The IRS Form 1041 is an essential tool for managing the financial responsibilities of estates and trusts in the United States. When an individual passes away, their assets often enter a transition period where they are managed by a personal representative or trustee. This is where Form 1041 comes into play, as it acts as a tax return for estates and trusts that generated income during the tax year. The form accounts for income, deductions, and credits, ensuring that the estate or trust fulfills its tax obligations. Additionally, beneficiaries may receive income distributions from estates or trusts, which are reported to the IRS using this form. Filing Form 1041 is not just a matter of compliance; it involves careful consideration of various tax implications that can influence both the estate’s and beneficiaries’ financial situations. Understanding the nuances of this form can be vital for effective estate administration and can help avoid potential legal pitfalls down the road.

Note: The form, instructions, or publication you are looking

for begins after this coversheet.

Please review the updated information below.

Reporting Excess Deductions on Termination of an Estate or Trust on Forms 1040,

Under Proposed Regulations

For tax year 2019, an excess deduction for IRC section 67(e) expenses is reported as a

For tax year 2018, an excess deduction for IRC section 67(e) expenses is reported as a

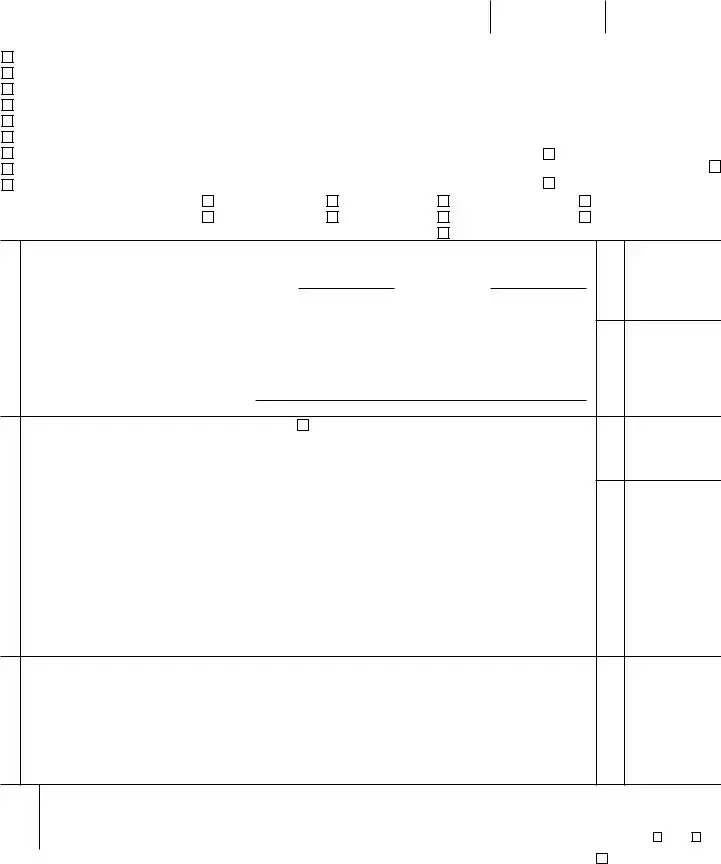

Form

1041 |

Department of the |

U.S. Income Tax Return for Estates and Trusts |

|

Go to www.irs.gov/Form1041 for instructions and the latest information. |

2019

OMB No.

A Check all that apply: |

For calendar year 2019 or fiscal year beginning |

, 2019, and ending |

, 20 |

||||

Decedent’s estate |

Name of estate or trust (If a grantor type trust, see the instructions.) |

|

C |

Employer identification number |

|||

Simple trust |

|

|

|

|

|

|

|

Complex trust |

Name and title of fiduciary |

|

|

D |

Date entity created |

||

Qualified disability trust |

|

|

|

|

|

|

|

ESBT (S portion only) |

Number, street, and room or suite no. (If a P.O. box, see the instructions.) |

|

E Nonexempt charitable and |

||||

Grantor type trust |

|

|

|

|

|

trusts, check applicable box(es). |

|

|

|

|

|

|

See instructions. |

||

Bankruptcy |

|

|

|

|

|

Described in sec. 4947(a)(1). Check here |

|

Bankruptcy |

City or town, state or province, country, and ZIP or foreign postal code |

|

|

if not a private foundation . . |

|||

Pooled income fund |

|

|

|

|

|

Described in sec. 4947(a)(2) |

|

B Number of Schedules |

F Check |

Initial return |

Final return |

Amended return |

|

Net operating loss carryback |

|

attached (see |

applicable |

Change in trust’s name |

Change in fiduciary |

Change in fiduciary’s name |

Change in fiduciary’s address |

||

instructions) |

boxes: |

||||||

G Check here if the estate or filing trust made a section 645 election |

Trust TIN |

|

|

||||

Income

Deductions

Tax and Payments

1 |

Interest income |

1 |

|

|

2a |

Total ordinary dividends |

2a |

||

b |

Qualified dividends allocable to: (1) Beneficiaries |

(2) Estate or trust |

|

|

3 |

Business income or (loss). Attach Schedule C (Form 1040 or |

3 |

|

|

4 |

Capital gain or (loss). Attach Schedule D (Form 1041) |

4 |

|

|

5Rents, royalties, partnerships, other estates and trusts, etc. Attach Schedule E (Form 1040 or

|

5 |

||

6 |

Farm income or (loss). Attach Schedule F (Form 1040 or |

6 |

|

7 |

Ordinary gain or (loss). Attach Form 4797 |

7 |

|

8 |

Other income. List type and amount |

|

8 |

9 |

Total income. Combine lines 1, 2a, and 3 through 8 |

9 |

|

10 |

Interest. Check if Form 4952 is attached |

. . . . . . . . . . . . . . . . . |

10 |

11 |

Taxes |

11 |

|

12 |

Fiduciary fees. If only a portion is deductible under section 67(e), see instructions |

12 |

|

13 |

Charitable deduction (from Schedule A, line 7) |

13 |

|

14Attorney, accountant, and return preparer fees. If only a portion is deductible under section 67(e),

|

see instructions |

14 |

|

||||

15a |

Other deductions (attach schedule). See instructions for deductions allowable under section 67(e) |

15a |

|||||

b |

Net operating loss deduction. See instructions |

15b |

|||||

16 |

Add lines 10 through 15b |

16 |

|

||||

17 |

Adjusted total income or (loss). Subtract line 16 from line 9 |

. . |

. . . |

17 |

|

|

|

18 |

Income distribution deduction (from Schedule B, line 15). Attach Schedules |

18 |

|

||||

19 |

Estate tax deduction including certain |

19 |

|

||||

20 |

Qualified business income deduction. Attach Form 8995 or |

20 |

|

||||

21 |

Exemption |

21 |

|

||||

22 |

Add lines 18 through 21 |

22 |

|

||||

23 |

Taxable income. Subtract line 22 from line 17. If a loss, see instructions |

23 |

|

||||

24 |

Total tax (from Schedule G, Part I, line 9) |

24 |

|

||||

25 |

2019 net 965 tax liability paid from Form |

25 |

|

||||

26 |

Total payments (from Schedule G, Part II, line 17) |

26 |

|

||||

27 |

Estimated tax penalty. See instructions |

27 |

|

||||

28 |

Tax due. If line 26 is smaller than the total of lines 24, 25, and 27, enter amount owed . . . . |

28 |

|

||||

29 |

Overpayment. If line 26 is larger than the total of lines 24, 25, and 27, enter amount overpaid . . |

29 |

|

||||

30 |

Amount of line 29 to be: a Credited to 2020 |

; |

b Refunded |

30 |

|

||

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

F |

|

|

|

|

May the IRS discuss this return |

||

|

|

|

|||||

|

|

|

|

with the preparer shown below? |

|||

Signature of fiduciary or officer representing fiduciary |

Date |

EIN of fiduciary if a financial institution |

|

See Instr. |

Yes |

No |

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

|

Check |

if |

PTIN |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

||

Use Only |

|

|

|

|

|

|

|||

Firm’s address |

|

|

|

Phone no. |

|

|

|

||

|

|

|

|

|

|

|

|||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11370H |

|

|

|

Form 1041 (2019) |

|

|||

Form 1041 (2019) |

Page 2 |

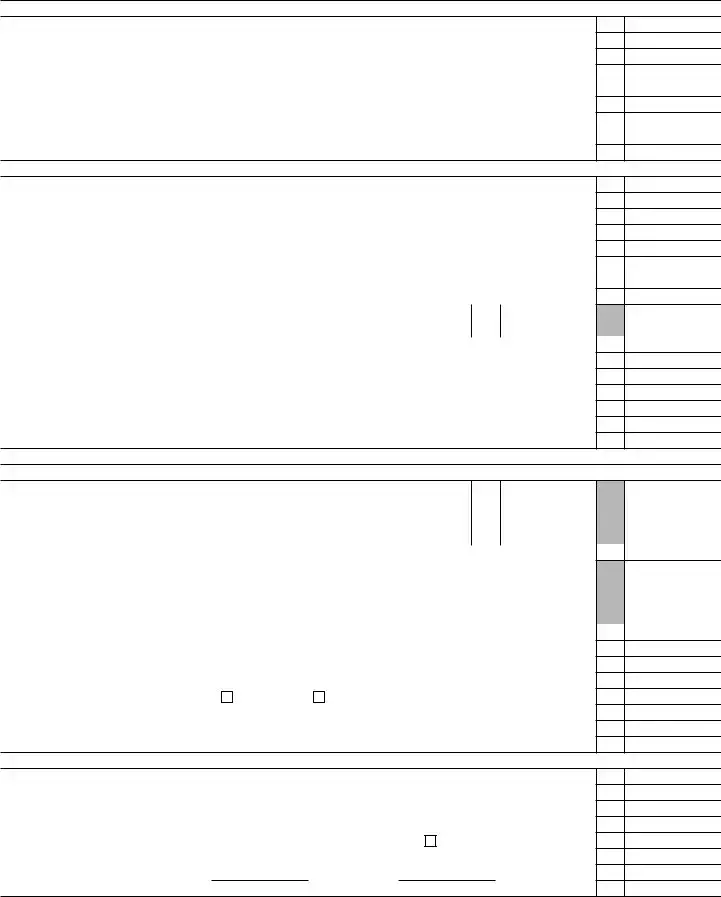

Schedule A Charitable Deduction. Don’t complete for a simple trust or a pooled income fund.

1Amounts paid or permanently set aside for charitable purposes from gross income. See instructions

2 |

|

3 |

Subtract line 2 from line 1 |

4Capital gains for the tax year allocated to corpus and paid or permanently set aside for charitable

purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Add lines 3 and 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6Section 1202 exclusion allocable to capital gains paid or permanently set aside for charitable purposes. See instructions . . . . . . . . . . . . . . . . . . . . . . . . .

7 Charitable deduction. Subtract line 6 from line 5. Enter here and on page 1, line 13 . . . . . .

1

2

3

4

5

6

7

Schedule B Income Distribution Deduction

1 |

Adjusted total income. See instructions |

2 |

Adjusted |

3 |

Total net gain from Schedule D (Form 1041), line 19, column (1). See instructions |

4 |

Enter amount from Schedule A, line 4 (minus any allocable section 1202 exclusion) |

5 |

Capital gains for the tax year included on Schedule A, line 1. See instructions |

6Enter any gain from page 1, line 4, as a negative number. If page 1, line 4, is a loss, enter the loss as a

positive number . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Distributable net income. Combine lines 1 through 6. If zero or less, enter

8If a complex trust, enter accounting income for the tax year as determined

|

under the governing instrument and applicable local law |

8 |

9 |

Income required to be distributed currently |

|

10 |

Other amounts paid, credited, or otherwise required to be distributed |

|

11 |

Total distributions. Add lines 9 and 10. If greater than line 8, see instructions |

|

12 |

Enter the amount of |

|

13 |

Tentative income distribution deduction. Subtract line 12 from line 11 |

|

14 |

Tentative income distribution deduction. Subtract line 2 from line 7. If zero or less, enter |

|

15 |

Income distribution deduction. Enter the smaller of line 13 or line 14 here and on page 1, line 18 . |

|

1

2

3

4

5

6

7

9

10

11

12

13

14

15

Schedule G Tax Computation and Payments (see instructions)

Part I — Tax Computation

1Tax:

a |

Tax on taxable income. See instructions |

1a |

|||

b |

Tax on |

1b |

|||

c |

Alternative minimum tax (from Schedule I (Form 1041), line 54) |

1c |

|||

d |

Total. Add lines 1a through 1c |

||||

2a |

Foreign tax credit. Attach Form 1116 |

2a |

|

||

b |

General business credit. Attach Form 3800 |

2b |

|

||

c |

Credit for prior year minimum tax. Attach Form 8801 |

2c |

|

||

d |

Bond credits. Attach Form 8912 |

2d |

|

||

e |

Total credits. Add lines 2a through 2d |

||||

3 |

Subtract line 2e from line 1d. If zero or less, enter |

||||

4 |

Tax on the ESBT portion of the trust (from ESBT Tax Worksheet, line 17). See instructions . . . . |

||||

5 |

Net investment income tax from Form 8960, line 21 |

||||

6 |

Recapture taxes. Check if from: |

Form 4255 |

Form 8611 |

||

7 |

Household employment taxes. Attach Schedule H (Form 1040 or |

||||

8 |

Other taxes and amounts due |

||||

9 |

Total tax. Add lines 3 through 8. Enter here and on page 1, line 24 |

||||

1d

2e

3

4

5

6

7

8

9

Part II — Payments

10 2019 estimated tax payments and amount applied from 2018 return . . . . . . . . . . .

11Estimated tax payments allocated to beneficiaries (from Form

12 |

Subtract line 11 from line 10 |

||

13 |

Tax paid with Form 7004. See instructions |

||

14 |

Federal income tax withheld. If any is from Form(s) 1099, check here |

. . . . . . . . . |

|

15 |

2019 net 965 tax liability from Form |

||

16 |

Other payments: a Form 2439 |

; b Form 4136 |

; Total . . |

17 |

Total payments. Add lines 12 through 15 and 16c. Enter here and on page 1, line 26 |

||

10

11

12

13

14

15

16c

17

Form 1041 (2019)

Form 1041 (2019) |

Page 3 |

Other Information |

Yes No |

1Did the estate or trust receive

Enter the amount of |

$ |

2Did the estate or trust receive all or any part of the earnings (salary, wages, and other compensation) of any

individual by reason of a contract assignment or similar arrangement? . . . . . . . . . . . . . . .

3At any time during calendar year 2019, did the estate or trust have an interest in or a signature or other authority over a bank, securities, or other financial account in a foreign country? . . . . . . . . . . . . . .

See the instructions for exceptions and filing requirements for FinCEN Form 114. If “Yes,” enter the name of the foreign country

4During the tax year, did the estate or trust receive a distribution from, or was it the grantor of, or transferor to, a

foreign trust? If “Yes,” the estate or trust may have to file Form 3520. See instructions . . . . . . . . .

5Did the estate or trust receive, or pay, any qualified residence interest on

the instructions for the required attachment . . . . . . . . . . . . . . . . . . . . . . .

6 If this is an estate or a complex trust making the section 663(b) election, check here. See instructions . .

7 To make a section 643(e)(3) election, attach Schedule D (Form 1041), and check here. See instructions . .

8If the decedent’s estate has been open for more than 2 years, attach an explanation for the delay in closing the

estate, and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 Are any present or future trust beneficiaries skip persons? See instructions . . . . . . . . . . . . .

10Was the trust a specified domestic entity required to file Form 8938 for the tax year (see the Instructions for

Form 8938)? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11a Did the estate or trust distribute S corporation stock for which it made a section 965(i) election? . . . . . .

bIf “Yes,” did each beneficiary enter into an agreement to be liable for the net tax liability? See instructions . . .

12Did the estate or trust make a section 965(i) election for S corporation stock held on the last day of the tax year?

See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13 ESBTs only. Does the ESBT have a nonresident alien grantor? If “Yes,” see instructions . . . . . . . .

14ESBTs only. Did the S portion of the trust claim a qualified business income deduction? If “Yes,” see instructions

Form 1041 (2019)

| Fact Name | Description |

|---|---|

| Purpose | The IRS 1041 form is used to report income, deductions, and tax liability of estates and trusts. |

| Filing Requirement | Form 1041 must be filed if the estate or trust generates $600 or more in income during the tax year. |

| Filing Deadline | The due date for filing is April 15 of the year following the tax year, unless it falls on a weekend or holiday. |

| Beneficiary Information | Income distributions to beneficiaries must be reported on Schedule K-1, which is included with Form 1041. |

| Governing Law | Federal tax law governs the filing of Form 1041, as per the Internal Revenue Code. |

| State-Specific Forms | Many states require their own forms for estate and trust taxes. Check state regulations for specifics. |

| Estimated Taxes | Estates and trusts may need to pay estimated taxes if they expect to owe $1,000 or more when filing Form 1041. |

| Amendments | Form 1041 can be amended by filing a corrected return using the same form. |

Filling out the IRS Form 1041 is an essential step for managing the income of a decedent's estate or a trust. After gathering the necessary financial information, the following steps will guide you through the process of completing the form accurately.

What is the IRS 1041 form?

The IRS 1041 form is used to report income, deductions, gains, losses, and other tax-related information for estates and trusts. When an estate or trust has generated more than $600 in income during the tax year, filing this form is required. The 1041 helps calculate taxes owed by the estate or trust and may also provide necessary information for beneficiaries.

Who needs to file Form 1041?

Form 1041 must be filed by the fiduciary of an estate or trust that has generated a gross income of $600 or more. It’s also needed if the estate has any income, regardless of the amount, that is taxable to the beneficiaries. Additionally, if the estate is comprised of a non-resident alien's estate, a Form 1041 must be filed even if there’s no taxable income.

What information is required to complete Form 1041?

Completing Form 1041 requires several pieces of information. You’ll need the name and address of the estate or trust, the Employer Identification Number (EIN), and the date of death of the decedent for estates. In addition, you’ll enter details about income received, such as interest, dividends, and rental income, along with any deductions the estate or trust is eligible to claim. Be prepared to address distributions to beneficiaries as well.

How is Form 1041 filed?

Form 1041 can be filed electronically via the IRS e-file system or by mailing a paper form to the applicable IRS address based on the estate's or trust's location. Each method has its own advantages, but electronic filing can expedite processing and reduce errors. Remember that deadlines will vary depending on the type of entity, so check the specific due dates for timely filing.

What are the consequences of not filing Form 1041?

Failing to file Form 1041 when required can lead to penalties and interest charges. The IRS imposes a penalty for late filing, which starts at $205 per month for each month the return is late. Additionally, if the estate or trust owes taxes and fails to report, it could lead to more severe consequences, such as audits or additional penalties for noncompliance.

Can beneficiaries receive distributions before Form 1041 is filed?

Yes, beneficiaries can receive distributions before Form 1041 is filed. However, they should be aware that the estate or trust must still file the form to report the income and distributions accurately. Beneficiaries will likely need this information for their personal tax returns, and the fiduciary should communicate clearly about any distributions made.

Not correctly identifying the type of entity filing the form. Trusts and estates differ in their tax obligations, and understanding the distinction is crucial.

Failing to report all income received by the estate or trust. All interest, dividends, and other income must be included to avoid discrepancies.

Omitting deductions and expenses. Many forget to list valid deductions, which can reduce the taxable income significantly.

Listing inaccurate beneficiary information. Double-check that names, Social Security numbers, and addresses are correct.

Neglecting to sign the form. An unsigned return is considered incomplete and can lead to delays or penalties.

Submitting the form late. Timeliness is important, as late submissions can incur penalties and interest on unpaid taxes.

Using the wrong year’s form. Always ensure you are using the correct version of the 1041 form for the tax year you are filing.

Not keeping copies of the submitted form and supporting documents. Keeping records can help resolve any future issues.

Ignoring state tax obligations. Some states may have additional forms or requirements, which must be addressed along with federal filings.

Relying solely on software or online services without review. While these tools can be helpful, it’s essential to review the output for accuracy.

The IRS Form 1041 is an essential document used by estates and trusts to report income, deductions, gains, and losses for the fiscal year. While the 1041 serves as the main reporting tool, several other forms and documents often accompany it to ensure comprehensive compliance with federal tax regulations. Below is a list of important forms typically used in conjunction with the IRS Form 1041.

Utilizing these forms and documents in conjunction with the IRS Form 1041 ensures that estates and trusts accurately report their financial activities. By maintaining thorough and detailed records, fiduciaries can navigate the complexities of tax compliance while supporting the interests of the beneficiaries involved.

The IRS 1040 form is a personal income tax return form used by individual taxpayers to report their annual income. Like the 1041, which is specifically for estates and trusts, the 1040 allows taxpayers to detail their income sources, claim deductions, and calculate taxes owed. Both forms require similar information regarding income types, such as wages, dividends, and investments. The IRS uses both these forms to assess how much income tax the taxpayer or entity is responsible for in a given year.

The IRS 1065 form, known as the partnership return of income, is used by partnerships to report their income, deductions, and losses. Similar to the 1041, which details financial activity for estates and trusts, the 1065 does not result in a direct tax liability for the partnership itself. Instead, it passes the income through to individual partners, who report their shares on their personal tax returns. This "pass-through" tax treatment creates a connection between the two forms, emphasizing the responsibilities of managing and reporting income in a collective entity.

The IRS Form 990 is an informational return required for tax-exempt organizations, including charities. Like the 1041, Form 990 ensures transparency in financial reporting, requiring organizations to disclose income, expenses, and assets. Both forms serve to hold respective entities accountable for financial activities and provide essential information to the IRS and the public. While the 1041 pertains to estates and trusts, Form 990 is specifically geared toward organizations that operate without profit motives.

The IRS Form 1065-B applies specifically to electing large partnerships and is a variation of the 1065. It handles the income and deductions for large partnerships that choose to file in this way. Similar to the 1041, it allows large partnerships to report their financial activities while disseminating information to partners, who then report their shares individually. Both forms facilitate proper tax filing processes for their respective entities, ensuring compliance with IRS regulations.

The IRS Form 1120 is the corporate income tax return for C corporations. This document shares similarities with the 1041 in that it details a tax entity's income, deductions, and tax liability. Both forms require meticulous documentation and reporting to assess the appropriate level of tax owed. The key difference lies in the entity type, as the 1120 is aimed at corporations while the 1041 focuses on estates and trusts, emphasizing the need for proper representation of different income-producing structures.

Finally, the IRS Form 709 is the gift tax return. While not a direct analog to the 1041, it relates to the management and reporting of financial transactions involving estates and gifts. Both forms require careful compliance with tax laws and reporting guidelines to accurately detail the financial activities of the taxpayer or entity. The 709 focuses on transfers made while the 1041 concerns the income generated from the assets of an estate or trust, connecting them through their roles in estate planning and tax obligations.

When filling out the IRS 1041 form, it's essential to approach the task with caution and care. This form is vital for estates and trusts, and getting it right can save time and avoid complications. Here’s a handy list of things to do and not do while completing this form:

By following these guidelines, you can navigate the complexities of the IRS 1041 form with greater confidence and accuracy.

The IRS Form 1041 is used for reporting income, deductions, gains, losses, and other tax-related information for estates and trusts. Despite its importance, several misconceptions persist. Here are seven common misunderstandings:

Addressing these misconceptions can help individuals better understand their obligations and make informed decisions regarding estate and trust taxation.

Filling out and utilizing the IRS 1041 form is crucial for the administration of estates and trusts. Here are some key takeaways to keep in mind:

By following these guidelines, individuals can navigate the complexities of the IRS 1041 form more effectively.