The IRS Form 720 plays a crucial role in the landscape of federal taxation in the United States, primarily serving as a means for certain taxpayers to report and pay federal excise taxes. This form is essential for a range of businesses and individuals engaged in activities subject to these specific taxes, including but not limited to environmental taxes, communications taxes, and the tax on the sale of certain goods and services. Understanding the various sections of Form 720 can feel daunting, as it requires meticulous attention to detail. Taxpayers must accurately disclose their tax liability within specific categories, ensuring compliance with federal regulations. Moreover, the deadlines for filing this form are important to adhere to, as late submissions may lead to penalties. Different periods of reporting may apply, likening this form to both a quarterly and an annual obligation, depending on the circumstances. Knowing when and how to file can alleviate concerns and prevent complications with the IRS. For those who navigate this process, assistance from a knowledgeable professional may be helpful in demystifying the steps involved. By approaching the Form 720 with careful consideration and preparation, individuals and businesses can fulfill their tax obligations effectively while contributing to broader fiscal responsibilities.

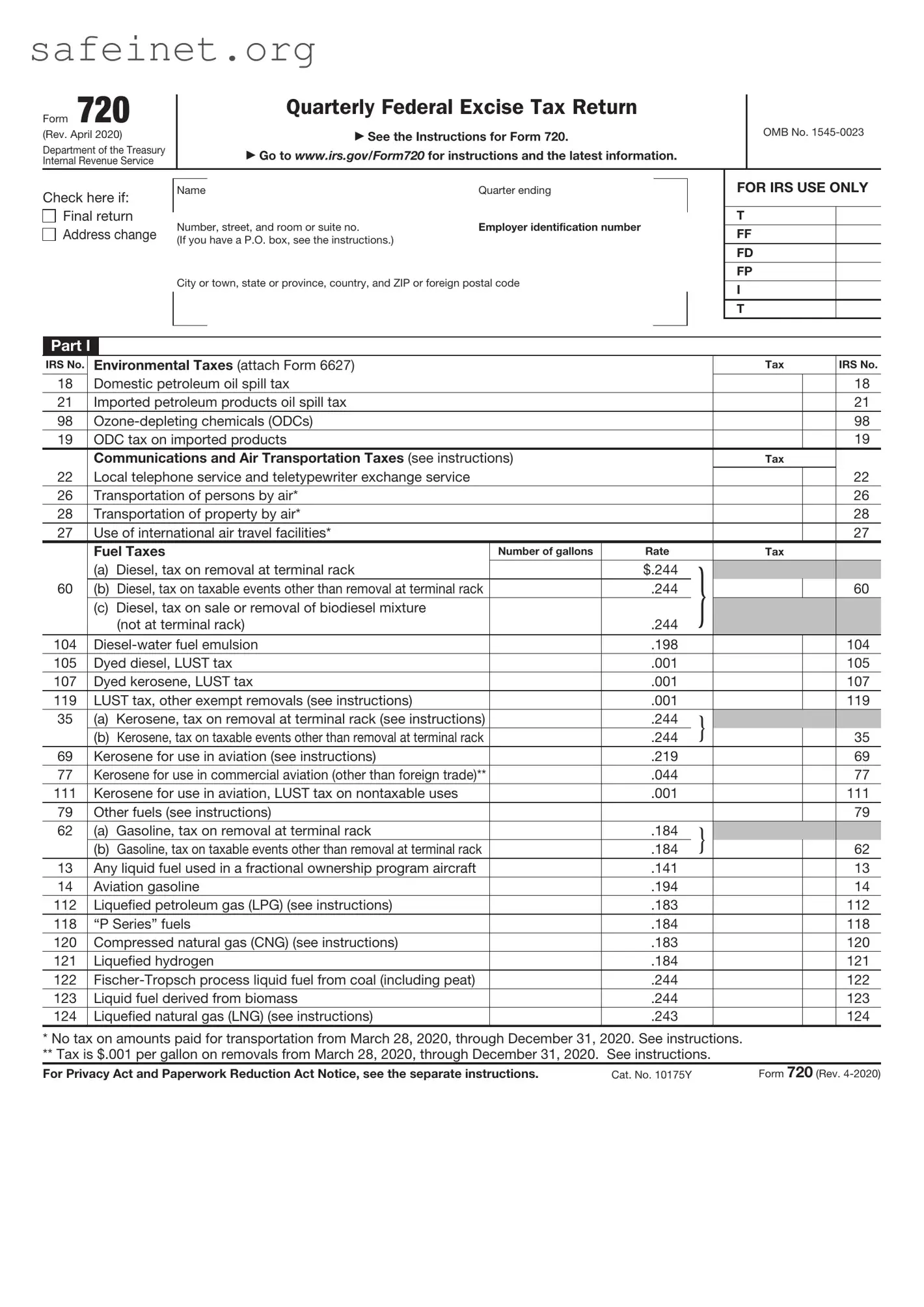

Form 720

(Rev. April 2020)

Department of the Treasury

Internal Revenue Service

Quarterly Federal Excise Tax Return

See the Instructions for Form 720.

Go to www.irs.gov/Form720 for instructions and the latest information.

OMB No.

Check here if:

Final return

Final return

Address change

Name |

Quarter ending |

Number, street, and room or suite no. |

Employer identification number |

(If you have a P.O. box, see the instructions.) |

|

City or town, state or province, country, and ZIP or foreign postal code

FOR IRS USE ONLY

T

FF

FD

FP

I

T

Part I

IRS No. |

Environmental Taxes (attach Form 6627) |

|

|

|

Tax |

|

IRS No. |

|

18 |

|

Domestic petroleum oil spill tax |

|

|

|

|

|

18 |

21 |

|

Imported petroleum products oil spill tax |

|

|

|

|

|

21 |

98 |

|

|

|

|

|

|

98 |

|

19 |

|

ODC tax on imported products |

|

|

|

|

|

19 |

|

|

Communications and Air Transportation Taxes (see instructions) |

|

|

Tax |

|

|

|

22 |

|

Local telephone service and teletypewriter exchange service |

|

|

|

|

|

22 |

26 |

|

Transportation of persons by air* |

|

|

|

|

|

26 |

28 |

|

Transportation of property by air* |

|

|

|

|

|

28 |

27 |

|

Use of international air travel facilities* |

|

|

|

|

|

27 |

|

|

Fuel Taxes |

Number of gallons |

Rate |

|

Tax |

|

|

|

|

(a) Diesel, tax on removal at terminal rack |

|

$.244 |

} |

|

|

|

60 |

|

(b) Diesel, tax on taxable events other than removal at terminal rack |

|

.244 |

|

|

60 |

|

|

|

(c) Diesel, tax on sale or removal of biodiesel mixture |

|

|

|

|

|

|

|

|

(not at terminal rack) |

|

.244 |

|

|

|

|

104 |

|

|

.198 |

|

|

|

104 |

|

105 |

|

Dyed diesel, LUST tax |

|

.001 |

|

|

|

105 |

107 |

|

Dyed kerosene, LUST tax |

|

.001 |

|

|

|

107 |

119 |

|

LUST tax, other exempt removals (see instructions) |

|

.001 |

|

|

|

119 |

35 |

|

(a) Kerosene, tax on removal at terminal rack (see instructions) |

|

.244 |

} |

|

|

|

|

|

(b) Kerosene, tax on taxable events other than removal at terminal rack |

|

.244 |

|

|

35 |

|

69 |

|

Kerosene for use in aviation (see instructions) |

|

.219 |

|

|

|

69 |

77 |

|

Kerosene for use in commercial aviation (other than foreign trade)** |

|

.044 |

|

|

|

77 |

111 |

|

Kerosene for use in aviation, LUST tax on nontaxable uses |

|

.001 |

|

|

|

111 |

79 |

|

Other fuels (see instructions) |

|

|

|

|

|

79 |

62 |

|

(a) Gasoline, tax on removal at terminal rack |

|

.184 |

} |

|

|

|

|

|

(b) Gasoline, tax on taxable events other than removal at terminal rack |

|

.184 |

|

|

62 |

|

13 |

|

Any liquid fuel used in a fractional ownership program aircraft |

|

.141 |

|

|

|

13 |

14 |

|

Aviation gasoline |

|

.194 |

|

|

|

14 |

112 |

|

Liquefied petroleum gas (LPG) (see instructions) |

|

.183 |

|

|

|

112 |

118 |

|

“P Series” fuels |

|

.184 |

|

|

|

118 |

120 |

|

Compressed natural gas (CNG) (see instructions) |

|

.183 |

|

|

|

120 |

121 |

|

Liquefied hydrogen |

|

.184 |

|

|

|

121 |

122 |

|

|

.244 |

|

|

|

122 |

|

123 |

|

Liquid fuel derived from biomass |

|

.244 |

|

|

|

123 |

124 |

|

Liquefied natural gas (LNG) (see instructions) |

|

.243 |

|

|

|

124 |

* No tax on amounts paid for transportation from March 28, 2020, through December 31, 2020. See instructions. ** Tax is $.001 per gallon on removals from March 28, 2020, through December 31, 2020. See instructions.

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 10175Y |

Form 720 (Rev. |

Form 720 (Rev. |

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 2 |

||

IRS No. |

|

|

|

|

|

|

|

|

|

Rate |

|

|

Tax |

IRS No. |

||

|

Retail |

|

|

|

|

|

|

|

||||||||

33 |

12% of sales price |

|

|

|

33 |

|||||||||||

|

Ship Passenger Tax |

|

|

|

Number of persons |

|

Rate |

|

|

Tax |

|

|||||

29 |

Transportation by water |

|

|

|

|

|

|

$3 per person |

|

|

|

29 |

||||

|

Other Excise Tax |

|

|

|

Amount of obligations |

|

Rate |

|

|

Tax |

|

|||||

31 |

Obligations not in registered form |

|

|

|

|

|

|

$.01 |

|

|

|

|

|

31 |

||

|

Foreign Insurance |

Premiums paid |

|

Rate |

|

|

Tax |

IRS No. |

||||||||

|

|

Casualty insurance and indemnity bonds |

|

|

|

|

|

|

$.04 |

|

} |

|

|

|

|

|

30 |

|

Life insurance, sickness and accident policies, and annuity |

|

|

|

|

|

|

|

|

|

|

||||

|

|

contracts |

|

|

|

|

|

|

.01 |

|

|

|

|

30 |

||

|

|

Reinsurance |

|

|

|

|

|

|

.01 |

|

|

|

|

|

||

|

Manufacturers Taxes |

Number of tons |

Sales price |

|

|

|

|

|

|

|

|

|||||

36 |

|

|

|

|

|

|

$1.10 per ton |

|

|

|

|

36 |

||||

37 |

|

|

|

|

|

|

4.4% of sales price |

|

|

|

37 |

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||

38 |

|

|

|

|

|

|

|

$.55 per ton |

|

|

|

|

38 |

|||

39 |

|

|

|

|

|

|

4.4% of sales price |

|

|

|

39 |

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

Number of tires |

|

Tax |

IRS No. |

||||

108 |

Taxable tires other than bias ply or super single tires |

|

|

|

|

|

|

|

|

|

|

|

|

108 |

||

109 |

Taxable bias ply or super single tires (other than super single tires designed for steering) |

|

|

|

|

|

|

|

109 |

|||||||

113 |

Taxable tires, super single tires designed for steering |

|

|

|

|

|

|

|

|

|

|

|

|

113 |

||

40 |

Gas guzzler tax. Attach Form 6197. Check if |

. . . . . |

|

|

|

|

|

40 |

||||||||

97 |

Vaccines (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

97 |

|

|

|

|

|

|

|

Sales price |

|

|

|

|

|

|

|

|

||

|

Reserved for future use |

|

|

|

|

|

|

2.3% of sales price |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Total. Add all amounts in Part I. Complete Schedule A unless |

|

|

|

|

$ |

|

|

|

|||||||

Part II |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Avg. number |

(b) Rate for |

|

(c) Fee (see |

|

|

|

|

||||||||

IRS No. |

instructions) |

|

of lives covered |

avg. |

|

|

|

|

|

|||||||

|

(see inst.) |

covered life |

|

instructions) |

|

Tax |

IRS No. |

|||||||||

|

Specified health insurance policies |

|

|

|

|

|

|

|

|

|

|

} |

|

|

|

|

|

(a) With a policy year ending before October 1, 2019 |

|

|

|

$2.45 |

|

|

|

|

|

|

|

||||

|

(b) With a policy year ending on or after October 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

2019, and before October 1, 2020 |

|

|

|

|

$2.54 |

|

|

|

|

|

|

|

|||

133 |

Applicable |

|

|

|

|

|

|

|

|

|

|

|

|

133 |

||

|

(c) With a plan year ending before October 1, 2019 |

|

|

|

$2.45 |

|

|

|

|

|

|

|

||||

|

(d) With a plan year ending on or after October 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

2019, and before October 1, 2020 |

|

|

|

|

$2.54 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Rate |

|

|

Tax |

|

||

41 |

Sport fishing equipment (other than fishing rods and fishing poles) |

|

|

10% of sales price |

|

|

|

41 |

||||||||

110 |

Fishing rods and fishing poles (limits apply, see instructions) |

|

|

|

10% of sales price |

|

|

|

110 |

|||||||

42 |

Electric outboard motors |

|

|

|

|

|

|

3% of sales price |

|

|

|

42 |

||||

114 |

Fishing tackle boxes |

|

|

|

|

|

|

3% of sales price |

|

|

|

114 |

||||

44 |

Bows, quivers, broadheads, and points |

|

|

|

|

|

|

11% of sales price |

|

|

|

44 |

||||

106 |

Arrow shafts |

|

|

|

|

|

|

$.52 per shaft |

|

|

|

106 |

||||

140 |

Indoor tanning services |

|

|

|

|

|

|

10% of amount paid |

|

|

|

140 |

||||

|

|

|

|

|

|

Number of gallons |

|

Rate |

|

|

Tax |

|

||||

64 |

Inland waterways fuel use tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$.29 |

|

|

|

|

|

64 |

||||

125 |

LUST tax on inland waterways fuel use (see instructions) |

|

|

|

.001 |

|

|

|

|

|

125 |

|||||

51 |

Section 40 fuels (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

51 |

|

117 |

Biodiesel sold as but not used as fuel |

|

|

|

|

|

|

|

|

|

|

|

|

|

117 |

|

20 |

Floor Stocks |

|

|

|

|

|

|

|

20 |

|||||||

2 |

Total. Add all amounts in Part II |

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

Form 720 (Rev.

Form 720 (Rev. |

Page 3 |

|

Part III |

|

|

3 |

Total tax. Add Part I, line 1, and Part II, line 2 |

|

|||||||

4 |

Claims (see instructions; complete Schedule C) |

. . . . . . . |

|

4 |

|

|

|||

5 |

Deposits made for the quarter . . . . |

|

5 |

|

|

|

|

|

|

|

Check here if you used the safe harbor rule to make your deposits. |

|

|

|

|

||||

6 |

Overpayment from previous quarters . . |

6 |

|

|

|

|

|

|

|

7Enter the amount from Form

|

on line 6, if any |

|

7 |

|

|

|

|

8 |

Add lines 5 and 6 |

. . . . . . . . . |

8 |

|

|

||

9 |

Add lines 4 and 8 |

|

|||||

10Balance Due. If line 3 is greater than line 9, enter the difference. Pay the full amount with the return (see instructions)

11Overpayment. If line 9 is greater than line 3, enter the difference. Check if you want the

overpayment: |

Applied to your next return, or |

Refunded to you. |

3

9

10

11

Third Party Designee

Sign

Here

Paid

Preparer

Use Only

Do you want to allow another person to discuss this return with the IRS (see instructions)? |

Yes. Complete the following. |

No |

|||||

Designee name |

Phone no. |

Personal identification number (PIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

F |

|

|

|

|

F |

|

|

|

|

|

Signature |

|

Date |

|

Title |

|

|

||||

|

|

|

|

|

|

|||||

|

Type or print name below signature. |

|

|

|

Telephone number |

|

|

|||

Print/Type preparer’s name |

Preparer’s signature |

Date |

|

|

Check |

if |

PTIN |

|||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

|

Firm’s EIN |

|

|

||

Firm’s address |

|

|

|

|

|

Phone no. |

|

|

||

Form 720 (Rev.

Form 720 (Rev. |

Page 4 |

Schedule A Excise Tax Liability (see instructions)

Note: You must complete Schedule A if you have a liability for any tax in Part I of Form 720. Don’t complete Schedule A for Part II taxes or for a

1Regular method taxes

(a) Record of Net |

|

|

Period |

|

|||

Tax Liability |

|

|

|

|

|||

First month |

A |

|

|

B |

|

|

|

Second month |

C |

|

|

D |

|

|

|

Third month |

E |

|

|

F |

|

|

|

Special rule for September |

* |

. . . . . . . . . |

|

G |

|

|

|

(b)Net liability for regular method taxes. Add the amounts for each semimonthly period.

2Alternative method taxes (IRS Nos. 22, 26, 28, and 27)

(a) Record of Taxes |

|

|

Period |

|

|||

Considered as |

|

|

|

|

|||

Collected |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First month |

M |

|

|

N |

|

|

|

Second month |

O |

|

|

P |

|

|

|

Third month |

Q |

|

|

R |

|

|

|

Special rule for September |

* |

. . . . . . . . . |

|

S |

|

|

|

(b)Alternative method taxes. Add the amounts for each semimonthly period.

* Complete only as instructed (see instructions).

Schedule T

Fuel |

Number of gallons |

Diesel fuel, gallons received in a |

|

on Form 720, IRS No. 60(a) |

|

Diesel fuel, gallons delivered in a |

|

|

|

Kerosene, gallons received in a |

|

on Form 720, IRS No. 35(a), 69, 77, or 111 |

|

Kerosene, gallons delivered in a |

|

|

|

Gasoline, gallons received in a |

|

on Form 720, IRS No. 62(a) |

|

Gasoline, gallons delivered in a |

|

|

|

Aviation gasoline, gallons received in a |

|

on Form 720, IRS No. 14 |

|

Aviation gasoline, gallons delivered in a |

|

|

|

|

Form 720 (Rev. |

Form 720 (Rev. |

|

Page 5 |

Schedule C |

Claims |

Month your income tax year ends |

•Complete Schedule C for claims only if you are reporting liability in Part I or II of Form 720.

•See instructions for kerosene used in commercial aviation from March 28, 2020, through December 31, 2020.

•Attach a statement explaining each claim as required. Include your name and EIN on the statement (see instructions).

Caution: Claimant has the name and address of the person(s) who sold the fuel to the claimant, the dates of purchase, and if exported, the required proof of export. For claims on lines 1a and 2b (type of use 13 and 14), 3c, 4b, and 5, claimant hasn’t waived the right to make the claim.

1 |

Nontaxable Use of Gasoline |

Note: CRN is credit reference number. |

Period of claim |

|

|

|

||

|

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a Gasoline (see Caution above line 1) |

|

$.183 |

|

$ |

|

362 |

||

|

|

|

|

|

|

|

|

|

b Exported (see Caution above line 1) |

|

.184 |

|

|

|

411 |

||

2 |

Nontaxable Use of Aviation Gasoline |

Period of claim |

|

|

|

|||

|

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a Used in commercial aviation (other than foreign trade) |

|

$.15 |

|

$ |

|

354 |

||

|

|

|

|

|

|

|

|

|

b Other nontaxable use (see Caution above line 1) |

|

.193 |

|

|

|

324 |

||

|

|

|

|

|

|

|

|

|

c Exported (see Caution above line 1) |

|

.194 |

|

|

|

412 |

||

|

|

|

|

|

|

|

|

|

d LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

||

3 |

Nontaxable Use of Undyed Diesel Fuel |

Period of claim |

|

|

|

|||

Claimant certifies that the diesel fuel did not contain visible evidence of dye.

Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach a detailed explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

Type of use |

Rate |

Gallons |

|

Amount of claim |

CRN |

|

a |

Nontaxable use |

|

$.243 |

|

$ |

|

|

360 |

b |

Use in trains |

|

.243 |

|

|

|

|

353 |

c Use in certain intercity and local buses (see Caution above line 1) |

|

.17 |

|

|

|

|

350 |

|

|

|

|

|

|

|

|

|

|

d Use on a farm for farming purposes |

|

.243 |

|

|

|

|

360 |

|

|

|

|

|

|

|

|

|

|

e Exported (see Caution above line 1) |

|

.244 |

|

|

|

|

413 |

|

4Nontaxable Use of Undyed Kerosene (Other Than Kerosene Used in Aviation) Period of claim

Claimant certifies that the kerosene did not contain visible evidence of dye.

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach a detailed explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

Caution: Claims cannot be made on line 4 for kerosene sales from a blocked pump. |

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Nontaxable use |

|

$.243 |

|

$ |

|

346 |

b |

Use in certain intercity and local buses (see Caution above line 1) |

|

.17 |

|

|

|

347 |

c |

Use on a farm for farming purposes |

|

.243 |

|

|

|

346 |

d |

Exported (see Caution above line 1) |

|

.244 |

|

|

|

414 |

e |

Nontaxable use taxed at $.044 |

|

.043 |

|

|

|

377 |

f |

Nontaxable use taxed at $.219 |

|

.218 |

|

|

|

369 |

5 Kerosene Used in Aviation (see Caution above line 1) |

Period of claim |

|

|

|

|||

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Kerosene used in commercial aviation (other than foreign |

|

|

|

|

|

|

|

trade) taxed at $.244 |

|

$.200 |

|

$ |

|

417 |

b |

Kerosene used in commercial aviation (other than foreign |

|

|

|

|

|

|

|

trade) taxed at $.219 |

|

.175 |

|

|

|

355 |

c |

Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

government) taxed at $.244 |

|

.243 |

|

|

|

346 |

d |

Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

government) taxed at $.219 |

|

.218 |

|

|

|

369 |

e |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

Form 720 (Rev.

Form 720 (Rev. |

Page 6 |

6Nontaxable Use of Alternative Fuel

Caution: There is a reduced credit rate for use in certain intercity and local buses (type of use 5) (see instructions).

|

|

Type of use |

Rate |

Gallons, or gasoline |

Amount of claim |

CRN |

|

|

|

or diesel gallon |

|||||

|

|

|

|

equivalents |

|

|

|

a |

Liquefied petroleum gas (LPG) (see instructions) |

|

$.183 |

|

$ |

|

419 |

b |

“P Series” fuels |

|

.183 |

|

|

|

420 |

c |

Compressed natural gas (CNG) (see instructions) |

|

.183 |

|

|

|

421 |

d |

Liquefied hydrogen |

|

.183 |

|

|

|

422 |

e |

|

.243 |

|

|

|

423 |

|

f |

Liquid fuel derived from biomass |

|

.243 |

|

|

|

424 |

g |

Liquefied natural gas (LNG) (see instructions) |

|

.243 |

|

|

|

425 |

h |

Liquefied gas derived from biomass |

|

.183 |

|

|

|

435 |

7 Sales by Registered Ultimate Vendors of Undyed Diesel Fuel |

|

Period of claim |

|

|

|

||

|

|

|

Registration number |

|

|

|

|

Claimant certifies that it sold the diesel fuel at a

|

|

Rate |

Gallons |

|

Amount of claim |

CRN |

|

a Use by a state or local government |

$.243 |

|

$ |

|

|

360 |

|

|

|

|

|

|

|

|

|

b Use in certain intercity and local buses |

.17 |

|

|

|

|

350 |

|

8 Sales by Registered Ultimate Vendors of Undyed Kerosene |

|

Period of claim |

|

|

|

|

|

|

(Other Than Kerosene For Use in Aviation) |

Registration number |

|

|

|

|

|

Claimant certifies that it sold the kerosene at a

explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

Rate |

Gallons |

Amount of claim |

CRN |

|

a Use by a state or local government |

$.243 |

|

$ |

|

346 |

|

|

|

|

|

|

|

|

b Sales from a blocked pump |

.243 |

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

|

|

c Use in certain intercity and local buses |

.17 |

|

|

|

347 |

|

9 Sales by Registered Ultimate Vendors of Kerosene For Use in Aviation |

Registration number |

|

|

|

||

•See Caution above line 1.

•Claimant sold the kerosene for use in aviation at a

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Use in commercial aviation (other than foreign trade) taxed at $.219 |

|

$.175 |

|

$ |

|

355 |

b |

Use in commercial aviation (other than foreign trade) taxed at $.244 |

|

.200 |

|

|

|

417 |

c |

Nonexempt use in noncommercial aviation |

|

.025 |

|

|

|

418 |

d |

Other nontaxable uses taxed at $.244 |

|

.243 |

|

|

|

346 |

e |

Other nontaxable uses taxed at $.219 |

|

.218 |

|

|

|

369 |

f |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

10 Sales by Registered Ultimate Vendors of Gasoline |

Registration number |

|

|

|

|||

Claimant sold the gasoline at a

|

|

Rate |

Gallons |

Amount of claim |

CRN |

|

a Use by a nonprofit educational organization |

$.183 |

|

$ |

|

362 |

|

|

|

|

|

|

|

|

b Use by a state or local government |

.183 |

|

|

|

||

|

|

|

|

|||

Form 720 (Rev.

Form 720 (Rev. |

|

|

|

|

|

|

|

Page 7 |

|

11 Sales by Registered Ultimate Vendors of Aviation Gasoline |

Registration number |

|

|

|

|

||||

|

Claimant sold the aviation gasoline at a |

||||||||

|

of tax to the buyer, or has obtained written consent of the buyer to take the claim; and obtained an unexpired certificate from the buyer |

||||||||

|

and has no reason to believe any information in the certificate is false. See the instructions for additional information to be submitted. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

Rate |

|

Gallons |

|

Amount of claim |

|

CRN |

|

a Use by a nonprofit educational organization |

$.193 |

|

|

$ |

|

|

|

324 |

|

|

|

|

|

|

|

|

|

|

|

b Use by a state or local government |

.193 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

12 |

Biodiesel or Renewable Diesel Mixture Credit Period of claim |

|

|

Registration number |

|

||||

|

Biodiesel mixtures. Claimant produced a mixture by mixing biodiesel with diesel fuel. The biodiesel used to produce the |

||||||||

|

mixture met ASTM D6751 and met EPA’s registration requirements for fuels and fuel additives. The mixture was sold by the |

||||||||

|

claimant to any person for use as a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for |

|

|||||||

|

Biodiesel and, if applicable, the Statement of Biodiesel Reseller. Renewable diesel mixtures. Claimant produced a mixture by |

||||||||

|

mixing renewable diesel with liquid fuel (other than renewable diesel). The renewable diesel used to produce the renewable |

||||||||

|

diesel mixture was derived from biomass, met EPA’s registration requirements for fuels and fuel additives, and met ASTM |

||||||||

|

D975, D396, or other equivalent standard approved by the IRS. The mixture was sold by the claimant to any person for use as |

||||||||

|

a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable, Statement of |

||||||||

|

Biodiesel Reseller, both of which have been edited as discussed in the instructions for line 12. See the instructions for line 12 |

||||||||

|

for information about renewable diesel used in aviation. |

|

|

|

|

|

|

|

|

|

|

Rate |

Gal. of biodiesel or |

|

Amount of claim |

|

CRN |

||

|

|

|

renewable diesel |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a Biodiesel (other than |

$1.00 |

|

|

$ |

|

|

|

388 |

|

b |

1.00 |

|

|

|

|

|

|

390 |

|

c |

Renewable diesel mixtures |

1.00 |

|

|

|

|

|

|

307 |

13 Alternative Fuel Credit and Alternative Fuel Mixture Credit |

|

Registration number |

|

||||||

For the alternative fuel mixture credit, claimant produced a mixture by mixing taxable fuel with alternative fuel. Claimant certifies that it (a) produced the alternative fuel, or (b) has in its possession the name, address, and EIN of the person(s) that sold the alternative fuel to the claimant; the date of purchase; and an invoice or other documentation identifying the amount of the alternative fuel. The claimant also certifies that it made no other claim for the amount of the alternative fuel, or has repaid the amount to the government. The alternative fuel mixture was sold by the claimant to any person for use as a fuel or was used as a fuel by the claimant.

|

|

|

Gallons, or |

|

|

|

|

|

|

Rate |

gasoline or diesel |

Amount of claim |

CRN |

||

|

|

|

gallon equivalents |

|

|

|

|

|

|

|

(see instructions) |

|

|

|

|

a |

Liquefied petroleum gas (LPG)* |

$.50 |

|

|

$ |

|

426 |

b |

“P Series” fuels |

.50 |

|

|

|

|

427 |

c |

Compressed natural gas (CNG)* |

.50 |

|

|

|

|

428 |

d |

Liquefied hydrogen |

.50 |

|

|

|

|

429 |

e |

.50 |

|

|

|

|

430 |

|

f |

Liquid fuel derived from biomass |

.50 |

|

|

|

|

431 |

g |

Liquefied natural gas (LNG)* |

.50 |

|

|

|

|

432 |

h |

Liquefied gas derived from biomass* |

.50 |

|

|

|

|

436 |

i |

Compressed gas derived from biomass* |

.50 |

|

|

|

|

437 |

|

* You can’t claim the alternative fuel mixture credit for this fuel. |

|

|

|

|

|

|

|

|

|

|

|

|||

14 |

Other claims. See the instructions. For lines 14b and 14c, see the Caution above line 1 on page 5. |

Amount of claim |

CRN |

||||

a |

Section 4051(d) tire credit (tax on vehicle reported on IRS No. 33) |

|

|

|

$ |

|

366 |

b |

Exported dyed diesel fuel and exported gasoline blendstocks taxed at $.001 |

|

|

|

|

415 |

|

c |

Exported dyed kerosene |

|

|

|

|

|

416 |

d |

|

|

|

|

|

|

|

e |

Registered credit card issuers |

|

|

|

|

|

|

|

|

|

Number of tires |

Amount of claim |

CRN |

||

f |

Taxable tires other than bias ply or super single tires |

|

|

|

$ |

|

396 |

g |

Taxable tires, bias ply or super single tires (other than super single tires designed for steering) |

|

|

|

|

304 |

|

h |

Taxable tires, super single tires designed for steering |

|

|

|

|

|

305 |

i |

|

|

|

|

|

|

|

j |

|

|

|

|

|

|

|

k |

|

|

|

|

|

|

|

15 |

Total claims. Add amounts on lines 1 through 14. Enter the result here and on Form 720, Part III, line 4. |

15 |

|

|

|

||

Form 720 (Rev.

Form

Purpose of Form

Complete Form

If you have your return prepared by a third party and a payment is required, provide this payment voucher to the return preparer.

Don’t file Form

Specific Instructions

Box 1. If you don’t have an EIN, you may apply for one online by visiting www.irs.gov/EIN. You may also apply for an EIN by faxing or mailing Form

Box 2. Enter the amount paid from line 10 of Form 720.

Box 3. Darken the circle identifying the quarter for which the payment is made. Darken only one circle.

Box 4. Enter your name and address as shown on Form 720.

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your

EIN (SSN for

•Detach the completed voucher and send it with your payment and Form 720. See Where To File in the Instructions for Form 720.

Form

Detach here and mail with your payment and Form 720.

Form

Department of the Treasury

Internal Revenue Service

1Enter your employer identification

number (EIN). See instructions.

|

Payment Voucher |

OMB No. |

|

|

|

|

|

|

Don’t staple or attach this voucher to your payment. |

2020 |

|

|

||

|

|

|

2 |

Dollars |

Cents |

Enter the amount of your payment.

Make your check or money order payable to “United States Treasury.”

3Tax Period

1st |

3rd |

Quarter |

Quarter |

2nd |

4th |

Quarter |

Quarter |

4Enter your business name (individual name if sole proprietor).

Enter your address.

City or town, state or province, country, and ZIP or foreign postal code

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 720 is used to report and pay federal excise taxes. This form is typically filed quarterly and covers various types of transactions, including sales of certain goods and services. |

| Filing Frequency | Form 720 must be submitted on a quarterly basis. The due dates for filing are April 30, July 31, October 31, and January 31 of the following year. |

| Who Should File? | Businesses that produce or sell goods subject to excise tax, such as fuel producers, manufacturers of certain goods, and businesses involved in specific services, should complete and file this form. |

| State-Specific Forms | While the IRS Form 720 is a federal form, individual states may have their own excise tax forms. The governing laws vary by state, including for example: California's Revenue and Taxation Code Section 38001 for state-specific excise taxes. |

Filling out IRS Form 720 requires attention to detail and organization. Following these steps can help you complete the form accurately.

After submitting the form, keep a copy for your records. You may also want to monitor any correspondence from the IRS pertaining to your submission.

What is the IRS Form 720?

The IRS Form 720 is a tax form used to report and pay federal excise taxes. This includes taxes on specific goods, services, and activities. Businesses or individuals who engage in these activities may be required to use this form to report any applicable excise taxes owed to the IRS.

Who needs to file Form 720?

Any business or individual that owes federal excise taxes must file Form 720. This could include manufacturers, importers, and distributors of certain goods, as well as service providers in areas such as communications or environmental impact. If you're unsure, it’s wise to consult a tax professional.

When is Form 720 due?

Form 720 is typically due quarterly. The deadlines for each quarter are as follows: April 30 for the first quarter, July 31 for the second, October 31 for the third, and January 31 of the following year for the fourth. Timely filing helps avoid penalties and interest.

What types of taxes are reported on Form 720?

Form 720 covers a variety of excise taxes. These include fuel taxes, taxes on air transportation, and environmental taxes, among others. It's essential to review which specific taxes your business is liable for and report them accordingly.

How do I complete Form 720?

Start by gathering the necessary information about your business and the applicable excise taxes. Next, fill out the form, providing all required details and calculations. Make sure to check for accuracy before submission. Detailed instructions are available on the IRS website to assist you.

Can I file Form 720 electronically?

Yes, you can file Form 720 electronically through the IRS e-file system. Electronic filing can be more efficient and offers the benefit of quicker processing and confirmation of receipt. Many tax software programs simplify this process for you.

What if I don’t file Form 720 on time?

If you miss the deadline, you may face penalties and interest on any unpaid taxes. The IRS typically calculates the penalty based on the amount owed and the duration of the delay. It's important to file as soon as possible to minimize these consequences.

Can I correct a mistake on Form 720 after filing?

Absolutely. If you realize that you’ve made a mistake after submitting Form 720, you can file an amended return. Use the IRS Form 720-X to correct any errors. Be sure to include detailed information about what needs to be changed to avoid issues.

Where do I send my completed Form 720?

Where you send your completed Form 720 depends on your location and whether you're including a payment. Specific mailing addresses are available on the IRS website. It's crucial to check these details to ensure timely processing of your form.

How can I get more help with Form 720?

If you need more assistance, the IRS provides resources online, including instructions for completing Form 720. Additionally, you can contact the IRS directly or consult a tax professional for personalized guidance. Don't hesitate to reach out for help if you need it!

Incorrect Identification Information: Many individuals forget to double-check their name, Social Security number, or Employer Identification Number. Even a small typo can cause delays in processing.

Missing Signature: Some applicants neglect to sign the form. A signature is essential, and in its absence, the submission may be considered incomplete.

Filing for the Wrong Quarter: It’s important to ensure that the filing period corresponds with the quarter selected on the form. Misalignment can lead to confusion and potential penalties.

Inaccurate Calculation of Taxes: Errors in calculating the amount owed can create significant issues. Reviewing the math prior to submitting the form can help prevent overpayments or underpayments.

Neglecting to Include Additional Forms: Some people mistakenly believe that the IRS 720 form stands alone. It often requires additional documentation, which, if overlooked, can result in an incomplete submission.

Failing to Keep Copies: After submission, individuals sometimes forget to save a copy of their completed form for their records. Keeping a personal copy is crucial for future reference and correspondence.

Ignoring Deadlines: Lastly, many do not pay close attention to filing deadlines. Submitting the form late can incur penalties, making it important to mark the due dates on a calendar.

The IRS Form 720 is primarily used for reporting and paying the federal excise taxes imposed on certain goods and services, as well as for various other purposes related to compliance with tax obligations. However, several other forms and documents often accompany it in practice. Each of these forms serves a specific role in the larger framework of tax compliance and reporting.

Understanding these accompanying forms and documents not only clarifies the tax compliance process but can also help taxpayers navigate the complexities of federal obligations effectively. Properly managing these forms can ensure individuals and organizations meet their tax responsibilities accurately and on time.

The IRS Form 941 is similar to the IRS Form 720 in that both documents are used for reporting taxes. However, Form 941 is specifically for employers to report wages paid and the taxes withheld from employees’ paychecks. This includes federal income tax, Social Security tax, and Medicare tax. Unlike Form 720, which is for reporting certain types of liabilities, Form 941 is focused on employee-related payroll taxes. Both forms must be filed regularly, typically on a quarterly basis, which ensures that the IRS maintains updated records of tax liabilities.

The IRS Form 944 is another document that bears similarities to the Form 720. The main distinction lies in its use by smaller employers. Form 944 allows businesses with smaller annual payrolls to report their payroll liabilities once a year instead of quarterly, as is the case with Form 941. Like Form 941 and Form 720, it requires accurate reporting of withheld taxes and payments owed, simplifying the process for employers who meet specific criteria and thereby reducing their filing burden.

The IRS Form 1099 series shares similarities with the IRS Form 720 in terms of reporting income and certain tax liabilities. Form 1099 covers a range of specific income types, such as freelance earnings and interest income. Each variation, such as 1099-MISC or 1099-NEC, provides information to the IRS about different income sources. Unlike Form 720, which focuses on excise taxes, the 1099 forms primarily report income information, ensuring that all taxable earnings are accounted for by both taxpayers and the IRS.

The IRS Form 1065 also has comparable features with Form 720 as both are used in relation to tax liabilities, but for different types of entities. Form 1065 is intended for partnerships to report income, deductions, gains, and losses. Partnerships do not pay tax at the entity level; instead, the income is passed through to individual partners. Thus, while Form 720 focuses on excise taxes, Form 1065 centers on partnership tax reporting, providing a snapshot of financial activities and tax responsibilities for multiple stakeholders.

The IRS Form 1120 is another tax document that bears a resemblance to Form 720 when considering that both relate to corporate entities. Form 1120 is used by corporations to report their income, gains, losses, deductions, and tax liability. The primary distinction is that while Form 720 addresses specific excise taxes, Form 1120 is centered on corporate income tax. Corporations must file Form 1120 annually to ensure compliance and accurate reporting of their financial activities.

Lastly, the IRS Form 720-TO is closely aligned with the IRS Form 720 as both pertain to the reporting of excise taxes. Form 720-TO is specifically utilized by certain businesses that qualify for a streamlined process for reporting and remitting these taxes. While Form 720 is a general excise tax form, 720-TO simplifies the reporting for eligible organizations, allowing them to report fewer details on a less frequent basis. Both forms ensure that excise tax obligations are met, but Form 720-TO caters to specific criteria designed for efficiency.

When filling out the IRS Form 720, it is important to follow certain guidelines to ensure accuracy and compliance. Here are some dos and don'ts to consider:

By following these guidelines, you can help ensure that your submission is processed smoothly. Taking these steps can minimize the risk of delays or issues with your application.

Misconceptions about the IRS Form 720 can lead to confusion and potential errors in filing. Below is a list of nine common misunderstandings regarding this form, along with clarifications to help individuals navigate the tax landscape more effectively.

Understanding the realities behind these misconceptions is vital for compliance and peace of mind. Education about tax forms like IRS Form 720 can empower individuals to manage their financial responsibilities confidently.

Filling out the IRS 720 form correctly is essential for anyone who needs to report and pay specific federal excise taxes. Here are key takeaways to keep in mind:

Understand the Purpose: The IRS 720 form is used primarily to report and pay federal excise taxes related to certain goods and activities.

Know the Deadlines: Make sure to check the due dates for filing the form. Generally, quarterly filings are required, with specific deadlines for each quarter.

Be Accurate: Double-check your entries. Errors can lead to delays in processing or incorrect tax bills, which can create unnecessary headaches later.

Use the Right Tax Rates: Familiarize yourself with the correct excise tax rates. Various categories may apply, such as those related to fuel, healthcare, or other specific goods.

Keep Records: Retain copies of your submitted forms and any supporting documentation. This can help in case of questions or audits from the IRS.

Consider E-Filing: Filing electronically may streamline the process and provide immediate confirmation of receipt.

By paying close attention to these takeaways, you can ensure a smoother experience with the IRS 720 form and its associated requirements.