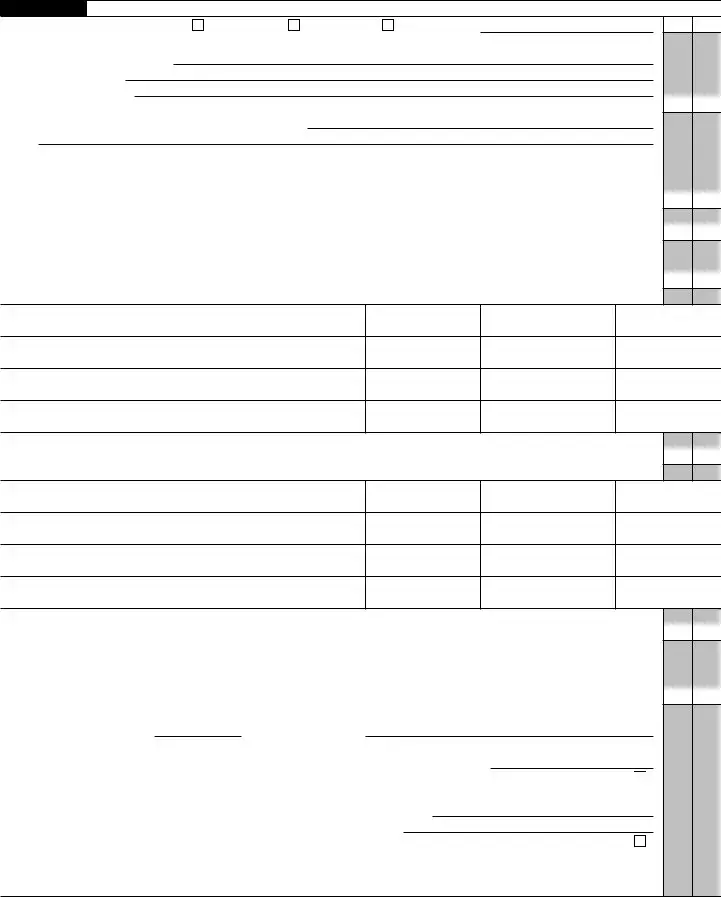

The IRS Form 1120 plays a crucial role in the financial landscape for corporations operating in the United States. This form is primarily used by C corporations to report their income, gains, losses, deductions, and credits, allowing the Internal Revenue Service to assess the corporation's tax liability. Filing this form is not just a legal obligation; it provides a comprehensive snapshot of a corporation's financial health over the tax year. Alongside reporting income, Form 1120 requires corporations to disclose various details, including the types of income earned, deductions taken for business expenses, and any tax credits claimed. Additionally, the form includes sections for reporting dividends paid to shareholders, which can impact both the corporation's tax situation and the shareholders' personal tax obligations. Understanding the nuances of Form 1120 is essential for corporate compliance and can also influence strategic financial planning. As corporations navigate their fiscal responsibilities, attention to detail in completing this form can help avoid potential penalties and ensure a smoother tax process.

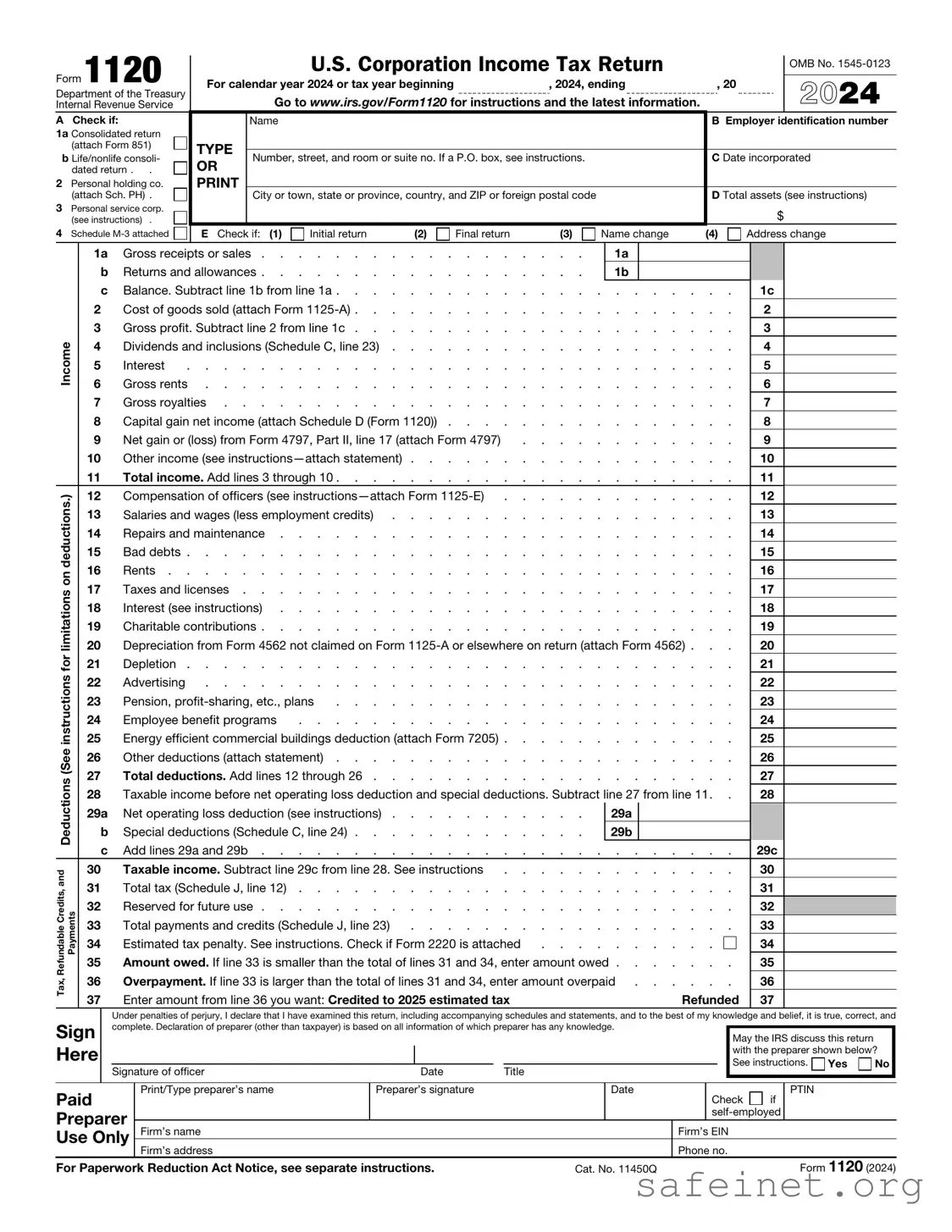

Form 1120

Department of the Treasury

Internal Revenue Service

A Check if:

1a Consolidated return (attach Form 851)

b Life/nonlife consoli- dated return . .

2Personal holding co.

(attach Sch. PH) .

3Personal service corp.

(see instructions) .

4 Schedule

|

|

U.S. Corporation Income Tax Return |

|

|

OMB No. |

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

For calendar year 2024 or tax year beginning |

|

, 2024, ending |

, 20 |

|

2024 |

||||

|

Go to www.irs.gov/Form1120 for instructions and the latest information. |

|

|

||||||

|

Name |

|

|

|

|

|

B Employer identification number |

||

TYPE |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

C Date incorporated |

|||||||

OR |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

D Total assets (see instructions) |

|||||||

|

|

||||||||

|

|

|

|

|

|

|

|

$ |

|

E Check if: (1) |

Initial return |

(2) |

Final return |

(3) |

Name change |

(4) |

Address change |

||

Income

Deductions (See instructions for limitations on deductions.) |

|

Refundable Credits, and |

Payments |

Tax, |

|

1a |

Gross receipts or sales |

|

1a |

|

|

||||||

b |

Returns and allowances |

|

1b |

|

|

||||||

c |

Balance. Subtract line 1b from line 1a |

. . . . . . . |

|

1c |

|||||||

2 |

Cost of goods sold (attach Form |

. . . . . . . |

|

2 |

|

||||||

3 |

Gross profit. Subtract line 2 from line 1c |

. . . . . . . |

|

3 |

|

||||||

4 |

Dividends and inclusions (Schedule C, line 23) |

. . . . . . . |

|

4 |

|

||||||

5 |

Interest |

. . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . . . |

|

5 |

|

||||

6 |

Gross rents |

. . . . . . . |

|

6 |

|

||||||

7 |

Gross royalties |

. . . . . . . |

|

7 |

|

||||||

8 |

Capital gain net income (attach Schedule D (Form 1120)) |

. . . . . . . |

|

8 |

|

||||||

9 |

Net gain or (loss) from Form 4797, Part II, line 17 (attach Form 4797) |

. . . . . |

|

. . . . . . . |

|

9 |

|

||||

10 |

Other income (see |

. . . . . . . |

|

10 |

|

||||||

11 |

Total income. Add lines 3 through 10 |

. . . . . . . |

|

11 |

|

||||||

12 |

Compensation of officers (see |

. . . . . . . |

|

12 |

|

||||||

13 |

Salaries and wages (less employment credits) |

. . . . . . . |

|

13 |

|

||||||

14 |

Repairs and maintenance |

. . . . . . . |

|

14 |

|

||||||

15 |

Bad debts |

. . . . . . . |

|

15 |

|

||||||

16 |

Rents |

. . . . . . . |

|

16 |

|

||||||

17 |

Taxes and licenses |

. . . . . . . |

|

17 |

|

||||||

18 |

Interest (see instructions) |

. . . . . . . |

|

18 |

|

||||||

19 |

Charitable contributions |

. . . . . . . |

|

19 |

|

||||||

20 |

Depreciation from Form 4562 not claimed on Form |

20 |

|

||||||||

21 |

Depletion |

. . . . . . . |

|

21 |

|

||||||

22 |

Advertising |

. . . . . . . |

|

22 |

|

||||||

23 |

Pension, |

. . . . . . . . . . . . . . . |

|

. . . . . . . |

|

23 |

|

||||

24 |

Employee benefit programs |

. . . . . . . . . . . . . . . . . |

|

. . . . . . . |

|

24 |

|

||||

25 |

Energy efficient commercial buildings deduction (attach Form 7205) |

. . . . . . . |

|

25 |

|

||||||

26 |

Other deductions (attach statement) |

. . . . . . . |

|

26 |

|

||||||

27 |

Total deductions. Add lines 12 through 26 |

. . . . . . . |

|

27 |

|

||||||

28 |

Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11. . |

28 |

|

||||||||

29a |

Net operating loss deduction (see instructions) |

|

29a |

|

|

|

|

||||

b |

Special deductions (Schedule C, line 24) |

|

29b |

|

|

|

|||||

c |

Add lines 29a and 29b |

. . . . . . . |

|

29c |

|||||||

30 |

Taxable income. Subtract line 29c from line 28. See instructions |

. . . . . . . |

|

30 |

|

||||||

31 |

Total tax (Schedule J, line 12) |

. . . . . . . |

|

31 |

|

||||||

32 |

Reserved for future use |

. . . . . . . |

|

32 |

|

||||||

33 |

Total payments and credits (Schedule J, line 23) |

. . . . . . . |

|

33 |

|

||||||

34 |

Estimated tax penalty. See instructions. Check if Form 2220 is attached . . . . |

. . . . . . |

|

34 |

|

||||||

35 |

Amount owed. If line 33 is smaller than the total of lines 31 and 34, enter amount owed |

. . . . . . . |

|

35 |

|

||||||

36 |

Overpayment. If line 33 is larger than the total of lines 31 and 34, enter amount overpaid |

|

36 |

|

|||||||

37 |

Enter amount from line 36 you want: Credited to 2025 estimated tax |

|

|

|

Refunded |

37 |

|

||||

Sign |

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and |

|||||||||||||

|

complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|

|

|

|

||||||||

|

|

|

|

May the IRS discuss this return |

|

||||||||||

Here |

|

|

|

|

|

|

|

|

|

|

|

with the preparer shown below? |

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

See instructions. Yes |

No |

||

|

|

Signature of officer |

|

Date |

|

Title |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

|

Print/Type preparer’s name |

Preparer’s signature |

|

|

Date |

|

Check |

if |

PTIN |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

Preparer |

|

|

|

|

|

|

|

|

|

||||||

Firm’s name |

|

|

|

|

|

Firm’s EIN |

|

|

|

||||||

Use Only |

|

|

|

|

|

|

|

|

|||||||

Firm’s address |

|

|

|

|

|

Phone no. |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

Cat. No. 11450Q |

|

|

|

|

|

Form 1120 (2024) |

|||||||

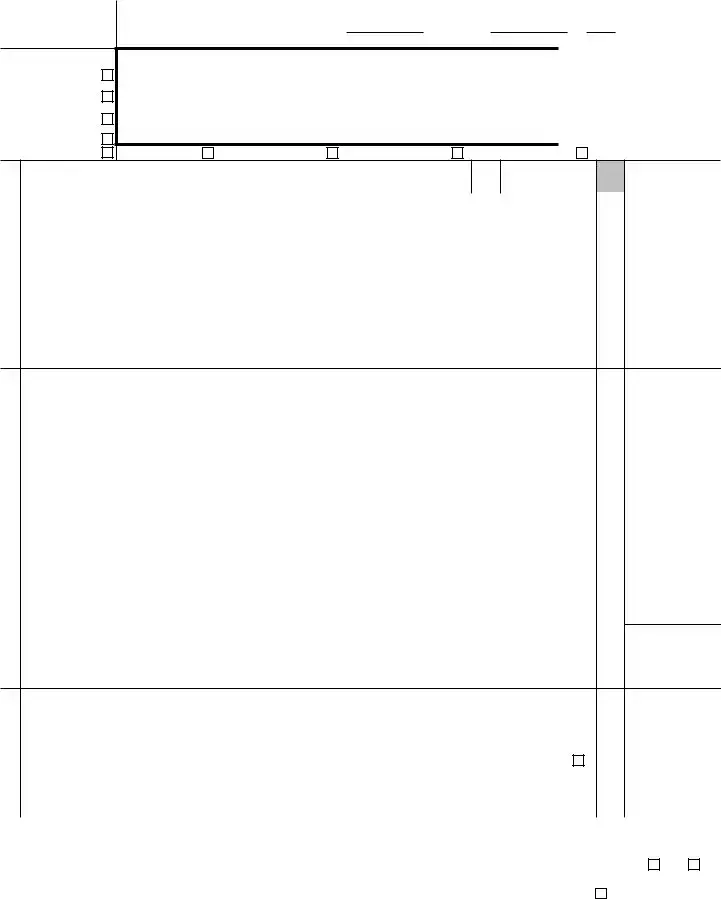

Form 1120 (2024) |

|

|

Page 2 |

|

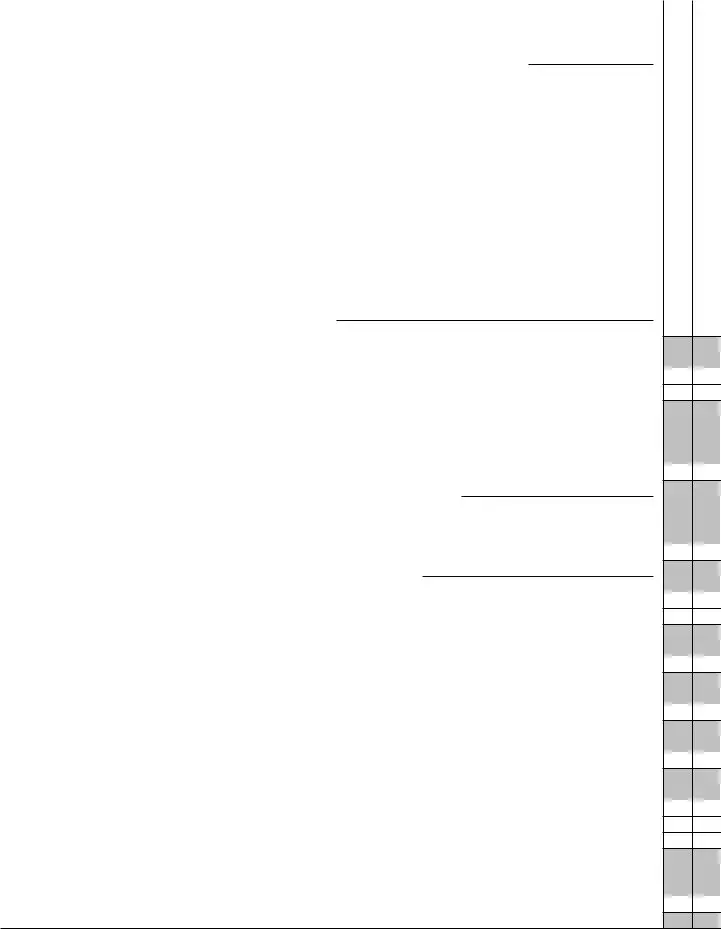

Schedule C |

Dividends, Inclusions, and Special Deductions |

(a) Dividends and |

(b) % |

(c) Special deductions |

|

(see instructions) |

inclusions |

(a) × (b) |

|

|

|

|||

1Dividends from

stock) |

50 |

2Dividends from

|

stock) |

65 |

|

|

See |

3 |

Dividends on certain |

instructions |

4 |

Dividends on certain preferred stock of |

23.3 |

5 |

Dividends on certain preferred stock of |

26.7 |

6 |

Dividends from |

50 |

7 |

Dividends from |

65 |

8 |

Dividends from wholly owned foreign subsidiaries |

100 |

|

|

See |

9 |

Subtotal. Add lines 1 through 8. See instructions for limitations |

instructions |

10Dividends from domestic corporations received by a small business investment

|

company operating under the Small Business Investment Act of 1958 |

100 |

11 |

Dividends from affiliated group members |

100 |

12 |

Dividends from certain FSCs |

100 |

13

|

corporation (excluding hybrid dividends) (see instructions) |

|

100 |

|

|

14 |

Dividends from foreign corporations not included on line 3, 6, 7, 8, 11, 12, or 13 |

|

|

||

|

(including any hybrid dividends) |

|

|

|

|

15 |

Reserved for future use |

|

|

|

|

16a |

Subpart F inclusions derived from the sale by a controlled foreign corporation (CFC) of |

|

|

||

|

the stock of a |

100 |

|

||

|

(see instructions) |

|

|

||

b |

Subpart F inclusions derived from hybrid dividends of tiered corporations (attach Form(s) |

|

|

||

|

5471) (see instructions) |

|

|

|

|

c |

Other inclusions from CFCs under subpart F not included on line 16a, 16b, or 17 (attach |

|

|

||

|

Form(s) 5471) (see instructions) |

|

|

||

17 |

Global Intangible |

18 |

|

19 |

|

20 |

Other dividends |

21 |

Deduction for dividends paid on certain preferred stock of public utilities . . . . |

22 |

Section 250 deduction (attach Form 8993) |

23Total dividends and inclusions. Add column (a), lines 9 through 20. Enter here and on page 1, line 4 . . . . . . . . . . . . . . . . . . . . . .

24 |

Total special deductions. Add column (c), lines 9 through 22. Enter here and on page 1, line 29b |

Form 1120 (2024)

Form 1120 (2024) |

|

|

|

|

|

|

Page 3 |

|

Schedule J |

Tax Computation and Payment (see instructions) |

|

|

|

|

|

|

|

1a |

Income tax (see instructions) |

|

1a |

|

|

|

|

|

b |

Tax from Form |

|

1b |

|

|

|

|

|

c |

Section 1291 tax from Form 8621 |

|

1c |

|

|

|

|

|

d |

Tax adjustment from Form 8978 |

|

1d |

|

|

|

|

|

e |

Additional tax under section 197(f) |

|

1e |

|

|

|

|

|

f |

Base erosion minimum tax from Form 8991 |

|

1f |

|

|

|

|

|

g |

Amount from Form 4255, Part I, line 3, column (q) |

|

1g |

|

|

|

|

|

z |

Other chapter 1 tax |

|

1z |

|

|

|

|

|

2 |

Total income tax. Add lines 1a through 1z |

. . . . . . . . |

|

2 |

|

|||

3 |

Corporate alternative minimum tax from Form 4626, Part II, line 13 (attach Form 4626) . |

. . . . . . . . |

|

3 |

|

|||

4 |

Add lines 2 and 3 |

. . . . . . . . |

|

4 |

|

|||

5a |

Foreign tax credit (attach Form 1118) |

|

5a |

|

|

|

|

|

b |

Credit from Form 8834 (see instructions) |

|

5b |

|

|

|

||

c |

General business credit (see |

|

5c |

|

|

|

||

d |

Credit for prior year minimum tax (attach Form 8827) |

|

5d |

|

|

|

||

e |

Bond credits from Form 8912 |

|

5e |

|

|

|

||

f |

Adjustment from Form 8978 |

|

5f |

|

|

|

||

6 |

Total credits. Add lines 5a through 5f |

. . . . . . . . |

|

6 |

|

|||

7 |

Subtract line 6 from line 4 |

. . . . . . . . |

|

7 |

|

|||

8 |

Personal holding company tax (attach Schedule PH (Form 1120)) |

. . . . . . . . |

|

8 |

|

|||

9a |

Amount from Form 4255, Part I, line 3, column (r) |

|

9a |

|

|

|

|

|

b |

Recapture of |

|

9b |

|

|

|

||

c |

Completed |

|

9c |

|

|

|

||

d |

Interest due under the |

|

9d |

|

|

|

||

e |

Alternative tax on qualifying shipping activities (attach Form 8902) |

|

9e |

|

|

|

||

f |

Interest/tax due under section 453A(c) |

|

9f |

|

|

|

||

g |

Interest/tax due under section 453(l) |

|

9g |

|

|

|

||

z |

Other (see |

|

9z |

|

|

|

||

10 |

Total. Add lines 9a through 9z |

. . . . . . . . |

|

10 |

|

|||

11a |

Total tax before deferred taxes. Add lines 7, 8, and 10 |

|

11a |

|

|

|||

bDeferred tax on the corporation's share of undistributed earnings of a qualified electing

|

fund |

|

11b |

|

|

|

||

c |

Deferred LIFO recapture tax (section 1363(d)) |

. . . . . . . . . . . . |

|

11c |

|

|

|

|

12 |

Total tax. Subtract the sum of lines 11b and 11c from 11a. Enter here and on page 1, line 31 |

12 |

|

|

||||

13 |

Preceding year’s overpayment credited to the current year |

. . . . . . . . |

|

13 |

|

|

||

14 |

Current year’s estimated tax payments |

. . . . . . . . |

|

14 |

|

|

||

15 |

Current year’s refund applied for on Form 4466 |

. . . . . . . . |

|

15 |

( |

) |

||

16 |

Reserved for future use |

. . . . . . . . |

|

16 |

|

|

||

17 |

Tax deposited with Form 7004 |

. . . . . . . . |

|

17 |

|

|

||

18 |

Withholding (see instructions) |

. . . . . . . . |

|

18 |

|

|

||

19 |

Total payments. Combine lines 13 through 18 |

. . . . . . . . |

|

19 |

|

|

||

20Refundable credits from:

a |

Form 2439 |

20a |

b |

Form 4136 |

20b |

cCredit for tax withheld under chapter 3 or 4 from Form

|

8288 (attach the applicable form) |

20c |

|

|

z |

Other (attach |

20z |

|

|

21 |

Total credits. Add lines 20a through 20z |

. . . . . . . |

|

21 |

22 |

Elective payment election amount from Form 3800 |

. . . . . . . |

|

22 |

23 |

Total payments and credits. Add lines 19, 21, and 22. Enter here and on page 1, line 33 . |

. . . . . . . |

|

23 |

Form 1120 (2024)

Form 1120 (2024) |

Page 4 |

Schedule K Other Information (see instructions)

1 |

Check accounting method: a |

Cash |

b |

Accrual |

c |

Other (specify) |

2See the instructions and enter the: a Business activity code no.

b Business activity c Product or service

3 Is the corporation a subsidiary in an affiliated group or a

If “Yes,” enter name and EIN of the parent corporation

4At the end of the tax year:

aDid any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or

corporation’s stock entitled to vote? If “Yes,” complete Part I of Schedule G (Form 1120) (attach Schedule G) . . . . . .

bDid any individual or estate own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all

classes of the corporation’s stock entitled to vote? If “Yes,” complete Part II of Schedule G (Form 1120) (attach Schedule G) .

5At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote of any foreign or domestic corporation not included on Form 851, Affiliations Schedule? For rules of constructive ownership, see instructions If “Yes,” complete (i) through (iv) below.

Yes No

(i)Name of Corporation

(ii)Employer

Identification Number

(if any)

(iii)Country of Incorporation

(iv)Percentage Owned in Voting

Stock

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions If “Yes,” complete (i) through (iv) below.

(i)Name of Entity

(ii)Employer

Identification Number

(if any)

(iii)Country of Organization

(iv)Maximum

Percentage Owned in Profit, Loss, or Capital

6During this tax year, did the corporation pay dividends (other than stock dividends and distributions in exchange for stock) in

excess of the corporation’s current and accumulated earnings and profits? See sections 301 and 316 . . . . . . . .

If “Yes,” file Form 5452, Corporate Report of Nondividend Distributions. See the instructions for Form 5452. If this is a consolidated return, answer here for the parent corporation and on Form 851 for each subsidiary.

7At any time during this tax year, did one foreign person own, directly or indirectly, at least 25% of the total voting power of all classes of the corporation’s stock entitled to vote or at least 25% of the total value of all classes of the corporation’s stock? .

For rules of attribution, see section 318. If “Yes,” enter:

(a) Percentage owned |

and (b) Owner’s country |

(c) The corporation may have to file Form 5472, Information Return of a 25%

8 Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . . . . If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

9Enter the amount of

10Enter the number of shareholders at the end of the tax year (if 100 or fewer)

11 |

If the corporation has an NOL for the tax year and is electing to forego the carryback period, check here (see instructions) . |

|

If the corporation is filing a consolidated return, the statement required by Regulations section |

|

or the election will not be valid. |

12Enter the available NOL carryover from prior tax years (do not reduce it by any deduction reported on page 1, line 29a) $

Form 1120 (2024)

Form 1120 (2024) |

|

|

Page 5 |

|

Schedule K |

Other Information (continued from page 4) |

|

|

|

13 |

Are the corporation’s total receipts (page 1, line 1a, plus lines 4 through 10) for the tax year and its total assets at the end of |

Yes |

No |

|

|

|

|||

|

the tax year less than $250,000? |

|

|

|

|

If “Yes,” the corporation is not required to complete Schedules L, |

|

|

|

|

distributions and the book value of property distributions (other than cash) made during this tax year $ |

|

|

|

14 |

Is the corporation required to file Schedule UTP (Form 1120), Uncertain Tax Position Statement? See instructions . . . . |

|

|

|

|

If “Yes,” complete and attach Schedule UTP. |

|

|

|

15a |

Did the corporation make any payments that would require it to file Form(s) 1099? |

|

|

|

b |

If “Yes,” did or will the corporation file required Form(s) 1099? |

|

|

|

16 |

During this tax year, did the corporation have an |

|

|

|

|

its own stock? |

|

|

|

17 |

During or subsequent to this tax year, but before the filing of this return, did the corporation dispose of more than 65% (by |

|

|

|

|

value) of its assets in a taxable, |

|

|

|

18 |

Did this corporation receive assets in a section 351 transfer in which any of the transferred assets had a fair market basis or |

|

|

|

|

fair market value of more than $1 million? |

|

|

|

19 |

During this corporation’s tax year, did the corporation make any payments that would require it to file Forms 1042 and |

|

|

|

|

under chapter 3 (sections 1441 through 1464) or chapter 4 (sections 1471 through 1474) of the Code? |

|

|

|

20 |

Is the corporation operating on a cooperative basis? |

|

|

|

21 |

During this tax year, did the corporation pay or accrue any interest or royalty for which the deduction is not allowed under |

|

|

|

|

section 267A? See instructions |

|

|

|

|

If “Yes,” enter the total amount of the disallowed deductions $ |

|

|

|

22Does this corporation have gross receipts of at least $500 million in any of the 3 preceding tax years? (See sections 59A(e)(2) and (3).) If “Yes,” complete and attach Form 8991.

23Did the corporation have an election under section 163(j) for any real property trade or business or any farming business in

|

effect during this tax year? See instructions |

24 |

Does the corporation satisfy one or more of the following? If “Yes,” complete and attach Form 8990. See instructions . . . |

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $30 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense.

25 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

. . . . . . . . . . . . . |

|

If “Yes,” enter amount from Form 8996, line 15 |

. $ |

26Since December 22, 2017, did a foreign corporation directly or indirectly acquire substantially all of the properties held directly or indirectly by the corporation, and was the ownership percentage (by vote or value) for purposes of section 7874 greater than 50% (for example, the shareholders held more than 50% of the stock of the foreign corporation)? If “Yes,” list the ownership

percentage by vote and by value. See instructions . . . . . . . . . . . . . . . . . . . . . . .

Percentage: By Vote |

|

By Value |

27At any time during this tax year, did the corporation (a) receive a digital asset (as a reward, award, or payment for property or

|

services); or (b) sell, exchange, or otherwise dispose of a digital asset (or a financial interest in a digital asset)? See instructions . |

28 |

Is the corporation a member of a controlled group? |

|

If “Yes,” attach Schedule O (Form 1120). See instructions. |

29Corporate Alternative Minimum Tax:

a Was the corporation an applicable corporation under section 59(k)(1) in any prior tax year? . . . . . . . . . . .

If “Yes,” go to question 29b. If “No,” skip to question 29c.

bIs the corporation an applicable corporation under section 59(k)(1) in the current tax year because the corporation was an

applicable corporation in the prior tax year? . . . . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” complete and attach Form 4626. If “No,” continue to question 29c.

cDoes the corporation meet the requirements of the safe harbor method as provided under section 59(k)(3)(A) for the current tax

year? See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If “No,” complete and attach Form 4626. If “Yes,” the corporation is not required to file Form 4626.

30Is the corporation required to file Form 7208 relating to the excise tax on repurchase of corporate stock (see instructions):

a |

Under the rules for stock repurchased by a covered corporation (or stock acquired by its specified affiliate)? |

b |

Under the applicable foreign corporation rules? |

c |

Under the covered surrogate foreign corporation rules? |

|

If “Yes” to either 30a, 30b, or 30c, complete Form 7208, Excise Tax on Repurchase of Corporate Stock. See the Instructions |

|

for Form 7208. |

31Is this a consolidated return with gross receipts or sales of $1 billion or more and a subchapter K basis adjustment, as

described in the instructions, of $10 million or more? . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” attach a statement. See instructions.

Form 1120 (2024)

Form 1120 (2024) |

|

|

|

|

|

|

|

|

|

|

|

|

Page 6 |

||

Schedule L |

|

Balance Sheets per Books |

|

|

Beginning of tax year |

|

|

End of tax year |

|

||||||

|

|

|

Assets |

|

|

|

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

||||

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less allowance for bad debts . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|||||

4 |

U.S. government obligations |

. . . . . |

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

|

|

|

|

|

|

|

|

|

|||||

6 |

Other current assets (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

||||

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

||||

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

||||

10a |

Buildings and other depreciable assets . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depreciation . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depletion . . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|||||

13a |

Intangible assets (amortizable only) |

. . . |

|

|

|

|

|

|

|

|

|

|

|||

b |

Less accumulated amortization . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|||||

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|||||

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

||||

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

||||

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

||||

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

||||

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

||||

22 |

Capital stock: |

a Preferred stock . . . . |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

b Common stock . . . . |

|

|

|

|

|

|

|

|

|

|

||

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

||||

24 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

25 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

26 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

27 |

Less cost of treasury stock |

|

|

|

|

( |

) |

|

|

( |

) |

||||

28 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|||||

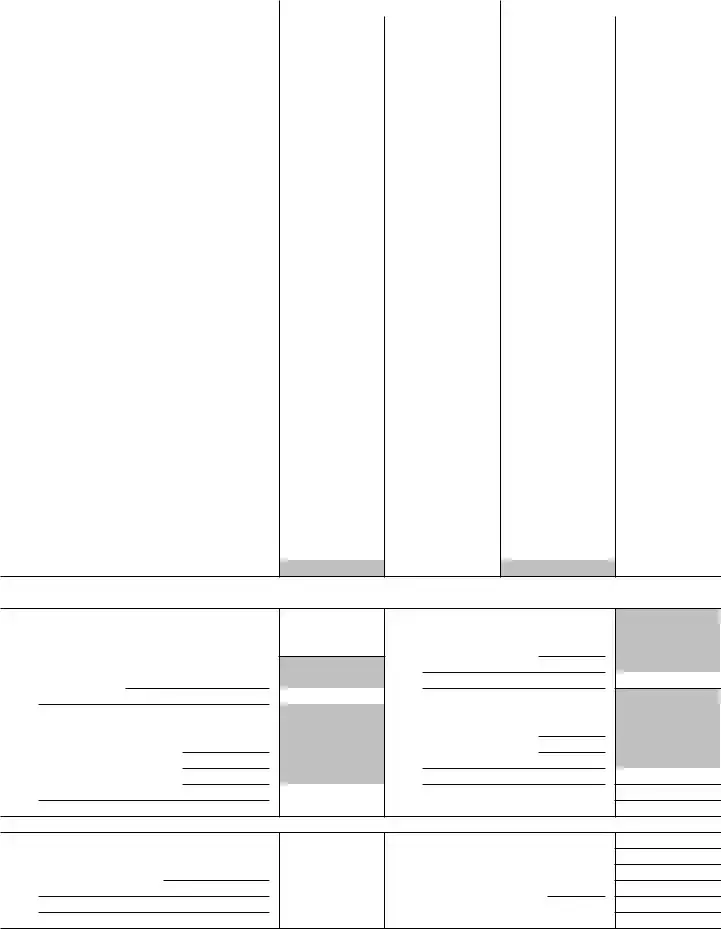

Schedule

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books |

7 |

Income recorded on books this year |

|

2 |

Federal income tax per books |

|

|

not included on this return (itemize): |

3 |

Excess of capital losses over capital gains . |

|

|

|

4Income subject to tax not recorded on books this year (itemize):

|

|

|

8 |

|

Deductions on this return not charged |

5 |

Expenses recorded on books this year not |

|

against book income this year (itemize): |

||

|

deducted on this return (itemize): |

a |

Depreciation . . $ |

||

a |

Depreciation . . . . $ |

b |

Charitable contributions $ |

||

bCharitable contributions . $

cTravel and entertainment . $

|

|

|

9 |

Add lines 7 and 8 |

6 |

Add lines 1 through 5 |

10 |

Income (page 1, line |

|

Schedule

1 |

Balance at beginning of year |

5 |

Distributions: a Cash |

||

2 |

Net income (loss) per books |

|

|

|

b Stock . . . . |

3 |

Other increases (itemize): |

|

|

|

c Property . . . . |

|

|

|

6 |

Other decreases (itemize): |

|

|

|

|

7 |

Add lines 5 and 6 |

|

4 |

Add lines 1, 2, and 3 |

8 |

Balance at end of year (line 4 less line 7) |

||

Form 1120 (2024)

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1120 is used by corporations to report income, gains, losses, deductions, and credits. |

| Filing Requirement | All domestic corporations must file Form 1120 annually, regardless of income. |

| Due Date | Form 1120 is typically due on the 15th day of the fourth month after the end of the corporation's tax year. |

| Tax Rate | The corporate tax rate is a flat 21% on taxable income, as of the Tax Cuts and Jobs Act of 2017. |

| State-Specific Forms | Many states require their own corporate tax forms. For example, California uses Form 100, governed by California Revenue and Taxation Code. |

| Extensions | Corporations can file for an extension using Form 7004, allowing an additional six months to file. |

| Estimated Payments | Corporations may need to make estimated tax payments throughout the year, typically quarterly. |

| Penalties | Failure to file or pay taxes on time can result in penalties, including fines and interest on unpaid taxes. |

Completing the IRS 1120 form involves a series of steps to ensure accurate reporting of corporate income, deductions, and credits. After filling out the form, it will need to be submitted to the IRS by the designated deadline. Below are the steps to follow when completing the form.

What is the IRS 1120 form?

The IRS 1120 form is the U.S. Corporation Income Tax Return. It is used by C corporations to report their income, gains, losses, deductions, and credits, as well as to calculate their tax liability. This form is essential for corporations to fulfill their federal tax obligations.

Who needs to file Form 1120?

Any corporation that is classified as a C corporation must file Form 1120. This includes domestic corporations that are not S corporations or other types of entities. If your business operates as a corporation and earns income, you will likely need to file this form.

When is Form 1120 due?

Form 1120 is typically due on the 15th day of the fourth month after the end of your corporation's tax year. For most corporations that follow the calendar year, this means the form is due on April 15. If the due date falls on a weekend or holiday, the deadline is extended to the next business day.

What information is required on Form 1120?

Form 1120 requires various pieces of information, including your corporation's name, address, and Employer Identification Number (EIN). You'll also need to report your corporation's income, deductions, and tax credits. Additionally, you must include details about any dividends paid and other relevant financial data.

Can I e-file Form 1120?

Yes, you can e-file Form 1120. The IRS encourages electronic filing as it is faster and more efficient. Many tax software programs support e-filing for corporations, making it easier to submit your return accurately and on time.

What happens if I miss the deadline for filing Form 1120?

If you miss the deadline, your corporation may face penalties and interest on any unpaid taxes. The IRS can impose a failure-to-file penalty, which can be significant. It's important to file as soon as possible, even if you cannot pay the full amount owed.

Are there any deductions available on Form 1120?

Yes, Form 1120 allows corporations to claim various deductions that can reduce taxable income. Common deductions include operating expenses, salaries and wages, rent, and certain business-related travel expenses. Understanding which deductions apply to your corporation can help minimize your tax liability.

What is the difference between Form 1120 and Form 1120-S?

Form 1120 is for C corporations, while Form 1120-S is specifically for S corporations. The main difference lies in how these entities are taxed. C corporations are taxed at the corporate level, while S corporations pass income directly to shareholders, who report it on their personal tax returns. This distinction affects how each form is filled out and the tax implications for the business owners.

Where can I find help with completing Form 1120?

There are several resources available to help you complete Form 1120. The IRS website provides detailed instructions for the form, including guidelines for specific sections. Additionally, you may consider consulting a tax professional who can offer personalized assistance based on your corporation's unique circumstances.

Failing to include all income sources. Many businesses overlook certain revenue streams, which can lead to discrepancies in reported income.

Incorrectly calculating deductions. Taxpayers often misinterpret what qualifies as a deductible expense, resulting in either over- or under-reporting.

Not using the correct tax year. Some filers mistakenly apply the wrong fiscal year, leading to confusion and potential penalties.

Omitting necessary schedules. Certain businesses may need to attach additional forms or schedules, which, if missing, can delay processing.

Providing inaccurate information. Errors in names, addresses, or Employer Identification Numbers (EIN) can cause significant issues.

Neglecting to sign and date the form. A common oversight, failing to sign can render the submission invalid.

Not keeping adequate records. Insufficient documentation can lead to challenges if the IRS questions any reported figures.

Missing deadlines. Timely submission is crucial. Late filings can incur penalties and interest on unpaid taxes.

The IRS Form 1120 is used by corporations to report their income, gains, losses, deductions, and credits. When filing this form, there are several other documents and forms that may be required to provide additional information or to comply with various regulations. Here’s a list of commonly used forms and documents that often accompany the IRS Form 1120:

Filing the IRS Form 1120 can be complex, and including the right additional documents is essential for accuracy and compliance. Each of these forms serves a specific purpose and helps provide a complete picture of the corporation's financial situation. It is advisable to consult with a tax professional or accountant to ensure all necessary documents are included and correctly filled out.

The IRS Form 1065 is similar to Form 1120 in that both are used to report income, deductions, and other financial information to the IRS. However, while Form 1120 is specifically designed for corporations, Form 1065 is used by partnerships. Partnerships do not pay income tax at the entity level; instead, they pass their profits and losses through to the individual partners. This means that each partner reports their share of the partnership's income on their personal tax returns, making the reporting process slightly different yet still focused on transparency and accuracy in financial reporting.

Form 1120-S is another closely related document, intended for S corporations. Like Form 1120, it is used to report income, gains, losses, deductions, and credits. The key difference lies in the tax treatment; S corporations pass their income directly to shareholders, avoiding double taxation. This form is crucial for S corporations to maintain their status and ensure that income is reported correctly by each shareholder on their personal tax returns, similar to how partnerships operate under Form 1065.

Form 990 is utilized by tax-exempt organizations, including charities and non-profits. While Form 1120 focuses on taxable entities, Form 990 serves to provide transparency regarding the financial activities of non-profits. Both forms require detailed financial information, but Form 990 emphasizes accountability to the public and donors, showcasing how funds are used in furtherance of the organization’s mission, rather than profit generation.

Form 1040 is the individual income tax return that most Americans file. Although it differs significantly from Form 1120 in terms of the entity type it addresses, both forms share the goal of reporting income and calculating tax liability. Individuals report their earnings, deductions, and credits on Form 1040, while corporations do so on Form 1120. The similarities lie in the structure and purpose of reporting financial information to the IRS.

Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. While it targets payroll taxes rather than corporate income, both Form 941 and Form 1120 require meticulous record-keeping and accurate reporting. Employers must ensure that they comply with tax laws, just as corporations must do when filing their annual returns, highlighting the importance of financial responsibility in different contexts.

Lastly, Form 1099 is a series of forms used to report various types of income other than wages, salaries, and tips. While Form 1120 focuses on corporate income, Form 1099 serves to report payments made to independent contractors, freelancers, and other non-employees. Both forms aim to ensure that income is accurately reported to the IRS, but they cater to different types of financial transactions and entities, showcasing the diverse landscape of tax reporting requirements.

When completing the IRS Form 1120, it is essential to approach the process with care and attention to detail. Below are some important guidelines to follow, as well as common pitfalls to avoid.

By adhering to these guidelines, you can navigate the process of filling out the IRS Form 1120 with greater confidence and accuracy.

The IRS Form 1120 is an essential document for corporations in the United States, but there are several misconceptions surrounding it. Understanding these misconceptions can help ensure compliance and avoid unnecessary stress. Here’s a list of common misunderstandings about the IRS Form 1120:

By understanding these misconceptions, corporations can better navigate their tax obligations and ensure they are in compliance with IRS regulations.

The IRS Form 1120 is essential for corporations in the United States to report their income, gains, losses, deductions, and credits. Understanding how to fill it out correctly can help ensure compliance and maximize potential tax benefits. Here are some key takeaways regarding the use of this form:

By keeping these points in mind, you can navigate the complexities of Form 1120 more effectively and ensure your corporation remains compliant with tax regulations.