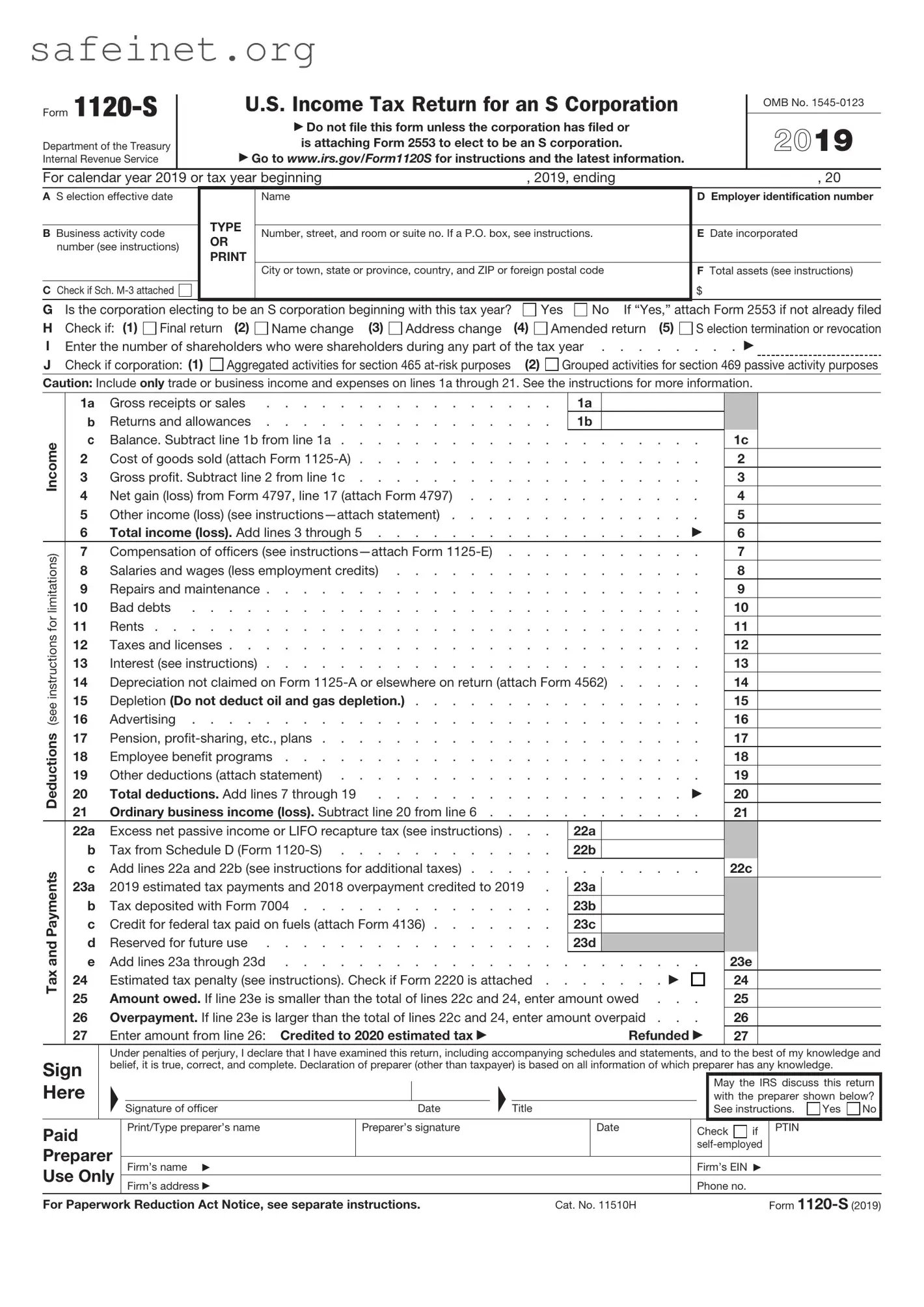

For business owners operating as S corporations, understanding the intricacies of the IRS 1120-S form is essential for effective tax compliance and strategic financial planning. This unique tax return allows eligible corporations to report their income, deductions, and credits while avoiding double taxation, as the income passes through to shareholders. Typically, the form is completed annually and is due on the 15th day of the third month after the end of the corporation's tax year. Shareholders receive a Schedule K-1, summarizing their share of the corporation's income, losses, and other tax-related items, enabling them to report this information accurately on their individual tax returns. Familiarity with the requirements of the IRS 1120-S can result in significant benefits, as it provides opportunities for potential tax savings and allows shareholders to leverage business expenses against personal income. Completing the form correctly and timely ensures compliance with IRS regulations, minimizing the risk of penalties and audits while promoting the overall financial health of the business.

Form

Department of the Treasury Internal Revenue Service

U.S. Income Tax Return for an S Corporation

Do not file this form unless the corporation has filed or

is attaching Form 2553 to elect to be an S corporation.

Go to www.irs.gov/Form1120S for instructions and the latest information.

OMB No.

2019

For calendar year 2019 or tax year beginning |

|

, 2019, ending |

, 20 |

||||||||

A S election effective date |

|

|

|

Name |

|

|

|

|

D Employer identification number |

||

|

|

|

|

TYPE |

|

|

|

|

|

|

|

B |

Business activity code |

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

E Date incorporated |

|||||||

|

OR |

||||||||||

|

number (see instructions) |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

F Total assets (see instructions) |

||||

|

|

|

|

|

|

|

|

|

|

||

C Check if Sch. |

|

|

|

|

|

|

|

|

$ |

||

G |

Is the corporation electing to be an S corporation beginning with this tax year? |

|

Yes |

No If “Yes,” attach Form 2553 if not already filed |

|||||||

H |

Check if: (1) |

Final return |

(2) |

Name change (3) |

Address change |

(4) |

Amended return (5) |

S election termination or revocation |

|||

I |

Enter the number of shareholders who were shareholders during any part of the tax year |

||||||||||

J |

Check if corporation: (1) |

|

Aggregated activities for section 465 |

(2) |

Grouped activities for section 469 passive activity purposes |

||||||

Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Deductions (see instructions for limitations) Income

Tax and Payments

1a |

Gross receipts or sales |

|

1a |

|

|

|

b |

Returns and allowances |

|

1b |

|

|

|

c |

Balance. Subtract line 1b from line 1a |

. . . . . . . . |

1c |

|

||

2 |

Cost of goods sold (attach Form |

. . . . . . . . |

2 |

|

||

3 |

Gross profit. Subtract line 2 from line 1c |

. . . . . . . . |

3 |

|

||

4 |

Net gain (loss) from Form 4797, line 17 (attach Form 4797) |

. . . . . . . . |

4 |

|

||

5 |

Other income (loss) (see |

. . . . . . . . |

5 |

|

||

6 |

Total income (loss). Add lines 3 through 5 |

. . . . . . . |

6 |

|

||

7 |

Compensation of officers (see |

. . . . . . . . |

7 |

|

||

8 |

Salaries and wages (less employment credits) |

. . . . . . . . |

8 |

|

||

9 |

Repairs and maintenance |

. . . . . . . . |

9 |

|

||

10 |

Bad debts |

. . . . . . . . |

10 |

|

||

11 |

Rents |

. . . . . . . . |

11 |

|

||

12 |

Taxes and licenses |

. . . . . . . . |

12 |

|

||

13 |

Interest (see instructions) |

. . . . . . . . |

13 |

|

||

14 |

Depreciation not claimed on Form |

14 |

|

|||

15 |

Depletion (Do not deduct oil and gas depletion.) |

. . . . . . . . |

15 |

|

||

16 |

Advertising |

. . . . . . . . |

16 |

|

||

17 |

Pension, |

. . . . . . . . |

17 |

|

||

18 |

Employee benefit programs |

. . . . . . . . |

18 |

|

||

19 |

Other deductions (attach statement) |

. . . . . . . . |

19 |

|

||

20 |

Total deductions. Add lines 7 through 19 |

. . . . . . . |

20 |

|

||

21 |

Ordinary business income (loss). Subtract line 20 from line 6 . . . . |

. . . . . . . . |

21 |

|

||

22a |

Excess net passive income or LIFO recapture tax (see instructions) . . . |

|

22a |

|

|

|

b |

Tax from Schedule D (Form |

|

22b |

|

|

|

c |

Add lines 22a and 22b (see instructions for additional taxes) |

. . . . . . . . |

22c |

|

||

23a |

2019 estimated tax payments and 2018 overpayment credited to 2019 . |

|

23a |

|

|

|

b |

Tax deposited with Form 7004 |

|

23b |

|

|

|

c |

Credit for federal tax paid on fuels (attach Form 4136) |

|

23c |

|

|

|

d |

Reserved for future use |

|

23d |

|

|

|

e |

Add lines 23a through 23d |

. . . . . . . . |

23e |

|

||

24 |

Estimated tax penalty (see instructions). Check if Form 2220 is attached . |

. . . . . . |

24 |

|

||

25 |

Amount owed. If line 23e is smaller than the total of lines 22c and 24, enter amount owed . . . |

25 |

|

|||

26 |

Overpayment. If line 23e is larger than the total of lines 22c and 24, enter amount overpaid . . . |

26 |

|

|||

27 |

Enter amount from line 26: Credited to 2020 estimated tax |

|

|

Refunded |

27 |

|

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

F |

|

|

F |

|

|

May the IRS discuss this return |

||

|

|

|

||||||

|

|

|

|

with the preparer shown below? |

||||

Signature of officer |

Date |

Title |

|

See instructions. |

Yes |

No |

||

|

|

|

|

|

|

|

|

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

Check |

if |

PTIN |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

|

Use Only |

|

|

|

|

|

|

||

Firm’s address |

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

|

||

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11510H |

|

|

Form |

|

|||

Form |

|

|

|

Page 2 |

|

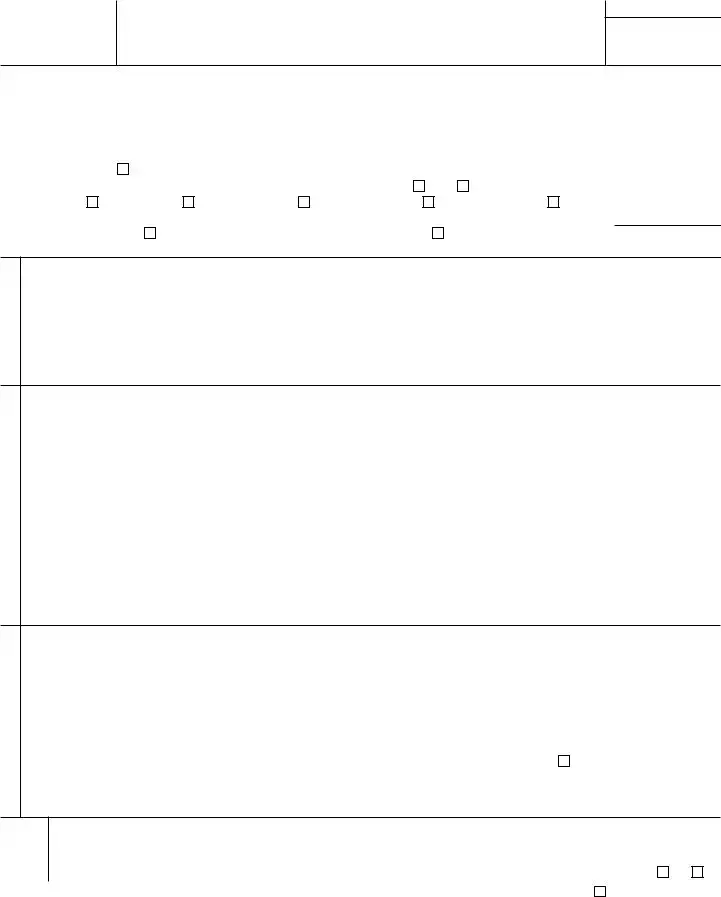

Schedule B |

Other Information (see instructions) |

|

|||

1 Check accounting method: a |

Cash |

b |

Accrual |

Yes No |

|

c

Other (specify)

Other (specify)

2 See the instructions and enter the:

a Business activity |

b Product or service |

3At any time during the tax year, was any shareholder of the corporation a disregarded entity, a trust, an estate, or a nominee or similar person? If “Yes,” attach Schedule

4At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total stock issued and outstanding of any foreign or domestic corporation? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v)

below . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(i) Name of Corporation |

(ii) Employer |

(iii) Country of |

(iv) Percentage of |

(v) If Percentage in (iv) Is 100%, Enter |

|

Identification |

Incorporation |

Stock Owned |

the Date (if any) a Qualified Subchapter |

|

Number (if any) |

|

|

S Subsidiary Election Was Made |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v) below . . . . . . .

(i) Name of Entity |

(ii) Employer |

(iii) Type of Entity |

(iv) Country of |

(v) Maximum Percentage Owned |

|

Identification |

|

Organization |

in Profit, Loss, or Capital |

|

Number (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5a At the end of the tax year, did the corporation have any outstanding shares of restricted stock? . . . . . . . .

If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of restricted stock |

(ii) |

Total shares of |

bAt the end of the tax year, did the corporation have any outstanding stock options, warrants, or similar instruments? . If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of stock outstanding at the end of the tax year |

. |

(ii)Total shares of stock outstanding if all instruments were executed

6Has this corporation filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide

|

information on any reportable transaction? |

. . . . . . . . . . . . . . . . . . . . . . . . |

7 |

Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . |

|

|

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount |

|

|

Instruments. |

|

8If the corporation (a) was a C corporation before it elected to be an S corporation or the corporation acquired an asset with a basis determined by reference to the basis of the asset (or the basis of any other property) in the hands of a C corporation and

(b) has net unrealized

gain reduced by net recognized |

$ |

9Did the corporation have an election under section 163(j) for any real property trade or business or any farming business

|

in effect during the tax year? See instructions |

10 |

Does the corporation satisfy one or more of the following? See instructions |

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense. If “Yes,” complete and attach Form 8990.

11 Does the corporation satisfy both of the following conditions? . . . . . . . . . . . . . . . . . .

aThe corporation’s total receipts (see instructions) for the tax year were less than $250,000. b The corporation’s total assets at the end of the tax year were less than $250,000.

If “Yes,” the corporation is not required to complete Schedules L and

Form

Form |

Page 3 |

|

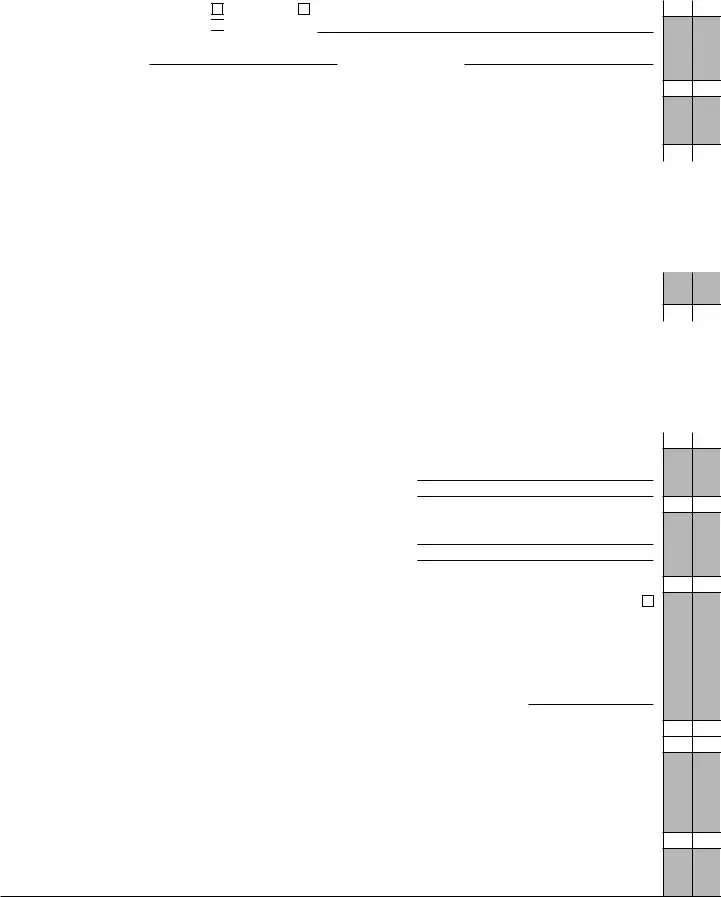

Schedule B |

Other Information (see instructions) (continued) |

Yes No |

12During the tax year, did the corporation have any

terms modified so as to reduce the principal amount of the debt? . . . . . . . . . . . . . . . . .

If “Yes,” enter the amount of principal reduction |

$ |

13During the tax year, was a qualified subchapter S subsidiary election terminated or revoked? If “Yes,” see instructions .

14a |

Did the corporation make any payments in 2019 that would require it to file Form(s) 1099? |

|

b |

If “Yes,” did the corporation file or will it file required Form(s) 1099? |

|

15 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|

|

If “Yes,” enter the amount from Form 8996, line 14 |

$ |

Schedule K |

|

Shareholders’ Pro Rata Share Items |

|

|

|

|

|

|||||

|

1 |

|

Ordinary business income (loss) (page 1, line 21) |

|||||||||

|

2 |

|

Net rental real estate income (loss) (attach Form 8825) |

|||||||||

|

3a |

Other gross rental income (loss) |

. . . . . . . |

|

3a |

|

||||||

|

b |

Expenses from other rental activities (attach statement) |

. . . . |

|

3b |

|

||||||

(Loss) |

c |

Other net rental income (loss). Subtract line 3b from line 3a |

||||||||||

4 |

|

Interest income |

||||||||||

|

|

|||||||||||

|

5 |

|

Dividends: a Ordinary dividends |

|||||||||

Income |

|

|

b Qualified dividends |

. . . . . . . |

|

5b |

|

|||||

6 |

|

Royalties |

||||||||||

|

|

|||||||||||

|

7 |

|

Net |

. . . . . . . . |

||||||||

|

8a |

Net |

||||||||||

|

b |

Collectibles (28%) gain (loss) |

. . . . . . . |

|

8b |

|

||||||

|

c |

Unrecaptured section 1250 gain (attach statement) |

|

8c |

|

|||||||

|

9 |

|

Net section 1231 gain (loss) (attach Form 4797) |

|||||||||

|

10 |

|

Other income (loss) (see instructions) . . . |

Type |

|

|

|

|

||||

Deductions |

11 |

|

Section 179 deduction (attach Form 4562) |

|||||||||

12a |

Charitable contributions |

|||||||||||

|

||||||||||||

|

b |

Investment interest expense |

||||||||||

|

c |

Section 59(e)(2) expenditures (1) Type |

|

|

|

|

|

(2) Amount |

||||

|

d |

Other deductions (see instructions) . . . . |

Type |

|

|

|

|

|||||

|

13a |

|||||||||||

|

b |

|||||||||||

Credits |

c |

Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) . . |

||||||||||

d |

Other rental real estate credits (see instructions) |

Type |

|

|

|

|

||||||

|

|

|

|

|

||||||||

|

e |

Other rental credits (see instructions) . . . |

Type |

|

|

|

|

|||||

|

f |

Biofuel producer credit (attach Form 6478) |

. . . . . . . . . . . . . . . . |

|||||||||

|

g |

Other credits (see instructions) |

Type |

|

|

|

|

|||||

|

14a |

Name of country or U.S. possession |

|

|

|

|

|

|

|

|||

|

b |

Gross income from all sources |

||||||||||

|

c |

Gross income sourced at shareholder level |

||||||||||

|

|

|

Foreign gross income sourced at corporate level |

|

|

|

|

|

||||

|

d |

Reserved for future use |

||||||||||

|

e |

Foreign branch category |

||||||||||

|

f |

Passive category |

. . . . . . . . . . . . . . . . . . . . . . . . |

|||||||||

Transactions |

g |

General category |

. . . . . . . . . . . . . . . . . . . . . . . . |

|||||||||

h |

Other (attach statement) |

|||||||||||

|

||||||||||||

|

|

|

Deductions allocated and apportioned at shareholder level |

|

|

|

|

|||||

|

i |

Interest expense |

||||||||||

Foreign |

j |

Other |

||||||||||

|

|

Deductions allocated and apportioned at corporate level to foreign source income |

||||||||||

|

|

|

||||||||||

|

k |

Reserved for future use |

||||||||||

|

l |

Foreign branch category |

||||||||||

|

m |

Passive category |

. . . . . . . . . . . . . . . . . . . . . . . . |

|||||||||

|

n |

General category |

. . . . . . . . . . . . . . . . . . . . . . . . |

|||||||||

|

o |

Other (attach statement) |

||||||||||

|

|

|

Other information |

|

|

|

|

|

|

|

|

|

|

p |

Total foreign taxes (check one): |

Paid |

|

Accrued |

|||||||

|

q |

Reduction in taxes available for credit (attach statement) |

||||||||||

rOther foreign tax information (attach statement)

Total amount

1

2

3c

4

5a

6

7

8a

9

10

11

12a

12b

12c(2)

12d

13a

13b

13c

13d

13e

13f

13g

14b

14c

14d

14e

14f

14g

14h

14i

14j

14k

14l

14m

14n

14o

14p

14q

Form

Form |

Page 4 |

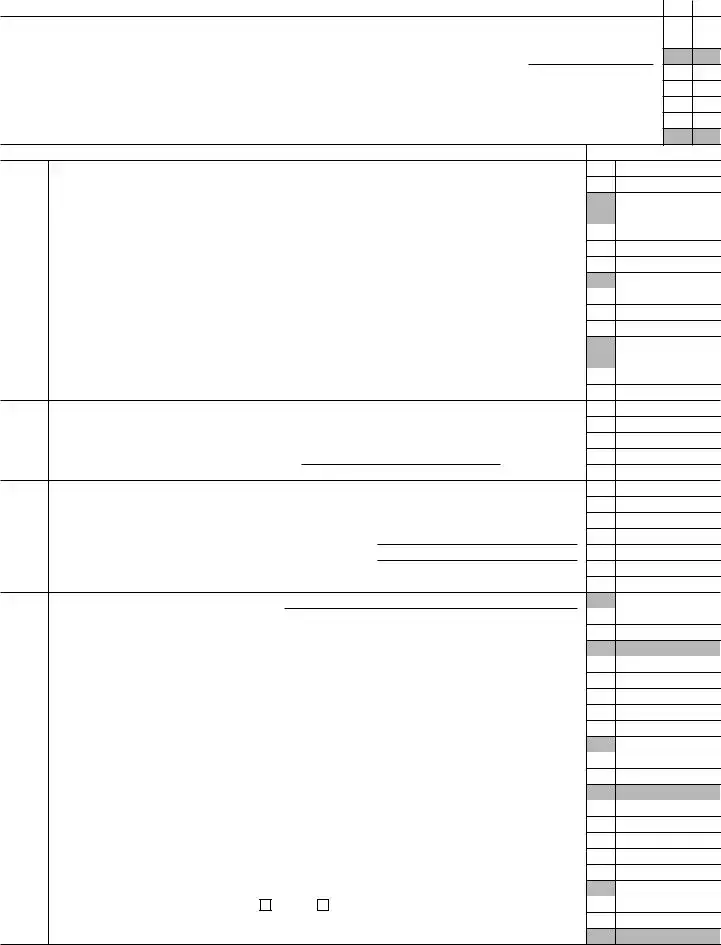

Schedule K |

Shareholders’ Pro Rata Share Items (continued) |

|||||

|

MinimumTax |

Items(AMT) |

15a |

|||

Alternative |

b |

Adjusted gain or loss |

||||

c |

Depletion (other than oil and gas) |

|||||

|

|

|

|

|||

|

|

|

|

d |

Oil, gas, and geothermal |

|

|

|

|

|

e |

Oil, gas, and geothermal |

|

AffectingItems |

Shareholder |

Basis |

f |

Other AMT items (attach statement) |

||

e |

Repayment of loans from shareholders |

|||||

|

|

|

|

16a |

||

|

|

|

|

b |

Other |

|

|

|

|

|

c |

Nondeductible expenses |

|

Other |

Information |

d |

Distributions (attach statement if required) (see instructions) |

|||

d |

Other items and amounts (attach statement) |

|||||

|

|

|

|

17a |

Investment income |

|

|

|

|

|

b |

Investment expenses |

|

|

|

|

|

c |

Dividend distributions paid from accumulated earnings and profits |

|

Recon- |

ciliation |

18 |

Income (loss) reconciliation. Combine the amounts on lines 1 through 10 in the far right |

|||

|

|

|

|

|||

|

|

|

|

|

column. From the result, subtract the sum of the amounts on lines 11 through 12d and 14p . |

|

|

|

|

|

|

|

|

Total amount

15a

15b

15c

15d

15e

15f

16a

16b

16c

16d

16e

17a

17b

17c

18

Schedule L |

Balance Sheets per Books |

|

Beginning of tax year |

|

End of tax year |

|

|||||

|

|

Assets |

|

(a) |

|

(b) |

(c) |

|

|

(d) |

|

1 |

Cash |

|

|

|

|

|

|

|

|

||

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

||

b |

Less allowance for bad debts |

( |

) |

|

|

( |

) |

|

|

||

3 |

Inventories |

|

|

|

|

|

|

|

|

||

4 |

U.S. government obligations |

|

|

|

|

|

|

|

|

||

5 |

|

|

|

|

|

|

|

|

|||

6 |

Other current assets (attach statement) . . . |

|

|

|

|

|

|

|

|

||

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

||

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

||

10a |

Buildings and other depreciable assets . . . |

|

|

|

|

|

|

|

|

||

b |

Less accumulated depreciation |

( |

) |

|

|

( |

) |

|

|

||

11a |

Depletable assets |

|

|

|

|

|

|

|

|

||

b |

Less accumulated depletion |

( |

) |

|

|

( |

) |

|

|

||

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

||

13a |

Intangible assets (amortizable only) . . . . |

|

|

|

|

|

|

|

|

||

b |

Less accumulated amortization |

( |

) |

|

|

( |

) |

|

|

||

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

||

15 |

Total assets |

|

|

|

|

|

|

|

|

||

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

||

16 |

Accounts payable |

|

|

|

|

|

|

|

|

||

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

||

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

||

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

||

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

||

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

||

22 |

Capital stock |

|

|

|

|

|

|

|

|

||

23 |

Additional |

|

|

|

|

|

|

|

|

||

24 |

Retained earnings |

|

|

|

|

|

|

|

|

||

25 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

||

26 |

Less cost of treasury stock |

|

|

( |

) |

|

|

( |

) |

||

27 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

||

Form

Form |

Page 5 |

|

Schedule |

Reconciliation of Income (Loss) per Books With Income (Loss) per Return |

|

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books . . . . |

2Income included on Schedule K, lines 1, 2, 3c, 4, 5a, 6, 7, 8a, 9, and 10, not recorded on books this year (itemize)

3Expenses recorded on books this year not included on Schedule K, lines 1 through 12 and 14p (itemize):

aDepreciation $

bTravel and entertainment $

4 Add lines 1 through 3 . . . . . .

5Income recorded on books this year not included on Schedule K, lines 1 through 10 (itemize):

a

6Deductions included on Schedule K, lines 1 through 12 and 14p, not charged against book income this year (itemize):

aDepreciation $

7 Add lines 5 and 6 . . . . . . .

8Income (loss) (Schedule K, line 18).

Subtract line 7 from line 4 . . . .

Schedule

(see instructions)

|

|

(a) Accumulated |

|

(b) Shareholders’ |

(c) Accumulated |

(d) Other adjustments |

|

|

|

|

adjustments account |

|

undistributed taxable |

earnings and profits |

|

account |

|

|

|

|

|

income previously taxed |

|

|

|

|

1 |

Balance at beginning of tax year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

2 |

Ordinary income from page 1, line 21 . . . |

|

|

|

|

|

|

|

3 |

Other additions |

|

|

|

|

|

|

|

4 |

Loss from page 1, line 21 |

( |

) |

|

|

|

|

|

5 |

Other reductions |

( |

) |

|

|

( |

) |

|

6 |

Combine lines 1 through 5 |

|

|

|

|

|

|

|

7 |

Distributions |

|

|

|

|

|

|

|

8 |

Balance at end of tax year. Subtract line 7 from |

|

|

|

|

|

|

|

|

line 6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

|

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1120-S is used by S corporations to report income, deductions, and credits for federal tax purposes. |

| Filing Requirements | To file Form 1120-S, S corporations must meet specific criteria, including having valid S corporation status and generally must be filed by March 15 of the following tax year. |

| Pass-Through Taxation | One of the key features of Form 1120-S is that it allows income to pass through to shareholders, avoiding double taxation at the corporate level. |

| State-Specific Requirements | Many states require their own S corporation forms to be filed in addition to the federal Form 1120-S. An example is California's Form 100S, governed by California Revenue and Taxation Code Section 23800. |

Filling out the IRS 1120-S form can feel overwhelming, but breaking it down into manageable steps makes it easier. This form is used for S corporations to report income, gains, losses, deductions, and credits. The following steps will guide you through the process.

Following these steps systematically ensures a smoother experience. Once the form is submitted, keep copies for your records and monitor for any communications from the IRS regarding your filing.

What is the IRS 1120-S form?

The IRS 1120-S form is a tax return specifically designed for S corporations. S corporations are a special type of corporation that meets specific Internal Revenue Code requirements. Filing this form allows these corporations to report their income, deductions, and credits to the IRS while generally avoiding double taxation on corporate income.

Who needs to file Form 1120-S?

Any corporation that has elected to be treated as an S corporation must file Form 1120-S annually. If the corporation has income or losses, it must report them using this form. This includes domestic corporations with up to 100 shareholders who meet certain qualifications.

What is the deadline for filing Form 1120-S?

The deadline for filing Form 1120-S is typically March 15th for calendar year corporations. If the corporation operates on a fiscal year basis, the return is due on the 15th day of the third month following the end of the fiscal year. There is the option to file for an automatic six-month extension using Form 7004.

What information is required on Form 1120-S?

The form requires basic information about the corporation, like its name, address, and Employer Identification Number (EIN). It also needs financial details such as total income, cost of goods sold, deductions, and credits. Any income or loss distributed to shareholders must also be reported.

What are the benefits of filing Form 1120-S?

One significant benefit of filing Form 1120-S is the avoidance of double taxation on corporate income. Instead, income and losses pass through to the shareholders, who report them on their personal tax returns. This can lead to a lower overall tax burden for S corporation shareholders.

What happens if Form 1120-S is filed late?

If you miss the deadline to file Form 1120-S, the corporation may face penalties. The IRS typically charges a penalty based on the number of shareholders in the S corporation multiplied by the number of months the return is late. Additionally, the late filing may complicate the shareholders' tax filings as they may not receive their Schedule K-1 forms on time.

Can an S corporation carry forward losses?

Yes, an S corporation can carry forward net operating losses (NOLs) to offset future income. However, shareholders can only claim losses on their personal returns up to the amount they have in the corporation (basis). Any excess losses may be carried forward to future tax years, subject to specific rules.

What is the Schedule K-1, and why is it important?

Schedule K-1 is a tax document provided to each shareholder of the S corporation, detailing their share of income, deductions, and credits from the corporation. It's important because shareholders need this information to accurately report their individual tax obligations. Each shareholder must receive their Schedule K-1 by the due date of Form 1120-S.

Are there specific deductions or credits available for S corporations?

S corporations can claim a variety of deductions and credits on Form 1120-S, including ordinary and necessary business expenses, certain retirement plan contributions, and health insurance premiums paid for shareholders. Various tax credits may also be available, depending on the corporation's activities and investments.

How can I amend a previously filed Form 1120-S?

If there is a need to amend a previously filed Form 1120-S, you should complete a new form with the correct information and write "Amended" at the top of the form. This amended return should be submitted to the IRS and a copy sent to each shareholder, especially if it affects their Schedule K-1 amounts.

When filling out the IRS 1120-S form, it’s easy to make mistakes that can lead to complications. Here are four common errors to avoid:

Some people forget to provide accurate details about shareholders. Names, addresses, and Social Security numbers must be provided for all shareholders. Missing or wrong information can cause delays.

All sources of income need to be reported. Ignoring income from side projects or other business activities can lead to issues with the IRS. Make sure every dollar earned is documented.

Many overlook deductions or credits that could benefit their tax situation. Research available options thoroughly. Taking advantage of every deduction can significantly affect your tax liability.

It is crucial to file the form on time. Missing the deadline can result in fines or penalties. Stay on track with important dates to avoid unnecessary issues.

Each of these mistakes can create additional challenges when filing taxes. Careful attention to detail is key in ensuring a smooth process.

The IRS 1120-S form is essential for S corporations and is used to report income, deductions, and tax credits. However, it is often accompanied by several other documents that are critical for providing a complete financial picture. Here are five key forms that are commonly filed along with the IRS 1120-S form.

These forms and documents work together with the IRS 1120-S to create a comprehensive tax report for S corporations. Properly completing and filing all necessary forms is crucial for compliance and for maintaining the corporation’s good standing with the IRS.

The IRS Form 1120-S is primarily used by S corporations to report income, deductions, and credits. It shares similarities with Form 1065, which is used for partnerships. Both forms provide a platform for entities that pass their income through to their owners, which allows for taxation at the individual level instead of the entity level. This feature helps avoid double taxation, creating a straightforward way for owners to report their share of income or losses on their personal tax returns.

Next, there’s the IRS Form 1040, the individual income tax return. While Form 1120-S is for businesses, Form 1040 is used by individuals. However, if an S corporation passes income to its shareholders, those individuals will need to report that income on their Form 1040. Therefore, both forms work in tandem, as the individual’s tax obligations may reflect the income reported on a corresponding 1120-S form.

Another document that shares similarities is the IRS Form 1065-B, which is designed specifically for electing large partnerships. Like S corporations, these partnerships also pass income to their partners and avoid entity-level taxation. Thus, they both require detailed reporting of income and expenses, ensuring that all shareholders or partners can accurately report their allocations on their personal returns.

Moving on to Form 1120, the standard corporate tax form, we see key differences. Unlike the 1120-S, which avoids double taxation, the 1120 pays corporate taxes directly. However, both forms require reports of income, deductions, and credits, illustrating the different tax structures that corporations can choose based on their size and operational style.

The IRS Form 990 also has some characteristics in common with the 1120-S, particularly regarding transparency and reporting requirements. Form 990 is used by non-profit organizations to provide the IRS with financial information and ensure accountability. Both forms require comprehensive data about income and expenditures, albeit they serve different types of organizations and objectives.

Similarly, auto-generating forms like Schedule C, used by sole proprietors, have a commonality with the 1120-S in that they report business income. Sole proprietors may have more straightforward reporting processes, but the essence of documenting income and expenses resonates between the two. Both forms help individuals and corporations navigate their tax responsibilities, serving distinct yet complementary roles within the tax framework.

Lastly, there’s Form 5500, which annual reports benefits plans must file. While not a direct similarity with tax forms, it emphasizes the importance of compliance and record-keeping that both the S corporations report on the 1120-S and employee benefit plans must adhere to. Capturing the financial health of the entity ensures informed stakeholders, allowing both forms to contribute essential data to the overall landscape of an organization’s finances.

When filling out the IRS 1120-S form, it's essential to follow specific guidelines to ensure accuracy and compliance. Here are some dos and don’ts to consider:

Understanding the IRS Form 1120-S is essential for small business owners operating as S corporations. Here are four common misconceptions about this form:

Clarifying these misconceptions can help business owners make informed decisions regarding their S corporations and tax obligations.

The IRS 1120-S form is specifically designed for S corporations to report income, deductions, and credits. It's essential for these entities to file this form annually to remain compliant with federal tax laws.

Eligibility is key. To qualify as an S corporation, you must meet specific requirements including having only allowable shareholders, which can include individuals, certain trusts, and estates but not partnerships or corporations.

Filing deadlines are crucial. The IRS 1120-S must typically be filed by the 15th day of the third month after the end of your corporation's tax year. This means that for a calendar year entity, the due date is March 15.

Shareholder reporting plays a significant role. Each shareholder must receive a Schedule K-1, which reports their share of the corporation’s income, deductions, and credits. This allows them to report their share on their individual tax returns.

Accurate records are your best friend. Keeping detailed records of any expenses, revenues, and other financial transactions throughout the year simplifies the process of completing the form and minimizes the risk of errors.

Consider professional help. While some businesses can handle filing their own forms, consulting with a tax professional familiar with S corporation regulations can help ensure compliance and maximize tax benefits.