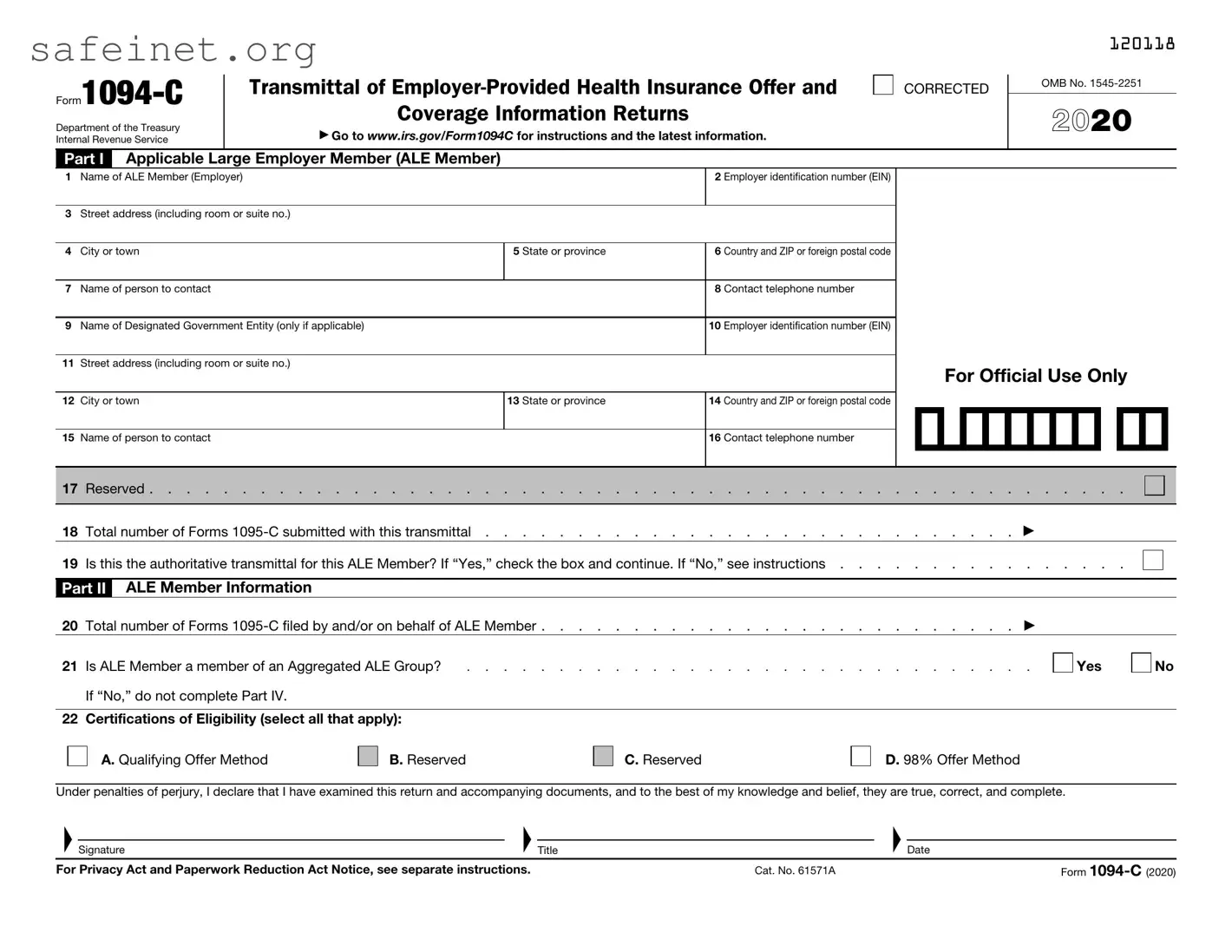

The IRS 1094-C form plays a crucial role in the realm of employer healthcare reporting, particularly in relation to the Affordable Care Act (ACA). Designed for applicable large employers, this form serves as a transmittal document for summarizing the information provided in individual employee forms, specifically the 1095-C forms. Employers utilize these forms to report on the health insurance coverage they offer to their employees. By compiling data about coverage, employee count, and related details, the 1094-C assists the IRS in assessing compliance with the ACA’s employer mandate. Its completion requires careful attention, as accuracy is vital. Notably, the form encompasses key sections that request essential information about employer status, the number of full-time employees, and the months during which healthcare coverage was offered. As the deadline for submission approaches each year, understanding the components and requirements of the 1094-C becomes increasingly important for businesses navigating the complexities of healthcare legislation.

|

Transmittal of |

||

|

|||

Department of the Treasury |

|

Coverage Information Returns |

|

|

▶ Go to www.irs.gov/Form1094C for instructions and the latest information. |

||

Internal Revenue Service |

|

||

|

|

|

|

Part I |

Applicable Large Employer Member (ALE Member) |

||

CORRECTED

120118

OMB No.

2020

1 Name of ALE Member (Employer) |

2 Employer identification number (EIN) |

|

|

3Street address (including room or suite no.)

4 |

City or town |

5 State or province |

6 |

Country and ZIP or foreign postal code |

|

|

|

|

|

7 |

Name of person to contact |

|

8 |

Contact telephone number |

|

|

|

|

|

9 |

Name of Designated Government Entity (only if applicable) |

|

10 |

Employer identification number (EIN) |

|

|

|

|

|

11Street address (including room or suite no.)

12 City or town |

13 State or province |

14 Country and ZIP or foreign postal code |

|

|

|

For Official Use Only

15Name of person to contact

16 Contact telephone number

17 |

Reserved |

|

|

|

|

|

|||

|

|

|

|

|

18 |

Total number of Forms |

|||

19 |

|

|

||

Is this the authoritative transmittal for this ALE Member? If “Yes,” check the box and continue. If “No,” see instructions |

|

|

||

Part II ALE Member Information

20 |

Total number of Forms |

. . . |

. |

. |

. . . . . . . |

▶ |

|

||||

21 |

Is ALE Member a member of an Aggregated ALE Group? |

. . . |

. |

. |

. . . . . . . |

. |

Yes |

||||

|

If “No,” do not complete Part IV. |

|

|

|

|

|

|

|

|

|

|

22 |

Certifications of Eligibility (select all that apply): |

|

|

|

|

|

|

|

|

||

|

A. Qualifying Offer Method |

|

B. Reserved |

|

C. Reserved |

|

|

|

D. 98% Offer Method |

|

|

|

|

|

|

|

|

|

|

||||

Under penalties of perjury, I declare that I have examined this return and accompanying documents, and to the best of my knowledge and belief, they are true, correct, and complete.

▲ |

|

▲ |

|

▲Date |

Signature |

Title |

No

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 61571A |

Form |

|

|

|

|

|

|

|

|

120218 |

Form |

|

|

|

|

Page 2 |

|||

Part III |

ALE Member |

|

|

|

|

|

||

|

|

(a) Minimum Essential Coverage |

(b) Section 4980H |

(c) Total Employee Count |

(d) Aggregated |

(e) Reserved |

||

|

|

Offer Indicator |

|

|||||

|

|

|

Employee Count for ALE Member |

for ALE Member |

Group Indicator |

|

||

|

|

|

|

|

|

|||

|

|

Yes |

|

No |

|

|

|

|

23 |

All 12 Months |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24 |

Jan |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 |

Feb |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

Mar |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

27 |

Apr |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

28 |

May |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29 |

June |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

July |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

31 |

Aug |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

32 |

Sept |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

33 |

Oct |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34 |

Nov |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

Dec |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

|

|

120316 |

Form |

Page 3 |

|

Part IV |

Other ALE Members of Aggregated ALE Group |

|

Enter the names and EINs of Other ALE Members of the Aggregated ALE Group (who were members at any time during the calendar year).

Name |

EIN |

Name |

36 |

|

51 |

|

||

37 |

|

52 |

38 |

|

53 |

39 |

|

54 |

40 |

|

55 |

41 |

|

56 |

42 |

|

57 |

43 |

|

58 |

44 |

|

59 |

45 |

|

60 |

46 |

|

61 |

47 |

|

62 |

48 |

|

63 |

49 |

|

64 |

50 |

|

65 |

|

|

|

EIN

Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS 1094-C form is used to report health coverage information to the IRS under the Affordable Care Act (ACA). |

| Filing Requirement | Applicable to employers with 50 or more full-time employees, including full-time equivalent employees. |

| Due Date | The form must be filed by February 28 if submitted on paper, and by March 31 if filed electronically. |

| Information Included | The form collects data about the employer, the number of full-time employees, and the health coverage offered. |

| Relation to 1095-C | Form 1094-C serves as a cover sheet for the 1095-C forms submitted for each employee. |

| State-Specific Requirements | Some states, like California and Massachusetts, have additional filing requirements and laws related to health coverage reporting. |

| Punitive Measures | Failure to file may result in penalties imposed by the IRS, potentially up to $250 per form. |

| Record Keeping | Employers must keep copies of the 1094-C and 1095-C forms for at least three years. |

Completing the IRS 1094-C form can seem a bit daunting, but breaking it down into manageable steps can make the process smoother. Once you gather the necessary information and follow the steps outlined below, you'll be well on your way to submitting this form accurately.

What is the IRS 1094-C form?

The IRS 1094-C form serves as a transmittal form for the 1095-C forms that large employers must provide to the IRS. This is part of the Affordable Care Act (ACA) reporting requirements. Employers with 50 or more full-time employees, including full-time equivalent employees, utilize this form to demonstrate compliance with the employer mandates concerning health insurance coverage.

Who needs to file the 1094-C form?

Large employers, defined as those with 50 or more full-time employees, are required to file the 1094-C form. Additionally, employers that are part of a controlled group or affiliated service group must file a single 1094-C for the entire group. If you qualify as an applicable large employer (ALE), submitting this form is crucial to report the health insurance coverage you offer to your employees.

What information is needed to complete the 1094-C form?

To complete the 1094-C form, employers must provide detailed information about their organization, including the name, address, and Employer Identification Number (EIN). They must indicate the number of employees during the calendar year, the months that health coverage was available, and other relevant details regarding their health plans. This data ensures the IRS understands the coverage offered to employees and whether it meets ACA standards.

When is the deadline for filing the 1094-C form?

The deadline for filing the 1094-C form with the IRS is generally February 28 of the year following the calendar year being reported. However, if you file electronically, this deadline extends to March 31. It’s essential to adhere to these deadlines to avoid potential penalties for late or incomplete filings.

What happens if I fail to file the 1094-C form?

Failing to file the 1094-C form may lead to penalties from the IRS. Employers may incur a penalty for each form not filed by the deadline. Additionally, not submitting this form can affect your standing with the IRS regarding compliance with the ACA, which may have implications for your health plan offerings and tax status. It’s advisable to ensure timely and accurate filing to prevent these issues.

Incorrect Employer Identification Number (EIN): Many individuals fail to double-check their EIN, resulting in errors. This number is crucial for proper tax identification, and a mistake can lead to significant delays.

Missing Parts III Details: Not providing enough detail in Part III regarding the covered individuals can cause complications. It's essential to ensure all required employee information is accurately reported.

Confusing Offer of Coverage Codes: Selecting the wrong codes in Part II can lead to misunderstandings about health coverage offerings. Familiarize yourself with the various codes to ensure accurate reporting.

Incorrect Reporting of Aggregated Groups: Businesses with multiple entities under common control might overlook accurate reporting of aggregated groups. This oversight can misrepresent the health care coverage provided.

Failure to Provide Signature: Forgetting to sign the form is a common error. A signed form is critical for validation and compliance, so make checking this step a priority.

Not Keeping Copies: Many forget to retain copies of submitted forms for their records. Keeping copies is important for future reference and in case of audits.

The IRS 1094-C form is a crucial document for applicable large employers as it helps report coverage under the Affordable Care Act (ACA). In addition to the 1094-C form, several other forms and documents often accompany it to ensure compliance with tax regulations related to health care coverage. Understanding these forms is essential for proper reporting and compliance.

Each of these forms and documents plays a specific role in the broader context of health care compliance and reporting. Familiarity with them not only safeguards against potential financial penalties but also supports a harmonious relationship between employers and employees regarding health coverage understanding.

The IRS 1095-A form is related to health coverage offered through the Health Insurance Marketplace. It provides information about the coverage, including who is covered and what the premium costs are. Like the 1094-C, it helps the IRS track compliance with the Affordable Care Act. Individuals use the 1095-A when filing their taxes to reconcile premium tax credits received during the year.

The IRS 1095-B form serves as proof of minimum essential coverage. Issued by health insurers or government programs, it details who is covered under the health plan. Similar to the 1094-C, it confirms compliance with health coverage requirements mandated by the Affordable Care Act, assisting taxpayers in demonstrating that they had coverage throughout the year.

The IRS 1095-C form is closely related to 1094-C, as both are used by applicable large employers (ALEs). The 1095-C provides information about the health insurance offered to employees. It informs the IRS and employees about the coverage's affordability and minimum value. Together with the 1094-C, these forms help ensure that employers meet their obligations under the Affordable Care Act.

The IRS W-2 form reports wages and tax withheld from employees’ paychecks. While it does not focus on health coverage specifically, it is similar in that it communicates vital employment and income information to both the IRS and the employee. The W-2 assists in determining eligibility for certain tax benefits that may relate to health insurance costs, just as the 1094-C aids in reporting insurance information.

The IRS 941 form is the Employer's Quarterly Federal Tax Return. It documents employment taxes withheld from employee paychecks. Similarly to the 1094-C, the 941 highlights employer responsibilities regarding employee compensation and tax obligations. Both forms are crucial in ensuring compliance with federal regulations, although they focus on different aspects of employment and associated benefits.

The Form 990 is a public document that tax-exempt organizations, including charities and non-profits, file with the IRS. It includes financial information about the organization’s operations, including employee benefits. While the significance of 990 does not lie directly in health insurance, the reporting requirements draw parallels in terms of transparency and accountability in providing benefits, as does the 1094-C for employers.

The Schedule C form is for sole proprietors to report income and expenses. Though it focuses on individual income, it also requires reporting of health insurance deductions. This connection to health coverage is similar to that of the 1094-C which outlines employer-offered coverage. Both forms allow taxpayers to account for health expenses related to their financial responsibilities.

The IRS 1040 form is the standard individual income tax return form. Taxpayers use it to report their annual income and claim deductions, such as those for health insurance premiums. While 1094-C focuses on employer-provided health coverage, both documents play essential roles in helping taxpayers report compliance with healthcare regulations and assess their tax situations.

When filling out the IRS 1094-C form, it's essential to be meticulous. This document is crucial for reporting information about your employer-sponsored health coverage. Here are six important things to consider while completing it:

Completing the IRS 1094-C form accurately is vital. By following these guidelines, you can help ensure compliance and avoid unnecessary complications.

The IRS 1094-C form is important for large employers in relation to the Affordable Care Act (ACA). However, several misconceptions surround this form. Here are seven common misunderstandings:

Understanding these misconceptions can help employers navigate their responsibilities related to the IRS 1094-C form more effectively.

Here are ten key takeaways to keep in mind when filling out and using the IRS 1094-C form:

Staying informed and cautious can help you navigate the process more effectively.