The IRS 5304-SIMPLE form plays a crucial role for small businesses looking to establish a SIMPLE IRA plan, which stands for Savings Incentive Match Plan for Employees Individual Retirement Account. This form is designed to provide essential information about the plan to employees, ensuring they understand their options for retirement savings. By using this form, employers can outline the terms of the SIMPLE IRA plan, including eligibility criteria, contribution limits, and the matching contributions that employers are required to make. It also serves as a tool for employees to make informed decisions about their retirement savings, as it details how they can contribute to their accounts and the benefits of participating in the plan. Proper completion and distribution of the IRS 5304-SIMPLE form are vital for compliance with IRS regulations and for fostering a transparent relationship between employers and employees regarding retirement benefits. Understanding this form is essential for both employers and employees to maximize the advantages of a SIMPLE IRA plan.

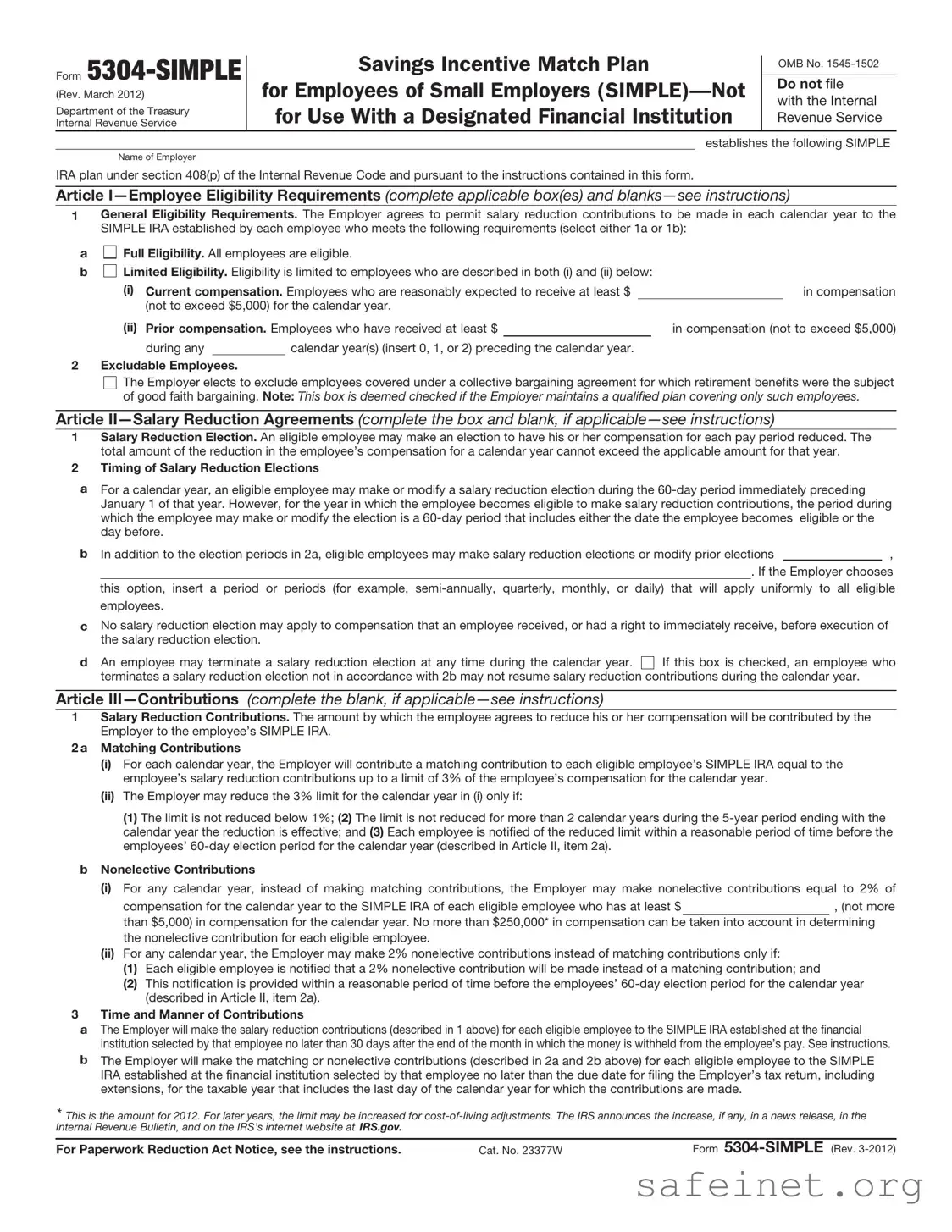

Form

(Rev. March 2012)

Department of the Treasury

Internal Revenue Service

Savings Incentive Match Plan

for Employees of Small Employers

OMB No.

Do not file

with the Internal Revenue Service

establishes the following SIMPLE

Name of Employer

IRA plan under section 408(p) of the Internal Revenue Code and pursuant to the instructions contained in this form.

Article

1General Eligibility Requirements. The Employer agrees to permit salary reduction contributions to be made in each calendar year to the SIMPLE IRA established by each employee who meets the following requirements (select either 1a or 1b):

a |

Full Eligibility. All employees are eligible. |

|

|

||||||

b |

Limited Eligibility. Eligibility is limited to employees who are described in both (i) and (ii) below: |

|

|

||||||

|

(i) |

Current compensation. Employees who are reasonably expected to receive at least $ |

|

in compensation |

|||||

|

(ii) |

(not to exceed $5,000) for the calendar year. |

|

|

|

||||

|

Prior compensation. Employees who have received at least $ |

|

|

in compensation (not to exceed $5,000) |

|||||

|

|

during any |

|

calendar year(s) (insert 0, 1, or 2) preceding the calendar year. |

|

|

|||

2Excludable Employees.

The Employer elects to exclude employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. Note: This box is deemed checked if the Employer maintains a qualified plan covering only such employees.

Article

1Salary Reduction Election. An eligible employee may make an election to have his or her compensation for each pay period reduced. The total amount of the reduction in the employee’s compensation for a calendar year cannot exceed the applicable amount for that year.

2Timing of Salary Reduction Elections

aFor a calendar year, an eligible employee may make or modify a salary reduction election during the

b In addition to the election periods in 2a, eligible employees may make salary reduction elections or modify prior elections,

. If the Employer chooses this option, insert a period or periods (for example,

cNo salary reduction election may apply to compensation that an employee received, or had a right to immediately receive, before execution of the salary reduction election.

dAn employee may terminate a salary reduction election at any time during the calendar year. If this box is checked, an employee who terminates a salary reduction election not in accordance with 2b may not resume salary reduction contributions during the calendar year.

Article

1Salary Reduction Contributions. The amount by which the employee agrees to reduce his or her compensation will be contributed by the Employer to the employee’s SIMPLE IRA.

2 a Matching Contributions

(i)For each calendar year, the Employer will contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions up to a limit of 3% of the employee’s compensation for the calendar year.

(ii)The Employer may reduce the 3% limit for the calendar year in (i) only if:

(1) The limit is not reduced below 1%; (2) The limit is not reduced for more than 2 calendar years during the

bNonelective Contributions

(i)For any calendar year, instead of making matching contributions, the Employer may make nonelective contributions equal to 2% of

compensation for the calendar year to the SIMPLE IRA of each eligible employee who has at least $, (not more

than $5,000) in compensation for the calendar year. No more than $250,000* in compensation can be taken into account in determining the nonelective contribution for each eligible employee.

(ii)For any calendar year, the Employer may make 2% nonelective contributions instead of matching contributions only if:

(1)Each eligible employee is notified that a 2% nonelective contribution will be made instead of a matching contribution; and

(2)This notification is provided within a reasonable period of time before the employees’

3Time and Manner of Contributions

aThe Employer will make the salary reduction contributions (described in 1 above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than 30 days after the end of the month in which the money is withheld from the employee’s pay. See instructions.

bThe Employer will make the matching or nonelective contributions (described in 2a and 2b above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than the due date for filing the Employer’s tax return, including extensions, for the taxable year that includes the last day of the calendar year for which the contributions are made.

* This is the amount for 2012. For later years, the limit may be increased for

For Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 23377W |

Form |

Form |

Page 2 |

Article |

|

1Contributions in General. The Employer will make no contributions to the SIMPLE IRAs other than salary reduction contributions (described in Article III, item 1) and matching or nonelective contributions (described in Article III, items 2a and 2b).

2Vesting Requirements. All contributions made under this SIMPLE IRA plan are fully vested and nonforfeitable.

3No Withdrawal Restrictions. The Employer may not require the employee to retain any portion of the contributions in his or her SIMPLE IRA or otherwise impose any withdrawal restrictions.

4Selection of IRA Trustee. The Employer must permit each eligible employee to select the financial institution that will serve as the trustee, custodian, or issuer of the SIMPLE IRA to which the Employer will make all contributions on behalf of that employee.

5Amendments To This SIMPLE IRA Plan. This SIMPLE IRA plan may not be amended except to modify the entries inserted in the blanks or boxes provided in Articles I, II, III, VI, and VII.

6Effects Of Withdrawals and Rollovers

aAn amount withdrawn from the SIMPLE IRA is generally includible in gross income. However, a SIMPLE IRA balance may be rolled over or transferred on a

bIf an individual withdraws an amount from a SIMPLE IRA during the

Article

1Compensation

aGeneral Definition of Compensation. Compensation means the sum of the wages, tips, and other compensation from the Employer subject to federal income tax withholding (as described in section 6051(a)(3)), the amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority, and the employee’s salary reduction contributions made under this plan, and, if applicable, elective deferrals under a section 401(k) plan, a SARSEP, or a section 403(b) annuity contract and compensation deferred under a section 457 plan required to be reported by the Employer on Form

bCompensation for

2Employee. Employee means a

3Eligible Employee. An eligible employee means an employee who satisfies the conditions in Article I, item 1 and is not excluded under Article I, item 2.

4SIMPLE IRA. A SIMPLE IRA is an individual retirement account described in section 408(a), or an individual retirement annuity described in section 408(b), to which the only contributions that can be made are contributions under a SIMPLE IRA plan and rollovers or transfers from another SIMPLE IRA.

Article

are unavailable, or (2) that financial institution provides the procedures directly to the employee. See Employee Notification in the instructions.)

Article

This SIMPLE IRA plan is effective |

|

|

|

|

. See |

|

instructions. |

|

|

|

|

|

|

* |

* |

* |

* |

* |

|

|

|

|

|

|

|

|

|

Name of Employer |

|

By: |

Signature |

Date |

||

|

|

|

|

|

|

|

Address of Employer |

|

Name and title |

|

|

||

Form

Form |

Page 3 |

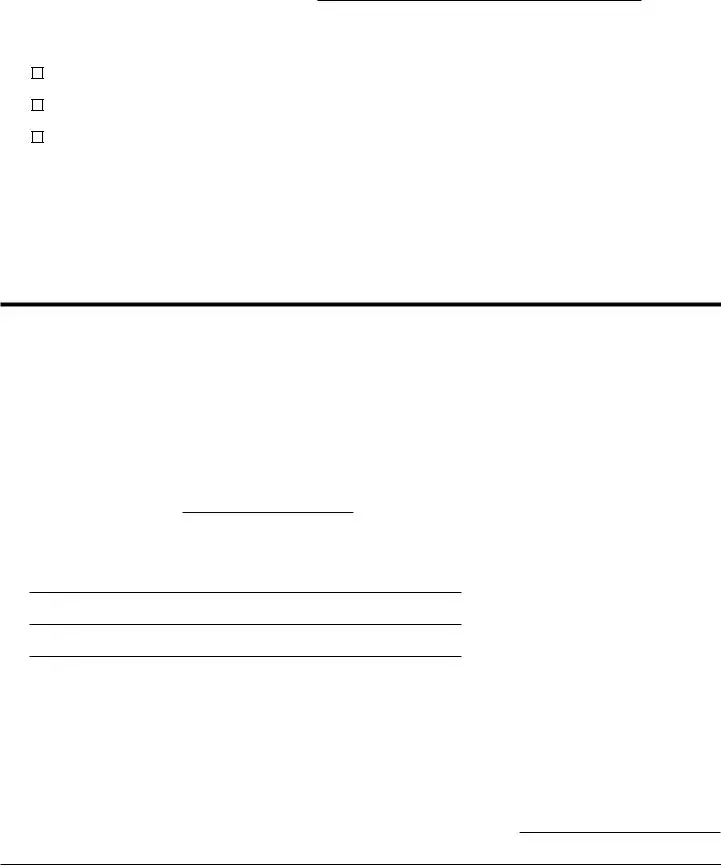

Model Notification to Eligible Employees

I.Opportunity to Participate in the SIMPLE IRA Plan

You are eligible to make salary reduction contributions to theSIMPLE IRA

plan. This notice and the attached summary description provide you with information that you should consider before you decide whether to start, continue, or change your salary reduction agreement.

II.Employer Contribution Election

For the |

|

calendar year, the Employer elects to contribute to your SIMPLE IRA (employer must select either (1), (2), or (3)): |

|||||

(1) |

A matching contribution equal to your salary reduction contributions up to a limit of 3% of your compensation for the year; |

||||||

(2) |

A matching contribution equal to your salary reduction contributions up to a limit of |

% (employer must insert a |

|||||

number from 1 to 3 and is subject to certain restrictions) of your compensation for the |

year; or |

|

|||||

(3) |

A nonelective contribution equal to 2% of your compensation for the year (limited to compensation of $250,000*) if you are an |

||||||

employee who makes at least $ |

|

(employer must insert an amount that is $5,000 or less) in compensation for |

|||||

the year. |

|

|

|

|

|

||

|

|

|

|

|

|||

III.Administrative Procedures

To start or change your salary reduction contributions, you must complete the salary reduction agreement and return it to

|

|

|

(employer should designate a place or |

individual by |

|

(employer should insert a date that is not less than 60 |

days after notice is given). |

|

|

|

|

IV. Employee Selection of Financial Institution

You must select the financial institution that will serve as the trustee, custodian, or issuer of your SIMPLE IRA and notify your Employer of your selection.

Model Salary Reduction Agreement

I.Salary Reduction Election

Subject to the requirements of the SIMPLE IRA plan of |

|

|

|

|

(name of |

|||

employer) I authorize |

|

% or $ |

|

|

(which equals |

|

% of my current rate of pay) to be withheld from |

|

my pay for each pay period and contributed to my SIMPLE IRA as a salary reduction contribution.

II.Maximum Salary Reduction

I understand that the total amount of my salary reduction contributions in any calendar year cannot exceed the applicable amount for that year. See instructions.

III.Date Salary Reduction Begins

I understand that my salary reduction contributions will start as soon as permitted under the SIMPLE IRA plan and as soon as

administratively feasible or, if later,. (Fill in the date you want the salary reduction contributions to begin. The date must be after you sign this agreement.)

IV. Employee Selection of Financial Institution

I select the following financial institution to serve as the trustee, custodian, or issuer of my SIMPLE IRA.

Name of financial institution

Address of financial institution

SIMPLE IRA account name and number

I understand that I must establish a SIMPLE IRA to receive any contributions made on my behalf under this SIMPLE IRA plan. If the information regarding my SIMPLE IRA is incomplete when I first submit my salary reduction agreement, I realize that it must be completed by the date contributions must be made under the SIMPLE IRA plan. If I fail to update my agreement to provide this information by that date, I understand that my Employer may select a financial institution for my SIMPLE IRA.

V.Duration of Election

This salary reduction agreement replaces any earlier agreement and will remain in effect as long as I remain an eligible employee under the SIMPLE IRA plan or until I provide my Employer with a request to end my salary reduction contributions or provide a new salary reduction agreement as permitted under this SIMPLE IRA plan.

Signature of employee |

|

Date |

*This is the amount for 2012. For later years, the limit may be increased for

Form

Form |

Page 4 |

General Instructions

Section references are to the Internal Revenue Code unless otherwise noted.

Purpose of Form

Form

SIMPLE IRA.

These instructions are designed to assist in the establishment and administration of the SIMPLE IRA plan. They are not intended to supersede any provision in the SIMPLE IRA plan.

Do not file Form

For more information, see Pub. 560, Retirement Plans for Small Business (SEP, SIMPLE, and Qualified Plans), and Pub. 590, Individual Retirement Arrangements (IRAs).

Note. If you used the March 2002, August 2005, or September 2008 version of Form

Which Employers May

Establish and Maintain a

SIMPLE IRA Plan?

To establish and maintain a SIMPLE IRA plan, you must meet both of the following requirements:

1.Last calendar year, you had no more than 100 employees (including

2.You do not maintain during any part of the calendar year another qualified plan with respect to which contributions are made, or benefits are accrued, for service in the calendar year. For this purpose, a qualified plan (defined in section 219(g)(5)) includes a qualified pension plan, a

participating in the SIMPLE IRA plan. If the failure to continue to satisfy the

Certain related employers (trades or businesses under common control) must be treated as a single employer for purposes of the SIMPLE IRA requirements. These are: (1) a controlled group of corporations under section 414(b); (2) a partnership or sole proprietorship under common control under section 414(c); or (3) an affiliated service group under section 414(m). In addition, if you have leased employees required to be treated as your own employees under the rules of section 414(n), then you must count all such leased employees for the requirements listed above.

What Is a SIMPLE IRA Plan?

A SIMPLE IRA plan is a written arrangement that provides you and your employees with an easy way to make contributions to provide retirement income for your employees. Under a SIMPLE IRA plan, employees may choose whether to make salary reduction contributions to the SIMPLE IRA plan rather than receiving these amounts as part of their regular compensation. In addition, you will contribute matching or nonelective contributions on behalf of eligible employees (see Employee Eligibility Requirements below and Contributions later). All contributions under this plan will be deposited into a SIMPLE individual retirement account or annuity established for each eligible employee with the financial institution selected by him or her.

When To Use Form

A SIMPLE IRA plan may be established by using this Model Form or any other document that satisfies the statutory requirements.

Do not use Form

1.You want to require that all SIMPLE IRA plan contributions initially go to a financial institution designated by you. That is, you do not want to permit each of your eligible employees to choose a financial institution that will initially receive contributions. Instead, use Form

2.You want employees who are nonresident aliens receiving no earned income from you that is income from sources within the United States to be eligible under this plan; or

3.You want to establish a SIMPLE 401(k) plan.

Completing Form

Pages 1 and 2 of Form

The SIMPLE IRA plan is a legal document with important tax consequences for you and your employees. You may want to consult with your attorney or tax advisor before adopting this plan.

Employee Eligibility Requirements (Article I)

Each year for which this SIMPLE IRA plan is effective, you must permit salary reduction contributions to be made by all of your employees who are reasonably expected to receive at least $5,000 in compensation from you during the year, and who received at least $5,000 in compensation from you in any 2 preceding years. However, you can expand the group of employees who are eligible to participate in the SIMPLE IRA plan by completing the options provided in Article I, items 1a and 1b. To choose full eligibility, check the box in Article I, item 1a. Alternatively, to choose limited eligibility, check the box in Article I, item 1b, and then insert “$5,000” or a lower compensation amount (including zero) and “2” or a lower number of years of service in the blanks in (i) and (ii) of Article I, item 1b.

In addition, you can exclude from participation those employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. You may do this by checking the box in Article I, item 2. Under certain circumstances, these employees must be excluded. See Which Employers May Establish and Maintain a SIMPLE IRA Plan? above.

Salary Reduction Agreements (Article II)

As indicated in Article II, item 1, a salary reduction agreement permits an eligible employee to make a salary reduction election to have his or her compensation for each pay period reduced by a percentage (expressed as a percentage or dollar amount). The total amount of

Form |

Page 5 |

the reduction in the employee’s compensation cannot exceed the applicable amount for any calendar year. The applicable amount is $11,500 for 2012. After 2012, the $11,500 amount may be increased for

Timing of Salary Reduction Elections

For any calendar year, an eligible employee may make or modify a salary reduction election during the

You can extend the

You may use the Model Salary Reduction Agreement on page 3 to enable eligible employees to make or modify salary reduction elections.

Employees must be permitted to terminate their salary reduction elections at any time. They may resume salary reduction contributions for the year if permitted under Article II, item 2b. However, by checking the box in Article II, item 2d, you may prohibit an employee who terminates a salary reduction election outside the normal election cycle from resuming salary reduction contributions during the remainder of the calendar year.

Contributions (Article III)

Only contributions described below may be made to this SIMPLE IRA plan. No additional contributions may be made.

Salary Reduction Contributions

As indicated in Article III, item 1, salary reduction contributions consist of the amount by which the employee agrees to reduce his or her compensation. You must contribute the salary reduction contributions to the financial institution selected by each eligible employee.

Matching Contributions

In general, you must contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions. This matching contribution cannot exceed 3% of the employee’s compensation. See Definition of Compensation, below.

You may reduce this 3% limit to a lower percentage, but not lower than 1%. You cannot lower the 3% limit for more than 2 calendar years out of the

Note. If any year in the

To elect this option, you must notify the employees of the reduced limit within a reasonable period of time before the applicable

Nonelective Contributions

Instead of making a matching contribution, you may, for any year, make a nonelective contribution equal to 2% of compensation for each eligible employee who has at least $5,000 in compensation for the year.

Nonelective contributions may not be based on more than $250,000* of compensation.

To elect to make nonelective contributions, you must notify employees within a reasonable period of time before the applicable

Note. Insert “$5,000” in Article III, item 2b(i) to impose the $5,000 compensation requirement. You may expand the group of employees who are eligible for nonelective contributions by inserting a compensation amount lower than $5,000.

Effective Date (Article VII)

Insert in Article VII the date you want the provisions of the SIMPLE IRA plan to become effective. You must insert January 1 of the applicable year unless this is the first year for which you are adopting any SIMPLE IRA plan. If this is the first year for which you are adopting a SIMPLE IRA plan, you may insert any date between January 1 and October 1, inclusive of the applicable year.

Additional Information

Timing of Salary Reduction Contributions

The employer must make the salary reduction contributions to the financial institution selected by each eligible employee for his or her SIMPLE IRA no later than the 30th day of the month following the month in which the amounts would otherwise have been payable to the employee in cash.

The Department of Labor has indicated that most SIMPLE IRA plans are also subject to Title I of the Employee Retirement Income Security Act of 1974 (ERISA). Under Department of Labor regulations at 29 CFR

Definition of Compensation

“Compensation” means the amount described in section 6051(a)(3) (wages, tips, and other compensation from the employer subject to federal income tax withholding under section 3401(a)), and amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority. Usually, this is the amount shown in box 1 of Form

For

Employee Notification

You must notify each eligible employee prior to the employee’s

*This is the amount for 2012. For later years, the limit may be increased for

Form |

Page 6 |

issuer of the employee’s SIMPLE IRA. In this notification, you must indicate whether you will provide:

1.A matching contribution equal to your employees’ salary reduction contributions up to a limit of 3% of their compensation;

2.A matching contribution equal to your employees’ salary reduction contributions subject to a percentage limit that is between 1 and 3% of their compensation; or

3.A nonelective contribution equal to 2% of your employees’ compensation.

You can use the Model Notification to Eligible Employees earlier to satisfy these employee notification requirements for this SIMPLE IRA plan. A Summary Description must also be provided to eligible employees at this time. This summary description requirement may be satisfied by providing a completed copy of pages 1 and 2 of Form

Article

If you fail to provide the employee notification (including the summary description) described above, you will be liable for a penalty of $50 per day until the notification is provided. If you can show that the failure was due to reasonable cause, the penalty will not be imposed.

If the financial institution’s name, address, or withdrawal procedures are not available at the time the employee must be given the summary description, you must provide the summary description without this information. In that case, you will have reasonable cause for not including this information in the summary description, but only if you ensure that it is provided to the employee as soon as administratively feasible.

Reporting Requirements

You are not required to file any annual information returns for your SIMPLE IRA plan, such as Form 5500, Annual Return/Report of Employee Benefit Plan, or Form

Deducting Contributions

Contributions to this SIMPLE IRA plan are deductible in your tax year containing the end of the calendar year for which the contributions are made.

Contributions will be treated as made for a particular tax year if they are made for that year and are made by the due date (including extensions) of your income tax return for that year.

Summary Description

Each year the SIMPLE IRA plan is in effect, the financial institution for the SIMPLE IRA of each eligible employee must provide the employer the information described in section 408(l)(2)(B). This requirement may be satisfied by providing the employer a current copy of Form

There is a penalty of $50 per day imposed on the financial institution for each failure to provide the summary description described above. However, if the failure was due to reasonable cause, the penalty will not be imposed.

Paperwork Reduction Act Notice. You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete this form will vary depending on individual circumstances. The estimated average time is:

Recordkeeping . . |

. |

. |

3 hr., 38 min. |

Learning about the |

|

|

|

law or the form . . |

. |

. |

2 hr., 26 min. |

Preparing the form |

. |

. |

. . 47 min. |

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can write to the Internal Revenue Service, Tax Products Coordinating Committee, SE:W:CAR:MP:T:M:S, 1111 Constitution Ave. NW,

| Fact Name | Description |

|---|---|

| Purpose | The IRS 5304-SIMPLE form is used by employers to establish a SIMPLE IRA plan for their employees. |

| Eligibility | Employers with 100 or fewer employees who earned $5,000 or more in the preceding year can use this form. |

| Contribution Limits | For 2023, employees can contribute up to $15,500, with an additional $3,500 catch-up contribution for those aged 50 and older. |

| Filing Requirement | Employers must provide employees with the completed form and any necessary information about the plan. |

| State-Specific Forms | Some states may have additional requirements; for example, California requires compliance with state labor laws. |

| Deadline | The form must be established by October 1 of the year in which contributions will be made. |

| Tax Benefits | Contributions to a SIMPLE IRA are tax-deductible for employers, and employees can defer taxes on their contributions until withdrawal. |

Completing the IRS 5304-SIMPLE form is essential for setting up a SIMPLE IRA plan. After filling out this form, you will need to submit it to the IRS and provide copies to your employees. Ensure all information is accurate to avoid delays.

What is the IRS 5304-SIMPLE form?

The IRS 5304-SIMPLE form is used by employers to set up a SIMPLE IRA plan for their employees. SIMPLE stands for Savings Incentive Match Plan for Employees. This form outlines the plan's terms, including employee contribution limits and employer matching contributions. It’s designed for small businesses with 100 or fewer employees, making it a popular choice for those looking to offer retirement benefits without the complexity of larger plans.

Who is eligible to participate in a SIMPLE IRA plan?

Employees who earned at least $5,000 during any two preceding years and are expected to earn at least that amount in the current year can participate in a SIMPLE IRA plan. Employers must also meet specific criteria, such as having 100 or fewer employees who received at least $5,000 in compensation during the previous calendar year. This makes the plan accessible for many small business employees.

What are the contribution limits for a SIMPLE IRA?

For 2023, employees can contribute up to $15,500 to their SIMPLE IRA. If an employee is 50 years old or older, they can make an additional catch-up contribution of $3,500, bringing the total possible contribution to $19,000. Employers are required to either match employee contributions up to 3% of their compensation or provide a flat 2% contribution for all eligible employees, regardless of whether they contribute.

How do employers submit the IRS 5304-SIMPLE form?

Employers must complete the IRS 5304-SIMPLE form and provide it to their employees. This form does not need to be submitted to the IRS but should be kept on file as part of the plan documentation. Employers should also ensure that employees understand the plan's features and how to make contributions, as this information is crucial for participation.

Can employees withdraw funds from their SIMPLE IRA?

Yes, employees can withdraw funds from their SIMPLE IRA, but there are restrictions. Withdrawals made within the first two years of participation may be subject to a 25% penalty, while withdrawals after that period incur a 10% penalty if taken before age 59½. It's important for employees to understand these penalties and consider their long-term retirement goals before making withdrawals.

What happens if an employer decides to terminate the SIMPLE IRA plan?

If an employer decides to terminate the SIMPLE IRA plan, they must notify employees and provide them with information about their options. Employees can roll over their funds into another retirement account or withdraw the funds, but they should be aware of any tax implications. Employers must also ensure that all contributions are made up to the termination date and provide necessary documentation for the employees’ records.

Failing to provide accurate employer information. Ensure that the name, address, and Employer Identification Number (EIN) are correct.

Not checking eligibility requirements. Confirm that both the employer and employees meet the qualifications for a SIMPLE IRA.

Incorrectly calculating contribution limits. Be aware of the annual contribution limits set by the IRS and adhere to them.

Omitting employee signatures. All employees must sign the form to indicate their acceptance of the SIMPLE IRA plan.

Not including the correct plan year. Specify the correct year for which the SIMPLE IRA plan applies.

Ignoring the deadline for submission. Submit the form by the deadline to ensure compliance and avoid penalties.

Providing incomplete information. Double-check all sections of the form to ensure that no fields are left blank.

Misunderstanding the employer's contribution options. Familiarize yourself with the two contribution methods available for SIMPLE IRAs.

Failing to keep copies of submitted forms. Retain a copy of the completed form for your records and future reference.

Not consulting a tax professional when needed. Seek guidance if uncertain about any part of the form or the SIMPLE IRA plan.

The IRS 5304-SIMPLE form is used by employers to establish a Savings Incentive Match Plan for Employees (SIMPLE) IRA. This plan allows employees to contribute to their retirement savings with matching contributions from their employer. Alongside this form, there are several other documents that are commonly utilized to ensure compliance and proper management of the SIMPLE IRA. Below is a list of five such documents, each serving a distinct purpose.

These documents work together to create a comprehensive framework for managing a SIMPLE IRA plan. They ensure that both employers and employees understand their roles and responsibilities, while also providing the necessary information to comply with IRS regulations. Proper use of these forms can lead to successful retirement planning for employees and a smooth administration process for employers.

The IRS 5304-SIMPLE form is a key document for employers who wish to establish a SIMPLE IRA plan for their employees. It serves as a notice to employees about the plan's features and benefits. Similar to this form is the IRS Form 5500. This document is used to report information about employee benefit plans, including retirement plans. While the IRS 5304-SIMPLE focuses on informing employees about the SIMPLE IRA, Form 5500 provides a broader overview of all employee benefits, ensuring compliance and transparency in reporting.

Another related document is the IRS Form 8880, which is used to claim the Retirement Savings Contributions Credit. This form is for individuals who contribute to retirement accounts, including SIMPLE IRAs. While the 5304-SIMPLE informs employees about their options, Form 8880 allows them to benefit financially from their contributions, making retirement savings more accessible.

The IRS Form 1040 is also relevant, as it serves as the standard individual income tax return form. Individuals who contribute to a SIMPLE IRA will report their contributions on this form. While the 5304-SIMPLE outlines the plan's specifics, Form 1040 is where individuals reflect their financial activities, including retirement savings, on their tax returns.

Form W-2 is another important document that relates to the IRS 5304-SIMPLE. This form reports an employee's annual wages and the amount of taxes withheld. Contributions made to a SIMPLE IRA may be reflected on the W-2, showing how much has been set aside for retirement. While the 5304-SIMPLE informs employees about the plan, the W-2 provides a tangible record of their financial contributions.

The IRS Form 5305-SEP is also similar, as it is used to establish a Simplified Employee Pension plan. Both forms facilitate retirement savings for employees, but the 5305-SEP is designed for self-employed individuals and small business owners. While the 5304-SIMPLE focuses on a specific type of retirement account, the 5305-SEP provides an alternative option for those looking to save for retirement.

Form 401(k) is yet another related document. This form is used for a 401(k) retirement plan, which is a popular employer-sponsored retirement savings plan. While the 5304-SIMPLE is specific to SIMPLE IRAs, the 401(k) offers a different structure and contribution limits. Both forms aim to encourage retirement savings, but they cater to different employer and employee needs.

The IRS Form 8881 is also noteworthy, as it allows small businesses to claim a credit for setting up retirement plans. This form can be utilized by employers who establish a SIMPLE IRA plan. While the 5304-SIMPLE informs employees about their retirement options, Form 8881 incentivizes employers to offer such plans, ultimately benefiting employees.

Form 1099-R is another document that complements the IRS 5304-SIMPLE. This form is used to report distributions from retirement plans, including SIMPLE IRAs. When employees withdraw funds from their SIMPLE IRAs, Form 1099-R provides essential information for tax purposes. The 5304-SIMPLE sets the stage for retirement savings, while the 1099-R captures the financial impact of those savings when distributions occur.

Lastly, the IRS Form 5307 is relevant as it is used for a plan that is not a prototype or volume submitter plan. This form is used to apply for a determination letter for a retirement plan. While the 5304-SIMPLE provides the necessary information for employees about their SIMPLE IRA, Form 5307 helps employers ensure that their plan complies with IRS regulations, further supporting the retirement savings framework.

When filling out the IRS 5304-SIMPLE form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

Understanding the IRS 5304-SIMPLE form can be challenging, leading to various misconceptions. Here are nine common misunderstandings about this form, clarified for better comprehension.

This is not true. The IRS 5304-SIMPLE form is designed for small businesses with 100 or fewer employees. It provides a simple way for employers to offer retirement savings plans.

Participation is not mandatory. Employees can choose whether or not to contribute to the SIMPLE IRA plan, giving them flexibility based on their financial situation.

This is a misconception. Part-time employees who meet certain criteria, such as earning at least $5,000 in any two preceding years, can also participate in the plan.

On the contrary, employers are required to make contributions. They can choose between matching employee contributions or making a fixed contribution for all eligible employees.

This is incorrect. Employers can amend their SIMPLE IRA plan, but changes must comply with IRS regulations and be communicated to employees.

Employers can actually establish multiple SIMPLE IRA plans, provided they adhere to the rules and regulations governing these plans.

This is a misunderstanding. Contributions to a SIMPLE IRA are tax-deferred, meaning employees do not pay taxes on their contributions until they withdraw funds during retirement.

While primarily a retirement savings tool, the SIMPLE IRA can also serve as an important part of an overall financial strategy, helping employees save for various future needs.

Many find the process straightforward. The form is designed to be user-friendly, allowing employers to easily set up and manage the retirement plan.

By addressing these misconceptions, individuals and employers can better understand the benefits and requirements of the IRS 5304-SIMPLE form, ensuring they make informed decisions about retirement savings options.

When filling out and using the IRS 5304-SIMPLE form, it is essential to understand its purpose and requirements. Here are some key takeaways: