The IRS 8332 form plays a crucial role in the lives of divorced or separated parents who share custody of their children. This form allows one parent to release their claim to the child’s tax exemption, enabling the other parent to claim it on their tax return. It is essential for those navigating custody arrangements and tax responsibilities to understand the implications of this form. By completing and submitting IRS 8332, the custodial parent can formally grant the non-custodial parent the right to claim the child as a dependent, which can lead to significant tax benefits. Additionally, the form outlines specific conditions under which the exemption can be claimed, ensuring clarity and compliance with IRS regulations. Understanding how to properly fill out and file this form is vital for parents looking to maximize their tax benefits while fulfilling their obligations to their children.

Form 8332 |

|

|

Release/Revocation of Release of Claim |

|

OMB No. |

|||

|

|

|||||||

|

|

|

|

|

|

|

||

|

|

|

to Exemption for Child by Custodial Parent |

|

|

|

||

(Rev. October 2018) |

|

|

|

Attachment |

115 |

|||

Department of the Treasury |

|

|

▶ Attach a separate form for each child. |

|

Sequence No. |

|||

|

|

▶ Go to www.irs.gov/Form8332 for the latest information. |

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

|||

Name of noncustodial parent |

|

|

|

Noncustodial parent’s |

|

|

|

|

|

|

|

|

social security number (SSN) ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

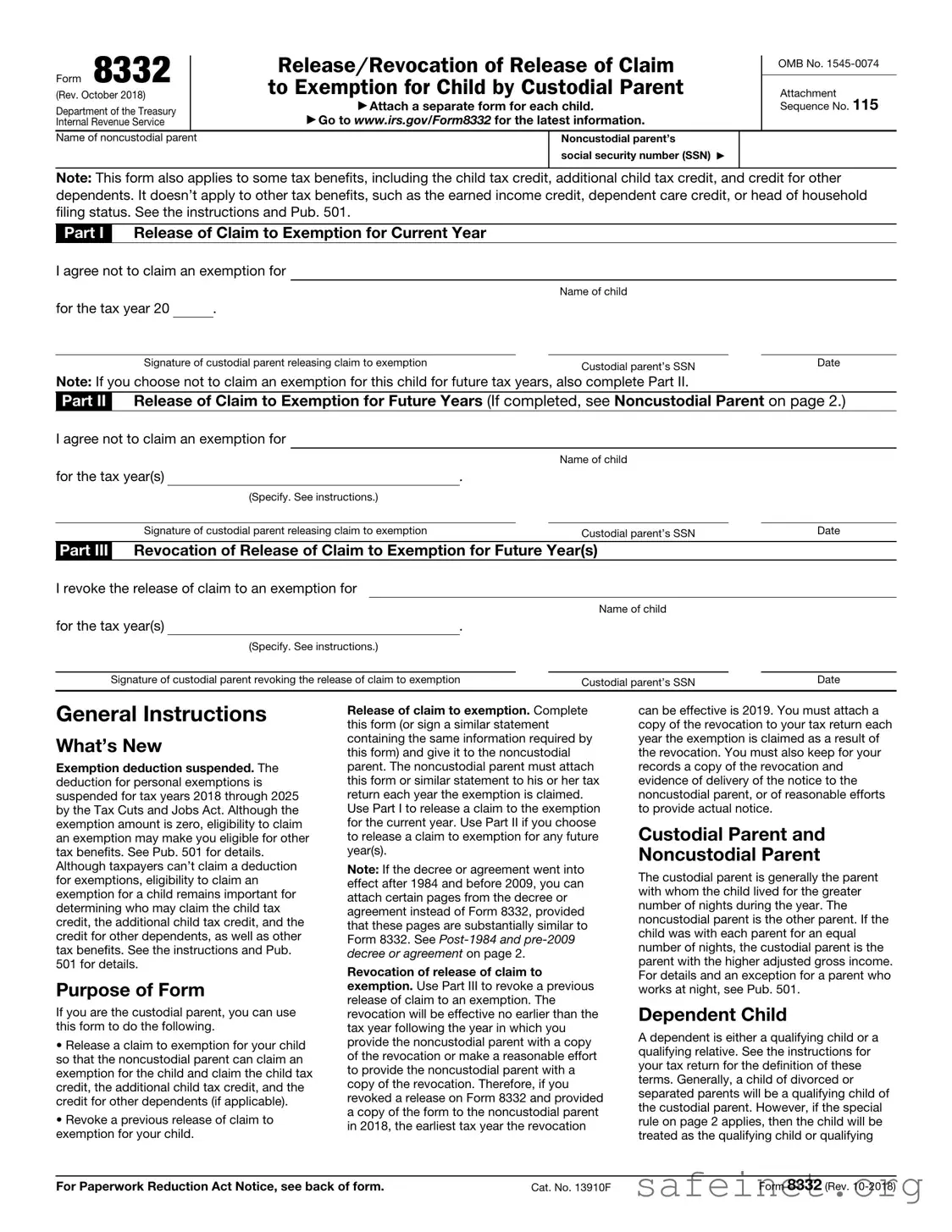

Note: This form also applies to some tax benefits, including the child tax credit, additional child tax credit, and credit for other dependents. It doesn’t apply to other tax benefits, such as the earned income credit, dependent care credit, or head of household filing status. See the instructions and Pub. 501.

Part I Release of Claim to Exemption for Current Year

I agree not to claim an exemption for

Name of child

for the tax year 20 |

|

. |

Signature of custodial parent releasing claim to exemption |

|

Custodial parent’s SSN |

|

Date |

|

|

|

|

Note: If you choose not to claim an exemption for this child for future tax years, also complete Part II.

Part II Release of Claim to Exemption for Future Years (If completed, see Noncustodial Parent on page 2.)

I agree not to claim an exemption for

|

|

|

|

|

Name of child |

|

|

for the tax year(s) |

. |

|

|

|

|

||

|

(Specify. See instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of custodial parent releasing claim to exemption |

|

|

|

Custodial parent’s SSN |

|

Date |

|

Part III Revocation of Release of Claim to Exemption for Future Year(s)

I revoke the release of claim to an exemption for

|

|

|

|

Name of child |

|

|

for the tax year(s) |

. |

|

|

|

|

|

|

(Specify. See instructions.) |

|

|

|

|

|

|

|

|

|

|

||

Signature of custodial parent revoking the release of claim to exemption |

|

Custodial parent’s SSN |

|

Date |

||

General Instructions

What’s New

Exemption deduction suspended. The deduction for personal exemptions is suspended for tax years 2018 through 2025 by the Tax Cuts and Jobs Act. Although the exemption amount is zero, eligibility to claim an exemption may make you eligible for other tax benefits. See Pub. 501 for details. Although taxpayers can’t claim a deduction for exemptions, eligibility to claim an exemption for a child remains important for determining who may claim the child tax credit, the additional child tax credit, and the credit for other dependents, as well as other tax benefits. See the instructions and Pub. 501 for details.

Purpose of Form

If you are the custodial parent, you can use this form to do the following.

•Release a claim to exemption for your child so that the noncustodial parent can claim an exemption for the child and claim the child tax credit, the additional child tax credit, and the credit for other dependents (if applicable).

•Revoke a previous release of claim to exemption for your child.

Release of claim to exemption. Complete this form (or sign a similar statement containing the same information required by this form) and give it to the noncustodial parent. The noncustodial parent must attach this form or similar statement to his or her tax return each year the exemption is claimed. Use Part I to release a claim to the exemption for the current year. Use Part II if you choose to release a claim to exemption for any future year(s).

Note: If the decree or agreement went into effect after 1984 and before 2009, you can attach certain pages from the decree or agreement instead of Form 8332, provided that these pages are substantially similar to Form 8332. See

Revocation of release of claim to exemption. Use Part III to revoke a previous release of claim to an exemption. The revocation will be effective no earlier than the tax year following the year in which you provide the noncustodial parent with a copy of the revocation or make a reasonable effort to provide the noncustodial parent with a copy of the revocation. Therefore, if you revoked a release on Form 8332 and provided a copy of the form to the noncustodial parent in 2018, the earliest tax year the revocation

can be effective is 2019. You must attach a copy of the revocation to your tax return each year the exemption is claimed as a result of the revocation. You must also keep for your records a copy of the revocation and evidence of delivery of the notice to the noncustodial parent, or of reasonable efforts to provide actual notice.

Custodial Parent and

Noncustodial Parent

The custodial parent is generally the parent with whom the child lived for the greater number of nights during the year. The noncustodial parent is the other parent. If the child was with each parent for an equal number of nights, the custodial parent is the parent with the higher adjusted gross income. For details and an exception for a parent who works at night, see Pub. 501.

Dependent Child

A dependent is either a qualifying child or a qualifying relative. See the instructions for your tax return for the definition of these terms. Generally, a child of divorced or separated parents will be a qualifying child of the custodial parent. However, if the special rule on page 2 applies, then the child will be treated as the qualifying child or qualifying

For Paperwork Reduction Act Notice, see back of form. |

Cat. No. 13910F |

Form 8332 (Rev. |

Form 8332 (Rev. |

Page 2 |

relative of the noncustodial parent for purposes of the dependency exemption, the child tax credit, the additional child tax credit, and the credit for other dependents.

Special Rule for Children of Divorced or Separated Parents

A child is treated as a qualifying child or a qualifying relative of the noncustodial parent if all of the following apply.

1.The child received over half of his or her support for the year from one or both of the parents (see the Exception below). If you received payments under the Temporary Assistance for Needy Families (TANF) program or other public assistance program and you used the money to support the child, see Pub. 501.

2.The child was in the custody of one or both of the parents for more than half of the year.

3.Either of the following applies.

a. The custodial parent agrees not to claim an exemption for the child by signing this form or a similar statement. If the decree or agreement went into effect after 1984 and before 2009, see

b. A

For this rule to apply, the parents must be one of the following.

•Divorced or legally separated under a decree of divorce or separate maintenance.

•Separated under a written separation agreement.

•Living apart at all times during the last 6 months of the year.

If this rule applies, and the other dependency tests in the instructions for your tax return are also met, the noncustodial parent can claim an exemption for the child.

Exception. If the support of the child is determined under a multiple support agreement, this special rule does not apply, and this form should not be used.

instead of Form 8332, provided that these pages are substantially similar to Form 8332. To be able to do this, the decree or agreement must state all three of the following.

1.The noncustodial parent can claim the child as a dependent without regard to any condition (such as payment of support).

2.The other parent will not claim the child as a dependent.

3.The years for which the claim is released.

The noncustodial parent must attach all of the following pages from the decree or agreement.

•Cover page (include the other parent’s SSN on that page).

•The pages that include all of the information identified in (1) through (3) above.

•Signature page with the other parent’s signature and date of agreement.

The noncustodial parent must ▲! attach the required information

even if it was filed with a return in CAUTION an earlier year.

Specific Instructions

Custodial Parent

Part I. Complete Part I to release a claim to exemption for your child for the current tax year.

Part II. Complete Part II to release a claim to exemption for your child for one or more future years. Write the specific future year(s) or “all future years” in the space provided in Part II.

To help ensure future support, you TIP may not want to release your

claim to the exemption for the child for future years.

Part III. Complete Part III if you are revoking a previous release of claim to exemption for your child. Write the specific future year(s) or “all future years” in the space provided in Part III.

The revocation will be effective no earlier than the tax year following the year you provide the noncustodial parent with a copy of the revocation or make a reasonable effort to provide the noncustodial parent with a copy of the revocation. Also, you must attach a copy of the revocation to your tax return for each year you are claiming the exemption as a result of the revocation. You must also keep for your records a copy of the revocation and evidence of delivery of the notice to the noncustodial parent, or of reasonable efforts to provide actual notice.

Example. In 2015, you released a claim to exemption for your child on Form 8332 for the years 2016 through 2020. In 2018, you decided to revoke the previous release of exemption. If you completed Part III of Form 8332 and provided a copy of the form to the noncustodial parent in 2018, the revocation will be effective for 2019 and 2020. You must attach a copy of the revocation to your 2019 and 2020 tax returns and keep certain records as stated earlier.

Noncustodial Parent

Attach this form or similar statement to your tax return for each year you claim the exemption for your child. You can claim the exemption only if the other dependency tests in the instructions for your tax return are met.

If the custodial parent released his TIP or her claim to the exemption for

the child for any future year, you must attach a copy of this form or similar statement to your tax return

for each future year that you claim the exemption. Keep a copy for your records.

Note: If you are filing your return electronically, you must file Form 8332 with Form 8453, U.S. Individual Income Tax Transmittal for an IRS

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You aren’t required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by Internal Revenue Code section 6103.

The average time and expenses required to complete and file this form will vary depending on individual circumstances. For the estimated averages, see the instructions for your income tax return.

If you have suggestions for making this form simpler, we would be happy to hear from you. See the instructions for your income tax return.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 8332 allows a custodial parent to release a claim to exemption for a child, enabling the non-custodial parent to claim the child as a dependent on their tax return. |

| Eligibility | Only custodial parents can complete this form. The custodial parent is the one with whom the child lived for the greater part of the year. |

| Usage | This form is typically used in divorce or separation situations where parents share custody of a child. |

| Submission | Form 8332 does not need to be submitted with the tax return. However, it should be kept with tax records in case of an audit. |

| State-Specific Forms | Some states may have their own forms or requirements for claiming a child as a dependent. Always check local laws for any additional documentation needed. |

After obtaining the IRS 8332 form, you will need to provide accurate information to ensure proper processing. Follow these steps carefully to complete the form correctly.

What is the IRS Form 8332?

The IRS Form 8332 is a document that allows a custodial parent to release their claim to a child's dependency exemption to the non-custodial parent. This form is especially important in cases of divorce or separation where parents share custody of a child. By completing and signing this form, the custodial parent grants permission for the non-custodial parent to claim the child as a dependent on their tax return.

Who needs to fill out Form 8332?

Typically, the custodial parent—the one with whom the child lives for the greater part of the year—needs to fill out Form 8332. If the custodial parent agrees to let the non-custodial parent claim the child as a dependent, they should complete this form. It's important to note that both parents must agree on this arrangement, and the custodial parent must sign the form for it to be valid.

How do I complete Form 8332?

Completing Form 8332 is straightforward. First, provide the names and Social Security numbers of both parents and the child. Next, indicate the tax year for which the exemption is being released. Finally, sign and date the form. It's a good idea to keep a copy for your records. The non-custodial parent must attach this form to their tax return when claiming the child as a dependent.

Is Form 8332 required every year?

Not necessarily. If the custodial parent grants the non-custodial parent the right to claim the child as a dependent for multiple years, they can indicate this on the form. However, if the arrangement changes or if the custodial parent decides to revoke the release, a new Form 8332 must be completed. Always check the latest IRS guidelines to ensure compliance.

What if I don’t file Form 8332 but still claim the child?

If the non-custodial parent claims the child without the signed Form 8332, it could lead to complications. The IRS may disallow the claim, resulting in penalties or adjustments to tax returns. To avoid issues, always ensure that Form 8332 is properly filled out and submitted with the tax return when claiming a child as a dependent.

Where can I find Form 8332?

Form 8332 can be easily found on the IRS website. Simply visit the forms section, and you can download it for free. Additionally, many tax preparation software programs include this form, making it easy to fill out as part of your tax filing process. If you need assistance, consider reaching out to a tax professional who can guide you through the process.

Missing Signatures: One common mistake is failing to sign the form. Without a signature, the IRS will not accept the document, which can lead to complications during tax filing.

Incorrect Dates: Many people overlook the importance of filling in the correct dates. This includes the date of signing the form and the tax year for which the form applies. Errors in dates can result in delays or rejection of the form.

Not Including All Required Information: The IRS 8332 form requires specific information, such as the custodial parent's name and Social Security number. Omitting any of these details can render the form invalid.

Using an Outdated Version: Tax forms can change from year to year. Submitting an outdated version of the IRS 8332 form may lead to issues with processing. Always check for the most current version before submitting.

Filing with Incomplete Documentation: Sometimes, individuals forget to attach necessary documentation, such as proof of custody arrangements. This can lead to delays in processing and potential disputes over tax deductions.

The IRS 8332 form allows a custodial parent to release their claim to the child’s tax exemption to the non-custodial parent. When filing taxes, several other documents may be relevant to ensure a smooth process. Below is a list of forms and documents that are often used in conjunction with the IRS 8332 form.

These documents play a vital role in ensuring compliance with tax regulations and maximizing potential benefits. Having them organized can streamline the filing process and help avoid delays or issues with the IRS.

The IRS Form 8332 allows a custodial parent to release a claim to a child's tax exemption to the non-custodial parent. A similar document is Form 8862, which is used to claim the Earned Income Tax Credit (EITC) after a prior disallowance. Like Form 8332, Form 8862 requires specific information and documentation to support the claim. Both forms aim to clarify eligibility and ensure that tax benefits are appropriately assigned, helping to prevent disputes between parents regarding tax exemptions and credits.

Another comparable document is Form 1040, the U.S. Individual Income Tax Return. While Form 8332 deals specifically with the transfer of a tax exemption for dependents, Form 1040 is the overall tax return that reports income, deductions, and credits. Both forms require accurate information about dependents and their tax implications. They serve to ensure that taxpayers claim the correct benefits and comply with IRS regulations, thus streamlining the tax filing process.

Form 2441, which is used to claim the Child and Dependent Care Credit, also shares similarities with Form 8332. Both forms address tax benefits related to dependents, albeit in different contexts. Form 2441 focuses on expenses incurred for child care, while Form 8332 pertains to exemptions. Each form requires documentation to substantiate claims and must be filed with the taxpayer's return, reinforcing the importance of maintaining accurate records for tax purposes.

Lastly, Form 8863, which is used to claim education credits, is another document that aligns with Form 8332 in terms of dependents. Both forms require the taxpayer to provide information about qualifying dependents and their associated benefits. While Form 8863 is specifically for education-related expenses, both forms emphasize the necessity of proper documentation and the accurate reporting of dependent-related claims, ensuring that taxpayers receive the credits and exemptions they are entitled to.

When filling out the IRS 8332 form, there are important guidelines to follow. Here is a list of things you should and shouldn't do:

The IRS Form 8332 is an important document related to child custody and tax benefits. However, several misconceptions surround this form that can lead to confusion for parents. Below are five common misconceptions, along with clarifications to help ensure accurate understanding.

While this form allows the custodial parent to release their claim to the child as a dependent, it does not automatically ensure the non-custodial parent can claim the child. The non-custodial parent must still meet all other IRS requirements for claiming a dependent.

Although the custodial parent typically completes the form, both parents must agree to the arrangement. The non-custodial parent may need to provide information or sign off on the agreement.

This form is not limited to divorced parents. It is also relevant for unmarried parents or those who have separated but not legally divorced. Any situation where one parent claims a child as a dependent may require this form.

This is not accurate. The custodial parent can revoke the release of the dependency exemption in future tax years. However, they must do so in writing, and the revocation must comply with IRS guidelines.

While it is advisable to keep Form 8332 with tax records, it does not need to be submitted with the tax return. Instead, it should be made available if the IRS requests it during an audit.

Understanding these misconceptions can help parents navigate the complexities of tax benefits related to children. Clarity on this form can lead to more informed decisions and smoother tax filing experiences.

Understanding the IRS 8332 form is crucial for divorced or separated parents who wish to allocate the tax benefits of claiming a child as a dependent. Here are some key takeaways: