The IRS 2210 form is an essential tool for taxpayers who need to report an underpayment of estimated taxes. This form primarily addresses situations where individuals or businesses have failed to pay enough tax throughout the year, leading to potential penalties. The form allows taxpayers to calculate their required annual payments and determine if they owe any penalties for underpayment. Additionally, it provides options for different methods, including the annualized income method, which can be beneficial for those with fluctuating earnings. By filling out the IRS 2210, taxpayers can also request a waiver for penalties under specific situations, providing them with a way to potentially reduce financial burdens. Understanding the nuances of this form can significantly impact your tax situation, making it a crucial subject for anyone managing their taxes responsibly.

Form 2210 |

|

Underpayment of Estimated Tax by |

|

OMB No. |

|

|

Individuals, Estates, and Trusts |

|

2019 |

||

Department of the Treasury |

|

Go to www.irs.gov/Form2210 for instructions and the latest information. |

|

||

|

|

|

|

Attachment |

|

Internal Revenue Service |

|

Attach to Form 1040, |

|

Sequence No. 06 |

|

Name(s) shown on tax return |

|

|

Identifying number |

||

|

|

|

|

|

|

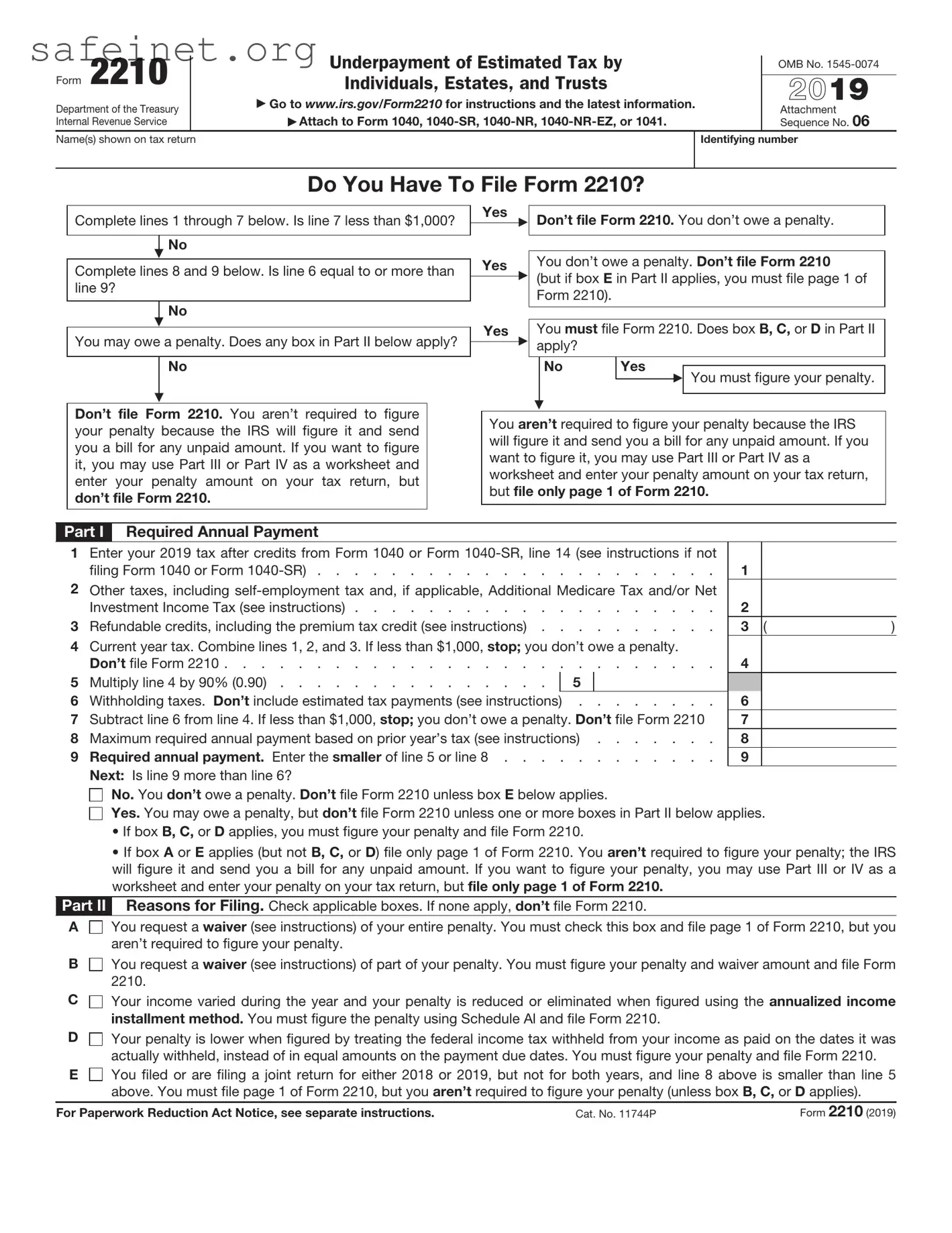

Do You Have To File Form 2210?

Complete lines 1 through 7 below. Is line 7 less than $1,000?

No

Complete lines 8 and 9 below. Is line 6 equal to or more than line 9?

No

You may owe a penalty. Does any box in Part II below apply?

No

Don’t file Form 2210. You aren’t required to figure your penalty because the IRS will figure it and send you a bill for any unpaid amount. If you want to figure it, you may use Part III or Part IV as a worksheet and enter your penalty amount on your tax return, but don’t file Form 2210.

Yes |

Don’t file Form 2210. You don’t owe a penalty. |

|

|

Yes |

|

You don’t owe a penalty. Don’t file Form 2210 |

|||||

|

|

|||||||

|

|

|

|

(but if box E in Part II applies, you must file page 1 of |

||||

|

|

|

|

|||||

|

|

|

|

Form 2210). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

|

You must file Form 2210. Does box B, C, or D in Part II |

|||||

|

||||||||

|

|

|

|

apply? |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

No |

Yes |

|

|

|

|

|

|

|

You must figure your penalty. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You aren’t required to figure your penalty because the IRS will figure it and send you a bill for any unpaid amount. If you want to figure it, you may use Part III or Part IV as a worksheet and enter your penalty amount on your tax return, but file only page 1 of Form 2210.

Part I Required Annual Payment

1Enter your 2019 tax after credits from Form 1040 or Form

filing Form 1040 or Form |

1 |

2Other taxes, including

Investment Income Tax (see instructions) |

2 |

|

|

3 Refundable credits, including the premium tax credit (see instructions) |

3 |

( |

) |

4Current year tax. Combine lines 1, 2, and 3. If less than $1,000, stop; you don’t owe a penalty.

|

Don’t file Form 2210 |

4 |

|

||

5 |

Multiply line 4 by 90% (0.90) |

5 |

|

|

|

6 |

Withholding taxes. Don’t include estimated tax payments (see instructions) |

6 |

|

||

7 |

Subtract line 6 from line 4. If less than $1,000, stop; you don’t owe a penalty. Don’t file Form 2210 |

7 |

|

||

8 |

Maximum required annual payment based on prior year’s tax (see instructions) |

8 |

|

||

9 |

Required annual payment. Enter the smaller of line 5 or line 8 |

9 |

|

||

|

Next: Is line 9 more than line 6? |

|

|

|

|

|

No. You don’t owe a penalty. Don’t file Form 2210 unless box E below applies. |

|

|

||

|

Yes. You may owe a penalty, but don’t file Form 2210 unless one or more boxes in Part II below applies. |

||||

•If box B, C, or D applies, you must figure your penalty and file Form 2210.

•If box A or E applies (but not B, C, or D) file only page 1 of Form 2210. You aren’t required to figure your penalty; the IRS will figure it and send you a bill for any unpaid amount. If you want to figure your penalty, you may use Part III or IV as a worksheet and enter your penalty on your tax return, but file only page 1 of Form 2210.

Part II Reasons for Filing. Check applicable boxes. If none apply, don’t file Form 2210.

A

You request a waiver (see instructions) of your entire penalty. You must check this box and file page 1 of Form 2210, but you aren’t required to figure your penalty.

You request a waiver (see instructions) of your entire penalty. You must check this box and file page 1 of Form 2210, but you aren’t required to figure your penalty.

B

You request a waiver (see instructions) of part of your penalty. You must figure your penalty and waiver amount and file Form 2210.

You request a waiver (see instructions) of part of your penalty. You must figure your penalty and waiver amount and file Form 2210.

C

Your income varied during the year and your penalty is reduced or eliminated when figured using the annualized income installment method. You must figure the penalty using Schedule Al and file Form 2210.

Your income varied during the year and your penalty is reduced or eliminated when figured using the annualized income installment method. You must figure the penalty using Schedule Al and file Form 2210.

D

Your penalty is lower when figured by treating the federal income tax withheld from your income as paid on the dates it was actually withheld, instead of in equal amounts on the payment due dates. You must figure your penalty and file Form 2210.

Your penalty is lower when figured by treating the federal income tax withheld from your income as paid on the dates it was actually withheld, instead of in equal amounts on the payment due dates. You must figure your penalty and file Form 2210.

E

You filed or are filing a joint return for either 2018 or 2019, but not for both years, and line 8 above is smaller than line 5 above. You must file page 1 of Form 2210, but you aren’t required to figure your penalty (unless box B, C, or D applies).

You filed or are filing a joint return for either 2018 or 2019, but not for both years, and line 8 above is smaller than line 5 above. You must file page 1 of Form 2210, but you aren’t required to figure your penalty (unless box B, C, or D applies).

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11744P |

Form 2210 (2019) |

Form 2210 (2019) |

Page 2 |

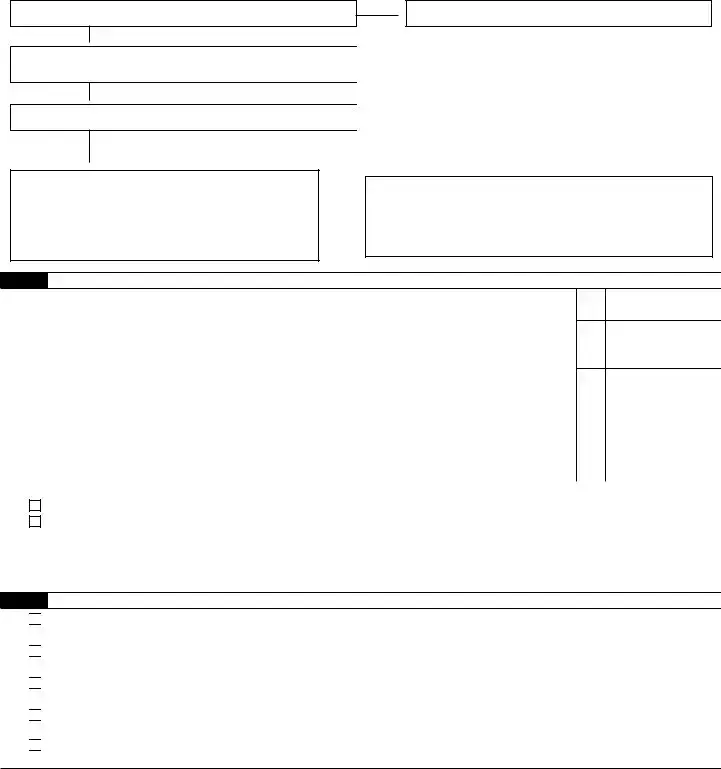

Part III Short Method

You can use the short method if:

• You made no estimated tax payments (or your only payments were withheld federal income tax), or

•You paid the same amount of estimated tax on each of the four payment due dates.

You must use the regular method (Part IV) instead of the short method if:

• You made any estimated tax payments late,

•You checked box C or D in Part II, or

•You are filing Form

Note: If any payment was made earlier than the due date, you can use the short method, but using it may cause you to pay a larger penalty than the regular method. If the payment was only a few days early, the difference is likely to be small.

10 |

Enter the amount from Form 2210, line 9 |

||

11 |

Enter the amount, if any, from Form 2210, line 6 |

11 |

|

12 |

Enter the total amount, if any, of estimated tax payments you made . . . |

12 |

|

13 |

Add lines 11 and 12 |

||

14Total underpayment for year. Subtract line 13 from line 10. If zero or less, stop; you don’t owe a

penalty. Don’t file Form 2210 unless you checked box E in Part II . . . . . . . . . . .

15 Multiply line 14 by 0.03398 . . . . . . . . . . . . . . . . . . . . . . . . .

16• If the amount on line 14 was paid on or after 4/15/20, enter

•If the amount on line 14 was paid before 4/15/20, make the following computation to find the amount to enter on line 16.

Amount on |

|

Number of days paid |

|

line 14 |

× |

before 4/15/20 |

× 0.00014 |

17Penalty. Subtract line 16 from line 15. Enter the result here and on Form 1040 or Form

Don’t file Form 2210 unless you checked a box in Part II . . . . . . . . . . . . .

10

13

14

15

16

17

Form 2210 (2019)

Form 2210 (2019) |

|

|

|

|

Page 3 |

||

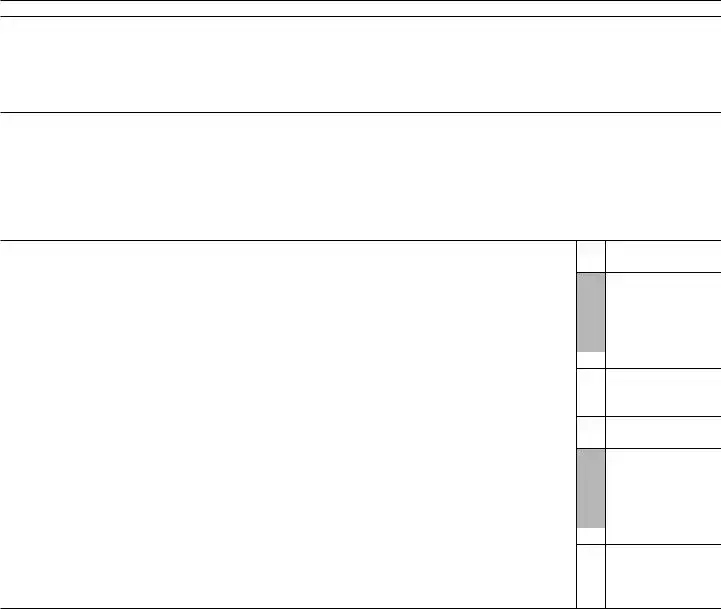

Part IV |

Regular Method (See the instructions if you are filing Form |

|

|||||

Section |

|

|

Payment Due Dates |

|

|||

|

(a) |

(b) |

(c) |

(d) |

|||

|

|

|

|

4/15/19 |

6/15/19 |

9/15/19 |

1/15/20 |

18 Required installments. If box C in Part II applies, |

|

|

|

|

|

||

enter the amounts from Schedule AI, line 27. |

|

|

|

|

|

||

Otherwise, enter 25% (0.25) of line 9, Form 2210, in |

|

|

|

|

|

||

each column |

|

18 |

|

|

|

|

|

19 Estimated tax paid and tax withheld (see the |

|

|

|

|

|

||

instructions). For column (a) only, also enter the |

|

|

|

|

|

||

amount from line 19 on line 23. If line 19 is equal to |

|

|

|

|

|

||

or more than line 18 for all payment periods, stop |

|

|

|

|

|

||

here; you don’t owe a penalty. Don’t file Form |

|

|

|

|

|

||

2210 unless you checked a box in Part II . . . |

19 |

|

|

|

|

||

Complete lines 20 through 26 of one column before going to line 20 of the next column.

20Enter the amount, if any, from line 26 in the previous

column |

. |

. . . |

. . . |

. |

. |

. |

20 |

|

|

21 Add lines 19 and 20 . |

. |

. . . |

. . . |

. |

. |

. |

21 |

|

|

22Add the amounts on lines 24 and 25 in the previous

column . . . . . . . . . . . . . . . 22

23Subtract line 22 from line 21. If zero or less, enter

19 . . . . . . . . . . . . . . . . . 23

24If line 23 is zero, subtract line 21 from line 22.

Otherwise, enter

25 |

Underpayment. If line 18 |

is equal to or more than |

|

|

|

line 23, subtract line 23 from line 18. Then go to line |

|

|

|

|

20 of the next column. Otherwise, go to line 26 . |

25 |

|

|

26 |

Overpayment. If line 23 |

is more than line 18, |

|

|

|

subtract line 18 from line 23. Then go to line 20 of |

|

|

|

|

the next column . . . |

. . . . . . . . . |

26 |

|

Section

27Penalty. Enter the total penalty from line 14 of the Worksheet for Form 2210, Part IV, Section

27

Form 2210 (2019)

Form 2210 (2019) |

Page 4 |

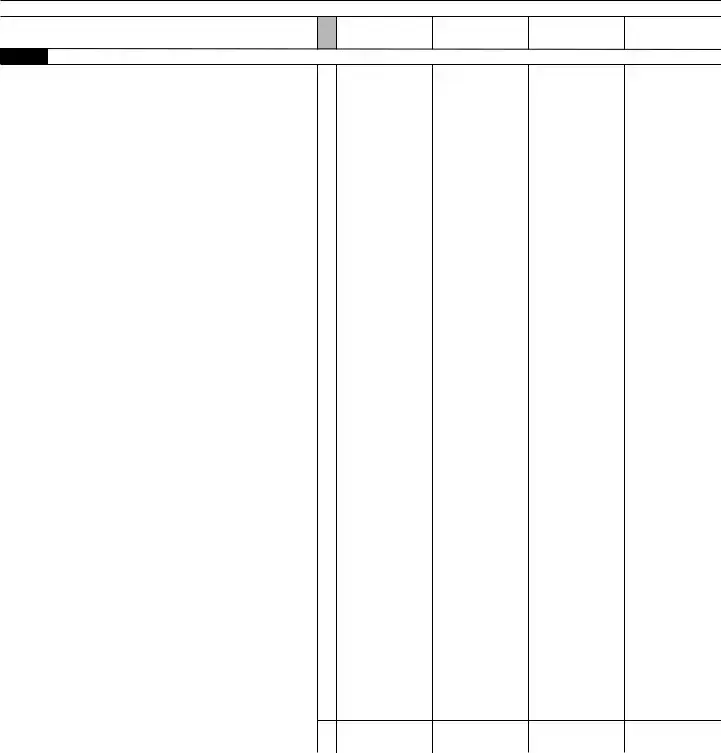

Schedule

Estates and trusts, don’t use the period ending dates shown to the right. Instead, use the following: 2/28/19, 4/30/19, 7/31/19, and 11/30/19.

(a)

(b)

(c)(d)

Part I Annualized Income Installments

1Enter your adjusted gross income for each period (see instructions). (Estates and trusts, enter your taxable

|

income without your exemption for each period.) . . |

1 |

|

|

|

|

2 |

Annualization amounts. (Estates and trusts, see instructions.) |

2 |

4 |

2.4 |

1.5 |

1 |

3 |

Annualized income. Multiply line 1 by line 2 . . . |

3 |

|

|

|

|

4 |

If you itemize, enter itemized deductions for the period |

|

|

|

|

|

|

shown in each column. All others enter |

|

|

|

|

|

|

line 7. Exception: Estates and trusts, skip to line 9 . |

4 |

|

|

|

|

5 |

Annualization amounts |

5 |

4 |

2.4 |

1.5 |

1 |

6 |

Multiply line 4 by line 5 |

6 |

|

|

|

|

7 |

In each column, enter the full amount of your standard |

|

|

|

|

|

|

deduction from Form 1040 or Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

students and business apprentices, see instructions.) . . |

7 |

|

|

|

|

8 |

Enter the larger of line 6 or line 7 |

8 |

|

|

|

|

9 |

Deduction for qualified business income. Estates and trusts: |

|

|

|

|

|

|

Subtract this amount from the amount on line 3, skip |

|

|

|

|

|

|

line 10, and enter the result on line 11 |

9 |

|

|

|

|

10 |

Add lines 8 and 9 |

10 |

|

|

|

|

11 |

Subtract line 10 from line 3 |

11 |

|

|

|

|

12 |

Form 1040, |

|

|

|

|

|

|

12 |

|

|

|

|

|

13 |

Subtract line 12 from line 11. If zero or less, enter |

13 |

|

|

|

|

14 |

Figure your tax on the amount on line 13 (see instructions) |

14 |

|

|

|

|

15 |

15 |

|

|

|

|

|

16 |

Enter other taxes for each payment period including, |

|

|

|

|

|

|

if applicable, Additional Medicare Tax and/or Net |

|

|

|

|

|

|

Investment Income Tax (see instructions) . . . . |

16 |

|

|

|

|

17 |

Total tax. Add lines 14, 15, and 16 |

17 |

|

|

|

|

18 |

For each period, enter the same type of credits as allowed |

|

|

|

|

|

|

on Form 2210, Part I, lines 1 and 3 (see instructions) . . |

18 |

|

|

|

|

19 |

Subtract line 18 from line 17. If zero or less, enter |

19 |

|

|

|

|

20 |

Applicable percentage |

20 |

22.5% |

45% |

67.5% |

90% |

21 |

Multiply line 19 by line 20 |

21 |

|

|

|

|

|

Complete lines |

|

|

|

|

|

|

going to line 22 of the next column. |

|

|

|

|

|

22 |

Enter the total of the amounts in all previous columns of line 27 |

22 |

|

|

|

|

23 |

Subtract line 22 from line 21. If zero or less, enter |

23 |

|

|

|

|

24 |

Enter 25% (0.25) of line 9 on page 1 of Form 2210 in each column |

24 |

|

|

|

|

25 |

Subtract line 27 of the previous column from line 26 of that column 25 |

|

|

|

|

|

26 |

Add lines 24 and 25 |

26 |

|

|

|

|

27Enter the smaller of line 23 or line 26 here and on

|

Form 2210, Part IV, line 18 |

27 |

|

|

|

|

|

Part II |

Annualized |

|

|||||

28 |

Net earnings from |

28 |

|

|

|

|

|

29 |

Prorated social security tax limit |

29 |

$33,225 |

$55,375 |

$88,600 |

$132,900 |

|

30 |

Enter actual wages for the period subject to social security tax |

|

|

|

|

|

|

|

or the 6.2% portion of the 7.65% railroad retirement (tier 1) tax. |

|

|

|

|

|

|

|

Exception: If you filed Form 4137 or Form 8919, see instructions |

30 |

|

|

|

|

|

31 |

Subtract line 30 from line 29. If zero or less, enter |

31 |

|

|

|

|

|

32 |

Annualization amounts |

32 |

0.496 |

0.2976 |

0.186 |

0.124 |

|

33 |

Multiply line 32 by the smaller of line 28 or line 31 . |

33 |

|

|

|

|

|

34 |

Annualization amounts |

34 |

0.116 |

0.0696 |

0.0435 |

0.029 |

|

35 |

Multiply line 28 by line 34 |

35 |

|

|

|

|

|

36 |

Add lines 33 and 35. Enter here and on line 15 above |

36 |

|

|

|

|

|

Form 2210 (2019)

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 2210 is used to determine whether a taxpayer owes a penalty for underpayment of estimated tax. |

| Eligibility | This form applies to individuals, estates, and trusts who owe taxes and fail to meet required payment thresholds. |

| Estimated Tax Payments | Taxpayers need to make estimated tax payments if they expect to owe $1,000 or more in taxes when they file their return. |

| Penalty Calculation | The penalty is calculated based on the amount of underpayment and the duration the payment was late. |

| Safe Harbor Rules | To avoid penalties, a taxpayer can pay 100% of the previous year's tax liability or 90% of the current year's liability. |

| Filing Deadline | Form 2210 must be filed with the annual tax return, usually due on April 15 or the next business day if it falls on a weekend. |

| State-Specific Considerations | State forms may vary. For example, California has its own Form 5805 for estimated tax underpayments, governed by California Revenue and Taxation Code. |

| Form Variations | There are two variations of Form 2210: a regular version and a simpler one for certain filers (Form 2210-F). |

| Interest Rates | The IRS sets interest rates for underpayment annually, which may change quarterly based on the federal short-term rate. |

| Payment Options | Taxpayers can pay owed taxes online, by phone, or through mailing a check or money order with their return. |

Filling out the IRS Form 2210 can seem daunting, but breaking it down into manageable steps can make the process smoother. After collecting the necessary information and ensuring accuracy, you'll be prepared to submit your form.

After completing these steps, make sure to keep a copy of the form for your records. It's always a good idea to stay organized and maintain documentation for your financial dealings with the IRS.

What is the IRS Form 2210?

The IRS Form 2210 is used to determine if you owe a penalty for underpaying your estimated tax. This form helps taxpayers calculate whether they have met the required annual payment of tax, which can help avoid unnecessary penalties when tax time arrives.

Who should file Form 2210?

If you find that you owe a penalty when you file your tax return, or if you did not pay enough tax during the year, you should consider filing Form 2210. It's particularly relevant for self-employed individuals, people with income from other sources, or those who had a significant change in income.

What are the common reasons for underpayment of tax?

There are several reasons one might underpay their taxes. This can happen due to a change in income, such as receiving a bonus or starting a new job where taxes are not withheld properly. Additionally, capital gains from investments or other sources of income can contribute to underpayment if not properly estimated and paid during the year.

How do I calculate my tax liability using Form 2210?

To calculate your tax liability, you will need to go through several steps. First, determine your total income for the year and subtract any adjustments to arrive at your taxable income. Then, apply the appropriate tax rates to calculate your overall tax liability. Finally, compare that amount to what you've already paid through withholding and estimated payments to see if you qualify for any penalties.

What are the penalties for underpayment?

The penalty for underpayment is typically calculated based on the amount of tax you owe and the length of time your payment was late. The IRS can charge interest on the unpaid amount and assess a penalty, which varies depending on how long you waited to pay. It’s essential to address these issues as soon as they are identified.

Can I avoid penalties by filing Form 2210?

Filing Form 2210 can help determine if you owe a penalty and, if so, you may qualify for an exception or a waiver. There are safe harbors where you can avoid penalties if you meet certain thresholds of payment, increasing your chances of reducing or eliminating additional costs.

Where do I send Form 2210?

The address to send Form 2210 will depend on whether you are enclosing a payment or not. If you are sending a payment, you can typically send it to the address listed on the form itself. If you are just filing the form without a payment, it may go to a different location based on your state of residence. Always check the latest IRS instructions for the most accurate information.

Can I amend Form 2210 once submitted?

Yes, if you find errors after you've submitted Form 2210, you can amend it. You would typically do this by filling out a new Form 2210 to correct any mistakes. However, be aware that the IRS may take some time to process amendments, so it's advisable to submit any necessary corrections as soon as possible.

Not understanding the purpose of the form. The IRS 2210 form is primarily used to determine whether you owe a penalty for underpayment of estimated taxes. Many individuals overlook this and may fill it out without assessing their actual tax situation.

Incorrectly calculating estimated tax payments. Some people fail to accurately calculate the amount they owed or how much they have already paid in estimated taxes. This can lead to underreporting or overreporting.

Forgetting to provide all necessary information. The form requires specific details about your income, tax payments, and any applicable credits. Omitting any critical information may delay processing and affect the outcome.

Not checking for applicable exceptions. Certain taxpayers might qualify for exceptions due to special circumstances like natural disasters or unexpected income scenarios. Neglecting to check if you qualify could lead to penalties.

Submitting the form late. The IRS has strict deadlines for filing tax forms. Missing these deadlines can result in penalties. Be sure to keep track of submission dates to avoid this mistake.

Failing to sign and date the form. It seems simple, but many forget this step. A missing signature or date will make the form invalid, leading to delays in processing.

Ignoring the form's instructions. Each section of the form comes with detailed instructions. Skipping these can lead to misinterpretation and errors in your submission.

The IRS Form 2210 is used to calculate underpayment penalties for individuals who do not pay enough tax throughout the year. When completing this form, several other documents may be needed for a comprehensive understanding of tax obligations. Below is a list of key forms often associated with Form 2210 that help taxpayers manage their finances more effectively.

These forms and documents assist individuals in effectively completing their tax responsibilities and understanding their financial standing. Utilizing them in conjunction with the IRS Form 2210 can provide a clearer picture of any potential penalties due to underpayment of taxes.

The IRS Form 1040 is the standard individual income tax return form used by taxpayers in the United States. Like Form 2210, it addresses tax issues but focuses on reporting income, deductions, and credits. Taxpayers fill out Form 1040 to determine their overall tax liability, while Form 2210 is specifically for calculating underpayment penalties. Both forms ultimately affect the taxpayer's financial standing with the IRS.

Form 4868 serves as an application for an automatic extension of time to file an individual tax return. Similar to Form 2210, it is used when a taxpayer anticipates being unable to meet the tax payment deadline. Both forms require attention to detail and address potential financial consequences. While Form 2210 deals with calculating underpayment, Form 4868 assures taxpayers they won't face immediate penalties for late filing.

Form 941 is used by employers to report payroll taxes withheld from employee wages. Like Form 2210, it can trigger penalties if proper payments are not made on time. Both forms help maintain compliance with IRS regulations, highlighting the need for timely payments and accurate reporting. Failure to submit either form correctly can lead to financial penalties for the individual or employer.

Form 1099-MISC is issued to report income from sources other than wages, salaries, and tips. Similar to Form 2210, it emphasizes the importance of accurate reporting in the tax process. While Form 2210 focuses on underpayment scenarios, Form 1099-MISC ensures that all income is reported to the IRS, thereby helping to prevent penalties related to unreported income.

The W-4 form is used by employees to inform employers of how much federal income tax to withhold from their paychecks. Like Form 2210, it plays a role in managing tax obligations. Correctly completing a W-4 can help prevent underpayment situations that may lead to the need for Form 2210. Both documents interconnectedly influence the amount of tax owed at year-end.

Schedule C is used by self-employed individuals to report income and expenses from their businesses. Similar to Form 2210, it addresses the taxpayer's liability to the IRS by calculating net income. Accurate completion of Schedule C is vital in avoiding underpayment and ensuring compliance. Both forms require taxpayers to provide thorough documentation and calculations to avoid penalties.

Form 8812 is used to claim the Additional Child Tax Credit. It relates to tax liability and potential penalties if not claimed correctly, much like Form 2210. Both documents are concerned with managing and optimizing tax credits to minimize financial burdens. Neglecting to claim credits can result in underpayment, which could lead to penalties noted on Form 2210.

Form 8880 allows taxpayers to claim a credit for contributions to retirement savings accounts. Similar to Form 2210, it addresses the impact of financial decisions on overall tax liability. Claims made via Form 8880 can influence tax obligations, potentially avoiding the need for additional payments that Form 2210 addresses. Both forms are essential for strategic tax planning.

The IRS Form 941-X is an adjusted quarterly payroll tax form. Much like Form 2210, it’s useful for correcting errors or adjustments to previous tax filings. Both forms require meticulous review and timely submission to avoid penalties. Submission of either form requires clarity to ensure compliance with IRS requirements and avoid financial repercussions.

Form 2063 relates to the return of a foreign individual to the United States. It parallels Form 2210 in that it ensures proper tax liability is calculated for non-residents. Both forms require detailed information to confirm tax obligations. That attention to detail is crucial for compliance, as any miscalculation can lead to penalties similar to those addressed in Form 2210.

When filling out the IRS 2210 form, keep these important tips in mind:

When considering the IRS Form 2210, it's essential to understand several important aspects. Here are six key takeaways to keep in mind:

Understanding these points can make the filing process smoother and ensure you handle your tax responsibilities effectively.