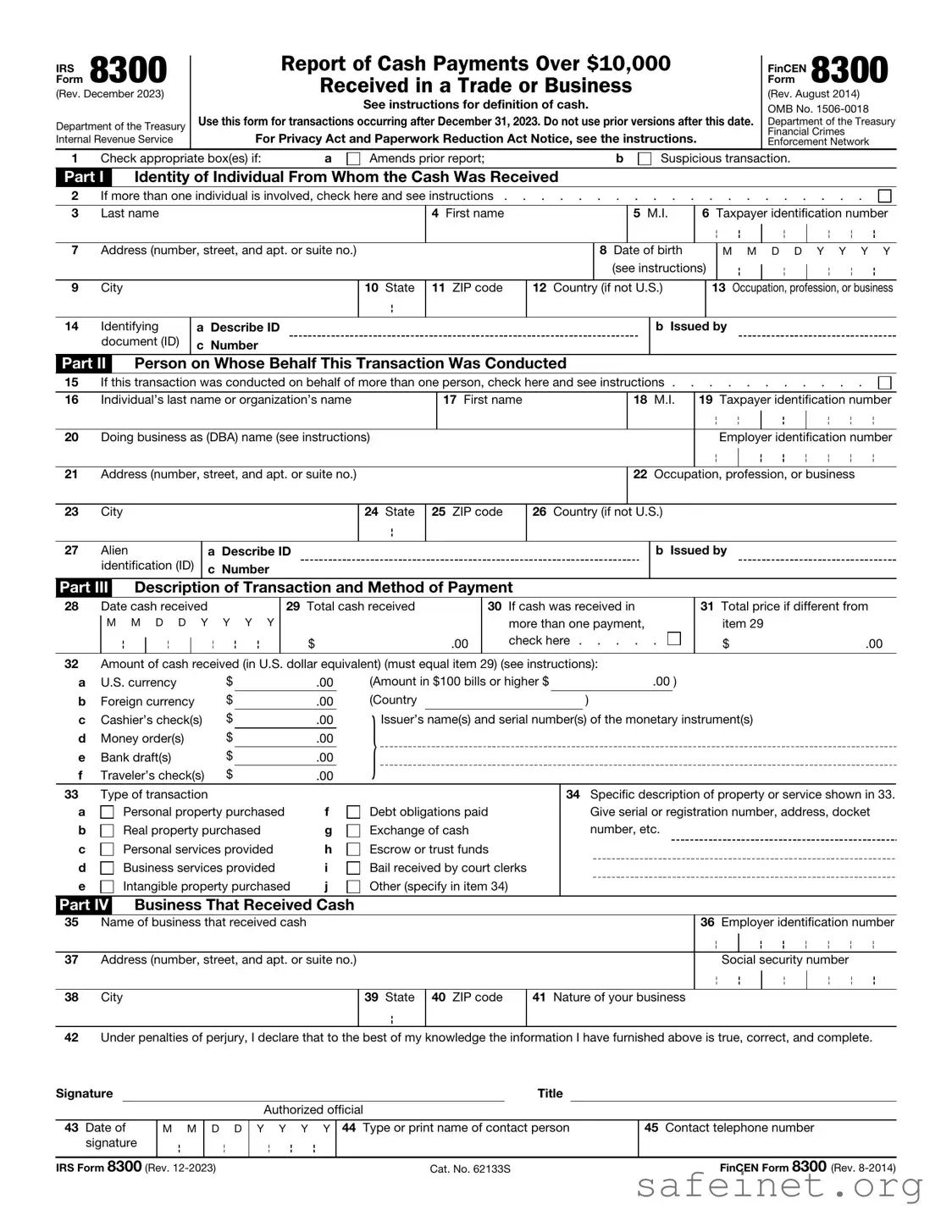

The IRS 8300 form plays a crucial role in the world of financial transactions, particularly when large sums of cash are involved. Businesses and individuals must be aware of the requirements surrounding this form, as it helps the government track significant cash payments. If you receive more than $10,000 in cash for goods or services, you are required to report this to the IRS using Form 8300. This reporting not only ensures compliance with federal regulations but also aids in the prevention of money laundering and other illicit activities. The form requires detailed information, including the identity of the payer, the amount received, and the nature of the transaction. Timeliness is essential; the form must be filed within 15 days of receiving the cash. Failing to report these transactions can lead to penalties, making it imperative for businesses to understand their obligations. Whether you are a small business owner or an individual receiving a large cash payment, knowing how to properly complete and submit the IRS 8300 form is essential for staying on the right side of the law.

IRS 8300

Form

(Rev. December 2023)

Department of the Treasury Internal Revenue Service

Report of Cash Payments Over $10,000

Received in a Trade or Business

See instructions for definition of cash.

Use this form for transactions occurring after December 31, 2023. Do not use prior versions after this date.

For Privacy Act and Paperwork Reduction Act Notice, see the instructions.

FinCEN 8300 Form

(Rev. August 2014)

OMB No.

Department of the Treasury

Financial Crimes

Enforcement Network

1 Check appropriate box(es) if: |

a |

Amends prior report; |

b |

Part I Identity of Individual From Whom the Cash Was Received

Suspicious transaction.

2 |

If more than one individual is involved, check here and see instructions |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

4 First name |

|

|

5 M.I. |

6 Taxpayer identification number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

|

8 Date of birth |

|

|

M M D D Y Y Y Y |

|||

|

|

|

|

|

(see instructions) |

|

|||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

9 |

City |

10 State |

11 ZIP code |

12 Country |

(if not U.S.) |

|

13 Occupation, profession, or business |

||||

|

|

|

|

|

|

|

|

|

|

|

|

14 Identifying |

a |

Describe ID |

document (ID) |

c |

Number |

Part II Person on Whose Behalf This Transaction Was Conducted

b Issued by

15 |

If this transaction was conducted on behalf of more than one person, check here and see instructions |

|||

|

|

|

|

|

16 |

Individual’s last name or organization’s name |

17 First name |

18 M.I. |

19 Taxpayer identification number |

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27 Alien |

a |

Describe ID |

identification (ID) |

c |

Number |

Part III Description of Transaction and Method of Payment

b Issued by

28Date cash received

M M D D Y Y Y Y

29Total cash received

$.00

30If cash was received in more than one payment, check here . . . . .

31Total price if different from item 29

$.00

32Amount of cash received (in U.S. dollar equivalent) (must equal item 29) (see instructions):

a |

U.S. currency |

$ |

.00 |

(Amount in $100 bills or higher $ |

.00 ) |

||||

b |

Foreign currency |

$ |

.00 |

(Country |

) |

|

|||

|

|

$ |

|

} |

|

|

|

||

c |

Cashier’s check(s) |

.00 |

Issuer’s name(s) and serial number(s) of the monetary instrument(s) |

||||||

d |

Money order(s) |

$ |

.00 |

|

|

|

|

|

|

e |

Bank draft(s) |

$ |

.00 |

|

|

|

|

|

|

f |

Traveler’s check(s) |

$ |

.00 |

|

|

|

|

|

|

33Type of transaction

a |

Personal property purchased |

f |

b |

Real property purchased |

g |

c |

Personal services provided |

h |

d |

Business services provided |

i |

e |

Intangible property purchased |

j |

Part IV |

Business That Received Cash |

|

Debt obligations paid Exchange of cash Escrow or trust funds

Bail received by court clerks Other (specify in item 34)

34Specific description of property or service shown in 33. Give serial or registration number, address, docket number, etc.

35Name of business that received cash

36Employer identification number

37Address (number, street, and apt. or suite no.)

Social security number

38City

39State

40ZIP code

41Nature of your business

42Under penalties of perjury, I declare that to the best of my knowledge the information I have furnished above is true, correct, and complete.

Signature |

|

|

|

|

|

Title |

|

|

|

|

|

|

Authorized official |

|

|

||

|

|

|

|

|

|

|

||

43 Date of |

M M |

D D |

Y Y Y Y |

44 Type or print name of contact person |

|

45 Contact telephone number |

||

signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

IRS Form 8300 (Rev. |

|

Cat. No. 62133S |

|

FinCEN Form 8300 (Rev. |

||||

IRS Form 8300 (Rev. |

Page 2 |

FinCEN Form 8300 (Rev. |

Multiple Parties

(Complete applicable parts below if box 2 or 15 on page 1 is checked.)

Part I

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

Part II

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

Comments – Please use the lines provided below to comment on or clarify any information you entered on any line in Parts I, II, III, and IV

IRS Form 8300 (Rev. |

FinCEN Form 8300 (Rev. |

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 8300 is used to report cash payments exceeding $10,000 received in a trade or business. |

| Filing Requirement | Businesses must file Form 8300 within 15 days of receiving cash payments over the threshold. |

| Definition of Cash | Cash includes currency, cashier's checks, money orders, and negotiable instruments. |

| Penalties | Failure to file Form 8300 can result in significant penalties, including fines and potential criminal charges. |

| Record Keeping | Businesses must keep copies of Form 8300 for at least five years for IRS review. |

| State-Specific Forms | Some states have their own reporting requirements, which may vary by state law. |

| Privacy Protection | Form 8300 includes a section to protect the privacy of individuals who make cash payments. |

| Who Must File | Any business that receives cash payments over $10,000 must file this form, regardless of the business type. |

| IRS Processing | The IRS uses the information from Form 8300 to combat money laundering and tax evasion. |

| Additional Reporting | In certain situations, businesses may need to report cash transactions on additional forms, depending on the nature of the transaction. |

The IRS Form 8300 must be completed accurately to report cash transactions exceeding $10,000. This form is crucial for compliance with federal regulations regarding large cash payments. Following the steps below will help ensure that the form is filled out correctly.

After filling out the form, it is important to keep a copy for your records. Ensure that you file the form on time to avoid potential penalties.

What is the IRS 8300 form?

The IRS 8300 form is a document used by businesses to report cash payments exceeding $10,000 received in a single transaction or related transactions. This form helps the Internal Revenue Service track large cash transactions, which may be indicative of money laundering or tax evasion activities.

Who is required to file the IRS 8300 form?

Any business or individual who receives more than $10,000 in cash in a single transaction or related transactions must file the IRS 8300 form. This requirement applies to a wide range of industries, including retail, real estate, and automotive sales. It is crucial for businesses to understand their obligations to avoid potential penalties.

What constitutes a cash payment for the IRS 8300 form?

Cash payments include physical currency, such as coins and paper money. Additionally, certain monetary instruments, like cashier's checks, bank drafts, and money orders, may also qualify as cash if they are used to pay for goods or services. However, personal checks and credit card payments do not count as cash for this purpose.

What is the deadline for filing the IRS 8300 form?

The IRS 8300 form must be filed within 15 days after the date the cash payment is received. This timeline is critical to ensure compliance with IRS regulations. Failure to file on time can result in penalties, so businesses should establish processes to track cash transactions effectively.

What information is required on the IRS 8300 form?

The form requires detailed information about the transaction, including the name and address of the person or business making the cash payment, the amount of cash received, and the date of the transaction. Additionally, the form may require information about the nature of the business and the purpose of the transaction.

Are there penalties for failing to file the IRS 8300 form?

Yes, there are penalties for failing to file the IRS 8300 form or for filing it incorrectly. The penalties can vary based on the severity of the violation, ranging from fines for late filings to more significant penalties for willful neglect or fraudulent activities. Businesses should take these obligations seriously to avoid financial repercussions.

Can a business file the IRS 8300 form electronically?

Yes, businesses can file the IRS 8300 form electronically using the IRS's e-file system. Electronic filing can streamline the process and help ensure that the form is submitted correctly and on time. Businesses should check the IRS website for specific instructions and requirements for electronic filing.

Where should a business send the IRS 8300 form?

The completed IRS 8300 form can be submitted to the IRS either by mail or electronically. If filing by mail, the form should be sent to the address specified in the form's instructions. Businesses should ensure they keep a copy of the submitted form for their records.

Incorrect Identification Information: Many individuals provide inaccurate names, addresses, or identification numbers. It's crucial to ensure that all personal details match official documents.

Missing Required Information: Some people overlook sections that must be filled out completely. Each part of the form is essential for accurate processing.

Failure to Report All Transactions: Individuals sometimes forget to report multiple cash transactions. The IRS requires reporting for any cash payments over $10,000.

Inaccurate Transaction Amounts: Errors can occur when entering the amount of cash received. Double-checking these figures helps avoid complications.

Not Signing the Form: Some filers neglect to sign the form. A signature is necessary for the submission to be valid.

Missing the Filing Deadline: Failing to submit the form on time can lead to penalties. Marking the deadline on your calendar can help ensure timely filing.

The IRS Form 8300 is an important document used to report cash payments over $10,000 received in a trade or business. However, there are other forms and documents that often accompany it to ensure compliance with federal regulations. Here are four common forms and documents that may be used alongside the IRS 8300.

Understanding these accompanying forms and documents can help ensure that you remain compliant with IRS regulations when dealing with large cash transactions. Keeping thorough records and filing the appropriate forms is essential for any business handling significant cash payments.

The IRS Form 1099 is a document used to report various types of income other than wages, salaries, and tips. Similar to Form 8300, which reports cash transactions over $10,000, Form 1099 is essential for tracking income that might not be captured through traditional employment. Businesses and individuals must file this form to ensure that all income is reported to the IRS, promoting transparency and compliance with tax regulations.

Form 1040 is the standard individual income tax return form used by U.S. taxpayers. While Form 8300 focuses on large cash transactions, Form 1040 encompasses all income earned within a tax year, including wages, dividends, and capital gains. Both forms serve the IRS's goal of accurately reporting income, but they target different aspects of a taxpayer’s financial activities.

Form W-2 is used by employers to report wages paid to employees and the taxes withheld from those wages. Like Form 8300, it ensures that the IRS receives accurate information about income. However, while Form 8300 deals with cash transactions, Form W-2 is specific to employee compensation, illustrating the relationship between employers and employees in the tax system.

Form 941 is the employer's quarterly federal tax return. It reports income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Similar to Form 8300, it plays a crucial role in ensuring compliance with federal tax obligations. Both forms require accurate reporting to avoid penalties, though Form 941 is more focused on payroll taxes rather than cash transactions.

Form 1065 is used by partnerships to report income, deductions, gains, and losses from the operation of a partnership. Like Form 8300, it is essential for transparency in financial reporting to the IRS. Both forms contribute to the accurate assessment of tax liabilities, but Form 1065 provides a broader view of a partnership's financial activities rather than focusing solely on cash transactions.

Form 990 is an annual reporting return that tax-exempt organizations must file with the IRS. Similar to Form 8300, it provides a comprehensive overview of an organization’s financial activities. Both forms aim to ensure that the IRS has a clear understanding of financial transactions, although Form 990 is specifically tailored for non-profit organizations and their financial disclosures.

Form 5500 is used to report information about employee benefit plans. It shares a similar purpose with Form 8300 in that both forms require accurate reporting to maintain compliance with federal regulations. While Form 8300 focuses on cash transactions, Form 5500 is dedicated to the reporting of benefits and financial conditions of employee benefit plans.

Form 8862 is used by taxpayers who have previously had their Earned Income Tax Credit (EITC) denied. This form serves to re-establish eligibility for the credit. While it may seem different from Form 8300, both forms are part of the IRS's efforts to ensure accurate reporting and compliance. Each form addresses specific tax issues, contributing to a fair tax system.

When filling out the IRS 8300 form, it is essential to ensure that you complete it accurately and thoroughly. Here are some important dos and don’ts to keep in mind:

By following these guidelines, you can help ensure that your IRS 8300 form is filled out correctly, minimizing the risk of complications. Remember, accuracy and attention to detail are key in this process.

The IRS Form 8300 is an important document for reporting cash payments over $10,000. However, several misconceptions surround its use. Here are nine common misunderstandings:

Understanding these misconceptions can help ensure compliance with IRS regulations and avoid potential penalties.

When dealing with large cash transactions, understanding the IRS 8300 form is essential. Here are some key takeaways to keep in mind:

Being aware of these points can help ensure compliance and avoid any potential issues with the IRS.