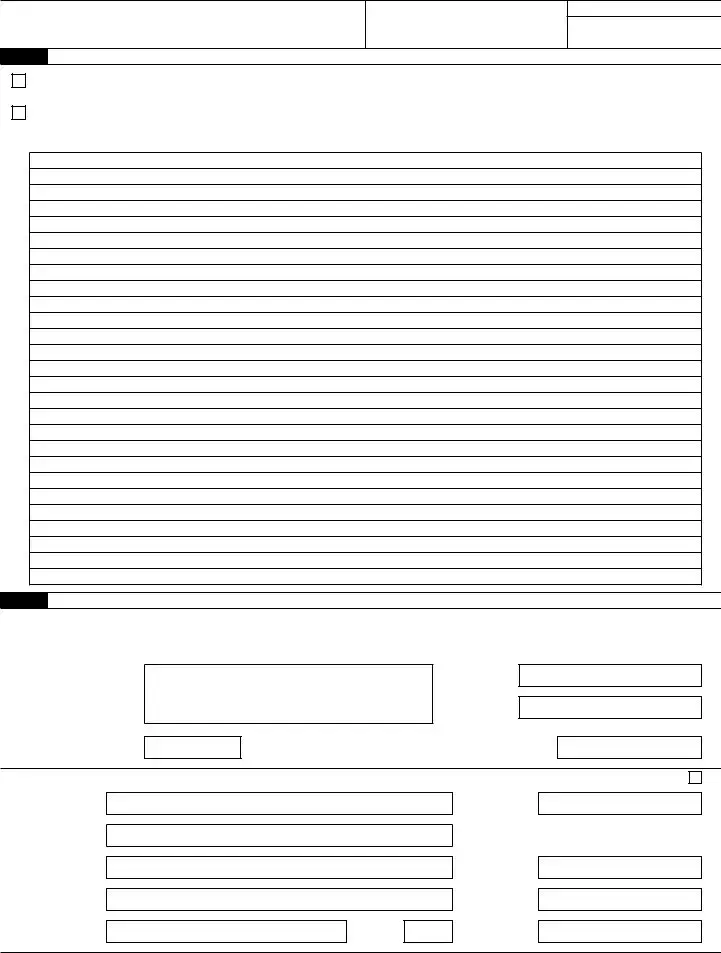

Read the separate instructions before completing this form. Use this form to correct errors you made on Form 941 or

Return You’re Correcting...

Check the type of return you’re correcting.

941

Check the ONE quarter you’re correcting.

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Enter the calendar year of the quarter you’re correcting.

(YYYY)

Part 1: Select ONLY one process. See page 5 for additional guidance.

1. Adjusted employment tax return. Check this box if you underreported amounts. Also check this box if you overreported amounts and you would like to use the adjustment process to correct the errors. You must check this box if you’re correcting both underreported and overreported amounts on this form. The amount shown on line 27, if less than zero, may only be applied as a credit to your Form 941, Form

2. Claim. Check this box if you overreported amounts only and you would like to use the claim process to ask for a refund or abatement of the amount shown on line 27. Don’t check this box if you’re correcting ANY underreported amounts on this form.

Enter the date you discovered errors.

/ |

|

/ |

(MM / DD / YYYY)

Part 2: Complete the certifications.

3. I certify that I’ve filed or will file Forms

Note: If you’re correcting underreported amounts only, go to Part 3 on page 2 and skip lines 4 and 5. If you’re correcting overreported amounts, for purposes of the certifications on lines 4 and 5, Medicare tax doesn’t include Additional Medicare Tax. Form

4.If you checked line 1 because you’re adjusting overreported federal income tax, social security tax, Medicare tax, or Additional Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected federal income tax or Additional Medicare Tax for the current year and the overcollected social security tax and Medicare tax for current and prior years. For adjustments of employee social security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

b. The adjustments of social security tax and Medicare tax are for the employer’s share only. I couldn’t find the affected employees or each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

c. The adjustment is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from employee wages.

5.If you checked line 2 because you’re claiming a refund or abatement of overreported federal income tax, social security tax, Medicare tax, or Additional Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected social security tax and Medicare tax. For claims of employee social security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

|

|

b. |

I have a written consent from each affected employee stating that I may file this claim for the employee’s share of social security |

|||

|

|

|

tax and Medicare tax. For refunds of employee social security tax and Medicare tax overcollected in prior years, I also have a |

|||

|

|

|

written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a |

|||

|

|

|

refund or credit for the overcollection. |

|

|

|

|

|

c. |

The claim for social security tax and Medicare tax is for the employer’s share only. I couldn’t find the affected employees, or each |

|||

|

|

|||||

|

|

|

affected employee didn’t give me a written consent to file a claim for the employee’s share of social security tax and Medicare tax, |

|||

|

|

|

or each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t |

|||

|

|

|

claim a refund or credit for the overcollection. |

|

|

|

|

|

d. |

The claim is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from |

|||

|

|

|

employee wages. |

|

|

|

|

|

|

|

|

Next N |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see the separate instructions. www.irs.gov/Form941X |

Cat. No. 17025J |

Form |

||||

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 3: Enter the corrections for this quarter. If any line doesn’t apply, leave it blank.

Column 1

Column 2

Column 3 |

Column 4 |

6. |

Wages, tips, and other |

|

compensation (Form 941, line 2) |

7. |

Federal income tax withheld |

|

from wages, tips, and other |

|

compensation (Form 941, line 3) |

8. |

Taxable social security wages |

|

(Form 941 or |

|

Column 1) |

Total corrected amount (for ALL employees)

.

.

.

Amount originally reported or as previously corrected

— (for ALL employees) |

||

— |

|

. |

— |

|

|

|

. |

|

— |

|

|

|

. |

|

=

=

=

=

Difference

(If this amount is a negative number, use a minus sign.)

.

.

.

Tax correction

Use the amount in Column 1 when you prepare your Forms

Copy Column |

|

. |

3 here |

|

|

|

|

|

× 0.124* = |

|

. |

9. |

Qualified sick leave wages |

|

(Form 941 or |

|

Column 1) |

.

— |

|

. |

|

|

|

* If you’re correcting your employer share only, use 0.062. See instructions.

= |

. |

× 0.062 = |

. |

|

10.Qualified family leave wages (Form 941 or

11.Taxable social security tips (Form 941 or

.

.

—

—

.

.

= |

|

|

. |

× |

0.062 = |

|

. |

|

|

|

|||||

= |

|

|

|

|

|

|

|

|

. |

× |

0.124* = |

|

. |

||

|

|

|

|||||

* If you’re correcting your employer share only, use 0.062. See instructions.

12.Taxable Medicare wages & tips (Form 941 or

.

—

.

= |

. |

× 0.029* = |

. |

|

* If you’re correcting your employer share only, use 0.0145. See instructions.

13.Taxable wages & tips subject to Additional Medicare Tax withholding (Form 941 or

14.Section 3121(q) Notice and

15.Tax adjustments (Form 941 or

16.Qualified small business payroll tax credit for increasing research activities (Form 941 or

17.Nonrefundable portion of credit for qualified sick and family leave wages (Form 941 or

.

.

.

.

.

—

—

—

—

—

. |

= |

. |

× 0.009* = |

. |

|

* Certain wages and tips reported in Column 3 shouldn’t be multiplied by 0.009. See instructions.

|

. |

= |

|

. |

Copy Column |

|

. |

|

|

|

|

|

3 here |

|

|||

|

|

= |

|

|

Copy Column |

|

|

|

|

. |

|

. |

|

. |

|||

|

|

|

|

3 here |

|

|||

|

|

|

= |

|

|

See |

|

|

|

. |

|

|

. |

|

. |

||

|

|

|

|

instructions |

|

|||

|

|

|

= |

|

|

See |

|

|

|

. |

|

|

. |

|

. |

||

|

|

|

|

instructions |

|

|||

18.Nonrefundable portion of employee retention credit (Form 941 or

19.Special addition to wages for federal income tax

20.Special addition to wages for social security taxes

21.Special addition to wages for Medicare taxes

22.Special addition to wages for Additional Medicare Tax

.

.

.

.

.

—

—

—

—

—

.

.

.

.

.

=

=

=

=

=

.

.

.

.

.

See instructions

See instructions

See instructions

See instructions

See instructions

.

.

.

.

.

23.Combine the amounts on lines 7 through 22 of Column 4

24.Deferred amount of social

security tax* (Form 941 or |

. |

|

|

|

25.Refundable portion of credit for

qualified sick and family leave |

. |

wages (Form 941 or |

|

|

|

13c) |

|

.

—

—

. . . . . . . . . . . . . . . . . .

|

. |

= |

|

|

. |

See |

|

|

|

instructions |

|||

|

|

= |

|

|

|

See |

|

. |

|

. |

|||

|

|

|

instructions |

|||

.

.

.

Next N

Page 2 |

Form |

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 3: Enter the corrections for this quarter. If any line doesn’t apply, leave it blank. (continued)

Column 1

Total corrected amount (for ALL employees)

26.Refundable portion of employee

retention credit (Form 941 or |

. |

|

Column 2

Amount originally reported or as previously corrected

—(for ALL employees)

—.

=

=

Column 3

Difference

(If this amount is a negative number, use a minus sign.)

.

See instructions

Column 4

Tax correction

.

27. Total. Combine the amounts on lines 23 through 26 of Column 4 . . . . . . . . . . . . . . . . .

If line 27 is less than zero:

.

•If you checked line 1, this is the amount you want applied as a credit to your Form 941 or

•If you checked line 2, this is the amount you want refunded or abated.

If line 27 is more than zero, this is the amount you owe. Pay this amount by the time you file this return. For information on how to pay, see Amount you owe in the instructions.

28.Qualified health plan expenses allocable to qualified sick leave wages (Form 941 or

.

—

.

=

.

29.Qualified health plan expenses allocable to qualified family leave wages (Form 941 or

30.Qualified wages for the employee retention credit (Form 941 or

31.Qualified health plan expenses allocable to wages reported on Form 941 or

32.Credit from Form

33a. Qualified wages paid March 13 through March 31, 2020, for the employee retention credit (use this line to correct only the second quarter of 2020) (Form 941 or

33b. Deferred amount of the employee share of social security tax included on Form 941 or

34.Qualified health plan expenses allocable to wages reported on Form 941 or

.

.

.

.

.

.

.

—

—

—

—

—

—

—

.

.

.

.

.

.

.

=

=

=

=

=

=

=

.

.

.

.

.

.

.

Next N

Page 3 |

Form |

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 4: Explain your corrections for this quarter.

35. Check here if any corrections you entered on a line include both underreported and overreported amounts. Explain both

your underreported and overreported amounts on line 37.

36. Check here if any corrections involve reclassified workers. Explain on line 37.

37.You must give us a detailed explanation of how you determined your corrections. See the instructions.

Part 5: Sign here. You must complete all four pages of this form and sign it.

Under penalties of perjury, I declare that I have filed an original Form 941 or Form

✗Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Check if you’re

PTIN

Date |

/ |

/ |

EIN

Address

Phone

City

State

ZIP code

Page 4 |

Form |

Type of errors you’re correcting

Form

Underreported |

Use the adjustment process to correct underreported amounts. |

|

• Check the box on line 1. |

||

amounts |

||

ONLY |

• Pay the amount you owe from line 27 by the time you file Form |

Overreported amounts

ONLY

The process you use depends on when you file Form

If you’re filing Form

Choose either the adjustment process or the claim process to correct the overreported amounts.

Choose the adjustment process if you want the amount shown on line 27 credited to your Form 941, Form

OR

Choose the claim process if you want the amount shown on line 27 refunded to you or abated. Check the box on line 2.

If you’re filing Form |

You must use the claim process to correct the |

WITHIN 90 days of the |

overreported amounts. Check the box on line 2. |

expiration of the period of |

|

limitations on credit or refund |

|

for Form 941 or Form |

|

BOTH underreported and overreported amounts

The process you use depends on when you file Form

If you’re filing Form

Choose either the adjustment process or both the adjustment process and the claim process when you correct both underreported and overreported amounts.

Choose the adjustment process if combining your underreported amounts and overreported amounts results in a balance due or creates a credit that you want applied to Form 941, Form

•File one Form

•Check the box on line 1 and follow the instructions on line 27.

OR

Choose both the adjustment process and the claim process if you want the overreported amount refunded to you or abated.

File two separate forms.

1.For the adjustment process, file one Form

2.For the claim process, file a second Form

If you’re filing Form

You must use both the adjustment process and the claim process.

File two separate forms.

1.For the adjustment process, file one Form

2.For the claim process, file a second Form

Page 5 |

Form |

| Fact Name | Description |

|---|---|

| Purpose | The IRS 941-X form is used to correct errors made on previously filed Form 941, which reports payroll taxes. |

| Who Must File | Employers who have filed Form 941 can file 941-X to amend their payroll tax returns. |

| Filing Deadline | Employers can file Form 941-X within three years from the date they filed the original Form 941. |

| Versioning | The form is updated periodically, so it’s essential to use the most current version available on the IRS website. |

| Types of Corrections | Common corrections include adjustments to wages, tips, and the amount of taxes owed or paid. |

| State-Specific Forms | Some states have their own forms for payroll tax corrections. Review state law for specific requirements. |

| Where to Submit | Form 941-X should be mailed to the IRS address provided on the form instructions based on the state of the employer. |

Completing the IRS 941-X form is an essential step if you need to correct errors on a previously filed Form 941. Taking care in filling out this form can help ensure accurate payroll tax reporting for your business. The following steps will guide you through the process.

After filing the form, keep a copy for your records. It is important to stay informed about any correspondence from the IRS regarding your submission. Patience is advisable, as processing times may vary.

What is the IRS 941-X form?

The IRS 941-X form, officially known as the "Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund," is used by employers to correct errors made on previously filed Form 941. This form allows businesses to amend their original filings, ensuring accurate reporting of employment taxes.

When should I use Form 941-X?

You should use Form 941-X if you discover an error on your previously filed Form 941. Common reasons for filing include corrections to wages, tips, tax withholdings, or any claim for overpayment. It's crucial to file this form to rectify any inaccuracies, as they can affect your tax obligations and potential refunds.

How do I fill out Form 941-X?

Filling out Form 941-X involves a few steps. First, obtain the current version of the form from the IRS website. Next, you'll need specific details about the quarter you are amending. Complete the form by indicating the original amount filed and the corrected amounts. Pay close attention to the instructions provided by the IRS for each section to ensure accuracy.

Are there any deadlines for filing Form 941-X?

Yes, there are deadlines depending on the type of correction you are making. Generally, you have up to three years from the date you filed the original Form 941 or two years from the date you paid the tax to file Form 941-X. It's essential to keep these timelines in mind to avoid any penalties or loss of refund eligibility.

Can I amend multiple quarters with one Form 941-X?

No, you cannot amend multiple quarters on a single Form 941-X. Each quarter needs its own form. This means if you have corrections for multiple quarters, you will have to complete a separate Form 941-X for each one.

What happens after I submit Form 941-X?

After submitting Form 941-X, the IRS will process your amendment. This may take some time, so it’s essential to keep a copy of the submitted form for your records. If a refund is due, it will be issued after the IRS completes its processing, but be prepared for possible delays if additional information is needed.

Will I face a penalty for filing Form 941-X?

Filing Form 941-X itself does not incur penalties; however, if the original error was due to negligence or an intentional disregard of the tax laws, penalties may apply. It is always best to file amendments promptly and accurately to minimize any potential issues.

Where can I get help if I have questions about Form 941-X?

If you have questions about completing Form 941-X or about your specific situation, consider reaching out to a tax professional or the IRS directly. The IRS offers various resources, including publications and assistance lines, to help you navigate the amendment process efficiently.

Incorrect Identification Information: Many people forget to double-check their employer identification number (EIN) and other contact details. Ensure these are accurate to avoid delays in processing your form.

Filing the Wrong Quarter: It's crucial to fill out the form for the correct tax period. Submitting a form for the wrong quarter can lead to significant complications.

Not Using the Latest Version: Using outdated versions of the form can lead to errors. Always download the latest version from the IRS website.

Ignoring Instructions: Each section of the 941-X has specific instructions. Failing to read these can cause mistakes that might require resubmission.

Omitting Required Signatures: Remember to sign the form before submitting it. An unsigned form will be considered invalid.

Incorrect Calculation of Adjustments: Accurate calculations for adjustments are essential. Review your numbers carefully to avoid discrepancies.

Not Keeping Copies: Always retain a copy of the 941-X form for your records. This documentation can prove invaluable for future reference.

Missing Deadline: Submitting the form late can lead to penalties. Stay aware of filing deadlines to keep your business in good standing.

Relying on Memory: It’s tempting to fill out the form from memory, but this often leads to forgetfulness. Always have the relevant documents handy.

Neglecting Other Relevant Forms: Sometimes, you may need to file additional forms alongside the 941-X. Be proactive and ensure you have everything you need.

The IRS 941-X form is essential for employers who need to correct errors on previously filed Form 941. However, several other documents and forms often accompany it to ensure compliance with tax regulations. Here’s a list of related forms that may be necessary when filing the 941-X, along with brief descriptions of each.

By understanding these forms and their purposes, employers can navigate the process of correcting payroll tax errors more effectively. Always ensure that you are utilizing the most current forms and guidelines from the IRS to remain compliant and avoid any complications. If ever in doubt, consulting a tax professional can be a wise step toward clarity and assurance.

The IRS Form 944 is similar to the 941-X in that both are used for reporting payroll taxes. Form 944 is the annual equivalent of the quarterly Form 941. While the 941-X is filed specifically to correct errors on a previously submitted 941, the 944 serves as a method for small employers to report and pay their taxes once a year instead of quarterly. Employers who qualify for Form 944 generally have a smaller payroll, which reduces the frequency of their tax reporting obligations.

Form 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return, shares similarities with the 941-X in that it addresses employer tax responsibilities. While Form 940 focuses specifically on unemployment taxes, both forms require employers to report how much they owe and remit payments to the IRS. Like the 941-X, the 940 can be amended if errors are discovered after initial submission, ensuring that the employer's tax records are accurate.

The IRS Form 1099-MISC is also relevant as it provides a mechanism for reporting payments made to non-employees, similar to how Forms 941 and 941-X deal with employee wages. Both forms require accurate reporting for tax calculation purposes. If a business realizes it has made an error in reporting payments on Form 1099-MISC, it too can be corrected with a separate form, similar to the correction process available with the 941-X.

The W-2 form, used to report wage and tax information for employees, is another document that parallels the purpose of the 941-X. While the W-2 is provided to employees, the information collected feeds back into the IRS reporting system, much like the 941-X corrects previous payroll tax filings. If an employer discovers discrepancies in the wage or tax information provided on a W-2, they must issue a corrected W-2C, demonstrating the ongoing need for accurate reporting, akin to the amendment process for the 941.

The IRS Form 945 is relevant as well, as it is used to report withholding on non-payroll payments, such as certain types of retirement distributions. Both Form 945 and 941-X can be used to amend previously reported amounts. Employers who realize they reported incorrect withholding amounts on the 945 can make necessary corrections using a similar process as with the 941-X amendments, highlighting the importance of maintaining accurate records across different types of tax submissions.

Finally, Form 1040-X, the amendment form for individual income tax returns, can be compared to the 941-X. Both forms serve the primary purpose of correcting previously submitted tax documents. If an individual discovers errors in their income tax return after filing, they use Form 1040-X, much like employers use the 941-X to amend their payroll tax filings. This illustrates the broader system of tax compliance that allows taxpayers to correct mistakes, reinforcing the importance of accurate reporting for both individuals and businesses.

When filling out the IRS 941-X form, accuracy is essential. Here are some dos and don'ts to keep in mind:

Filling out and using the IRS 941-X form can seem complex, but understanding its key aspects can facilitate the process. Here are some important takeaways to keep in mind:

Understanding these points will enhance your ability to use IRS Form 941-X effectively and ensure compliance with federal tax regulations.