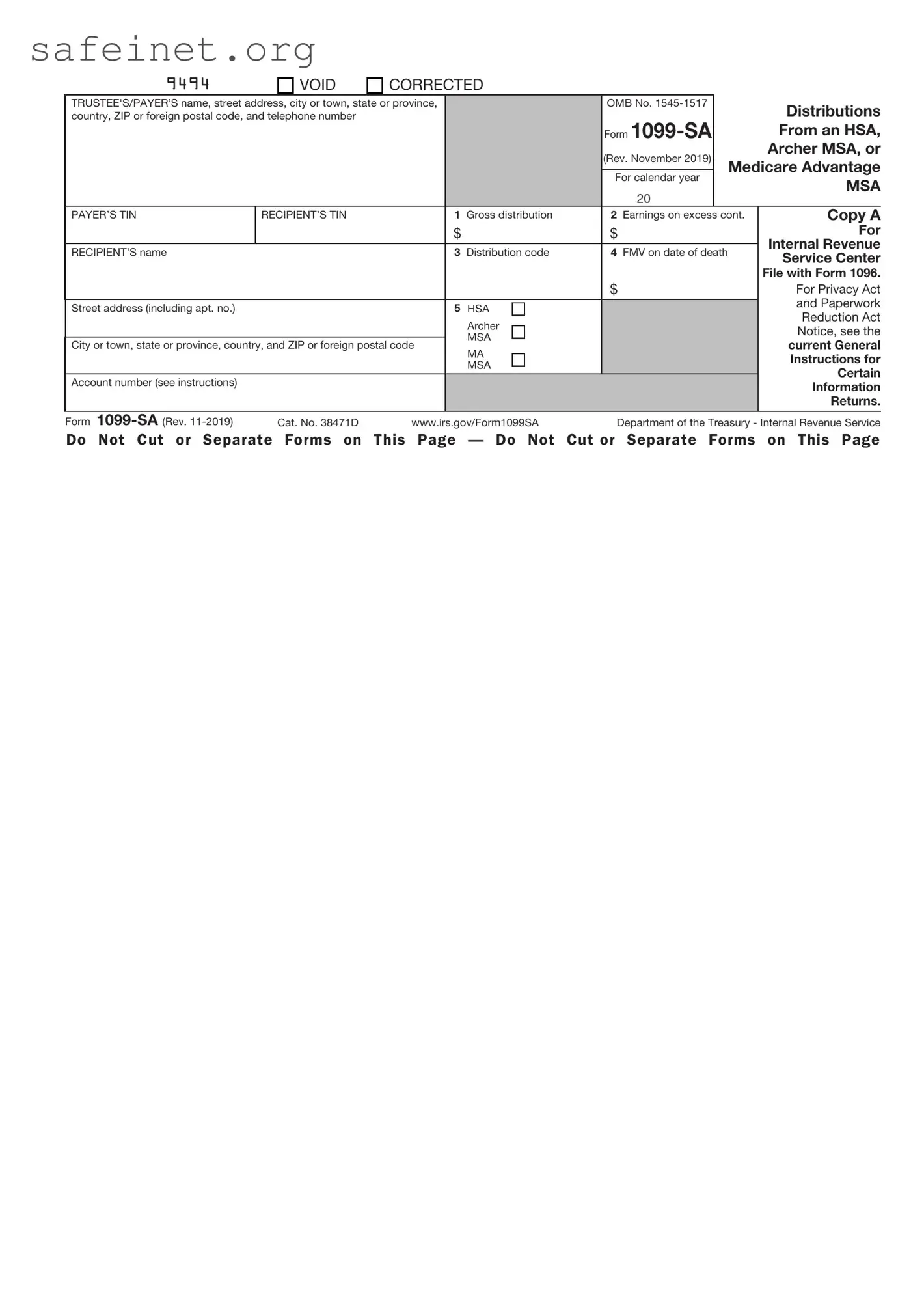

The IRS 1099-SA form plays a crucial role in the financial reporting process for individuals who have made distributions from their health savings accounts (HSAs), Archer Medical Savings Accounts (MSAs), or Medicare Advantage MSAs. It serves to inform both the taxpayer and the IRS about the total distributions taken from these accounts during the tax year. When an individual withdraws funds from their HSA or similar accounts for qualified medical expenses, this form details the amounts disbursed, helping to ensure compliance with tax regulations. Importantly, the form also distinguishes between taxable and non-taxable distributions, which is essential for accurate tax filing. Taxpayers typically receive this information by the end of January each year, allowing them sufficient time to incorporate it into their annual tax returns. Understanding the nuances of the 1099-SA can help individuals navigate potential tax implications and maximize their benefits from health-related savings accounts.

9494

VOID

CORRECTED

TRUSTEE'S/PAYER’S name, street address, city or town, state or province, |

|

|

|

OMB No. |

|

|

Distributions |

||

country, ZIP or foreign postal code, and telephone number |

|

|

|

|

Form |

|

|

||

|

|

|

|

|

|

|

|

From an HSA, |

|

|

|

|

|

|

|

(Rev. November 2019) |

|

|

Archer MSA, or |

|

|

|

|

|

|

|

Medicare Advantage |

||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

For calendar year |

|

||

|

|

|

|

|

|

|

|

MSA |

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

PAYER’S TIN |

RECIPIENT’S TIN |

|

1 Gross distribution |

|

2 Earnings on excess cont. |

Copy A |

|||

|

|

|

$ |

|

|

$ |

|

|

For |

|

|

|

|

|

|

|

|

|

Internal Revenue |

RECIPIENT’S name |

|

|

3 Distribution code |

|

4 FMV on date of death |

|

|||

|

|

|

|

Service Center |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

File with Form 1096. |

|

|

|

|

|

|

$ |

|

|

For Privacy Act |

|

|

|

|

|

|

|

|

|

and Paperwork |

Street address (including apt. no.) |

|

|

5 |

HSA |

|

|

|

|

|

|

|

|

|

|

|

Reduction Act |

|||

|

|

|

|

Archer |

|

|

|

|

|

|

|

|

|

|

|

|

|

Notice, see the |

|

|

|

|

|

MSA |

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

|

|

current General |

|||

|

MA |

|

|

|

|

||||

|

|

|

|

|

|

|

|

Instructions for |

|

|

|

|

|

MSA |

|

|

|

|

|

|

|

|

|

|

|

|

|

Certain |

|

Account number (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Information |

|

|

|

|

|

|

|

|

|

|

Returns. |

Form |

Cat. No. 38471D |

www.irs.gov/Form1099SA |

|

Department of the Treasury - Internal Revenue Service |

|||||

Do Not Cut or Separate Forms on |

This Page |

— Do Not |

Cut or Separate Forms |

on This Page |

|||||

CORRECTED (if checked)

TRUSTEE’S/PAYER’S name, street address, city or town, state or province, |

|

OMB No. |

|

|

Distributions |

|

country, ZIP or foreign postal code, and telephone number |

|

Form |

|

|

||

|

|

|

|

|

From an HSA, |

|

|

|

|

(Rev. November 2019) |

|

|

Archer MSA, or |

|

|

|

|

Medicare Advantage |

||

|

|

|

|

|

||

|

|

|

For calendar year |

|

||

|

|

|

|

|

MSA |

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

PAYER’S TIN |

RECIPIENT’S TIN |

1 Gross distribution |

2 Earnings on excess cont. |

Copy B |

||

|

|

$ |

$ |

|

|

For |

RECIPIENT’S name |

|

3 Distribution code |

4 FMV on date of death |

|

Recipient |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

Street address (including apt. no.) |

|

5 HSA |

|

|

|

|

|

|

Archer |

|

|

|

This information |

|

|

MSA |

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

is being furnished |

||

MA |

|

|

|

|||

|

|

|

|

|

to the IRS. |

|

|

|

MSA |

|

|

|

|

|

|

|

|

|

|

|

Account number (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

||

Form |

(keep for your records) |

www.irs.gov/Form1099SA |

Department of the Treasury - Internal Revenue Service |

|||

Instructions for Recipient

Distributions from a health savings account (HSA), Archer medical savings account (MSA), or Medicare Advantage (MA) MSA are reported to you on Form

An HSA or Archer MSA distribution isn’t taxable if you used it to pay qualified medical expenses of the account holder or eligible family member or you rolled it over. An HSA may be rolled over to another HSA; an Archer MSA may be rolled over to another Archer MSA or an HSA. An MA MSA isn’t taxable if you used it to pay qualified medical expenses of the account holder only. If you didn’t use the distribution from an HSA, Archer MSA, or MA MSA to pay for qualified medical expenses, or in the case of an HSA or Archer MSA, you didn’t roll it over, you must include the distribution in your income (see Form 8853 or Form 8889). Also, you may owe a penalty.

You may repay a mistaken distribution from an HSA no later than April 15 following the first year you knew or should have known the distribution was a mistake, providing the trustee allows the repayment.

For more information, see the Instructions for Form 8853 and the Instructions for Form 8889. Also see Pub. 969.

Recipient’s taxpayer identification number (TIN). For your protection, this form may show only the last four digits of your TIN (SSN, ITIN, ATIN, or EIN). However, the issuer has reported your complete identification number to the IRS.

Spouse beneficiary. If you inherited an Archer MSA or MA MSA because of the death of your spouse, special rules apply. See the Instructions for Form 8853. If you inherited an HSA because of the death of your spouse, see the Instructions for Form 8889.

Estate beneficiary. If the HSA, Archer MSA, or MA MSA account holder dies and the estate is the beneficiary, the fair market value (FMV) of the account on the date of death is includible in the account holder’s gross income. Report the amount on the account holder’s final income tax return.

Nonspouse beneficiary. If you inherited the HSA, Archer MSA, or MA MSA from someone who wasn’t your spouse, you must report as income on your tax return the FMV of the account as of the date of death. Report the FMV on your tax return for the year the account owner died even if you received the distribution from the account in a later year. See the Instructions for Form 8853 or the Instructions for Form 8889. Any earnings on the account after the date of death (box 1 minus box 4 of Form

Account number. May show an account or other unique number the payer assigned to distinguish your account.

Box 1. Shows the amount received this year. The amount may have been a direct payment to the medical service provider or distributed to you.

Box 2. Shows the earnings on any excess contributions you withdrew from an HSA or Archer MSA by the due date of your income tax return. If you withdrew the excess, plus any earnings, by the due date of your income tax return, you must include the earnings in your income in the year you received the distribution even if you used it to pay qualified medical expenses. This amount is included in box 1. Include the earnings on the “Other income” line of your tax return. An excise tax of 6% for each tax year is imposed on you for excess individual and employer contributions that remain in the account. See Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other

Box 3. These codes identify the distribution you received:

Box 4. If the account holder died, shows the FMV of the account on the date of death. Box 5. Shows the type of account that is reported on this Form

Form

VOID

CORRECTED

TRUSTEE’S/PAYER’S name, street address, city or town, state or province, |

|

OMB No. |

|

|

Distributions |

||

country, ZIP or foreign postal code, and telephone number |

|

|

Form |

|

|

||

|

|

|

|

|

|

From an HSA, |

|

|

|

|

|

(Rev. November 2019) |

|

|

Archer MSA, or |

|

|

|

|

|

Medicare Advantage |

||

|

|

|

|

For calendar year |

|

||

|

|

|

|

|

|

MSA |

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

|

PAYER’S TIN |

RECIPIENT’S TIN |

|

1 Gross distribution |

2 Earnings on excess cont. |

Copy C |

||

|

|

|

$ |

$ |

|

|

For |

RECIPIENT’S name |

|

|

3 Distribution code |

4 FMV on date of death |

|

Trustee/Payer |

|

|

|

|

|

$ |

|

|

For Privacy Act |

|

|

|

|

|

|

and Paperwork |

|

Street address (including apt. no.) |

|

|

5 HSA |

|

|

|

Reduction Act |

|

|

|

Archer |

|

|

|

Notice, see the |

|

|

|

|

|

|

current General |

|

City or town, state or province, country, and ZIP or foreign postal code |

MSA |

|

|

|

|||

MA |

|

|

|

Instructions for |

|||

|

|

|

|

|

|

Certain |

|

|

|

|

MSA |

|

|

|

|

Account number (see instructions) |

|

|

|

|

|

|

Information |

|

|

|

|

|

|

Returns. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Form |

|

www.irs.gov/Form1099SA |

Department of the Treasury - Internal Revenue Service |

||||

Instructions for Trustee/Payer

To complete Form

•The current General Instructions for Certain Information Returns, and

•The current Instructions for Forms

To get or to order these instructions, go to www.irs.gov/Form1099SA.

Filing and furnishing. For filing and furnishing instructions, including due dates, and to request filing or furnishing extensions, see the current General Instructions for Certain Information Returns.

To file electronically, you must have software that generates a file according to the specifications in Pub. 1220.

Need help? If you have questions about reporting on Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS 1099-SA form is used to report distributions from Health Savings Accounts (HSAs), Archer Medical Savings Accounts (MSAs), and Medicare Advantage MSAs. |

| Who Issues It | Financial institutions and organizations that manage HSAs or MSAs are responsible for issuing the 1099-SA to account holders. |

| Filing Deadline | The form must be filed with the IRS by March 31st if filed electronically, or by February 28th for paper submissions. |

| Recipient Copy | Account holders should receive their copy of the 1099-SA by January 31st of the following tax year. |

| Tax Implications | Distributions reported on the 1099-SA may be taxable unless they were used for qualified medical expenses. |

| State-Specific Forms | Some states require additional forms to report HSA distributions; check state law for specific requirements. |

| Record Keeping | It is advisable to keep a copy of the 1099-SA for at least three years for tax record purposes. |

Completing the IRS 1099-SA form involves a few straightforward steps. Once filled out correctly, this form can be submitted to the IRS along with any required documentation. Here’s how to fill out the form accurately:

After following these steps, your form will be ready for submission. Make sure to keep a copy for your records, as well as any other supporting documentation that may be necessary for tax purposes.

What is the IRS 1099-SA form?

The IRS 1099-SA form is a tax document used to report distributions made from Health Savings Accounts (HSAs), Archer Medical Savings Accounts (MSAs), or Medicare Advantage MSAs. If you have withdrawn funds from one of these accounts in a given tax year, the form provides necessary information for both you and the IRS regarding the amount and purpose of the distributions.

Who receives the 1099-SA form?

If you have taken a distribution from your HSA, Archer MSA, or Medicare Advantage MSA, your account custodian will provide you with the 1099-SA form. The custodian is responsible for completing this form and sending it to you and the IRS by January 31 of the year following the tax year in which distributions occurred.

What information is included on the 1099-SA?

The form contains several key pieces of information. This includes your name, address, and taxpayer identification number, along with the name and address of the account custodian. Most importantly, it reports the total distributions made from your account during the tax year. Additionally, the form specifies the types of distributions received—qualified medical expenses, non-qualified distributions, etc.—which is crucial for your tax reporting.

Do I need to report the amounts shown on a 1099-SA?

Yes, you must report the amounts from the 1099-SA when filing your federal tax return. This document helps determine your taxable income and any potential tax liabilities. If your distributions were used for qualified medical expenses, they may not be taxable. However, distributions used for non-qualified purposes typically are. Consult IRS guidelines to understand how these amounts may affect your tax obligations.

What happens if I don’t receive a 1099-SA?

If you believe you should have received a 1099-SA, but it hasn't arrived, reach out to your account custodian. It's possible they may have sent it to an incorrect address, or perhaps a mistake was made in reporting your distributions. Even if you do not receive it, you still have the responsibility to report any distributions used for tax purposes.

Can I correct an error on my 1099-SA?

If you notice an error on your 1099-SA form, you should contact the custodian of your account as soon as possible. They can issue a corrected form, known as a 1099-SA with corrections, which you will then need to use for accurate tax reporting. It is important to resolve these errors before you file your tax return to avoid complications with the IRS.

What are the penalties for reporting incorrect information from a 1099-SA?

Incorrectly reporting distributions from your 1099-SA can lead to various penalties, including additional taxes owed or fines from the IRS. If the IRS discovers discrepancies, they may impose penalties for failure to accurately report income or for improper withdrawals. Consulting with a tax professional can help clarify your situation and minimize potential penalties.

Are there any tax implications if I use HSA funds for non-medical expenses?

Using HSA funds for non-medical expenses typically incurs penalties and taxes. Specifically, non-qualified distributions are subject to income tax and, if taken before age 65, a 20% penalty. After you turn 65, while you will still owe income tax on non-qualified distributions, the penalty will not apply. Awareness of these implications is crucial for managing your HSA effectively.

How do I obtain a copy of my 1099-SA?

Your account custodian is responsible for providing you with a copy of your 1099-SA. If you need a duplicate, you can request it directly from them. Some custodians may also offer the ability to access your forms electronically through their online platforms, giving you easier access to your financial documents.

What is the deadline for the 1099-SA form to be issued?

The deadline for custodians to provide the 1099-SA form to account holders is usually January 31st of the year following the tax year in which the distributions were made. This timeline ensures you have sufficient time to review the information and report it accurately on your tax return before the tax filing deadline.

Incorrect Recipient Information: Many individuals fail to accurately enter the recipient's name, address, and taxpayer identification number (TIN). This can lead to delays or rejection of the form.

Wrong Distribution Amount: Reporting the wrong amount distributed during the tax year is a common error. It’s crucial to double-check this figure to ensure accuracy.

Misclassification of Distributions: People often label distributions incorrectly. Knowing whether the distribution is for qualified medical expenses or other purposes is essential for proper tax reporting.

Failing to Sign the Form: A signature is necessary on the 1099-SA. Omitting it can prevent the form from being processed correctly.

Neglecting to Send to the IRS: Completing the 1099-SA is just one step. Many forget to submit it to the IRS by the deadlines, which can result in penalties.

Not Providing a Copy to the Recipient: After filing with the IRS, a copy must be given to the recipient. Some individuals overlook this important part of the process.

Using Incorrect Form Version: Different tax years may require different versions of the form. Using an outdated form can lead to compliance issues.

Failure to Stay Informed: Tax laws and regulations may change. Remaining updated on relevant IRS guidelines is essential to avoid mistakes in the future.

The IRS 1099-SA form is primarily used to report distributions from a Health Savings Account (HSA), Archer Medical Savings Account (MSA), or a Medicare Advantage MSA. Alongside this form, there are several other documents that may be useful when managing health savings accounts, assisting in tax reporting, or gathering necessary information for tax filings. Below are six common forms and documents that individuals may encounter in conjunction with the 1099-SA.

These forms and documents play a crucial role in ensuring accurate reporting and compliance with IRS regulations relating to health savings accounts and other medical savings options. They collectively assist individuals in understanding their tax obligations and maximizing potential benefits associated with their accounts.

The IRS 1099-MISC form is often thought of alongside the 1099-SA. This document is used to report various types of income from sources other than employment. Similar to the 1099-SA, which reports distributions from Health Savings Accounts (HSAs) or medical savings accounts, the 1099-MISC provides the Internal Revenue Service (IRS) with information about payments made to independent contractors, freelancers, or other non-employee compensation. The 1099-MISC ensures that all parties involved are aware of taxable income, creating a clear record for tax season.

The 1099-INT form serves a similar purpose but focuses specifically on interest income. Just as the 1099-SA reports distributions from HSAs, the 1099-INT informs the IRS and taxpayers about interest earnings from financial institutions. This form is crucial for taxpayers to accurately report income and pay taxes accordingly. Both forms help maintain transparency between the taxpayer and the IRS regarding funds received or distributed, making tax filing more straightforward.

Another related form is the 1099-DIV, which reports dividend income from stocks and mutual funds. Similar to the 1099-SA, it officializes the amounts taxpayers received throughout the year, indicating how much they earned through investments. Accurate reporting of dividends is essential, as these can significantly impact an individual’s overall income and tax liabilities. Both forms require careful attention to detail to ensure accurate reporting to the IRS.

The 1099-R form is tailored for reporting distributions from retirement accounts and pensions. In this way, it shares similarities with the 1099-SA, which deals with distributions from health-related accounts. Both documents provide critical information on funds that have incurred tax implications. Understanding the details captured in these forms helps individuals manage their finances responsibly while ensuring compliance with tax regulations.

The 1099-B form is utilized for reporting sales of securities and is similar in function to the 1099-SA regarding clarity in financial distributions. While the 1099-SA concerns health savings, the 1099-B focuses on the capital gains achieved or losses incurred from asset sales. Both forms are vital for taxpayers to track various types of income, enabling accurate reporting and minimizing discrepancies with the IRS.

The 1099-C is specifically designed for cancellation of debt. It is comparable to the 1099-SA as it outlines financial transactions that may impact an individual’s tax situation. When debt is forgiven, it can result in taxable income, similar to how HSA distributions may affect a taxpayer's overall income. The importance of both forms lies in their role of informing taxpayers about financial events that require reporting to the IRS.

The 1099-G form relates to government payments and is akin to the 1099-SA in that it also reports incomes not categorized as wages. The 1099-G showcases income from unemployment benefits, state tax refunds, or other governmental support. Both forms are essential for maintaining transparency and ensuring compliance with tax obligations, highlighting sources of non-employment income that can affect an individual's tax return.

Finally, the 1099-S form is used for reporting proceeds from real estate transactions. Similar to the 1099-SA, the 1099-S helps ensure taxpayer awareness of taxable sales. Both forms reflect substantial financial movements and are instrumental in ensuring accurate tax filings. For those engaging in significant financial decisions, understanding these forms helps mitigate potential tax filing issues.

When filling out the IRS 1099-SA form, there are important guidelines to follow to ensure accuracy and compliance. Below are some helpful do's and don'ts:

The 1099-SA form, officially known as the "Distributions From an HSA, Archer MSA, or Medicare Advantage MSA," can create confusion for many taxpayers. Understanding it fully can help you navigate your tax responsibilities effectively. Here are five common misconceptions about the 1099-SA form:

By clearing up these misconceptions, you are better equipped to handle your tax responsibilities and make informed decisions regarding your health care accounts.

The IRS 1099-SA form is an important document primarily used for reporting distributions from Health Savings Accounts (HSAs), Archer Medical Savings Accounts (MSAs), and Medicare Advantage MSA accounts. Here are some key takeaways to consider when filling out and using this form:

By understanding these key points, you can ensure that you handle the IRS 1099-SA form correctly and avoid any potential issues during tax season.