The IRS 5472 form plays a crucial role in ensuring transparency and compliance for foreign-owned U.S. corporations. This form is specifically required for reporting transactions between a foreign shareholder and a U.S. corporation that is at least 25% foreign-owned. Businesses need to be aware that failure to file the 5472 can result in severe penalties, including hefty fines and other repercussions. The form gathers detailed information about foreign transactions, which assists the IRS in monitoring international business activities and adherence to U.S. tax laws. Understanding when and how to file the 5472 is essential for corporate compliance, making it imperative for business owners to pay attention to the reporting requirements. In this article, we will explore the common scenarios that trigger the need for this form, the information it requires, important deadlines to keep in mind, and the potential consequences of non-compliance.

Form 5472 |

Information Return of a 25% |

|

Foreign Corporation Engaged in a U.S. Trade or Business |

|

|

(Rev. December 2018) |

(Under Sections 6038A and 6038C of the Internal Revenue Code) |

OMB No. |

|

|

▶Go to www.irs.gov/Form5472 for instructions and the latest information.

Department of the Treasury |

For tax year of the reporting corporation beginning |

, |

, and ending |

, |

Internal Revenue Service |

Note: Enter all information in English and money items in U.S. dollars. |

|

||

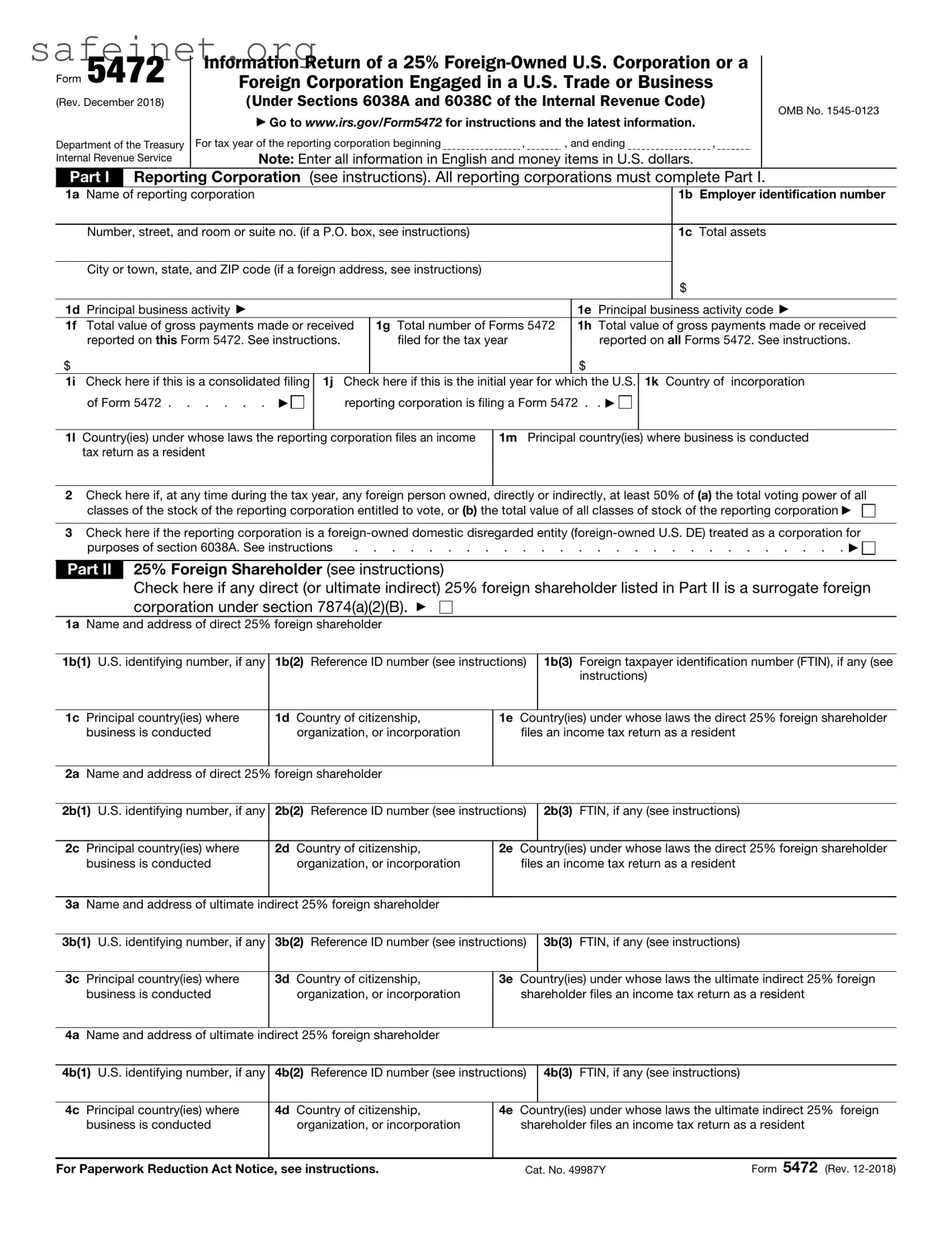

Part I Reporting Corporation (see instructions). All reporting corporations must complete Part I.

1a Name of reporting corporation |

|

|

|

|

|

1b Employer identification number |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. (if a P.O. box, see instructions) |

|

|

|

1c Total assets |

|||

|

|

|

|

|

|

|

|

City or town, state, and ZIP code (if a foreign address, see instructions) |

|

|

|

|

|||

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

1d Principal business activity ▶ |

|

|

|

1e Principal business activity code ▶ |

|||

1f Total value of gross payments made or received |

1g Total number of Forms 5472 |

1h Total value of gross payments made or received |

|||||

reported on this Form 5472. See instructions. |

|

filed for the tax year |

reported on all Forms 5472. See instructions. |

||||

$ |

|

|

|

|

$ |

|

|

1i Check here if this is a consolidated filing |

1j |

Check here if this is the initial year for which the U.S. |

1k Country of incorporation |

||||

of Form 5472 . . . . . . ▶ |

|

reporting corporation is filing a Form 5472 . . ▶ |

|

||||

|

|

|

|

||||

1l Country(ies) under whose laws the reporting corporation files an income |

1m Principal country(ies) where business is conducted |

||||||

tax return as a resident |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2Check here if, at any time during the tax year, any foreign person owned, directly or indirectly, at least 50% of (a) the total voting power of all

classes of the stock of the reporting corporation entitled to vote, or (b) the total value of all classes of stock of the reporting corporation ▶

3Check here if the reporting corporation is a

purposes of section 6038A. See instructions |

. . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ |

Part II 25% Foreign Shareholder (see instructions)

Check here if any direct (or ultimate indirect) 25% foreign shareholder listed in Part II is a surrogate foreign corporation under section 7874(a)(2)(B). ▶

1a Name and address of direct 25% foreign shareholder

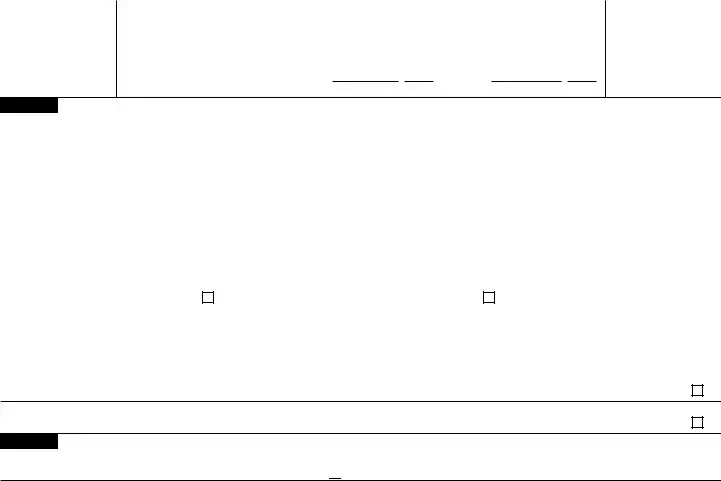

1b(1) U.S. identifying number, if any |

1b(2) Reference ID number (see instructions) |

1b(3) Foreign taxpayer identification number (FTIN), if any (see |

||||

|

|

|

|

|

instructions) |

|

|

|

|

|

|

|

|

1c |

Principal country(ies) where |

1d Country of citizenship, |

1e |

Country(ies) under whose laws the direct 25% foreign shareholder |

||

|

business is conducted |

organization, or incorporation |

|

files an income tax return as a resident |

|

|

|

|

|

|

|

|

|

2a |

Name and address of direct 25% |

foreign shareholder |

|

|

|

|

|

|

|

|

|||

2b(1) U.S. identifying number, if any |

2b(2) Reference ID number (see instructions) |

2b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

2c |

Principal country(ies) where |

2d Country of citizenship, |

2e |

Country(ies) under whose laws the direct 25% foreign shareholder |

||

|

business is conducted |

organization, or incorporation |

|

files an income tax return as a resident |

|

|

|

|

|

|

|

|

|

3a |

Name and address of ultimate indirect 25% foreign shareholder |

|

|

|

|

|

|

|

|

|

|||

3b(1) U.S. identifying number, if any |

3b(2) Reference ID number (see instructions) |

3b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

3c |

Principal country(ies) where |

3d Country of citizenship, |

3e |

Country(ies) under whose laws the ultimate indirect 25% foreign |

||

|

business is conducted |

organization, or incorporation |

|

shareholder files an income tax return as a resident |

||

|

|

|

|

|

|

|

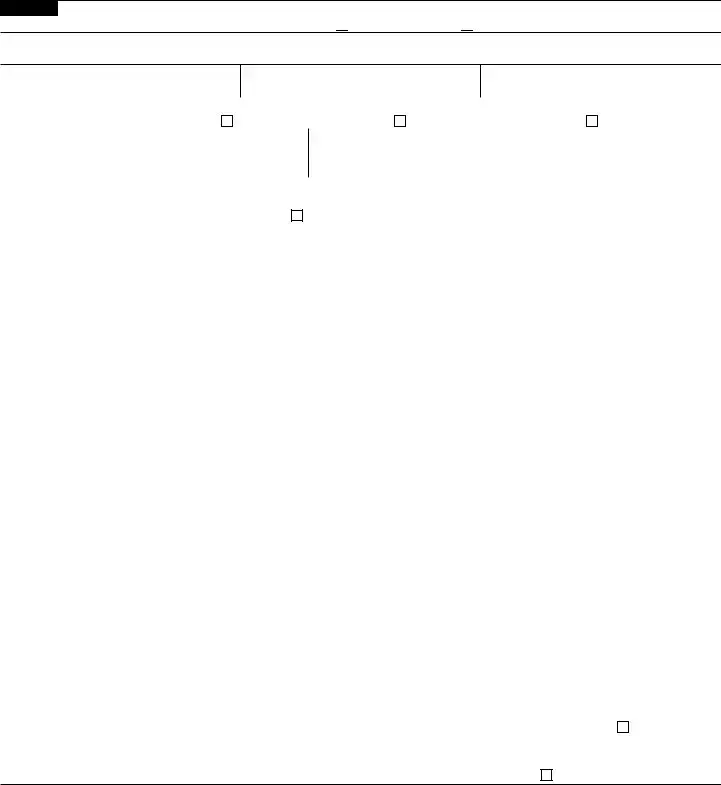

4a |

Name and address of ultimate indirect 25% foreign shareholder |

|

|

|

|

|

|

|

|

|

|||

4b(1) U.S. identifying number, if any |

4b(2) Reference ID number (see instructions) |

4b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

4c |

Principal country(ies) where |

4d Country of citizenship, |

4e |

Country(ies) under whose laws the ultimate indirect 25% foreign |

||

|

business is conducted |

organization, or incorporation |

|

shareholder files an income tax return as a resident |

||

|

|

|

|

|

||

For Paperwork Reduction Act Notice, see instructions. |

|

Cat. No. 49987Y |

Form 5472 (Rev. |

|||

Form 5472 (Rev. |

Page 2 |

Part III Related Party (see instructions). All reporting corporations must complete this question and the rest of Part III. Check applicable box: Is the related party a  foreign person or

foreign person or  U.S. person?

U.S. person?

1a Name and address of related party

1b(1) U.S. identifying number, if any

1b(2) Reference ID number (see instructions)

1b(3) FTIN, if any (see instructions)

1c |

Principal business activity ▶ |

|

|

|

1d Principal business activity code ▶ |

|

1e |

Related to reporting corporation |

Related to 25% foreign shareholder |

25% foreign shareholder |

|||

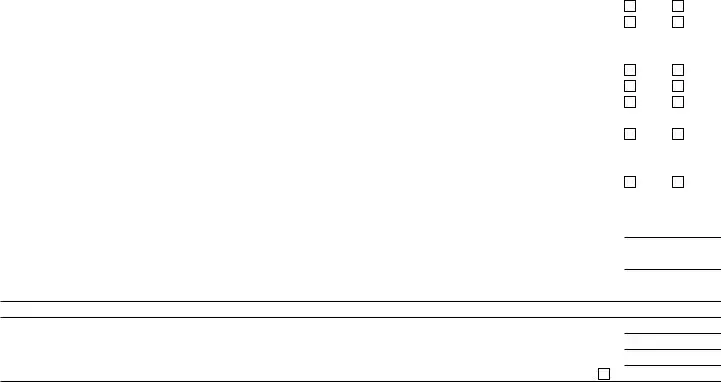

1f |

Principal country(ies) where business is conducted |

1g Country(ies) under whose laws the related party files an income tax return as a |

||||

|

|

|

resident |

|

|

|

Part IV |

Monetary Transactions Between Reporting Corporations and Foreign Related Party (see instructions) |

|||||

|

|

Caution: Part IV must be completed if the “foreign person” box is checked in the heading for Part III. |

||||

|

|

If estimates are used, check here. ▶ |

|

|

|

|

|

|

|

|

|

||

1 |

Sales of stock in trade (inventory) |

1 |

|

|||

2 |

Sales of tangible property other than stock in trade |

2 |

|

|||

3 |

Platform contribution transaction payments received |

3 |

|

|||

4 |

4 |

|

||||

5a |

Rents received (for other than intangible property rights) |

5a |

|

|||

b |

Royalties received (for other than intangible property rights) |

5b |

|

|||

6 |

Sales, leases, licenses, etc., of intangible property rights (for example, patents, trademarks, secret formulas) . . |

6 |

|

|||

7 |

Consideration received for technical, managerial, engineering, construction, scientific, or like services . . . . |

7 |

|

|||

8 |

Commissions received |

8 |

|

|||

9 |

Amounts borrowed (see instructions) a Beginning balance |

|

b Ending balance or monthly average ▶ |

9b |

|

|

10 |

Interest received |

10 |

|

|||

11 |

Premiums received for insurance or reinsurance |

11 |

|

|||

12 |

Other amounts received (see instructions) |

12 |

|

|||

13 |

Total. Combine amounts on lines 1 through 12 |

13 |

|

|||

14 |

Purchases of stock in trade (inventory) |

14 |

|

|||

15 |

Purchases of tangible property other than stock in trade |

15 |

|

|||

16 |

Platform contribution transaction payments paid |

16 |

|

|||

17 |

17 |

|

||||

18a |

Rents paid (for other than intangible property rights) |

18a |

|

|||

b |

Royalties paid (for other than intangible property rights) |

18b |

|

|||

19 |

Purchases, leases, licenses, etc., of intangible property rights (for example, patents, trademarks, secret formulas) |

19 |

|

|||

20 |

Consideration paid for technical, managerial, engineering, construction, scientific, or like services |

20 |

|

|||

21 |

Commissions paid |

21 |

|

|||

22 |

Amounts loaned (see instructions) a Beginning balance |

|

b Ending balance or monthly average ▶ |

22b |

|

|

23 |

Interest paid |

23 |

|

|||

24 |

Premiums paid for insurance or reinsurance |

24 |

|

|||

25 |

Other amounts paid (see instructions) |

25 |

|

|||

26 |

Total. Combine amounts on lines 14 through 25 |

26 |

|

|||

Part V |

Reportable Transactions of a Reporting Corporation That is a |

|||||

|

|

Describe on an attached separate sheet any other transaction as defined by Regulations section |

||||

|

|

such as amounts paid or received in connection with the formation, dissolution, acquisition, and disposition |

||||

|

|

of the entity, including contributions to and distributions from the entity, and check here. ▶ |

||||

|

|

|||||

Part VI |

Nonmonetary and |

|||||

|

|

the Foreign Related Party (see instructions) |

|

|

|

|

|

|

Describe these transactions on an attached separate sheet and check here. ▶ |

|

|

||

Form 5472 (Rev.

Form 5472 (Rev. |

Page 3 |

|

Part VII |

Additional Information. |

All reporting corporations must complete Part VII. |

1 |

Does the reporting corporation import goods from a foreign related party? |

2a |

If “Yes,” is the basis or inventory cost of the goods valued at greater than the customs value of the imported goods? . |

bIf “Yes,” attach a statement explaining the reason or reasons for such difference.

Yes Yes

No No

cIf the answers to questions 1 and 2a are “Yes,” were the documents used to support this treatment of the imported

goods in existence and available in the United States at the time of filing Form 5472? . . . . . . . . . . .

3 During the tax year, was the foreign parent corporation a participant in any

4During the course of the tax year, did the foreign parent corporation become a participant in any

5a During the tax year, did the reporting corporation pay or accrue any interest or royalty, to the related party, for which the deduction is not allowed under section 267A? See instructions . . . . . . . . . . . . . . . . . .

Yes

Yes

Yes

Yes

No

No

No

No

b If “Yes,” enter the total amount of the disallowed deductions . |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

$ |

|

|

6a Does the reporting corporation claim a |

|

|

|||||||||||||||||

respect to amounts listed in Part IV? |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

Yes |

No |

bIf “Yes,” enter the amount of gross income derived from sales, leases, exchanges, or other dispositions (but not licenses) of property to the foreign related party that the reporting corporation included in its computation of

deduction eligible income (FDDEI). See instructions . . . . . . . . . . . . . . . . . . . . $

cIf “Yes,” enter the amount of gross income derived from a license of property to the foreign related party that the

reporting corporation included in its computation of FDDEI. See instructions. . . . . . . . . . . . . $

dIf “Yes,” enter the amount of gross income derived from services provided to the foreign related party that the reporting

corporation included in its computation of FDDEI. See instructions . . . . . . . . . . . . . . . $

Part VIII Base Erosion Payments and Base Erosion Tax Benefits Under Section 59A (see instructions)

1 |

Amounts defined as base erosion payments under section 59A(d) |

. |

$ |

|

2 |

Amount of base erosion tax benefits under section 59A(c)(2) |

. |

$ |

|

3 |

Amount of total qualified derivative payments as described in section 59A(h) made by the reporting corporation . |

. |

$ |

|

4 |

Reserved for future use |

|

|

|

|

|

|

||

Form 5472 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 5472 is used to provide information on foreign-owned U.S. corporations and foreign corporations engaged in a trade or business in the United States. |

| Filing Requirement | Any U.S. corporation with at least 25% foreign ownership must file Form 5472 annually. |

| Deadline | The form is typically due on the 15th day of the 4th month after the end of the corporation's tax year. |

| Penalties | Failure to file Form 5472 timely can result in substantial penalties, which can reach up to $25,000 per form, per year. |

| Who Must File | Both foreign and domestic corporations, if they have foreign owners or engage in specified transactions with foreign parties. |

| Governing Laws | The IRS Form 5472 is governed by the Internal Revenue Code (IRC) Section 6038A and related regulations. |

| Additional Information | Supporting documents must be maintained and available upon request, including invoices and contracts related to reported transactions. |

After you've gathered the necessary information, filling out the IRS 5472 form can be straightforward. It may seem daunting at first, but by following these steps, you can ensure that you complete it accurately.

What is IRS Form 5472?

IRS Form 5472 is used by foreign-owned U.S. corporations or foreign corporations engaged in a trade or business in the United States. The form provides information about transactions between the reporting corporation and its foreign shareholders, related parties, or affiliates. Filing this form helps the IRS monitor potential issues with international tax compliance.

Who needs to file Form 5472?

Any foreign corporation that has a U.S. subsidiary where at least 25% of the stock is owned by a foreign person must file Form 5472. Additionally, foreign corporations with U.S. operations that have certain related party transactions need to file this form to provide transparency regarding those dealings.

When is Form 5472 due?

Form 5472 is typically due on the same date as your corporation's income tax return. For calendar year taxpayers, this means the due date is usually April 15. If you extend your income tax return, the Form 5472 deadline extends as well. However, filings must still be completed within the designated tax year.

What happens if I don’t file Form 5472?

Failure to file Form 5472 can lead to significant penalties. The IRS imposes an initial penalty of $25,000 for each failure to file. Additional penalties may accrue for continued infractions or if the form is filed late. It's crucial to stay compliant to avoid these financial repercussions.

Can I file Form 5472 electronically?

Yes, Form 5472 can be filed electronically as part of your corporate income tax return using compatible tax software. Ensure that the software provides an option for Form 5472, as it may not be included in all filing services. Otherwise, it may be necessary to file a paper copy directly to the IRS.

Where can I find the instructions for filling out Form 5472?

The instructions for Form 5472 can be found on the IRS website. The site provides comprehensive guidance on how to complete the form, including which transactions need to be reported and how to make corrections if necessary. Always refer to the latest version of the form and its instructions to ensure compliance.

Failing to file the form by the due date. Timeliness is crucial for avoiding penalties.

Omitting required information about foreign ownership. All details about the foreign shareholder must be accurate.

Not indicating the correct tax year for which the form is being filed. Each form must correspond to a specific reporting period.

Providing incomplete addresses for foreign owners and related parties. Full addresses are necessary for clarity.

Misidentifying the type of transactions conducted with related parties. Correct categorization is essential for reporting accuracy.

Failing to sign and date the form. A signature confirms the authenticity of the information provided.

Incorrectly calculating the amount of money transferred. Accurate financial information is critical.

Not keeping adequate records to support the information provided on the form. Documentation is vital for compliance.

Overlooking the need for an Employer Identification Number (EIN) if applicable. This number is often required for proper identification.

Ignoring the potential need for additional forms or schedules that may be necessary alongside the IRS 5472. Comprehensive filing can help avoid complications.

The IRS 5472 form is crucial for certain foreign-owned U.S. corporations and foreign corporations engaged in a trade or business in the U.S. However, it's not the only document you may need. Below is a compilation of other related forms and documents that often accompany the IRS 5472, providing essential details for compliance.

Ensuring accurate and timely submission of these forms not only fulfills legal requirements but also helps prevent complications with the IRS. Familiarizing yourself with these documents can streamline the process and ensure compliance.

The IRS Form 8858 is similar to Form 5472 as both are used for foreign entities and ownership. Specifically, Form 8858 is filed by U.S. persons who own a foreign disregarded entity or a foreign branch. It captures details regarding the financial activities of these foreign entities, including income, expenses, and transactions. Like Form 5472, it helps ensure transparency and compliance with U.S. tax laws, providing the IRS with comprehensive information about foreign holdings.

Another document that bears resemblance is IRS Form 8865. This form is utilized by U.S. taxpayers who are partners in a foreign partnership. Similar to Form 5472, it reports various financial details, including income, deductions, and the partners’ percentage of ownership. It facilitates the IRS in assessing the tax obligations tied to international partnerships, highlighting the intricate financial relationship between U.S. citizens and foreign entities.

IRS Form 8938, which mandates specified U.S. taxpayers to report foreign financial assets, shares some similarities with Form 5472. Both forms focus on ensuring U.S. taxpayers comply with disclosure requirements concerning foreign holdings. Form 8938 aims to provide the IRS with a broader understanding of an individual's foreign assets, whereas Form 5472 concentrates on transactions with foreign entities, but both ultimately promote transparency in international finance.

The IRS Form 1120 is also worth noting due to its connection with U.S. corporations. Similar to Form 5472's purpose, Form 1120 reports the income, gains, losses, and deductions of a domestic corporation. While Form 5472 specifically addresses transactions involving foreign entities, both highlight the importance of accurate reporting for compliance with U.S. tax regulations.

In the realm of international tax reporting, IRS Form 1042 is significant. This form provides information on amounts paid to foreign persons, along with withholding tax details. Much like Form 5472, it ensures that the IRS is informed about funds flowing across borders, promoting compliance with tax obligations for foreign recipients. Both forms play a crucial role in understanding international financial relationships.

Additionally, IRS Schedule B, which accompanies the Form 1040, focuses on reporting interest and dividend income from foreign assets. While it primarily addresses individual taxpayers, it shares the goal of Form 5472 by enhancing transparency surrounding foreign financial interests of U.S. citizens. Reporting under Schedule B highlights the importance of documenting all sources of income, including foreign earned income.

The IRS Form 1065, which reports income, gains, and losses from partnerships, is similar to Form 5472 regarding its focus on entity reporting. Both forms require detailed information about financial operations, although Form 1065 pertains specifically to domestic partnerships. It seeks to provide the IRS with a clear view of partnership transactions and activities, paralleling how Form 5472 works for foreign transactions.

Lastly, Form 8939, which relates to the transfer of estate assets, resembles Form 5472 in its reporting function. While the focus of Form 8939 is on estate tax matters, it requires disclosure of certain foreign financial assets. Both forms serve to enhance the IRS's understanding of potential tax liabilities tied to cross-border transactions or holdings, reinforcing the necessity of thorough reporting.

When completing the IRS 5472 form, it is essential to be diligent and accurate. Here are some important dos and don’ts to keep in mind.

Staying organized and meticulous while filling out the IRS 5472 form can help avoid complications later on.

The IRS Form 5472 is often misunderstood, leading to confusion among those required to file it. Here is a list of eight common misconceptions about this form:

Understanding the realities of Form 5472 can help individuals and businesses meet their tax obligations more effectively and accurately.

Filling out the IRS 5472 form may seem daunting at first, but understanding its key aspects can simplify the process significantly. Here are some essential takeaways:

Understanding these key points can make the process of filling out and using the IRS 5472 form much easier and more manageable. Keep careful records, meet deadlines, and consider seeking help when needed.