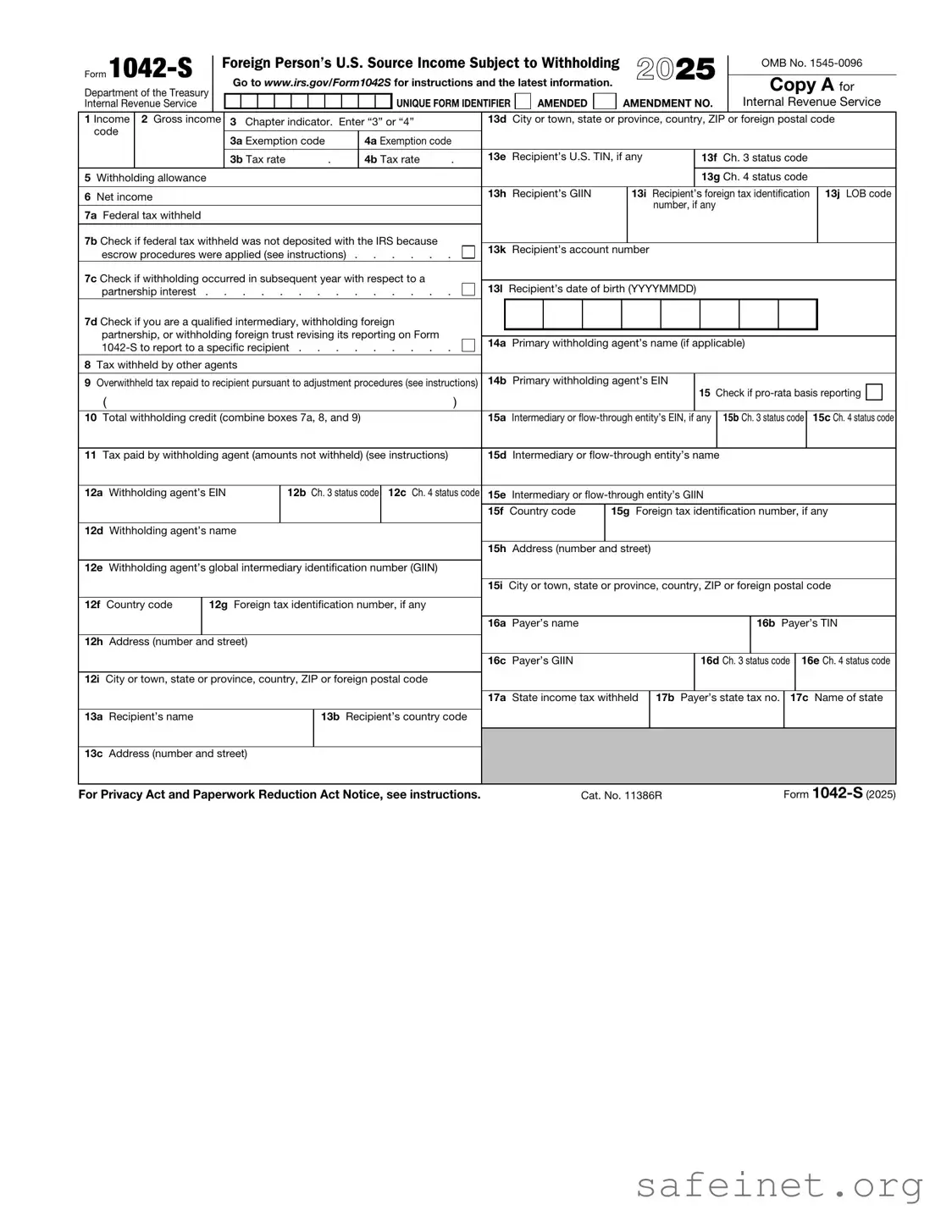

The IRS 1042-S form plays a crucial role in the reporting of income paid to non-resident aliens and foreign entities. This form is primarily used to report amounts subject to withholding, including interest, dividends, rents, and royalties, which may be earned by individuals or organizations outside of the United States. It is essential for U.S. withholding agents to accurately complete and file this form to ensure compliance with federal tax regulations. Each recipient of income must receive a copy of the 1042-S, which details the income they received and the amount withheld for tax purposes. The form also includes critical information such as the recipient's name, address, and taxpayer identification number, along with the specific type of income and the applicable tax rate. Timely and accurate submission of the 1042-S helps facilitate proper tax reporting and can prevent potential penalties for both the withholding agent and the recipient.

|

|

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2025 |

|

|

OMB No. |

|||||||||||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||||||||||||

Department of the Treasury |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Copy A for |

||||||||||

Form |

|

|

Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

|

|

|

||||||||||||||||||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

AMENDED |

|

|

AMENDMENT NO. |

|

|

Internal Revenue Service |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 Income |

2 Gross income |

|

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13d City or town, state or province, country, ZIP or foreign postal code |

|||||||||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13e Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13h |

Recipient’s GIIN |

|

13i |

Recipient’s foreign tax identification |

13j LOB code |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

13k Recipient’s account number |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

escrow procedures were applied (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

|||||||||||||||||||||||||||

partnership interest . |

. . . . . . . . . . . . . |

|

|

|

|

|

|

|

||||||||||||||||||||||||||

7d Check if you are a qualified intermediary, withholding foreign |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

partnership, or withholding foreign trust revising its reporting on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

14a Primary withholding agent’s name (if applicable) |

||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

8Tax withheld by other agents

9 Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions) |

14b |

Primary withholding agent’s EIN |

15 Check if |

|

|

|||||||

|

( |

|

) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

10 |

Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

15a |

Intermediary or |

15b Ch. 3 status code |

15c Ch. 4 status code |

|||||

|

|

|

|

|

|

|

|

|||||

11 |

Tax paid by withholding agent (amounts not withheld) (see instructions) |

15d |

Intermediary or |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12a Withholding agent’s EIN |

12b Ch. 3 status code |

12c Ch. 4 status code |

15e |

Intermediary or |

||||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

15f Country code |

15g Foreign tax identification number, if any |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12d Withholding agent’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

15h |

Address (number and street) |

||||||

12e Withholding agent’s global intermediary identification number (GIIN)

|

|

|

|

|

15i |

City or town, state or province, country, ZIP or foreign postal code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12f Country code |

12g Foreign tax identification number, if any |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

16a Payer’s name |

|

16b Payer’s TIN |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12h |

Address (number and street) |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16c Payer’s GIIN |

16d Ch. 3 status code |

|

16e Ch. 4 status code |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12i |

City or town, state or province, country, ZIP or foreign postal code |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

17a State income tax withheld |

17b Payer’s state tax no. |

|

17c Name of state |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

13a |

Recipient’s name |

|

13b Recipient’s country code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13c |

Address (number and street) |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||||||

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Cat. No. 11386R |

|

|

Form |

||||||||

Form |

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2025 |

|

|

OMB No. |

||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

|

Copy B |

||||||||||||||||||||||||||||||

Department of the Treasury |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

|

|

AMENDED |

|

|

AMENDMENT NO. |

|

|

for Recipient |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

1 Income |

2 Gross income |

|

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13d City or town, state or province, country, ZIP or foreign postal code |

|||||||||||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13e Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13h |

Recipient’s GIIN |

|

13i |

Recipient’s foreign tax identification |

13j LOB code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

13k Recipient’s account number |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

escrow procedures were applied (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

|||||||||||||||||||||||||||||

partnership interest . |

. . . . . . . . . . . . . |

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

7d Check if you are a qualified intermediary, withholding foreign |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

partnership, or withholding foreign trust revising its reporting on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

14a Primary withholding agent’s name (if applicable) |

||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

8Tax withheld by other agents

9 Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions) |

14b |

Primary withholding agent’s EIN |

15 Check if |

|

|

|||||||

|

( |

|

) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

10 |

Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

15a |

Intermediary or |

15b Ch. 3 status code |

15c Ch. 4 status code |

|||||

|

|

|

|

|

|

|

|

|||||

11 |

Tax paid by withholding agent (amounts not withheld) (see instructions) |

15d |

Intermediary or |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12a Withholding agent’s EIN |

12b Ch. 3 status code |

12c Ch. 4 status code |

15e |

Intermediary or |

||||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

15f Country code |

15g Foreign tax identification number, if any |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12d Withholding agent’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

15h |

Address (number and street) |

||||||

12e Withholding agent’s global intermediary identification number (GIIN)

|

|

|

|

|

|

15i City or town, state or province, country, ZIP or foreign postal code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

12f Country code |

|

12g Foreign tax identification number, if any |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16a Payer’s name |

|

|

16b Payer’s TIN |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

12h |

Address (number and street) |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16c Payer’s GIIN |

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

||

|

|

|

|

|

|

|

|

|

|

|

||

12i |

City or town, state or province, country, ZIP or foreign postal code |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17a State income tax withheld |

17b Payer’s state tax no. |

|

17c Name of state |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

13a |

Recipient’s name |

|

13b Recipient’s country code |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

13c |

Address (number and street) |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

||||

(keep for your records) |

|

|

|

|

|

|

|

Form |

||||

U.S. Income Tax Filing Requirements

Generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with U.S. income, including income that is effectively connected with the conduct of a trade or business in the United States, must file a U.S. income tax return. However, a return is generally not required to be filed by a nonresident alien individual, nonresident alien fiduciary, or foreign corporation if such person was not engaged in a trade or business in the United States at any time during the tax year and if the tax liability of such person was fully satisfied by the withholding of U.S. tax at the source. See the instructions for Forms

En règle générale, toute personne physique étrangère non résidente, tout fiduciaire étranger non résident et toute société étrangère ayant des revenus américains, y compris des revenus effectivement liés à la conduite d’un commerce ou d’une entreprise aux

Explanation of Codes

Box 1. Income Code.

Code

01Interest paid by U.S.

02Interest paid on real property mortgages

03Interest paid to controlling foreign corporations

04Interest paid by foreign corporations

05Interest on

|

22 |

Interest paid on deposit with a foreign branch of a domestic |

|

Interest |

30 |

corporation or partnership |

|

Original issue discount (OID) |

|||

|

29 |

Deposit interest |

|

|

31 |

||

|

33 |

Substitute |

|

|

51 |

Interest paid on certain actively traded or publicly offered |

|

|

|

securities1 |

|

|

54 |

Substitute |

|

|

|

or publicly offered securities1 |

|

Dividend |

06 |

Dividends paid by U.S. |

|

07 |

Dividends qualifying for direct dividend rate |

||

|

|||

|

08 |

Dividends paid by foreign corporations |

Por lo general, toda persona que es un extranjero no residente, todo fiduciario extranjero no residente, y toda sociedad anónima extranjera que perciba ingresos estadounidenses, inclusive de los ingresos que son efectivamente conectados con la operación de un comercio o negocio ubicado en los Estados Unidos, debe presentar una declaración del impuesto estadounidense sobre los ingresos. Sin embargo, por lo general no se requiere que un individuo extranjero no residente, una sociedad anónima extranjera u organismo fideicomisario extranjero no residente presenten una declaración si dicha persona no participaba en ningún comercio o negocio ubicado en los Estados Unidos en ningún momento durante el año tributario, y la responsabilidad tributaria de dicha persona fuera liquidada completamente mediante la retención del impuesto estadounidense en la fuente del ingreso. Consulte las instrucciones de los Formularios 1120F y

Grundsätzlich muss jede natürliche Person ohne Wohnsitz im Land, jeder Treuhänder ohne Wohnsitz im Land und jede ausländische Gesellschaft mit Einkünften in den USA, einschließlich Einkünften, die tatsächlich mit der Ausübung einer gewerblichen oder geschäftlichen Tätigkeit in den Vereinigten Staaten in Zusammenhang stehen, eine

|

34 |

Substitute |

|

40 |

Other dividend equivalents under IRC section 871(m) |

Dividend |

52 |

Dividends paid on certain actively traded or publicly offered |

|

securities1 |

|

|

|

|

|

53 |

Substitute |

|

|

or publicly offered securities1 |

|

56 |

Dividend equivalents under IRC section 871(m) as a result of |

|

|

applying the combined transaction rules |

|

|

|

|

09 |

Capital gains |

|

10 |

Industrial royalties |

|

11 |

Motion picture or television copyright royalties |

|

12 |

Other royalties (for example, copyright, software, |

|

|

broadcasting, endorsement payments) |

Other |

13 |

Royalties paid on certain publicly offered securities1 |

14 |

Real property income and natural resources royalties |

|

|

15 |

Pensions, annuities, alimony, and/or insurance premiums |

|

16 |

Scholarship or fellowship grants |

|

17 |

Compensation for independent personal services2 |

|

18 |

Compensation for dependent personal services2 |

|

19 |

Compensation for teaching2 |

See back of Copy C for additional codes

1This code should only be used if the income paid is described in Regulations section

2If compensation that would otherwise be covered under Income Codes 17 through 20 is directly attributable to the recipient’s occupation as an artist or athlete, use Income Code 42 or 43 instead.

| Fact Name | Description |

|---|---|

| Purpose | The IRS 1042-S form is used to report income paid to foreign persons, including non-resident aliens and foreign entities. |

| Filing Requirement | U.S. withholding agents must file the 1042-S form if they make payments subject to withholding to foreign recipients. |

| Income Types | Common types of income reported on the 1042-S include interest, dividends, royalties, and certain compensation for services. |

| Deadline | The form must be filed with the IRS by March 15 of the year following the payment, and recipients must receive their copies by the same date. |

| State-Specific Forms | Some states may have their own forms for reporting similar income, governed by state tax laws. For example, California requires Form 592. |

| Withholding Tax Rates | The withholding tax rates reported on the form may vary based on tax treaties between the U.S. and the recipient's country of residence. |

| Penalties | Failure to file the 1042-S form or providing incorrect information can result in penalties for the withholding agent. |

Filling out the IRS 1042-S form requires careful attention to detail. This form is used to report income that is subject to withholding tax for non-resident aliens and foreign entities. After completing the form, it is essential to ensure that all information is accurate and submitted to the appropriate parties in a timely manner.

What is the IRS 1042-S form?

The IRS 1042-S form is used to report income that is subject to withholding for non-resident aliens and foreign entities. This includes various types of income such as interest, dividends, royalties, and compensation for services. Essentially, if you are a foreign individual or entity receiving income from U.S. sources, this form helps ensure that the appropriate taxes are withheld and reported to the IRS.

Who needs to file the 1042-S form?

Any U.S. withholding agent—such as an employer, financial institution, or other payer—who makes payments to foreign individuals or entities must file the 1042-S form. This includes payments made to non-resident aliens for services rendered, as well as payments made to foreign businesses for goods or services provided in the U.S.

When is the 1042-S form due?

The due date for filing the 1042-S form is typically March 15 of the year following the calendar year in which the income was paid. If you are filing electronically, you may have an extension until March 31. However, recipients of the 1042-S form should receive their copies by the same March 15 deadline, allowing them to report the income on their own tax returns.

How do I fill out the 1042-S form?

Filling out the 1042-S form involves several steps. You need to provide information about the withholding agent, the recipient of the income, and the type and amount of income paid. Each section must be completed accurately to ensure compliance with IRS regulations. You can find detailed instructions on the IRS website, which guide you through each part of the form.

What types of income are reported on the 1042-S form?

Common types of income reported on the 1042-S form include interest, dividends, royalties, and compensation for services. Additionally, it may include certain types of pensions, annuities, and scholarships. If you're unsure whether your income falls under this category, consult the IRS guidelines or a tax professional.

What happens if I don’t receive a 1042-S form?

If you believe you should receive a 1042-S form but do not, it's important to contact the withholding agent who made the payment. They are responsible for issuing the form. Without it, you may face challenges when filing your tax return, as you need this information to report your income accurately.

Can I amend a 1042-S form?

Yes, if you discover an error on a previously filed 1042-S form, you can amend it. You will need to file a new form indicating that it is an amended return. It’s crucial to correct any mistakes to avoid potential issues with the IRS and to ensure that the recipient has the correct information for their tax filings.

What should I do if I disagree with the information on my 1042-S form?

If you disagree with the information reported on your 1042-S form, first reach out to the withholding agent for clarification. They may be able to resolve the issue. If necessary, you can also dispute the information with the IRS by providing supporting documentation that substantiates your claim.

Is there a penalty for not filing the 1042-S form?

Yes, there are penalties for failing to file the 1042-S form or for filing it late. The IRS imposes fines based on how late the form is filed, and these penalties can add up quickly. Therefore, it’s essential to meet the filing deadlines and ensure that the information is accurate to avoid these financial repercussions.

Where can I find more information about the 1042-S form?

For more detailed information about the 1042-S form, you can visit the IRS website. They provide comprehensive resources, including instructions, FAQs, and guidelines for both withholding agents and recipients. Additionally, consulting a tax professional can provide personalized assistance and ensure compliance with all tax obligations.

Incorrect Recipient Information: One common mistake is providing inaccurate or incomplete information about the recipient. This includes errors in the name, address, or taxpayer identification number (TIN). Always double-check these details to ensure they match official documents.

Wrong Income Code: Each type of income has a specific code that must be used on the form. Using the wrong code can lead to confusion and potential penalties. Familiarize yourself with the list of income codes to select the appropriate one for the payment being reported.

Failure to Report All Income: Sometimes, individuals overlook certain payments or fail to report them altogether. It’s crucial to report all income paid to foreign persons, as missing information can lead to compliance issues. Review all transactions carefully to ensure nothing is left out.

Incorrect Tax Rate Applied: Applying the wrong withholding tax rate can create significant problems. Different types of income may be subject to different rates, and some may even be exempt. Make sure to verify the correct rate based on the recipient's status and the type of income.

The IRS 1042-S form is essential for reporting income paid to foreign persons. Along with this form, several other documents are often required to ensure compliance with tax regulations. Below is a list of these forms and documents, each serving a specific purpose in the reporting process.

Understanding these documents is crucial for accurate tax reporting and compliance. Properly completing and submitting the necessary forms can help avoid issues with the IRS and ensure that all parties meet their obligations.

The IRS 1099 form is a well-known document that reports various types of income other than wages, salaries, and tips. Similar to the 1042-S, the 1099 is used to inform the IRS about payments made to individuals or entities. Both forms are essential for tax reporting, ensuring that income is accurately tracked and reported. While the 1042-S focuses on foreign persons receiving U.S. income, the 1099 covers a broader range of income types, including interest, dividends, and non-employee compensation.

The W-2 form is another important document that shares similarities with the 1042-S. Employers use the W-2 to report wages paid to employees and the taxes withheld from those wages. Like the 1042-S, the W-2 provides critical information needed for tax filing. However, the W-2 is specific to U.S. citizens and residents, while the 1042-S is designed for non-resident aliens and foreign entities receiving U.S. income.

The IRS 1040 form is a personal income tax return used by U.S. citizens and residents to report their annual income. While the 1040 is a comprehensive document that covers various income sources and deductions, the 1042-S serves a more specialized purpose. Both forms require accurate reporting of income, but the 1042-S is specifically for foreign income, highlighting the different tax obligations for non-resident aliens.

The 1098 form is utilized to report mortgage interest paid, and it bears some resemblance to the 1042-S in its reporting function. Both documents provide essential information that taxpayers need when preparing their tax returns. The 1098 focuses on interest payments made on loans, while the 1042-S reports income paid to foreign persons, illustrating the diverse nature of tax reporting requirements.

The Schedule K-1 form is used to report income, deductions, and credits from partnerships, S corporations, estates, and trusts. Similar to the 1042-S, the Schedule K-1 provides detailed information to recipients about their share of income. Both forms help ensure that all parties involved report their income accurately, but the K-1 is specific to partnerships and pass-through entities, while the 1042-S is tailored for foreign recipients.

The 1095-A form is associated with health insurance coverage under the Affordable Care Act. It reports information about health insurance premiums and subsidies. While it may seem unrelated at first glance, both the 1095-A and the 1042-S are crucial for tax purposes. They provide necessary information to help individuals complete their tax returns accurately, though they pertain to very different areas of tax reporting.

The 1099-DIV form reports dividends and distributions to shareholders. Like the 1042-S, it is used to inform the IRS about income received by individuals. Both forms aim to ensure that income is reported correctly, but the 1099-DIV focuses specifically on dividend income, while the 1042-S is aimed at foreign individuals receiving various types of income from U.S. sources.

The 1099-INT form reports interest income earned by individuals. Similar to the 1042-S, it serves to inform the IRS about income that may not have been subject to withholding. Both forms play a vital role in tax compliance, ensuring that all sources of income are reported. However, the 1099-INT is specific to interest payments, whereas the 1042-S covers a broader range of payments made to foreign persons.

Filling out the IRS 1042-S form can be a bit daunting, but knowing what to do and what to avoid can make the process smoother. Here’s a helpful list to guide you:

By following these guidelines, you can navigate the IRS 1042-S form with confidence and ensure compliance with tax regulations.

The IRS 1042-S form can be confusing, and many people hold misconceptions about it. Here are four common misunderstandings:

Understanding these misconceptions can help clarify your obligations and rights regarding the 1042-S form. If you have questions or need assistance, consider reaching out to a tax professional.

The IRS 1042-S form is essential for reporting income paid to foreign persons. Here are some key takeaways to keep in mind:

Understanding these key points can help ensure compliance and avoid potential issues with the IRS.