The IRS Form 8889 is a critical document that many individuals with Health Savings Accounts (HSAs) must navigate when filing their taxes. Designed to streamline the reporting process, this form captures essential information about contributions, distributions, and any other transactions related to HSAs throughout the tax year. Understanding how to effectively complete Form 8889 is important, as it helps ensure compliance with IRS guidelines while maximizing the tax advantages associated with HSAs. For instance, you’ll need to declare contributions made to your account, whether through payroll deductions or personal deposits. Furthermore, the form requires you to report any withdrawals and their specific uses, which are essential to ascertain whether those distributions qualify for tax-free treatment. It also accounts for any eligible medical expenses you may have used your HSA funds to pay for, thus protecting your hard-earned money from undue taxation. Navigating this form can seem daunting, but knowing its major aspects can empower you to handle your HSA finances more confidently and effectively.

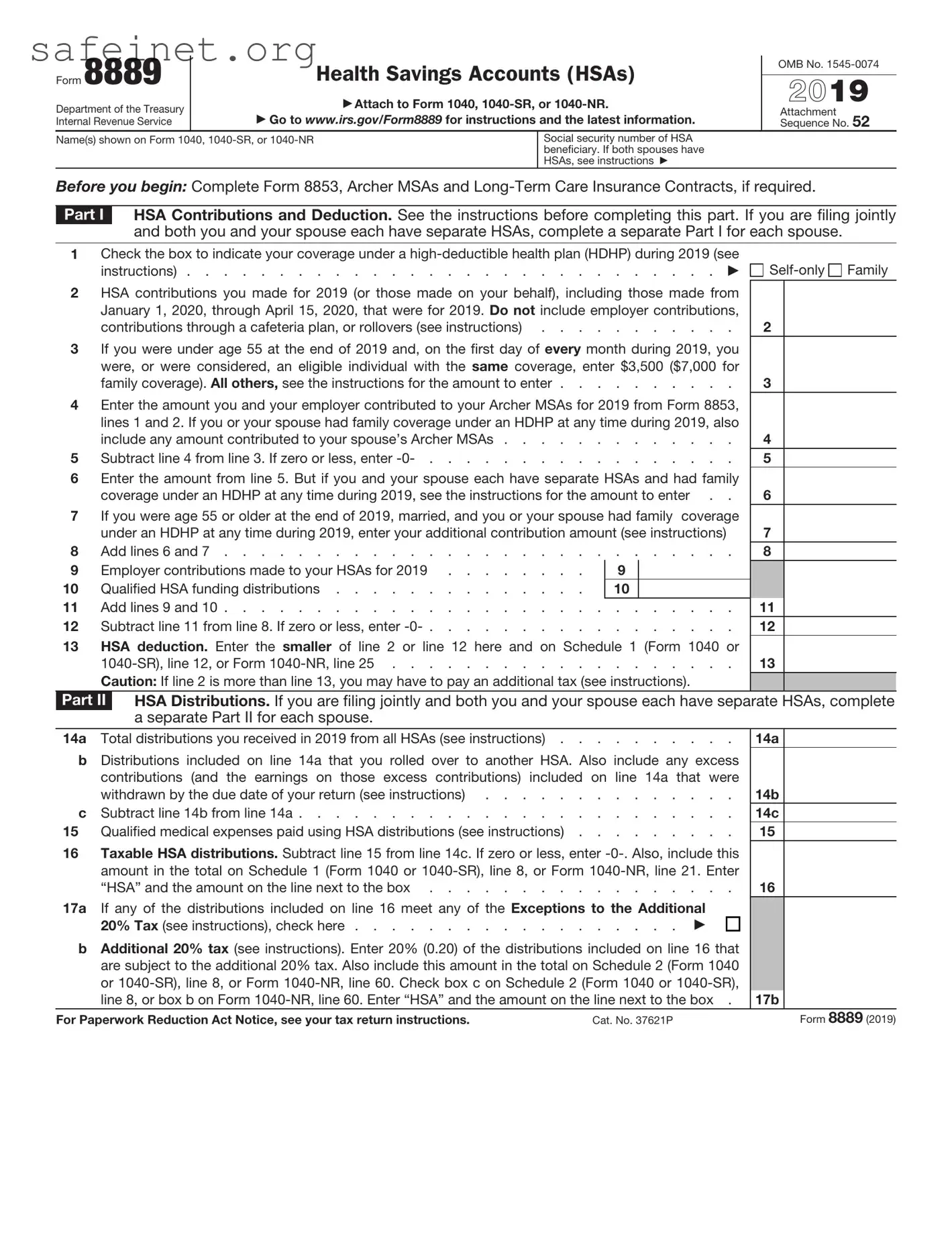

Form 8889

Department of the Treasury Internal Revenue Service

Health Savings Accounts (HSAs)

Attach to Form 1040,

Go to www.irs.gov/Form8889 for instructions and the latest information.

OMB No.

2019

Attachment Sequence No. 52

Name(s) shown on Form 1040,

Social security number of HSA beneficiary. If both spouses have HSAs, see instructions

Before you begin: Complete Form 8853, Archer MSAs and

Part I HSA Contributions and Deduction. See the instructions before completing this part. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part I for each spouse.

1Check the box to indicate your coverage under a

instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2HSA contributions you made for 2019 (or those made on your behalf), including those made from January 1, 2020, through April 15, 2020, that were for 2019. Do not include employer contributions,

contributions through a cafeteria plan, or rollovers (see instructions) . . . . . . . . . . .

3If you were under age 55 at the end of 2019 and, on the first day of every month during 2019, you were, or were considered, an eligible individual with the same coverage, enter $3,500 ($7,000 for

family coverage). All others, see the instructions for the amount to enter . . . . . . . . . .

4Enter the amount you and your employer contributed to your Archer MSAs for 2019 from Form 8853, lines 1 and 2. If you or your spouse had family coverage under an HDHP at any time during 2019, also

include any amount contributed to your spouse’s Archer MSAs . . . . . . . . . . . . .

5 Subtract line 4 from line 3. If zero or less, enter

6Enter the amount from line 5. But if you and your spouse each have separate HSAs and had family

coverage under an HDHP at any time during 2019, see the instructions for the amount to enter . .

7If you were age 55 or older at the end of 2019, married, and you or your spouse had family coverage under an HDHP at any time during 2019, enter your additional contribution amount (see instructions)

8 |

Add lines 6 |

and |

7 |

||

9 |

Employer contributions made to your HSAs for 2019 |

9 |

|

||

10 |

Qualified HSA funding distributions |

10 |

|

||

11 |

Add lines 9 |

and |

10 |

||

12 |

Subtract line 11 from line 8. If zero or less, enter |

||||

13HSA deduction. Enter the smaller of line 2 or line 12 here and on Schedule 1 (Form 1040 or

Caution: If line 2 is more than line 13, you may have to pay an additional tax (see instructions).

Family

Family

2

3

4

5

6

7

8

11

12

13

Part II HSA Distributions. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part II for each spouse.

14a Total distributions you received in 2019 from all HSAs (see instructions) . . . . . . . . . .

bDistributions included on line 14a that you rolled over to another HSA. Also include any excess contributions (and the earnings on those excess contributions) included on line 14a that were

|

withdrawn by the due date of your return (see instructions) |

c |

Subtract line 14b from line 14a |

15 |

Qualified medical expenses paid using HSA distributions (see instructions) |

16Taxable HSA distributions. Subtract line 15 from line 14c. If zero or less, enter

amount in the total on Schedule 1 (Form 1040 or

17a If any of the distributions included on line 16 meet any of the Exceptions to the Additional 20% Tax (see instructions), check here . . . . . . . . . . . . . . . . . .

bAdditional 20% tax (see instructions). Enter 20% (0.20) of the distributions included on line 16 that are subject to the additional 20% tax. Also include this amount in the total on Schedule 2 (Form 1040

or

14a

14b

14c

15

16

17b

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 37621P |

Form 8889 (2019) |

Form 8889 (2019) |

Page 2 |

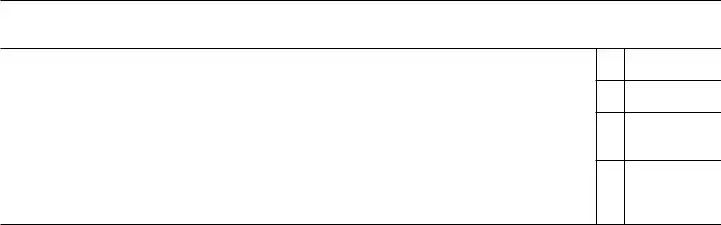

Part III Income and Additional Tax for Failure To Maintain HDHP Coverage. See the instructions before completing this part. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part III for each spouse.

18

19 Qualified HSA funding distribution . . . . . . . . . . . . . . . . . . . . . . .

20Total income. Add lines 18 and 19. Include this amount on Schedule 1 (Form 1040 or

8, or Form

21Additional tax. Multiply line 20 by 10% (0.10). Include this amount in the total on Schedule 2 (Form 1040 or

18

19

20

21

Form 8889 (2019)

| Fact Name | Detail |

|---|---|

| Purpose of Form | The IRS 8889 form is used to report Health Savings Account (HSA) contributions and distributions. |

| Who Must File | Individuals with an HSA need to file this form to provide information about contributions made to the account and any withdrawals. |

| Filing Deadline | This form is typically due on April 15th of the year following the tax year being reported, unless extensions are granted. |

| Types of Contributions | Both individual and employer contributions to the HSA need to be reported on this form. |

| Distributions | Health expenditures paid via HSA must be documented to ensure that funds were used for qualified medical expenses. |

| State-Specific Requirements | Some states may have additional forms or requirements regarding HSAs. Consult state regulations for specifics, as laws vary by state. |

Filling out Form 8889 is essential for reporting Health Savings Account (HSA) activity, which may impact your tax return for the year. Before tackling this form, gather your previous year's HSA statements and any receipts for eligible medical expenses. The following steps will guide you through the process of accurately completing the form.

What is IRS Form 8889?

IRS Form 8889 is used to report Health Savings Account (HSA) information. If you have an HSA, you need this form to report contributions made to the account and distributions taken from it. It helps ensure compliance with specific tax provisions related to HSAs.

Who needs to file Form 8889?

You need to file Form 8889 if you received contributions to an HSA during the tax year or if you took distributions from your HSA. Both individuals with their own HSAs and those who received contributions from employers must file this form.

What type of information is required on Form 8889?

Form 8889 requires details about HSA contributions, distributions, and any qualified medical expenses you paid with HSA funds. You'll need to provide information for both self-only and family coverage if applicable.

What are the contribution limits for HSAs?

The IRS sets annual contribution limits for HSAs. For 2023, the limit is $3,850 for individuals and $7,750 for families. If you are 55 or older, you may be eligible for an additional $1,000 catch-up contribution. Always verify the current limits before filing.

What happens if I don't file Form 8889?

Failure to file Form 8889 can lead to penalties and interest. If you are required to file and do not, the IRS may impose taxes on your HSA distributions, treating them as taxable income. Always file on time to avoid complications.

Are there penalties for excess contributions to an HSA?

Yes, if you contribute more to your HSA than the allowed limits, the IRS imposes a 6% excise tax on the excess contributions. To avoid this penalty, you should withdraw the excess amount before filing your tax return.

Can I use Form 8889 for other tax benefits?

Form 8889 is specific to HSAs and does not directly apply to other tax benefits. However, the deductions reported on this form can impact your overall tax liability. Be sure to consider how your HSA contributions fit into your broader tax strategy.

Where can I find Form 8889 and instructions?

You can find Form 8889 and its instructions on the IRS website. It is available for download as a PDF file. The IRS website also provides detailed guidance for completing the form correctly.

What if I have questions while filing Form 8889?

If you have questions while filling out Form 8889, consider reaching out to a tax professional. You can also consult the IRS website for FAQs and additional resources. Utilizing these resources can help clarify any uncertainties you may have.

When completing IRS Form 8889, which is used for Health Savings Accounts (HSAs), individuals often make common mistakes that can lead to delays or complications. Below is a detailed list of potential errors to avoid.

Many people fail to accurately report all contributions made to their HSA. This includes keeping track of contributions made by both the individual and their employer. Any omission can result in penalties.

Some filers miscalculate the amount they are eligible to deduct from their taxable income. It is important to understand annual contribution limits and ensure the correct figures are entered on the form.

A common oversight is failing to sign the form. This can cause delays in processing and may lead to the form being rejected entirely.

Individuals sometimes forget to include necessary documentation, such as proof of high-deductible health plan coverage or records of qualified medical expenses. Including these documents can be crucial for verifying claims.

By staying mindful of these common mistakes, you can help ensure that your Form 8889 is filled out accurately and submitted without issues. Proper attention to detail can alleviate complications and promote a smoother process.

The IRS Form 8889 is utilized to report Health Savings Account (HSA) contributions and distributions. It is often accompanied by other documents that provide necessary information about the taxpayer's medical expenses, contributions, and eligibility. Below is a list of forms and documents commonly used with Form 8889.

Filing Form 8889 with the relevant documents ensures that taxpayers accurately report their HSA activity. It is important to gather all necessary forms and receipts to facilitate a smooth filing process and avoid any potential issues with the IRS.

The IRS Form 8889 is specifically designed for Health Savings Accounts (HSAs) and shares similarities with Form 1040, the individual income tax return. Both forms require detailed financial information from the taxpayer. While Form 1040 serves as a comprehensive report of an individual's income and deductions, Form 8889 requires specific details about contributions to and distributions from HSAs. Taxpayers need to accurately report their HSA activities on Form 8889, which then feeds into their Form 1040, highlighting how health expenses have been managed tax-wise.

Another document that resembles the IRS Form 8889 is Form 5498-SA. This form is used to report contributions to HSAs and other similar accounts. Just like Form 8889, which provides the taxpayer's perspective on account management, Form 5498-SA offers a record from the trustee or custodian of the HSA. Both forms ultimately work together, creating a comprehensive picture of the taxpayer’s contributions and distributions during the tax year. This allows for accurate reporting and ensures compliance with tax laws surrounding HSAs.

Form 1099-SA also has close ties with the IRS Form 8889. Issued by HSA custodians, Form 1099-SA reports distributions made from HSAs. Similar to Form 8889, it requires taxpayers to account for these distributions during tax filing. This form provides a crucial element, confirming the amounts withdrawn, which taxpayers must include when detailing their HSA activities. Therefore, understanding the interplay between these two documents is vital for accurate tax preparation.

Lastly, the IRS Form 8889 can be compared to Form 8889-W, which is specifically tailored for employers, allowing them to report contributions made on behalf of their employees to HSAs. While both forms deal with similar accounts and financial activities, Form 8889-W is employer-focused, whereas Form 8889 is designed for individual taxpayers. This similarity ensures that the intricate details of HSA management are captured comprehensively, regardless of the source of contributions. Understanding both forms can aid taxpayers in preparing their returns and confirming that they receive proper tax advantages related to HSAs.

When filling out the IRS 8889 form, which is used for reporting Health Savings Account (HSA) information, it's essential to follow best practices to ensure accuracy and compliance. Here are eight dos and don'ts to keep in mind:

The IRS Form 8889 is essential for those with Health Savings Accounts (HSAs). Unfortunately, several misconceptions exist about this form that may lead to confusion and mistakes. Here are ten common misunderstandings:

This is incorrect. Anyone who had an HSA during the tax year, including employees, must file this form.

While contributions are reported, the form also includes information about distributions and allowable deductions related to your HSA.

This is not true. You must file the form to report the existence of the HSA, even if there were no distributions.

This is misleading. The form must be submitted with your tax return by the filing deadline for the year being reported.

This misunderstanding overlooks the purpose of reporting both deductions and distributions from the HSA.

This is incorrect. Being covered under a High Deductible Health Plan (HDHP) does not exempt you from filing Form 8889.

This is a common myth. Form 8889 is an attachment to Form 1040, serving a specific purpose regarding HSAs.

This is misleading. All transactions should be reported on the form, regardless of the amount.

This misconception fails to recognize that it also provides necessary details about contributions and withdrawals.

This is unwise. It is essential to retain documentation for contributions and distributions for reference and potential audits.

Understanding these misconceptions can help ensure proper compliance with IRS regulations related to HSAs and minimize potential errors on your tax return.

Filling out the IRS Form 8889 can be essential for those who have a Health Savings Account (HSA). Here are some key takeaways to consider:

Taking the time to understand and correctly complete Form 8889 can help ensure you maximize the benefits of your Health Savings Account while remaining compliant with tax regulations.