Understanding the IRS 8821 form is crucial for anyone who needs a designated representative to handle their tax matters. This form allows taxpayers to authorize one or more individuals to receive and review confidential tax information from the IRS on their behalf. Whether you’re dealing with a tax advisor, accountant, or another representative, having the right paperwork in place can help streamline communication with the IRS. The form itself is straightforward, requiring basic information about you, your representative, and the tax matters in question. It’s essential to ensure accuracy as you fill it out, as any discrepancies can lead to delays. The 8821 governs the scope of access your representative will have, so clarity here is key. Once completed, it must be submitted to the IRS for processing, giving your chosen representative the authority to engage with the agency regarding your tax issues. With this form, you can confidently ensure your tax matters are managed effectively and efficiently.

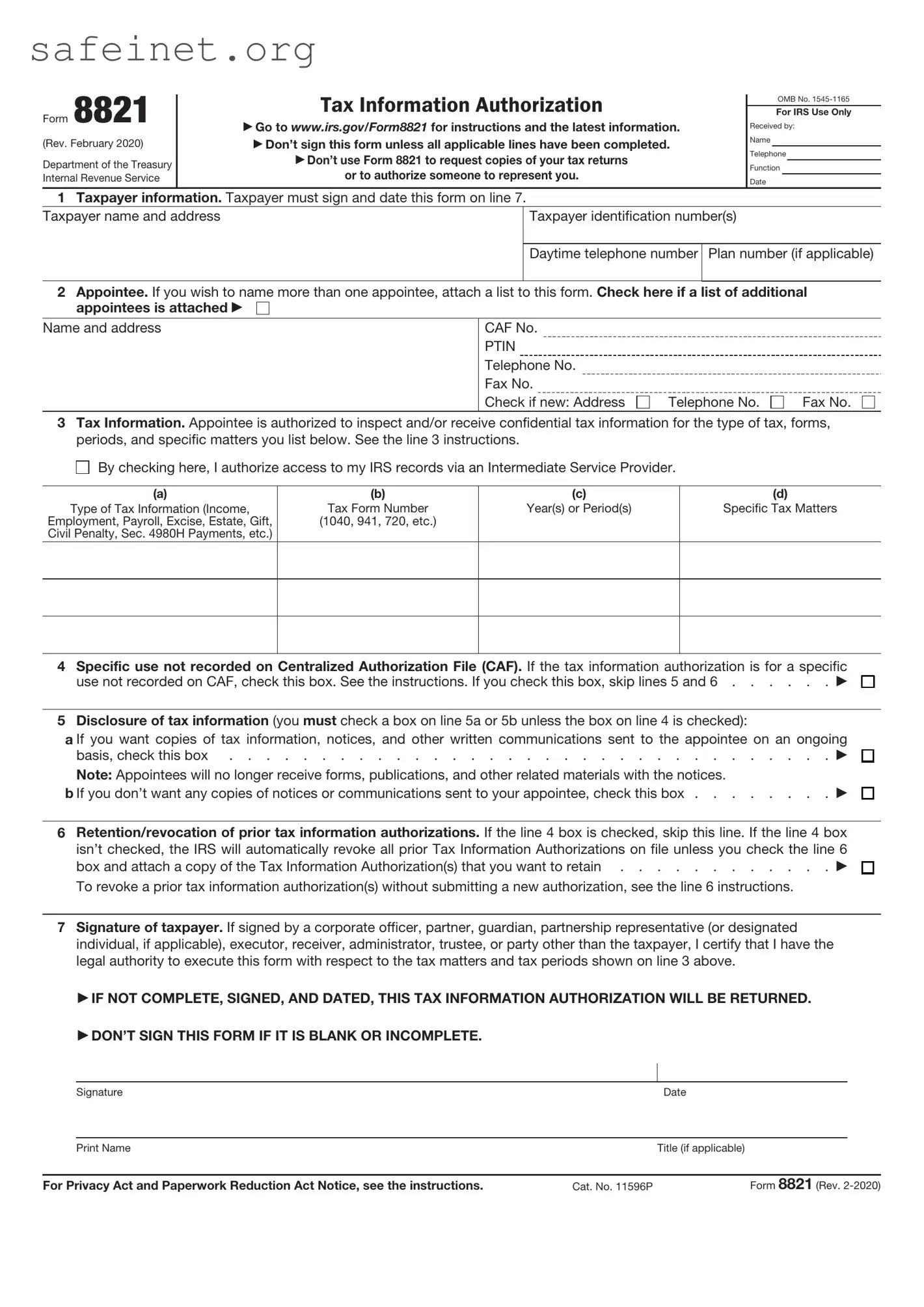

Form 8821

(Rev. February 2020)

Department of the Treasury Internal Revenue Service

Tax Information Authorization

Go to www.irs.gov/Form8821 for instructions and the latest information. Don’t sign this form unless all applicable lines have been completed.

Don’t use Form 8821 to request copies of your tax returns or to authorize someone to represent you.

OMB No.

For IRS Use Only

Received by:

Name

Telephone

Function

Date

1Taxpayer information. Taxpayer must sign and date this form on line 7.

Taxpayer name and address |

Taxpayer identification number(s) |

Daytime telephone number

Plan number (if applicable)

2Appointee. If you wish to name more than one appointee, attach a list to this form. Check here if a list of additional

appointees is attached

Name and address

CAF No.

PTIN Telephone No. Fax No.

Check if new: Address

Telephone No.

Fax No.

3Tax Information. Appointee is authorized to inspect and/or receive confidential tax information for the type of tax, forms, periods, and specific matters you list below. See the line 3 instructions.

By checking here, I authorize access to my IRS records via an Intermediate Service Provider.

By checking here, I authorize access to my IRS records via an Intermediate Service Provider.

(a) |

(b) |

(c) |

(d) |

Type of Tax Information (Income, |

Tax Form Number |

Year(s) or Period(s) |

Specific Tax Matters |

Employment, Payroll, Excise, Estate, Gift, |

(1040, 941, 720, etc.) |

|

|

Civil Penalty, Sec. 4980H Payments, etc.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 Specific use not recorded on Centralized Authorization File (CAF). If the tax information authorization is for a specific

use not recorded on CAF, check this box. See the instructions. If you check this box, skip lines 5 and 6 . . . . . .

5Disclosure of tax information (you must check a box on line 5a or 5b unless the box on line 4 is checked):

a If you want copies of tax information, notices, and other written communications sent to the appointee on an ongoing basis, check this box . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Note: Appointees will no longer receive forms, publications, and other related materials with the notices.

b If you don’t want any copies of notices or communications sent to your appointee, check this box . . . . . . . .

6Retention/revocation of prior tax information authorizations. If the line 4 box is checked, skip this line. If the line 4 box isn’t checked, the IRS will automatically revoke all prior Tax Information Authorizations on file unless you check the line 6

box and attach a copy of the Tax Information Authorization(s) that you want to retain . . . . . . . . . . . .

To revoke a prior tax information authorization(s) without submitting a new authorization, see the line 6 instructions.

7Signature of taxpayer. If signed by a corporate officer, partner, guardian, partnership representative (or designated individual, if applicable), executor, receiver, administrator, trustee, or party other than the taxpayer, I certify that I have the legal authority to execute this form with respect to the tax matters and tax periods shown on line 3 above.

IF NOT COMPLETE, SIGNED, AND DATED, THIS TAX INFORMATION AUTHORIZATION WILL BE RETURNED.

DON’T SIGN THIS FORM IF IT IS BLANK OR INCOMPLETE.

|

Signature |

|

Date |

|

|

|

|

|

|

|

Print Name |

|

Title (if applicable) |

|

|

|

|

|

|

For Privacy Act and Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 11596P |

Form 8821 (Rev. |

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 8821 allows taxpayers to designate a third party to receive and inspect their confidential tax information. |

| Eligibility | Any individual or entity can file this form to authorize another individual or organization to obtain tax information from the IRS on their behalf. |

| Effective Date | This form remains in effect until revoked by the taxpayer or until the taxpayer's death or legal incapacity. |

| Filing Requirement | Taxpayers must submit Form 8821 to the IRS only once per representative, although it can be revoked and replaced at any time. |

| State-Specific Forms | States often have similar forms that serve as authorizations for local tax matters. For example, California uses Form 3520, governed under Rev. & Tax Code Sections 18621 and 18622. |

Completing the IRS Form 8821 is an essential step for authorizing someone to receive your tax information. The following steps will help you accurately fill out the form. Ensure all sections are complete to avoid delays.

Once submitted, the IRS will process your request. You should allow some time for processing and confirm the designee’s access to the tax information you specified.

What is IRS Form 8821?

IRS Form 8821, also known as the "Tax Information Authorization," is a document that allows individuals or entities to authorize another person to receive and inspect their confidential tax information. The authorized person can be a tax professional or someone trusted in dealings with the IRS.

Who can file Form 8821?

Any taxpayer can file Form 8821, whether an individual or a business entity. The form is meant for anyone who wishes to permit another person to have access to their tax information without granting the authority to represent them before the IRS.

What type of information can be accessed using Form 8821?

Form 8821 allows the designated individual to access various tax information, including tax returns, account information, and other tax-related documents for the years specified on the form. However, it does not allow the representative to act on behalf of the taxpayer.

How do I complete Form 8821?

To complete Form 8821, provide your personal information at the top, including your name, address, and Social Security number or Employer Identification Number (EIN). Next, enter the name and information of the designated representative. Specify the types of tax information you are authorizing access to, and list the years for which this authorization applies. Finally, sign and date the form.

Can I revoke Form 8821 after it is filed?

Yes, you can revoke Form 8821 at any time. To do this, you should submit a written statement to the IRS clearly stating your intent to revoke authorization and identify the specific Form 8821 that you wish to revoke.

How long does Form 8821 remain in effect?

Form 8821 remains in effect until the specified expiration date, which can be set for up to one year from the date of signing, or until it is revoked. If no expiration date is set, it will last indefinitely until either of the two scenarios occurs.

Do I need to submit Form 8821 for each tax year?

If you want your representative to have access to information for more than one tax year, you can specify multiple years on the same Form 8821. If you need a new authorization in a subsequent year, you should file a new form with the updated information.

Is Form 8821 the same as Form 2848?

No, Form 8821 is different from Form 2848, the "Power of Attorney and Declaration of Representative." While Form 8821 allows the designated individual to obtain tax information, Form 2848 provides the representative with the authority to act on your behalf before the IRS, including making decisions and filing documents.

Where do I send Form 8821?

Form 8821 should be sent to the appropriate IRS office based on the type of tax information needed and your location. The specific mailing address and details can be found in the instructions included with the form. It’s advisable to send the form via certified mail for tracking purposes.

Is there a fee associated with filing Form 8821?

There is no fee for filing IRS Form 8821. Taxpayers can fill out and submit the form freely, depending solely on their need for a designated representative to access their tax information.

Missing Required Information: Failing to provide complete names, addresses, or identification numbers of both the taxpayer and the representative can delay processing.

Incorrect Identification Numbers: Miswriting Social Security numbers or Employer Identification Numbers can lead to the rejection of the form.

Not Signing the Form: The taxpayer's signature is essential. Omitting it will render the submission invalid.

Choosing the Wrong Type of Representation: Selecting an incorrect designation for the type of authority granted can confuse the IRS.

Failure to Specify Applicable Tax Years: Not indicating the specific tax years or periods can limit the representative’s ability to assist effectively.

Not Updating Information: If contact details or circumstances change, failing to submit a new form with updated information is a common error.

Neglecting to Check for Completeness: Before submission, not reviewing the entire form can result in overlooked mistakes.

Ignoring IRS Submission Guidelines: Failure to follow specific IRS instructions for mailing the form can cause unnecessary delays.

Not Retaining a Copy: Forgetting to keep a copy of the submitted form for personal records can create issues in the future.

Using Outdated Forms: Submitting an old version of the IRS 8821 can lead to processing issues, as the IRS updates forms periodically.

The IRS Form 8821 is used to appoint a third party to receive confidential tax information. It is important to know what other forms and documents may be needed in conjunction with this form. Here are some commonly used documents that might accompany Form 8821.

Being aware of these forms can help ensure that all necessary information is provided when dealing with the IRS. This practice will streamline the process of managing tax matters efficiently.

The IRS Form 4506 is similar to Form 8821 in that both are used to grant authorization related to tax information. Form 4506 allows individuals to request a copy of their tax returns from the IRS, while Form 8821 permits individuals to designate someone to receive their tax information without granting them the authority to file on their behalf. Both forms ensure that the taxpayer's information is handled with consent, providing a safeguard against unauthorized access.

Form 8879, the IRS e-file Signature Authorization, is another document that resonates with Form 8821. While Form 8821 designates an individual to receive tax information, Form 8879 is used to electronically sign a tax return. The connection lies in the need for taxpayer consent in both cases. However, Form 8879 places emphasis on electronically filing the return, whereas Form 8821 focuses solely on the sharing of information.

The IRS Form 2848, Power of Attorney and Declaration of Representative, is quite similar to Form 8821. Both forms allow taxpayers to designate representatives. However, Form 2848 grants broader authority, allowing representatives to act on behalf of the taxpayer, including filing returns, while Form 8821 strictly limits the authority to accessing information. Thus, while sharing a purpose of representation, they differ significantly in the scope of that representation.

Form 1040, the standard individual income tax return, shares some similarities with Form 8821 in terms of being integral to the tax filing process. While Form 1040 is used to report income and calculate tax liability, Form 8821 allows taxpayers to authorize someone to access their tax documents associated with the return. Both play vital roles in ensuring compliance and transparency in tax matters.

The IRS Form 4506-T, Request for Transcript of Tax Return, is comparable to Form 8821 as both facilitate access to taxpayer information. Form 4506-T allows taxpayers to request a transcript of their tax return to review or verify tax information. Similarly, Form 8821 enables a designee to obtain information from the IRS about the taxpayer's accounts and returns. Both forms ensure proper protocols are followed when handling sensitive financial data.

Form 9465, Installment Agreement Request, relates to Form 8821 through its focus on taxpayer communication with the IRS. While Form 9465 allows taxpayers to propose a payment plan for unpaid taxes, Form 8821 ensures that a designated individual can discuss and verify tax account details without affecting payment responsibilities. Both forms are essential in facilitating the management of taxpayer obligations.

Form 1098, Mortgage Interest Statement, is similar in that it involves the sharing of tax-related information, albeit between different parties. Form 1098 provides details about mortgage interest paid, which is cogent for tax deductions. In contrast, Form 8821 allows the recipient to access any information in the taxpayer's file, linking to the larger theme of transparency in tax affairs.

The IRS Form 5498, IRA Contribution Information, aligns with Form 8821 through its function of notifying taxpayers about specific financial activities that impact their tax filings. Form 5498 documents contributions to individual retirement accounts, while Form 8821 allows individuals to authorize someone to obtain information about their overall tax status, including contributions that may affect their tax liabilities.

Lastly, Form 1099, which reports various types of income other than wages, is somewhat akin to Form 8821 due to its role in informing taxpayers about income that must be reported to the IRS. Form 8821 ensures taxpayers can involve appointed individuals to access tax information, which may include details submitted through various 1099 forms. Both reinforce the importance of accurate reporting and understanding one's tax situation.

When filling out the IRS Form 8821, which authorizes third parties to receive and inspect confidential tax information, there are important guidelines to follow. Here’s a helpful list of things to consider.

The IRS Form 8821, also known as the Tax Information Authorization form, can often be misunderstood. Below is a list of common misconceptions about this form, along with clarifications to ensure better understanding.

This is not correct. While the form allows an individual or organization to receive your tax information, it does not give them authority to act on your behalf or make decisions related to your tax matters.

This is misleading. You can specify which tax years or specific tax matters an appointee can access, limiting the information to what is necessary.

Not necessarily. A submitted Form 8821 remains in effect until you revoke it or until the specific tax matter is resolved. However, if you wish to change your representative, a new form should be submitted.

This is incorrect. You might also choose to complete this form to facilitate communication with your tax preparer or advisor, even when there are no active tax issues.

This misconception arises often. While the IRS allows some forms to be submitted electronically, Form 8821 must be mailed or submitted via fax to the IRS, as electronic submission is not currently an option.

This is not true. The IRS does not take immediate action. They process forms in the order they are received, and there may be delays. Patience is often required.

In reality, the form is relatively straightforward. It requires basic information like your name, address, and the representative’s details, making it accessible for most taxpayers.

Filling out and using the IRS Form 8821 is crucial for taxpayers who wish to authorize someone to receive confidential tax information. Here are key takeaways to keep in mind: