The IOU form is a simple yet effective tool for documenting informal loan agreements, capturing the essential details of borrowed funds between parties. By clearly outlining the amount borrowed, the names of the lender and borrower, and the date of the transaction, this form serves as an acknowledgment of debt. While the IOU may lack the legal complexities of a formal contract, it still holds significant value in various personal and informal financial situations. Often used among friends, family, or colleagues, the IOU form encourages transparency and accountability, fostering trust between the involved parties. Additionally, it can outline specific terms regarding repayment, such as deadlines or interest, although these are not always included. Properly completed, the IOU provides a basis for reminding borrowers of their obligations and can serve as an informal reference should disputes arise later on.

IOU Template

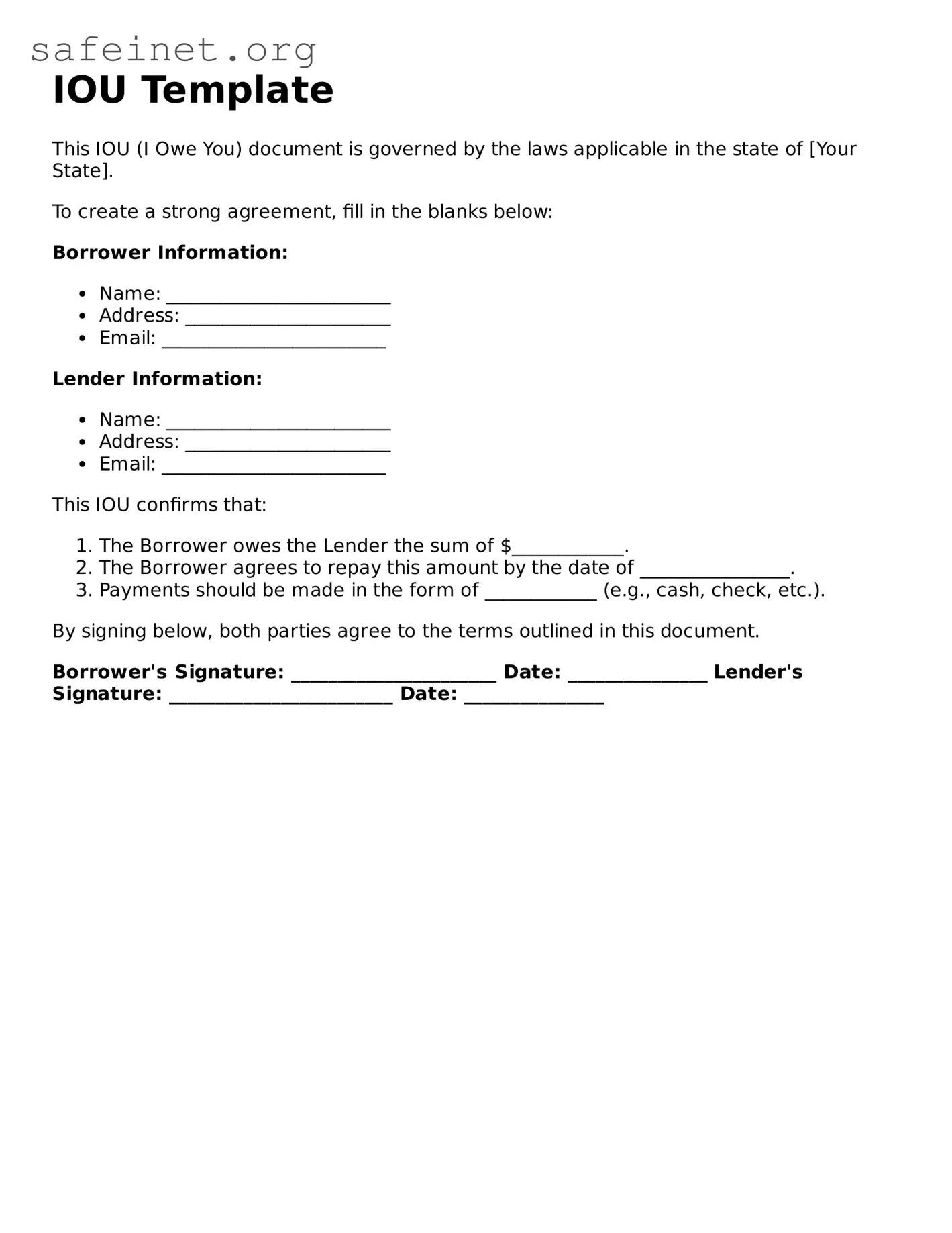

This IOU (I Owe You) document is governed by the laws applicable in the state of [Your State].

To create a strong agreement, fill in the blanks below:

Borrower Information:This IOU confirms that:

By signing below, both parties agree to the terms outlined in this document.

Borrower's Signature: ______________________ Date: _______________ Lender's Signature: ________________________ Date: _______________| Fact Name | Description |

|---|---|

| Definition | An IOU is a written acknowledgment of a debt, often informal and lacking legal structure. |

| Purpose | Individuals use an IOU to record a loan or obligation between two parties, creating a reference point. |

| Structure | Typically, an IOU includes the amount owed, the names of both parties, and the date of the loan. |

| Legality | While not a formal contract, in many states an IOU can serve as a legal document if properly executed. |

| State-Specific Forms | Different states may have additional requirements; it is advised to consult local laws. |

| Payment Terms | Many IOUs do not specify payment terms, which can lead to misunderstandings. |

| Acceptance | Both parties must agree to the terms outlined in the IOU for it to be valid and enforceable. |

| Governing Laws | The Uniform Commercial Code (UCC) and state contract laws govern IOUs in the United States. |

| Limitations | IOUs may not hold as much weight in court compared to formal contracts, particularly when larger amounts are involved. |

Filling out an IOU form is a straightforward process that helps document a financial obligation between individuals. Once completed, the form serves as a record of the amount owed, promoting transparency and accountability. Here are the steps to guide you through filling out the form effectively.

What is an IOU form?

An IOU form is a simple document that acknowledges a debt. It serves as a record between two parties, where one party owes money to another. The IOU typically includes the amount owed, the names of both parties, and the date. Unlike formal contracts, IOUs are often less detailed and may not require signatures, but they can still hold significant value in personal and informal transactions.

When should I use an IOU form?

You should use an IOU form when you lend money or goods and want to document the loan. It can be useful for informal arrangements, such as family or friends. An IOU helps clarify what was borrowed and establishes a timeline for repayment. While it’s not always necessary, using an IOU can prevent misunderstandings later on.

Is an IOU legally binding?

Generally, an IOU can be considered legally binding, but it depends on the details. If the form includes essential elements, such as the amount owed, the names of the parties, and the date, it may hold up in court. However, the lack of signatures or witnesses can make it difficult to enforce. Legal validity can also depend on state laws, so it's best to consult with a legal professional if you have specific concerns.

Can an IOU be modified?

Yes, an IOU can be modified if both parties agree to the changes. It's important to document any alterations to avoid confusion. This might involve writing an updated IOU or creating a new one altogether. Clear communication is essential when making changes, as both parties should understand and agree to the new terms.

What should I do if the IOU is not repaid?

If the IOU is not repaid, start by discussing the issue with the person who owes you money. Open and honest communication can often resolve the situation without further action. If that doesn’t work, review the IOU and consider sending a friendly reminder. If necessary, you may seek legal advice on enforcing the debt, depending on the amount and circumstances involved.

Failing to provide the borrower's name accurately. This can lead to confusion and make it difficult to enforce the agreement.

Not including the amount owed in both words and numbers. This can create ambiguity about the exact sum that is being borrowed.

Omitting the date of the loan. Without this crucial detail, tracking repayments could become challenging.

Neglecting to specify repayment terms. Clearly stating when and how the loan will be repaid can prevent disputes later.

Leaving out the lender's contact information. This information is vital for communication regarding the debt.

Not signing the form. A signature is essential for the document to be considered valid and legally binding.

Failing to have a witness or notarization when necessary. Some jurisdictions may require this for additional validation.

Overlooking additional conditions or agreements that may pertain to the loan. Including these can clarify expectations and responsibilities.

An IOU (I Owe You) form serves as a simple acknowledgment of a debt between two parties. However, several other documents complement the IOU, providing additional context or legal support for the agreement. Below are commonly used forms and documents that can enhance or clarify the understanding of a debt arrangement.

These accompanying documents serve various purposes, from ensuring clarity on repayment terms to providing formal records of agreements. Each plays a crucial role in facilitating fair and transparent financial transactions between parties.

One document similar to an IOU form is a promissory note. A promissory note is a written promise by one party to pay a certain amount of money to another party at a specified time or on demand. Like an IOU, it serves as a record of a debt; however, a promissory note often includes more formal terms, such as payment schedules and interest rates. While an IOU can be informal and simple, a promissory note typically holds more legal weight due to its structured nature.

Another comparable document is a loan agreement. This legal contract outlines the terms and conditions of a loan between the lender and borrower. While an IOU might simply state the amount owed, a loan agreement includes detailed terms regarding repayment, interest, and default scenarios. Loan agreements offer more protection to lenders since they define rights and responsibilities more clearly.

A personal check also bears similarities to an IOU form. Both documents signify an amount of money that one party owes to another. However, a check is a specific payment instrument that can be used to transfer funds directly from one bank account to another. Unlike an IOU, which often represents a promise to pay later, a check is a direct payment at the time it is written.

Similarly, a bill can be seen as a document akin to an IOU. A bill is an itemized statement of goods or services provided, along with the amount owed. While an IOU represents a general promise to pay, a bill specifies exactly what is being charged. Bills usually have due dates and can sometimes include the penalty for late payment.

Accounts receivable records often resemble an IOU as well. These records show the money owed to a business for services or goods provided on credit. Both documents track debts, but accounts receivable are typically maintained as part of a company’s financial records, reflecting amounts owed in a more structured context, often with payment terms and due dates.

Another relevant document is a receipt. When a transaction occurs, a receipt provides proof of payment. While an IOU can indicate that a payment is pending, a receipt serves as confirmation that a payment was made. Receipts are essential for keeping track of financial exchanges and can be used to validate claims in disputes.

A debt acknowledgment letter can serve a similar purpose to an IOU. This document is used to acknowledge a debt and its terms. Like an IOU, it confirms that money is owed, but it may also include details like the amount, date, and any interest conditions. A debt acknowledgment letter can provide additional context that an IOU might lack.

A lien waiver can also be parallel to an IOU form in certain contexts. While it primarily pertains to real estate transactions, a lien waiver releases a party’s right to claim a debt. Both documents address debts; however, a lien waiver explicitly relinquishes any claim to property as collateral, whereas an IOU merely acknowledges a debt without affecting ownership rights.

Finally, an installment agreement shares similarities with an IOU. An installment agreement outlines how a debt will be paid back in smaller, manageable payments over time. Like an IOU, it reflects an obligation to repay a debt, but it provides structured payment terms and conditions for repayment. This clarity can help both parties feel more secure in their financial arrangements.

Filling out an IOU form can seem straightforward, but attention to detail is crucial. Here are eight essential tips for doing it right, as well as common mistakes to avoid.

The IOU form is often misunderstood, which can lead to confusion when it comes to borrowing and lending money. Here are eight common misconceptions about the IOU form:

Many people believe that an IOU is a formal contract that holds up in court. While it can demonstrate an agreement was made, it lacks the legal rigor of a contract and often lacks specific terms needed to enforce repayment.

Not all IOUs are created equal. They can vary widely in terms of detail and specificity. Some may include the date, amount, and repayment terms, while others might be vague and lack important information.

While having a signature can strengthen the IOU’s validity, an IOU doesn’t always require one. A verbal agreement or written note can still be considered an IOU, though proving the terms may be more challenging.

This misconception arises from the belief that IOUs are worthless. While they may not be enforceable in court, they can still serve as evidence of a debt and can lead to negotiations or informal settlements.

It is a common belief that IOUs are limited to personal loans between friends. However, businesses often use IOUs for informal transactions as well, especially when establishing trust and maintaining relationships.

Just because there is an IOU doesn't mean the debtor will remember to pay, nor does it ensure the debt will be tracked or managed properly without additional reminders and follow-ups.

While typically associated with money, IOUs can document various types of obligations, including services or goods owed, as long as both parties clearly understand the exchange.

Even for small amounts, having an IOU can prevent misunderstandings and maintain clarity between the parties involved. Consider it a good practice to document any borrowing, no matter the amount.

Understanding these common misconceptions can help individuals approach IOUs with clarity and transparency, ensuring that both lenders and borrowers are on the same page.

When dealing with an IOU form, understanding its components and proper usage is essential. Here are key takeaways to consider:

The above points serve as a guide to ensure that the IOU form is filled out properly and used effectively. Clarity and communication are key to making the agreement beneficial for both parties.

Family (Friends) Personal Loan Agreement - This form can prevent potential misunderstandings about borrowed money.

Employee Loan Agreement Pdf - Informs employees about tax implications of the loan agreement.