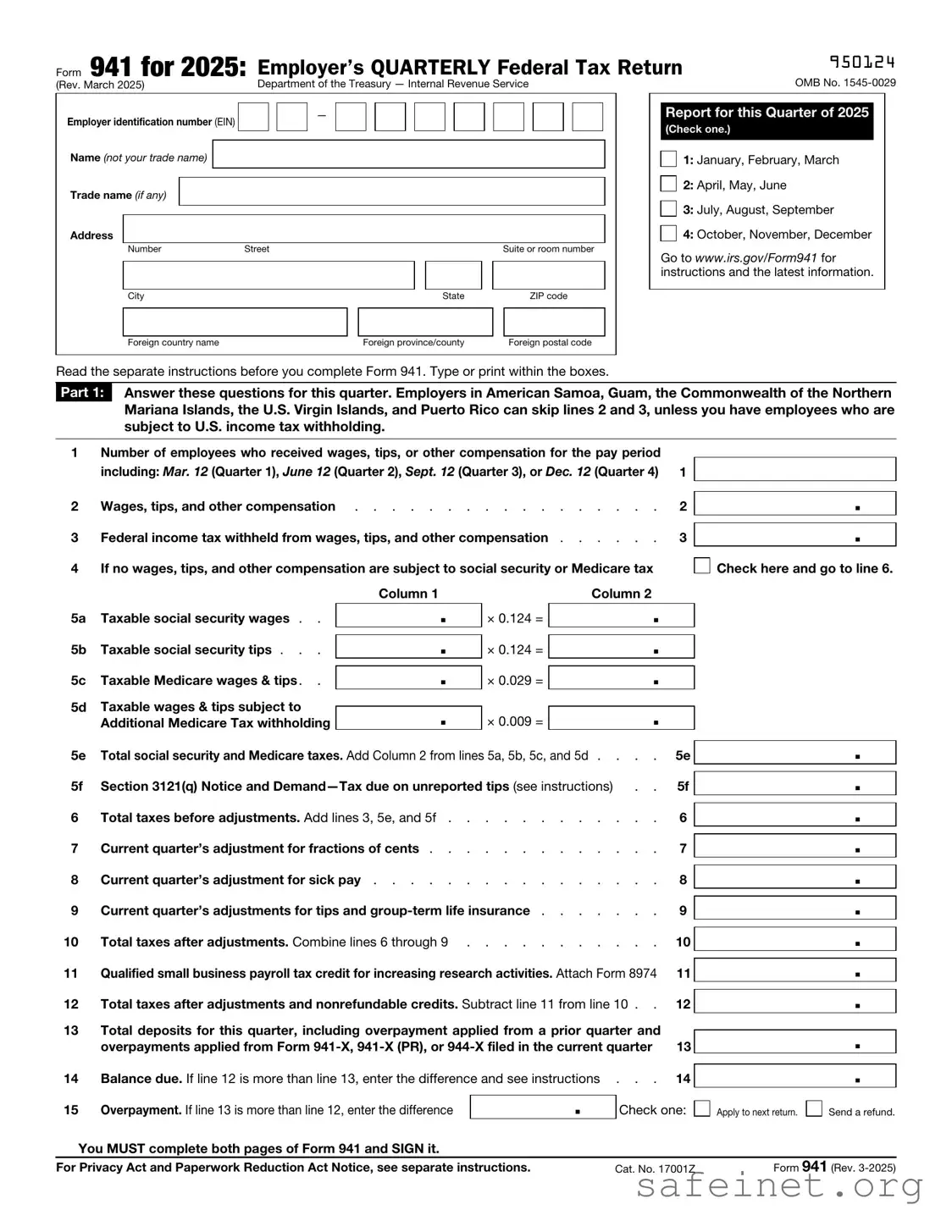

The IRS Form 941 plays a crucial role in the landscape of payroll taxes for employers in the United States. This quarterly form is used to report income taxes, Social Security tax, and Medicare tax withheld from employees’ paychecks. Employers must file Form 941 to provide the Internal Revenue Service with accurate information about their payroll tax obligations. Each quarter, businesses calculate their total payroll, determine the taxes owed, and report these figures on the form. In addition to reporting withheld taxes, Form 941 allows employers to claim certain tax credits, such as the Employee Retention Credit, which can significantly impact a company’s financial health. Understanding the nuances of this form is essential for compliance and for taking advantage of available tax benefits. By keeping accurate records and filing timely, employers can avoid penalties and ensure they meet their obligations under federal tax law.

Form 941 for 2025: |

Employer’s QUARTERLY Federal Tax Return |

950124 |

|

|

|

(Rev. March 2025) |

Department of the Treasury — Internal Revenue Service |

OMB No. |

Employer identification number (EIN) |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Number |

Street |

|

|

|

|

|

Suite or room number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

|

ZIP code |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

Foreign country name |

|

|

Foreign province/county |

|

|

Foreign postal code |

||

Report for this Quarter of 2025

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Go to www.irs.gov/Form941 for instructions and the latest information.

Read the separate instructions before you complete Form 941. Type or print within the boxes.

Part 1: Answer these questions for this quarter. Employers in American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, the U.S. Virgin Islands, and Puerto Rico can skip lines 2 and 3, unless you have employees who are subject to U.S. income tax withholding.

1 |

Number of employees who received wages, tips, or other compensation for the pay period |

|

including: Mar. 12 (Quarter 1), June 12 (Quarter 2), Sept. 12 (Quarter 3), or Dec. 12 (Quarter 4) 1 |

2 |

Wages, tips, and other compensation |

. . . . . |

2 |

|||

3 |

Federal income tax withheld from wages, tips, and other compensation . |

. . . . . |

3 |

|||

4 |

If no wages, tips, and other compensation are subject to social security or Medicare tax |

|

||||

|

|

Column 1 |

|

|

Column 2. |

|

5a |

Taxable social security wages . . |

. |

× 0.124 = |

|

|

|

|

|

|

|

|

. |

|

5b |

Taxable social security tips . . . |

. |

× 0.124 = |

|

|

|

|

|

|

|

|

. |

|

5c |

Taxable Medicare wages & tips. . |

. |

× 0.029 = |

|

|

|

.

.

Check here and go to line 6.

5d |

Taxable wages & tips subject to |

|

|

|

|

. |

× 0.009 = |

. |

|

||

|

Additional Medicare Tax withholding |

|

|||

5e |

Total social security and Medicare taxes. Add Column 2 from lines 5a, 5b, 5c, and 5d . . . . |

5e |

|||

5f |

Section 3121(q) Notice and |

5f |

|||

6 |

Total taxes before adjustments. Add lines 3, 5e, and 5f |

6 |

|||

7 |

Current quarter’s adjustment for fractions of cents |

7 |

|||

8 |

Current quarter’s adjustment for sick pay |

8 |

|||

9 |

Current quarter’s adjustments for tips and |

9 |

|||

10 |

Total taxes after adjustments. Combine lines 6 through 9 |

10 |

|||

11 |

Qualified small business payroll tax credit for increasing research activities. Attach Form 8974 |

11 |

|||

12Total taxes after adjustments and nonrefundable credits. Subtract line 11 from line 10 . . 12

13Total deposits for this quarter, including overpayment applied from a prior quarter and

|

overpayments applied from Form |

13 |

||

14 |

Balance due. If line 12 is more than line 13, enter the difference and see instructions |

. . . |

14 |

|

|

|

|

|

|

15 |

Overpayment. If line 13 is more than line 12, enter the difference |

. |

Check one: |

|

You MUST complete both pages of Form 941 and SIGN it.

.

.

.

.

.

.

.

.

.

.

.

Apply to next return. |

|

Send a refund. |

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 17001Z |

Form 941 (Rev. |

950224

Name (not your trade name)

Employer identification number (EIN)

–

Part 2: Tell us about your deposit schedule and tax liability for this quarter.

If you’re unsure about whether you’re a monthly schedule depositor or a semiweekly schedule depositor, see section 11 of Pub. 15.

16 Check one:

Line 12 on this return is less than $2,500 or line 12 on the return for the prior quarter was less than $2,500, and you didn’t incur a $100,000

You were a monthly schedule depositor for the entire quarter. Enter your tax liability for each month and total

liability for the quarter, then go to Part 3.

|

|

|

Tax liability: Month 1 |

. |

|

|

|

|

Month 2 |

. |

|

|

|

|

Month 3 |

. |

|

|

|

|

Total liability for quarter |

. |

Total must equal line 12. |

You were a semiweekly schedule depositor for any part of this quarter. Complete Schedule B (Form 941),

Report of Tax Liability for Semiweekly Schedule Depositors, and attach it to Form 941. Go to Part 3.

Part 3: Tell us about your business. If a question does NOT apply to your business, leave it blank.

17 If your business has closed or you stopped paying wages . . . . . . . . . . . . . . .

Check here and

enter the final date you paid wages

/ /

; also attach a statement to your return. See instructions.

18 If you’re a seasonal employer and you don’t have to file a return for every quarter of the year . . .

Check here.

Part 4: May we speak with your

Do you want to allow an employee, a paid tax preparer, or another person to discuss this return with the IRS? See the instructions

for details.

Yes. Designee’s name and phone number

Select a

No.

Part 5: Sign here. You MUST complete both pages of Form 941 and SIGN it.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Address

City

State

Check if you’re

PTIN |

|

|

|

|

|

|

|

Date |

/ |

/ |

|

EIN |

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

ZIP code

Page 2 |

Form 941 (Rev. |

Form

Purpose of Form

Complete Form

Making Payments With Form 941

To avoid a penalty, make your payment with Form 941 only if:

•Your total taxes after adjustments and nonrefundable credits (Form 941, line 12) for either the current quarter or the preceding quarter are less than $2,500, you didn’t incur a $100,000

•You’re a monthly schedule depositor making a payment in accordance with the accuracy of deposits rule. See section 11 of Pub. 15 for details. In this case, the amount of your payment may be $2,500 or more.

Otherwise, you must make deposits by electronic funds transfer. See section 11 of Pub. 15 for deposit instructions. Don’t use Form

▲! Use Form

CAUTION Form 941 that should’ve been deposited, you may be subject to a penalty. See Deposit Penalties in section 11 of Pub. 15.

Specific Instructions

Box

Box

Box

Box

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your

EIN, “Form 941,” and the tax period (“1st Quarter 2025,” “2nd Quarter 2025,” “3rd Quarter 2025,” or “4th Quarter 2025”) on your check or money order. Don’t send cash.

Don’t staple Form

•Detach Form

and Form 941 to the address in the Instructions for Form 941.

Note: You must also complete the entity information above Part 1 on Form 941.

Detach Here and Mail With Your Payment and Form 941.

Form |

|

|

|

|

Payment Voucher |

|

OMB No. |

||||

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||

|

Department of the Treasury |

|

|

Don’t staple this voucher or your payment to Form 941. |

|

2025 |

|||||

|

Internal Revenue Service |

|

|

|

|||||||

|

1 Enter your employer identification |

|

2 |

|

Dollars |

|

|

Cents |

|||

|

|

number (EIN). |

|

|

Enter the amount of your payment. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

– |

|

|

Make your check or money order payable to “United States Treasury.” |

|

|

|

|||

3 |

Tax Period |

|

4 Enter your business name (individual name if sole proprietor). |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1st |

|

3rd |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Quarter |

|

Quarter |

|

Enter your address. |

|

|

|||

|

|

|

|

|

|

|

|||||

|

|

2nd |

|

4th |

|

|

|||||

|

|

|

|

Enter your city, state, and ZIP code; or your city, foreign country name, foreign province/county, and foreign postal code. |

|||||||

|

|

Quarter |

|

Quarter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. |

| Filing Frequency | This form must be filed quarterly. Employers need to submit it for each quarter of the year. |

| Due Dates | Form 941 is due on the last day of the month following the end of each quarter. For example, the due date for Q1 is April 30. |

| State-Specific Forms | Some states require additional forms. For example, California has Form DE 9, governed by California Unemployment Insurance Code Section 1094. |

| Penalties | Failure to file Form 941 on time may result in penalties. The IRS imposes a penalty for late filing based on the amount owed. |

| Amendments | If an error is found after filing, employers can amend Form 941 using Form 941-X. |

| Record Keeping | Employers must keep copies of Form 941 for at least four years after the date they file the form. |

After gathering the necessary information, you are ready to fill out the IRS 941 form. This form is essential for reporting employment taxes. Follow the steps carefully to ensure accurate completion.

What is the IRS 941 form?

The IRS 941 form, officially known as the Employer's Quarterly Federal Tax Return, is a document that employers use to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. It is filed quarterly and helps the IRS track the taxes you owe and the taxes you have already paid.

Who needs to file Form 941?

Any employer who pays wages to employees must file Form 941. This includes businesses, non-profits, and government entities. If you have employees and withhold taxes from their paychecks, you are required to submit this form quarterly.

When is the IRS 941 form due?

Form 941 is due four times a year. The deadlines are typically the last day of the month following the end of each quarter. For example, the deadlines for 2023 are April 30 for Q1, July 31 for Q2, October 31 for Q3, and January 31 for Q4.

What information do I need to complete Form 941?

To complete Form 941, you will need details such as the number of employees, total wages paid, taxes withheld, and any adjustments for prior periods. You will also need your Employer Identification Number (EIN) and the quarter for which you are filing.

Can I file Form 941 electronically?

Yes, you can file Form 941 electronically. The IRS encourages e-filing as it is faster and more secure. Many payroll software programs offer e-filing options, making the process easier for employers.

What happens if I miss the deadline for filing Form 941?

If you miss the deadline, you may incur penalties and interest on any unpaid taxes. It's important to file as soon as possible, even if you cannot pay the full amount owed. The IRS may offer payment plans to help you manage your tax obligations.

Can I amend a previously filed Form 941?

Yes, if you need to correct errors on a previously filed Form 941, you can file Form 941-X, Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund. This form allows you to make adjustments and claim any refunds due.

What if I have no employees during a quarter?

If you have no employees during a quarter, you still need to file Form 941. You can indicate that there are no wages or taxes to report by checking the appropriate box on the form. This keeps your filing status up to date with the IRS.

Where can I find help if I have questions about Form 941?

If you have questions about Form 941, the IRS website offers resources, including instructions and FAQs. Additionally, consulting with a tax professional can provide personalized guidance based on your specific situation.

What are the consequences of not filing Form 941?

Failing to file Form 941 can lead to serious consequences, including penalties, interest on unpaid taxes, and potential legal action. It's crucial to stay compliant to avoid these issues and maintain a good standing with the IRS.

Failing to include accurate employer information. This includes the name, address, and Employer Identification Number (EIN). Incorrect details can delay processing.

Incorrectly calculating the number of employees. This figure should reflect the total number of employees who received wages during the quarter.

Omitting or miscalculating taxable wages. Ensure all taxable wages are reported correctly, as inaccuracies can lead to penalties.

Not reporting adjustments accurately. Adjustments for sick pay, tips, or group-term life insurance must be clearly stated to avoid discrepancies.

Neglecting to sign and date the form. The IRS requires a signature and date from an authorized individual to validate the submission.

Using outdated forms. Always ensure you are using the most current version of the IRS 941 form, as previous versions may no longer be accepted.

Failing to check for math errors. Simple arithmetic mistakes can lead to significant issues, so double-check all calculations before submission.

Not keeping copies of submitted forms. Retaining copies is essential for record-keeping and may be necessary for future reference or audits.

Ignoring deadlines. Timely filing is crucial to avoid penalties. Be aware of the specific due dates for each quarter.

Forgetting to report noncash payments. Any noncash benefits provided to employees must also be included in the taxable wages.

The IRS Form 941 is essential for employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. However, several other forms and documents often accompany or relate to Form 941. Understanding these documents can help ensure compliance and smooth processing of payroll taxes.

Familiarity with these forms can help streamline the payroll process and ensure that all tax obligations are met. Each form plays a specific role in the overall tax reporting system, making it crucial for employers to stay informed about their requirements.

The IRS Form 940 is similar to Form 941 in that both are used by employers to report taxes related to employee wages. While Form 941 is filed quarterly and focuses on income taxes withheld and Social Security and Medicare taxes, Form 940 is an annual report that deals specifically with federal unemployment taxes (FUTA). Employers need to file Form 940 to determine their unemployment tax liability for the year, making it a crucial document for understanding overall payroll tax obligations.

Form W-2 is another important document related to employee wages. Employers use Form W-2 to report annual wages and the amount of taxes withheld from an employee's paycheck. Unlike Form 941, which is filed quarterly, Form W-2 is provided to employees at the end of the year and must be submitted to the IRS by January 31. Both forms help the IRS track income and tax liabilities, but they serve different purposes and timelines.

Form 1099-MISC is also similar in that it reports payments made to individuals who are not employees. This form is typically used for independent contractors and freelancers. While Form 941 captures payroll taxes for employees, Form 1099-MISC focuses on non-employee compensation. Both forms help the IRS ensure that income is accurately reported and taxed, but they apply to different types of workers.

Form 945 is another IRS document that shares similarities with Form 941. Form 945 is used to report income tax withheld from non-payroll payments, such as pensions, annuities, and certain gambling winnings. Like Form 941, it is filed annually, but it focuses on different types of payments. Both forms play a role in ensuring that the correct amount of taxes is collected and reported to the IRS.

Form 1065 is relevant for partnerships and is similar to Form 941 in that it reports income and deductions. Partnerships use Form 1065 to report their income, gains, losses, deductions, and credits. While Form 941 focuses on payroll taxes for employees, Form 1065 helps the IRS track the financial performance of partnerships. Both forms are essential for tax compliance but cater to different business structures.

Form 1120 is the corporate income tax return and has similarities with Form 941 in that it reports income and taxes owed. Corporations must file Form 1120 annually to report their income and calculate their tax liability. While Form 941 is concerned with payroll taxes, Form 1120 deals with the overall financial health of a corporation. Both forms are vital for tax reporting but serve different types of entities.

Form 1040 is the individual income tax return and shares similarities with Form 941 in its role in tax reporting. While Form 941 is filed by employers for payroll-related taxes, Form 1040 is used by individuals to report their personal income and calculate their tax obligations. Both forms help the IRS track income and ensure that taxes are properly collected, but they apply to different taxpayers.

Form 941-X is an adjustment form that allows employers to correct errors made on previously filed Form 941. This form is essential for ensuring that the correct amount of payroll taxes is reported. Similar to Form 941, Form 941-X helps maintain accurate records with the IRS, but it specifically addresses corrections rather than initial reporting.

Form 720 is used to report and pay federal excise taxes, making it somewhat similar to Form 941 in that both involve tax reporting. Form 720 is filed quarterly and covers various excise taxes, such as those on fuel, air transportation, and certain goods. While Form 941 focuses on payroll taxes, both forms serve to keep the IRS informed about tax liabilities and compliance.

Finally, Form 8862 is a document used to claim the Earned Income Tax Credit (EITC) after a previous denial. While it is not directly related to payroll taxes like Form 941, it is similar in that it involves reporting and tax compliance. Both forms aim to ensure that taxpayers receive the correct credits and deductions, contributing to overall tax accuracy.

When filling out the IRS 941 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are seven things you should and shouldn't do:

The IRS Form 941 is a crucial document for employers in the United States. However, several misconceptions surround its purpose and requirements. Here are nine common misunderstandings about Form 941:

This is not true. Any employer who pays wages to employees must file Form 941, regardless of the size of the business.

These forms serve different purposes. Form 941 reports payroll taxes, while Form W-2 reports annual wages and tax withholdings for employees.

Filing Form 941 is mandatory for employers who withhold federal income tax, Social Security, or Medicare taxes from employee wages.

All employees, including part-time and seasonal workers, must be included in the Form 941 filing.

Form 941 is typically filed quarterly, not monthly. However, some employers may need to file it more frequently based on their tax liability.

Late filings can result in significant penalties. It is essential to file on time to avoid unnecessary fees.

Employers must maintain accurate records of wages paid and taxes withheld, as the IRS may request supporting documentation.

This is incorrect. If mistakes are made, employers can file Form 941-X to correct errors on a previously filed Form 941.

While it primarily addresses federal tax obligations, some state requirements may also need to be considered in conjunction with Form 941.

Understanding these misconceptions is vital for compliance and effective payroll management. Employers should stay informed and consult with tax professionals when necessary.

The IRS Form 941 is essential for employers to report payroll taxes. Here are key takeaways to keep in mind when filling it out and using it: