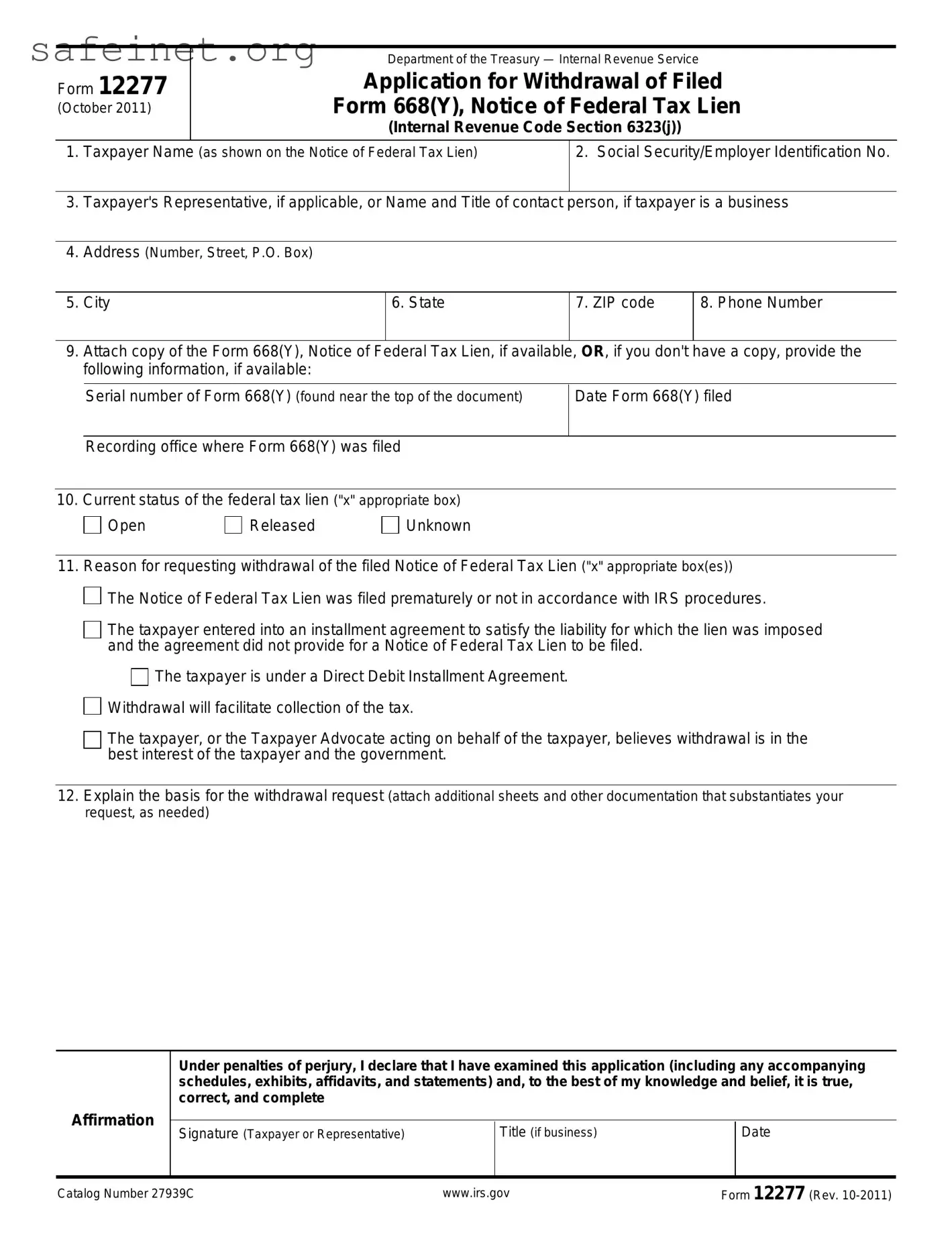

Understanding the nuances of tax regulations can sometimes feel like navigating a labyrinth. The IRS Form 12277 plays a significant role for taxpayers seeking relief from certain tax liabilities. Designed primarily for individuals who wish to withdraw or rescind a Notice of Federal Tax Lien, this form is essential for regaining financial peace of mind. By submitting Form 12277, taxpayers can request that the IRS remove a lien that may be affecting their credit or financial standing. Additionally, this form encompasses various important details, such as the taxpayer's information, the specifics regarding the tax liability, and the circumstances that necessitate the withdrawal. It’s crucial for individuals to present a compelling case when filling out this form, as the IRS reviews all applications carefully. In a world where understanding taxes can minimize stress, familiarity with the IRS Form 12277 empowers individuals to take control of their financial futures.

Form 12277

(October 2011)

Department of the Treasury — Internal Revenue Service

Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien

(Internal Revenue Code Section 6323(j))

1.Taxpayer Name (as shown on the Notice of Federal Tax Lien)

2. Social Security/Employer Identification No.

3.Taxpayer's Representative, if applicable, or Name and Title of contact person, if taxpayer is a business

4.Address (Number, Street, P.O. Box)

5. City

6. State

7. ZIP code

8. Phone Number

9.Attach copy of the Form 668(Y), Notice of Federal Tax Lien, if available, OR, if you don't have a copy, provide the following information, if available:

Serial number of Form 668(Y) (found near the top of the document)

Date Form 668(Y) filed

Recording office where Form 668(Y) was filed

10. Current status of the federal tax lien ("x" appropriate box)

Open

Released

Unknown

11. Reason for requesting withdrawal of the filed Notice of Federal Tax Lien ("x" appropriate box(es))

The Notice of Federal Tax Lien was filed prematurely or not in accordance with IRS procedures.

The Notice of Federal Tax Lien was filed prematurely or not in accordance with IRS procedures.

The taxpayer entered into an installment agreement to satisfy the liability for which the lien was imposed and the agreement did not provide for a Notice of Federal Tax Lien to be filed.

The taxpayer is under a Direct Debit Installment Agreement.

Withdrawal will facilitate collection of the tax.

The taxpayer, or the Taxpayer Advocate acting on behalf of the taxpayer, believes withdrawal is in the best interest of the taxpayer and the government.

The taxpayer, or the Taxpayer Advocate acting on behalf of the taxpayer, believes withdrawal is in the best interest of the taxpayer and the government.

12.Explain the basis for the withdrawal request (attach additional sheets and other documentation that substantiates your request, as needed)

Affirmation

Under penalties of perjury, I declare that I have examined this application (including any accompanying schedules, exhibits, affidavits, and statements) and, to the best of my knowledge and belief, it is true, correct, and complete

Signature (Taxpayer or Representative) |

Title (if business) |

Date |

|

|

|

Catalog Number 27939C |

www.irs.gov |

Form 12277 (Rev. |

Page 2 of 2

General Instructions

1.Complete the application. If the information you supply is not complete, it may be necessary for the IRS to obtain additional information before making a determination on the application.

Sections 1 and 2: Enter the taxpayer's name and Social Security Number (SSN) or Employer Identification Number (EIN) as shown on the Notice of Federal Tax Lien (NFTL).

Section 3: Enter the name of the person completing the application if it differs from the taxpayer's name in section 1 (for example, taxpayer representative). For business taxpayers, enter the name and title of person making the application. Otherwise, leave blank.

Sections 4 through 8: Enter current contact information of taxpayer or representative.

Section 9: Attach a copy of the NFTL to be withdrawn, if available. If you don't have a copy of the NFTL but have other information about the NFTL, enter that information to assist the IRS in processing your request.

Section 10: Check the box that indicates the current status of the lien.

"Open" means there is still a balance owed with respect to the tax liabilities listed on the NFTL. "Released" means the lien has been satisfied or is no longer enforceable.

"Unknown" means you do not know the current status of the lien.

Section 11: Check the box(es) that best describe the

reason(s) for the withdrawal request. NOTE: If you are requesting a withdrawal of a released NFTL, you generally should check the last box regarding the best interest provision.

Section 12: Provide a detailed explanation of the events or the situation to support your reason(s) for the withdrawal request. Attach additional sheets and supporting documentation, as needed.

Affirmation: Sign and date the application. If you are completing the application for a business taxpayer, enter your title in the business.

2.Mail your application to the IRS office assigned your account. If the account is not assigned or you are uncertain where it is assigned, mail your application to IRS, ATTN: Advisory Group Manager, in the area where you live or is the taxpayer's principal place of business. Use Publication 4235, Advisory Group Addresses, to determine the appropriate office.

3.Your application will be reviewed and, if needed, you may be asked to provide additional information. You will be contacted regarding a determination on your application.

a. If a determination is made to withdraw the NFTL, we will file a Form 10916(c), Withdrawal of Filed Notice of Federal Tax Lien, in the recording office where the original NFTL was filed and provide you a copy of the document for your records.

b. If the determination is made to not withdraw the NFTL, we will notify you and provide information regarding your rights to appeal the decision.

4.At your request, we will notify other interested parties of the withdrawal notice. Your request must be in writing and provide the names and addresses of the credit reporting agencies, financial institutions, and/or creditors that you want notified.

NOTE: Your request serves as our authority to release the notice of withdrawal information to the agencies, financial institutions, or creditors you have identified.

5.If, at a later date, additional copies of the withdrawal notice are needed, you must provide a written request to the Advisory Group Manager. The request must provide:

a.The taxpayer's name, current address, and taxpayer identification number with a brief statement authorizing the additional notifications;.

b.A copy of the notice of withdrawal, if available; and

c.A supplemental list of the names and addresses of any credit reporting agencies, financial institutions, or creditors to notify of the withdrawal of the filed Form 668(Y).

. |

Privacy Act Notice |

We ask for the information on this form to carry out the Internal Revenue laws of the United States. The primary purpose of this form is to apply for withdrawal of a notice of federal tax lien. The information requested on this form is needed to process your application and to determine whether the notice of federal tax lien can be withdrawn. You are not required to apply for a withdrawal; however, if you want the notice of federal tax lien to be withdrawn, you are required to provide the information requested on this form. Sections 6001, 6011, and 6323 of the Internal Revenue Code authorize us to collect this information. Section 6109 requires you to provide the requested identification numbers. Failure to provide this information may delay or prevent processing your application; providing false or fraudulent information may subject you to penalties.

Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

Catalog Number 27939C |

www.irs.gov |

Form 12277 (Rev. |

| Fact Name | Details |

|---|---|

| Purpose | Form 12277 is used to request the withdrawal of a federal tax lien. |

| Eligibility | Taxpayers must have paid their tax debt or made arrangements to settle the debt. |

| Filing Location | The completed form can be submitted to the local IRS office where the lien was filed. |

| Processing Time | Typically, it takes about 30 to 45 days for the IRS to process the form. |

| Required Information | Personal information, details of the tax lien, and the reason for withdrawal must be included. |

| Governing Law | The federal tax lien process is governed by the Internal Revenue Code, specifically Section 6323. |

| Form Availability | Form 12277 can be downloaded from the IRS website or obtained from an IRS office. |

| Limitations | Not all requests for withdrawal may be granted; the IRS evaluates them on a case-by-case basis. |

Filling out Form 12277 requires careful attention to detail to ensure that all necessary information is provided accurately. Once completed, the form should be submitted as per the instructions to move forward with your request.

What is IRS Form 12277?

IRS Form 12277 is used to request the withdrawal of a federal tax lien. Individuals may file this form when they have paid off their tax debt or when other circumstances warrant the release of the lien. A successfully processed Form 12277 can help individuals regain access to credit and make property transactions easier.

Who can file for IRS Form 12277?

Anyone who has an existing federal tax lien issued by the IRS can file Form 12277. This includes individuals who have settled their tax debts, or have entered into a payment plan. Additionally, the form can be used if the lien was filed in error or if the individual qualifies for lien withdrawal under specific conditions.

What are the requirements to use Form 12277?

To use Form 12277, the lien must be based on a tax liability that has been resolved. This might mean the outstanding balance due has been paid in full or legally settled. In some cases, the taxpayer may need to demonstrate that they meet certain criteria set by the IRS, such as financial hardship or a change in their circumstances.

How do I complete IRS Form 12277?

Filling out Form 12277 requires basic information like your name, address, and taxpayer identification number. You will also need to provide details about the tax lien you wish to withdraw, including the date it was filed and the location. Make sure to explain why you believe the lien should be withdrawn by including any relevant documentation that supports your case.

Where should I submit Form 12277?

Once completed, Form 12277 should be submitted to the office of the IRS that filed the lien. This is usually indicated on the lien notice you received. To ensure proper processing, be sure to send it to the correct address and consider sending it via certified mail to have proof of delivery.

How long does it take for the IRS to process Form 12277?

The IRS typically takes around 30 to 90 days to process Form 12277, though timelines can vary based on the complexity of the case or the current workload of the IRS. After the processing is complete, the IRS will send a confirmation letter indicating whether the withdrawal request was approved or denied.

What happens if my request for withdrawal is denied?

If the IRS denies your request to withdraw the lien, they will provide a reason for the denial. You can then either address the issues raised and submit another Form 12277 or request a reconsideration. It's also advisable to consult a tax professional to explore other options based on your situation.

Is there a fee associated with filing Form 12277?

There is no fee required for filing IRS Form 12277. This form is a service provided by the IRS to assist taxpayers in addressing issues related to federal tax liens. Submitting the form is free, making it easier for individuals-to seek relief from tax-related burdens.

Missing Information: Individuals often fail to provide all required details, such as their Social Security number or the tax year in question.

Incorrect Tax Year: Submitting the form for a tax year that does not match the IRS records can delay processing or result in rejection.

Not Signing the Form: Many overlook the necessity of signing the form, which is essential for submission validity.

Using Incorrect Mailing Address: Sending the form to the wrong address can cause significant delays, as it may not reach the intended department.

Omission of Payment Information: If applicable, individuals should include details about payments made towards the liability, which can affect the outcome.

Failure to Keep Copies: Not retaining a copy of the completed form for personal records can lead to issues if further clarification is needed later.

When working with the IRS 12277 form, which is used to request the withdrawal of a Notice of Federal Tax Lien, several other forms and documents may come into play. These documents can help support your request or ensure that all processes regarding your tax situation are handled correctly. Below is a list of such forms and documents.

These forms and documents play a vital role in supporting your request for a lien withdrawal and maintaining compliance with IRS regulations. Ensure that each form is filled out accurately to avoid any delays in processing your requests.

The IRS Form 12277, which is used to request the withdrawal of a federal tax lien, shares similarities with Form 4506, the Request for Copy of Tax Return. Both documents require taxpayers to provide personal information and details about the tax situation. They facilitate communication with the IRS and help taxpayers manage their records. While Form 4506 is focused on obtaining copies of past returns, Form 12277 directly addresses the removal of liens that may impact credit and financial dealings.

Another document similar to Form 12277 is Form 1040, the individual income tax return. Like Form 12277, the 1040 is a crucial tool in managing tax obligations. Both forms require accurate personal information and detailed financial data. The 1040 reflects an individual's tax liability, while Form 12277 addresses the legal status of unpaid tax debt, with an aim to rectify credit issues stemming from tax liens.

Form 941, the Employer's Quarterly Federal Tax Return, also relates to Form 12277 in certain ways. Both forms involve the IRS and tax reporting but cater to different audiences—individual taxpayers for the 12277 and employers for the 941. Completing both forms often requires meticulous calculation and disclosure of tax-related figures, maintaining an accurate record for compliance purposes.

Similar to the IRS Form 12277, Form 4868, which is the Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, allows taxpayers a means of dealing with their tax obligations. The primary similarity lies in the goal of managing tax-related issues; however, Form 4868 extends the deadline for filing a return, whereas Form 12277 directly seeks to address liens that may have already been imposed.

Additionally, Form 843, the Claim for Refund and Request for Abatement, offers another parallel. This document allows taxpayers to request a refund or abatement of certain taxes, penalties, or interest. Like Form 12277, it demands specific details concerning the taxpayer's situation and serves to mitigate tax burdens, albeit through different methods.

Form 2848, the Power of Attorney and Declaration of Representative, also shares similarities with Form 12277. Both forms serve as means of communication and authority in dealings with the IRS. While Form 2848 allows taxpayers to grant representatives the ability to act on their behalf, Form 12277 empowers individuals to take steps toward resolving tax liens specifically.

Form 9465, the Installment Agreement Request, complements the intentions of Form 12277 well. Taxpayers experiencing difficulty with tax debts can use Form 9465 to propose a payment plan. Like Form 12277, it addresses financial hardship and aims for resolution with the IRS, although it takes a different approach by allowing for gradual payment.

Form 13768, the Request for a Certificate of Release of Federal Tax Lien, directly aligns with the objectives of Form 12277. Both forms deal with lien-related issues, but while Form 12277 seeks to withdraw a lien, Form 13768 is used to confirm that a lien has been fully released. This makes it a critical step for taxpayers looking to clear their financial records.

Finally, Form 1099, especially the 1099-MISC, can resonate with the subject of Form 12277. While the 1099 series primarily serves to report income received throughout the year, it also represents aspects of financial responsibility and record-keeping. It's important for tax compliance, much like how Form 12277 aims to correct tax liabilities that can adversely affect one’s financial standing.

When filling out the IRS Form 12277, it's important to follow best practices to ensure your application is processed smoothly. Here are some dos and don'ts to keep in mind:

The IRS Form 12277, "Application for Withdrawal of Filed Form 668(Y)," is often surrounded by various misconceptions. Below are ten common misunderstandings about this form, along with clarifications.