The IRS 8840 form, officially known as the "Closer Connection Exception Statement for Aliens," plays a pivotal role for individuals navigating U.S. tax obligations while maintaining ties to foreign countries. It offers a pathway for certain non-resident aliens who might otherwise be classified as U.S. residents for tax purposes under the substantial presence test. By submitting Form 8840, these individuals can assert their eligibility to be treated as non-residents, highlighting their closer connections to a foreign jurisdiction. This form requires personal information, including residency details, a summary of days spent in the U.S., and the establishment of relevant ties to another country, such as family, business interests, or cultural connections. It is crucial to understand that timely and accurate completion of this form can significantly impact tax liabilities, potentially saving thousands of dollars for eligible individuals. Additionally, the IRS uses the information provided to ensure compliance with U.S. tax laws while safeguarding the interests of taxpayers who qualify under this exception. Without this form, one can face unintended tax consequences, making its importance even more pronounced for those with international connections.

Form 8840 |

|

Closer Connection Exception Statement for Aliens |

|

OMB No. |

|||

|

|

||||||

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

Attach to Form |

|

|

2020 |

|

|

|

|

Go to www.irs.gov/Form8840 for the latest information. |

|

|||

Department of the Treasury |

|

|

For the year January |

|

Attachment |

||

Internal Revenue Service |

|

beginning |

|

, 2020, and ending |

, 20 |

. |

Sequence No. 101 |

|

|

|

|||||

Your first name and initial |

|

|

|

Last name |

Your U.S. taxpayer identification number, if any |

||

|

|

|

|

|

|

|

|

Fill in your addresses only if you are filing this form by itself and not with your U.S. tax return

Address in country of residence

Address in the United States

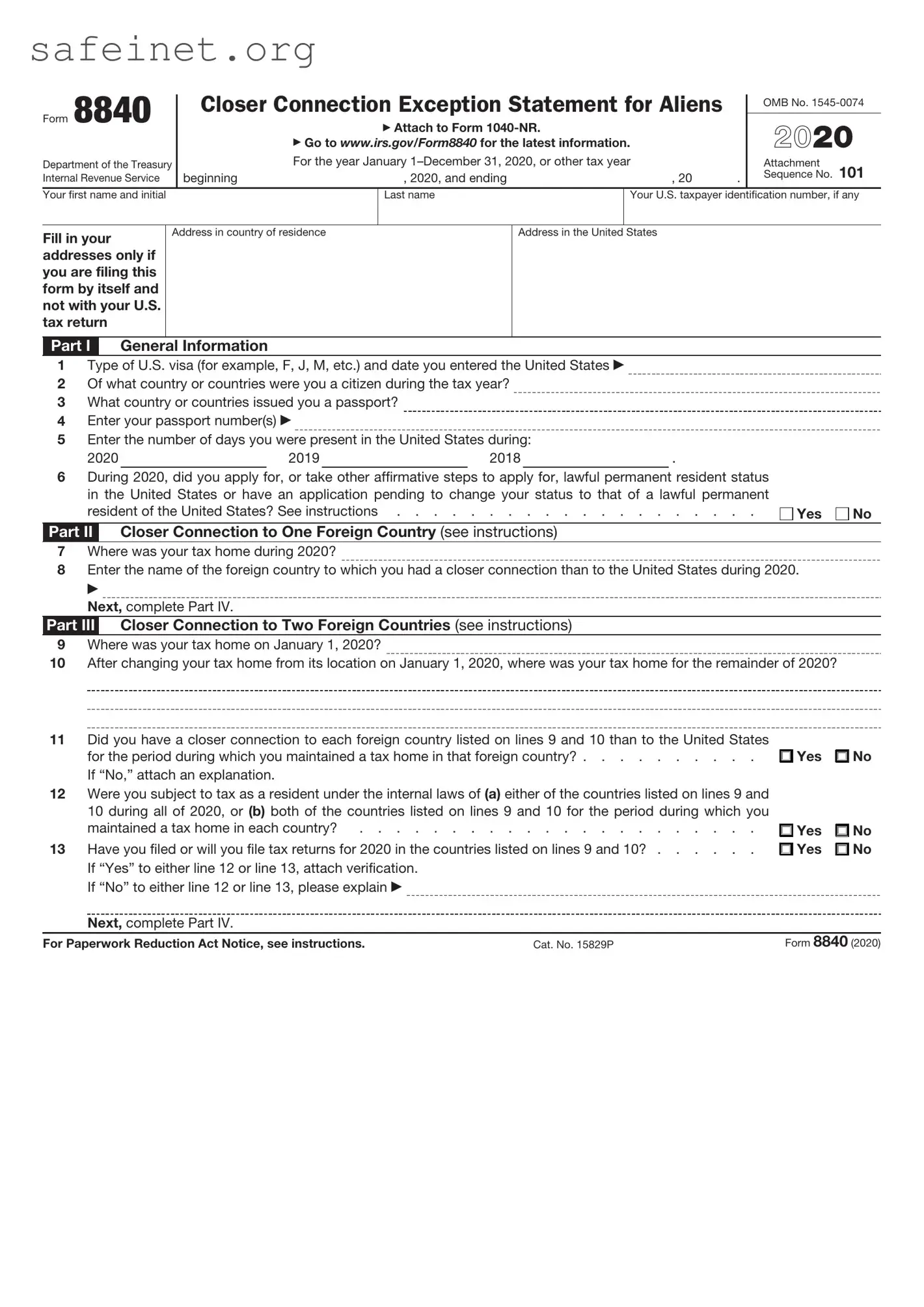

Part I General Information

1Type of U.S. visa (for example, F, J, M, etc.) and date you entered the United States

2 Of what country or countries were you a citizen during the tax year?

3 What country or countries issued you a passport?

4 Enter your passport number(s)

5 Enter the number of days you were present in the United States during:

2020 |

|

2019 |

|

2018 |

|

. |

6During 2020, did you apply for, or take other affirmative steps to apply for, lawful permanent resident status in the United States or have an application pending to change your status to that of a lawful permanent

resident of the United States? See instructions |

Yes |

No

Part II Closer Connection to One Foreign Country (see instructions)

7Where was your tax home during 2020?

8Enter the name of the foreign country to which you had a closer connection than to the United States during 2020.

Next, complete Part IV.

Part III Closer Connection to Two Foreign Countries (see instructions)

9Where was your tax home on January 1, 2020?

10After changing your tax home from its location on January 1, 2020, where was your tax home for the remainder of 2020?

11Did you have a closer connection to each foreign country listed on lines 9 and 10 than to the United States

for the period during which you maintained a tax home in that foreign country? . . . . . . . . . .

If “No,” attach an explanation.

12Were you subject to tax as a resident under the internal laws of (a) either of the countries listed on lines 9 and 10 during all of 2020, or (b) both of the countries listed on lines 9 and 10 for the period during which you

maintained a tax home in each country? . . . . . . . . . . . . . . . . . . . . . .

13Have you filed or will you file tax returns for 2020 in the countries listed on lines 9 and 10? . . . . . .

If “Yes” to either line 12 or line 13, attach verification. If “No” to either line 12 or line 13, please explain

Next, complete Part IV.

Yes

Yes Yes

No

No No

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 15829P |

Form 8840 (2020) |

Form 8840 (2020) |

Page 2 |

|

Part IV |

Significant Contacts With Foreign Country or Countries in 2020 |

|

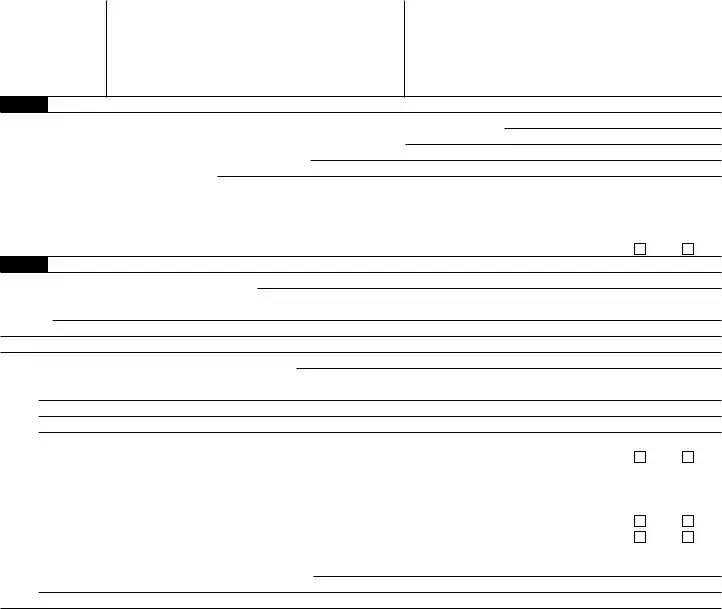

14Where was your regular or principal permanent home located during 2020? See instructions.

15If you had more than one permanent home available to you at all times during 2020, list the location of each and explain.

16Where was your family located?

17Where was your automobile(s) located?

18Where was your automobile(s) registered?

19Where were your personal belongings, furniture, etc., located?

20Where was the bank(s) with which you conducted your routine personal banking activities located?

a |

|

c |

b |

|

d |

21 |

Did you conduct business activities in a location other than your tax home? |

|

If “Yes,” where? |

22a |

Where was your driver’s license issued? |

bIf you hold a second driver’s license, where was it issued?

23Where were you registered to vote?

24When completing official documents, forms, etc., what country do you list as your residence?

25Have you ever completed:

a |

Form |

b |

Form |

cAny other U.S. official forms? If “Yes,” indicate the form(s)

26In what country or countries did you keep your personal, financial, and legal documents?

Yes

Yes

Yes

Yes

No

No

No

No

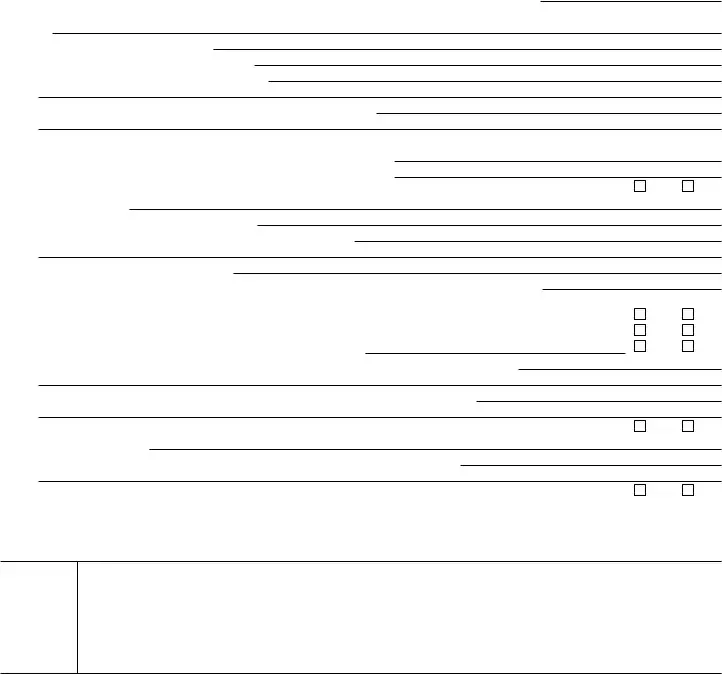

27From what country or countries did you derive the majority of your 2020 income?

28 Did you have any income from U.S. sources? . . . . . . . . . . . . . . . . . . . . .

If “Yes,” what type?

29In what country or countries were your investments located? See instructions.

Yes

No

30 Did you qualify for any type of “national” health plan sponsored by a foreign country? |

Yes |

No |

If “Yes,” in what country? If “No,” please explain

If you have any other information to substantiate your closer connection to a country other than the United States or you wish to explain in more detail any of your responses to lines 14 through 30, attach a statement to this form.

Sign here only if you are filing this form by itself and not with your U.S. tax return

Under penalties of perjury, I declare that I have examined this form and the accompanying attachments, and to the best of my knowledge and belief, they are true, correct, and complete.

F |

|

F |

|

|

Your signature |

Date |

|||

|

|

Form 8840 (2020)

Form 8840 (2020) |

Page 3 |

Section references are to the U.S. Internal Revenue Code, unless otherwise specified.

Future Developments

For the latest information about developments related to Form 8840 and its instructions, such as legislation

enacted after they were published, go to www.irs.gov/Form8840.

General Instructions

Purpose of Form

Use Form 8840 to claim the closer connection to a foreign country(ies) exception to the substantial presence test. The exception is described later and in Regulations section

Note: You are not eligible for the closer connection exception if any of the following apply.

•You were present in the United States 183 days or more in calendar year 2020.

•You are a lawful permanent resident of the United States (that is, you are a green card holder).

•You have applied for, or taken other affirmative steps to apply for, a green card; or have an application pending to change your status to that of a lawful permanent resident of the United States.

Steps to change your status to that of a permanent resident include, but are not limited to, the filing of the following forms.

•Form

•Form

•Form

•Form

•Form

•Form

Even if you are not eligible for the closer connection exception, you may qualify for nonresident status by reason of a treaty. See the instructions for line 6 for more details.

Who Must File

If you are an alien individual and you meet the closer connection exception to the substantial presence test, you must

file Form 8840 with the IRS to establish your claim that you are a nonresident of the United States by reason of that exception. Each alien individual must file a separate Form 8840 to claim the closer connection exception.

For more details on the substantial presence test and the closer connection exception, see Pub. 519.

Note: You can download forms and publications at IRS.gov.

Substantial Presence Test

You are considered a U.S. resident if you meet the substantial presence test for 2020. You meet this test if you were physically present in the United States for at least:

•31 days during 2020; and

•183 days during the period 2020, 2019, and 2018, counting all the days of physical presence in 2020 but only 1/3 the number of days of presence in 2019 and only 1/6 the number of days in 2018.

Days of presence in the United States.

Generally, you are treated as being present in the United States on any day that you are physically present in the country at any time during the day.

However, you do not count the following days of presence in the United States for purposes of the substantial presence test.

1.Days you regularly commuted to work in the United States from a residence in Canada or Mexico.

2.Days you were in the United States for less than 24 hours when you were traveling between two places outside the United States.

3.Days you were temporarily in the United States as a regular crew member of a foreign vessel engaged in transportation between the United States and a foreign country or a possession of the United States unless you otherwise engaged in trade or business on such a day.

4.Days you were unable to leave the United States because of a medical condition or medical problem that arose while you were in the United States.

5.Days you were an exempt individual.

In general, an exempt individual is

(a)a foreign

Note: If you qualify to exclude days of presence in the United States because you were an exempt individual (other than a foreign

Closer Connection

Exception

Even though you would otherwise meet the substantial presence test, you will not be treated as a U.S. resident for

2020 if:

•You were present in the United States for fewer than 183 days during 2020;

•You establish that, during 2020, you had a tax home in a foreign country; and

•You establish that, during 2020, you had a closer connection to one foreign country in which you had a tax home than to the United States, unless you had a closer connection to two foreign countries.

Closer Connection to Two Foreign Countries

You can demonstrate that you have a closer connection to two foreign countries (but not more than two) if all five of the following apply.

1.You maintained a tax home as of January 1, 2020, in one foreign country.

2.You changed your tax home during 2020 to a second foreign country.

3.You continued to maintain your tax home in the second foreign country for the rest of 2020.

4.You had a closer connection to each foreign country than to the United States for the period during which you maintained a tax home in that foreign country.

5.You are subject to tax as a resident under the tax laws of either foreign country for all of 2020 or subject to tax as a resident in both foreign countries for the period during which you maintained a tax home in each foreign country.

Tax Home

Your tax home is the general area of your main place of business, employment, or post of duty, regardless of where you maintain your family home. Your tax home is the place where you permanently or indefinitely work as an employee or a

Form 8840 (2020) |

Page 4 |

place where you regularly live. If you have neither a regular or main place of business nor a place where you regularly live, you are considered an itinerant and your tax home is wherever you work. For determining whether you have a closer connection to a foreign country, your tax home must also be in existence for the entire year, and must be located in the foreign country (or countries) in which you are claiming to have a closer connection.

Establishing a Closer Connection

You will be considered to have a closer connection to a foreign country than to the United States if you or the IRS establishes that you have maintained more significant contacts with the foreign country than with the United States.

Your answers to the questions in Part IV will help establish the jurisdiction to which you have a closer connection.

When and Where To File

If you are filing a 2020 Form

If you do not have to file a 2020 tax return, mail Form 8840 to the Department of the Treasury, Internal Revenue Service Center, Austin, TX

Penalty for Not Filing Form 8840

If you do not timely file Form 8840, you will not be eligible to claim the closer connection exception and may be treated as a U.S. resident.

You will not be penalized if you can show by clear and convincing evidence that you took reasonable actions to become aware of the filing requirements and significant steps to comply with those requirements.

Specific Instructions

Part I

Line 1

If you had a visa on the last day of the tax year, enter your visa type and the date you entered the United States. If you do not have a visa, enter your U.S. immigration status on the last day of the tax year and the date you entered the United States. For example, if you entered under the visa waiver program, enter “VWP,” the name of the Visa Waiver Program country, and the date you entered the United States.

Line 6

If you checked the “Yes” box on line 6, do not file Form 8840. You are not eligible for the closer connection exception. However, you may qualify for nonresident status by reason of a treaty. See Pub. 519 for details. If so, file Form 8833 with your Form

Parts II and III

If you had a tax home in the United States at any time during the year, do not file Form 8840. You are not eligible for the closer connection exception. Otherwise, complete Part II or Part III (but not both) depending on the number of countries to which you are claiming a closer connection. If you are claiming a closer connection to one country, complete Part II. If you are claiming a closer connection to two countries, complete Part III. After completing Part II or Part III, complete Part IV.

Part IV

Line 14

A “permanent home” is a dwelling unit (whether owned or rented, and whether a house, an apartment, or a furnished room) that is available at all times, continuously and not solely for short stays.

Line 29

For stocks and bonds, indicate the country of origin of the stock company or debtor. For example, if you own shares of a U.S. publicly traded corporation, the investment is considered located in the United States, even though the shares of stock are stored in a safe deposit box in a foreign country.

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. Section 7701(b) and its regulations require that you give us the information. We need it to determine if you meet the closer connection exception to the substantial presence test.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The average time and expenses required to complete and file this form will vary depending on individual circumstances. For the estimated averages, see the instructions for your income tax return.

If you have suggestions for making this form simpler, we would be happy to hear from you. See the instructions for your income tax return.

| Fact Name | Details |

|---|---|

| Purpose | The IRS 8840 form is used by individuals to claim the closer connection exception to the substantial presence test. |

| Who Must File | Non-U.S. citizens who reside in the U.S. but meet specific criteria may need to file this form. |

| Filing Deadline | The form is typically due by June 15 each year for the preceding calendar year. |

| Use of Form | By filing the 8840, individuals can avoid being classified as U.S. residents for tax purposes. |

| Closer Connection Test | To pass this test, one must demonstrate stronger ties to another country than to the U.S. |

| Supporting Documents | Filing the form often requires attaching documentation that proves closer ties to the foreign country. |

| State-Specific Forms | Some states may have their own forms that relate to residency status. For instance, California requires form 540NR for non-residents. |

| Potential Penalties | Failing to file the 8840 when necessary can lead to consequences, such as being taxed as a resident. |

| Form Accessibility | The form can be accessed and filed through the IRS website, ensuring it’s readily available for those who need it. |

Once you have gathered the necessary information, filling out the IRS Form 8840 can be straightforward. This form, known as the "Closer Connection Exception Statement for aliens," requires specific details about your residency status and physical presence in the United States. Following these steps will assist you in accurately completing the form.

What is IRS Form 8840?

IRS Form 8840, also known as the "Closer Connection Exception Statement for Aliens," is filed by individuals who are not U.S. citizens but claim to have a closer connection to a foreign country. This form helps determine whether you are considered a resident of the United States for tax purposes.

Who needs to file Form 8840?

If you are a non-resident alien, typically someone who does not meet the substantial presence test, but you have spent time in the U.S., you may need to file Form 8840. You must show that you have a closer connection to your home country for the tax year.

What is the substantial presence test?

The substantial presence test is a method to determine if you are a U.S. resident for tax purposes. It involves counting the number of days you have spent in the U.S. over the last three years. If the total meets or exceeds 183 days, you may be considered a resident alien.

When is Form 8840 due?

Form 8840 is typically due on April 15 of the year following the tax year. If you are outside the U.S., you may qualify for an automatic extension until June 15. It's important to file on time to avoid potential penalties.

What information do I need to complete Form 8840?

You will need your personal information, including your name, address, and taxpayer identification number. Additionally, you must provide details about your time spent in the U.S., your residency status, and your connections to your home country.

What happens if I don’t file Form 8840?

If you fail to file Form 8840 when required, you risk being classified as a U.S. resident for tax purposes. This could lead to increased tax liability and the requirement to report worldwide income to the IRS.

Can I file Form 8840 electronically?

Currently, Form 8840 cannot be filed electronically. You must print the completed form and mail it to the appropriate IRS address. Ensure to keep a copy for your records.

Where can I find Form 8840 and instructions?

Form 8840 and its instructions are available on the official IRS website. You can download the form, review the instructions neatly laid out, and ensure you fill it out correctly.

Is there any fee for filing Form 8840?

There is no fee to file Form 8840. However, if you hire a tax professional to assist you, they may charge for their services. It’s wise to consider this possibility when planning your filing.

Not including all relevant information: One of the most common mistakes is failing to provide complete personal information such as your name, address, and Social Security number. Without accurate details, the IRS may not process your form properly.

Incorrectly calculating days spent in the U.S.: Many people miscount the number of days they spent in the United States. It’s essential to keep track of your presence each year, as days can add up quickly and affect your residency status.

Neglecting to sign and date the form: This may seem simple, but failing to sign or date your form is a frequent error. Without a signature, the IRS considers the form invalid.

Submitting the form late: It’s important to submit IRS Form 8840 by the due date. Late submissions can lead to penalties or complications with your tax status.

Not answering all required questions: Every question on the form is there for a reason. Leaving questions unanswered may result in delays or a rejection of your application.

Using the wrong mailing address: Make sure to send your form to the correct address. Different addresses exist for different scenarios, such as whether you’re filing from inside or outside the U.S.

Assuming information from previous years is still accurate: Circumstances can change year to year. Always reevaluate your situation and avoid relying solely on past filings.

Not keeping a copy for personal records: After filing, it’s wise to keep a copy of your completed form. This can be helpful for future reference or in case of an audit.

Failing to seek help if confused: If anything is unclear, reaching out for help is always a good idea. There are many resources available, including IRS guidance, that can clarify any confusion.

The IRS 8840 form, also known as the "Closer Connection Exception Statement for Aliens," is essential for individuals seeking to clarify their tax residency status. However, several other forms and documents often accompany this form to ensure compliance and thoroughness in tax matters. Below is a list of related forms that may be necessary for individuals filing the IRS 8840.

Filling out the IRS 8840 form correctly is critical, but it's just one part of the process. Depending on your situation, consider which additional documents are relevant to your tax filing needs. Consulting with a tax professional may also be advantageous to ensure compliance with U.S. tax laws.

The IRS Form 8833, titled "Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b)," serves a role similar to Form 8840. While both forms are concerned with determining tax residency status and claiming treaty benefits, their focus differs. Form 8840 is primarily for individuals who wish to claim the "Closer Connection Exception" to the substantial presence test, effectively establishing their non-resident alien status for tax purposes. Conversely, Form 8833 is used when individuals are claiming specific benefits under a tax treaty with the United States, helping those who wish to rely on treaty provisions for reducing or eliminating U.S. tax liabilities. Understanding which form to use often hinges on the specific residency and tax treaty situations facing the taxpayer.

Another form that resembles the IRS Form 8840 is Form 1040-NR, the "U.S. Nonresident Alien Income Tax Return." While both forms are used by non-resident aliens, they serve different purposes. Form 8840 is focused on claiming the closer connection exception, which allows individuals to avoid being classified as U.S. residents for tax purposes. In contrast, Form 1040-NR is utilized to report income earned in the United States and calculate any tax owed. Therefore, if an individual is earning U.S. income while also working to establish a closer connection to another country, they may need to file both forms to fully address their tax situation.

Form 540NR, also known as the "California Nonresident or Part-Year Resident Income Tax Return," is similar to Form 8840 specifically for individuals dealing with state residency issues. Taxpayers may need to show they are non-residents of California for state tax purposes. While Form 8840 deals with federal tax residency, Form 540NR focuses on California state income tax obligations. Taxpayers who can demonstrate a closer connection to another state or country might find similar principles apply when completing both forms. They must understand the rules governing state residency, which can differ from federal regulations.

Form W-8BEN, or "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)," is another document that may seem related to Form 8840. Both forms concern individuals who are not U.S. citizens or residents. Form W-8BEN is primarily used to claim foreign status for purposes of reducing withholding rates or obtaining treaty benefits on certain types of income, such as dividends or royalties. Hence, while Form 8840 focuses on residency status, Form W-8BEN addresses taxation on U.S. source income, helping individuals navigate the complex U.S. tax landscape.

Finally, IRS Form 1116, which is the "Foreign Tax Credit," shares similarities with Form 8840 in that both deal with international tax issues. Form 8840 aids in determining whether a taxpayer can claim non-resident status based on a closer connection to their home country, while Form 1116 allows taxpayers to claim a credit for taxes paid to another country on foreign-sourced income. Individuals living abroad often find themselves completing both forms to ensure they maximize their benefits under U.S. tax law while respecting their status in their country of residence.

When filling out the IRS Form 8840, it's important to follow certain guidelines to ensure that your application is accurate and complete. Below are some essential dos and don'ts to keep in mind.

Following these guidelines can help avoid delays or issues with your submission. Careful attention to detail will benefit you in the long run.

The IRS Form 8840, also known as the "Closer Connection Exception Statement for Aliens," is often surrounded by misunderstandings. Here are seven common misconceptions about this form and clarifications to help you navigate the requirements.

Misconception 1: The form is only for people who live in the U.S.

Many believe that Form 8840 is restricted to individuals residing in the United States. However, it is primarily used by non-resident aliens who need to establish a closer connection to another country. This form is relevant regardless of your current location.

Misconception 2: Filing the form guarantees tax benefits.

While filing Form 8840 can help you claim a closer connection to a foreign country, it does not automatically guarantee tax benefits. The form primarily serves to assert your non-resident status, which may have implications for your tax liabilities.

Misconception 3: Everyone needs to file Form 8840.

Not everyone is required to file this form. It is specifically for individuals who meet certain criteria regarding their days present in the U.S. Interested parties should review their individual circumstances to determine their need to file.

Misconception 4: Information on the form is not checked.

Some individuals believe that the IRS does not verify the information provided on Form 8840. In reality, the IRS may cross-check details with other documents, aiding their enforcement of tax regulations.

Misconception 5: The form must be submitted with your tax return.

Another belief is that Form 8840 has to accompany your tax return. This form can actually be submitted separately and has its own filing deadlines that must be adhered to.

Misconception 6: Form 8840 is not important for future immigration status.

Some may underestimate the importance of Form 8840 in relation to future immigration considerations. Establishing a closer connection to another country might impact your immigration status or residency claims, so it should not be overlooked.

Misconception 7: Filing Form 8840 means you won’t owe taxes.

Lastly, the assumption that filing this form negates tax obligations is misleading. Form 8840 serves to clarify your tax residency status and does not eliminate the possibility of owing taxes based on U.S. sourced income.

Understanding these misconceptions can help clarify the purpose of Form 8840 and ensure compliance with IRS requirements. When in doubt, always seek advice from a qualified tax professional.

When filling out and utilizing the IRS Form 8840, it is important to keep several key points in mind. This form is primarily used by individuals who wish to claim the closer connection exception to the substantial presence test.

Following these guidelines can help ensure that your use of the IRS Form 8840 goes smoothly. Being thorough and organized will increase the likelihood of a successful outcome.