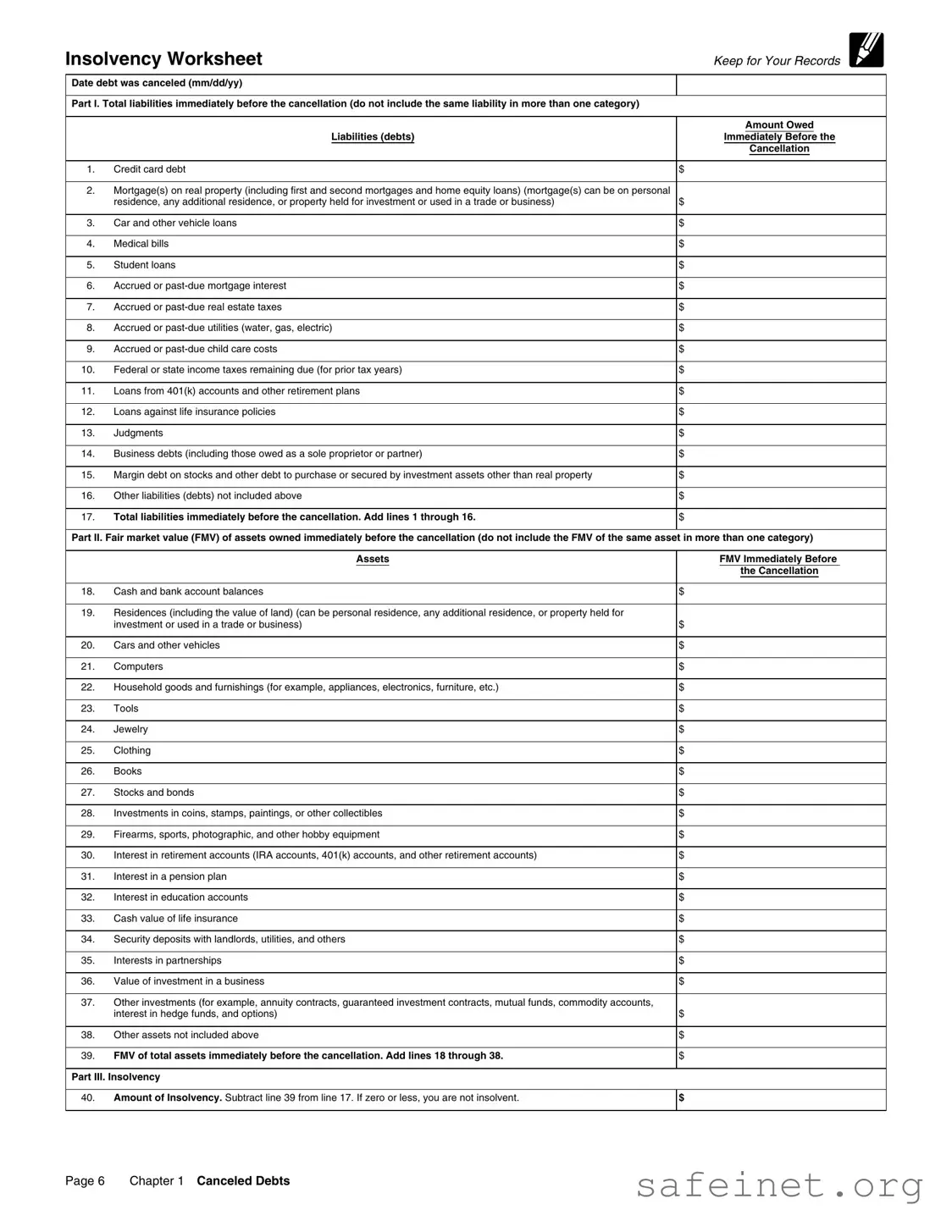

When dealing with financial distress, understanding the Insolvency IRS form becomes crucial for individuals and businesses alike. This form serves as a worksheet that helps you document your financial situation before any debt cancellation occurs. It consists of several parts, each designed to capture essential information about your liabilities and assets. In the first part, you will list all your outstanding debts, such as credit card balances, mortgages, vehicle loans, medical bills, and any other financial obligations you may have. Each category must be filled out accurately, as this will provide a comprehensive view of your total liabilities immediately prior to any cancellation of debt. The second part focuses on your assets, requiring you to assess the fair market value of everything you own, from cash and bank accounts to real estate and personal property. Finally, the form culminates in a calculation of your insolvency status by subtracting your total assets from your total liabilities. If the resulting figure is zero or less, it indicates that you are not insolvent, which can have significant implications for your tax obligations and financial recovery strategies. Completing this form with precision is essential, as it not only affects your current financial standing but also influences your future financial decisions.

Insolvency Worksheet

Keep for Your Records

Date debt was canceled (mm/dd/yy)

Part I. Total liabilities immediately before the cancellation (do not include the same liability in more than one category)

|

Amount Owed |

Liabilities (debts) |

Immediately Before the |

|

Cancellation |

|

|

1. Credit card debt |

$ |

2.Mortgage(s) on real property (including first and second mortgages and home equity loans) (mortgage(s) can be on personal

|

residence, any additional residence, or property held for investment or used in a trade or business) |

$ |

|

|

|

3. |

Car and other vehicle loans |

$ |

|

|

|

4. |

Medical bills |

$ |

|

|

|

5. |

Student loans |

$ |

|

|

|

6. |

Accrued or |

$ |

|

|

|

7. |

Accrued or |

$ |

|

|

|

8. |

Accrued or |

$ |

|

|

|

9. |

Accrued or |

$ |

|

|

|

10. |

Federal or state income taxes remaining due (for prior tax years) |

$ |

|

|

|

11. |

Loans from 401(k) accounts and other retirement plans |

$ |

|

|

|

12. |

Loans against life insurance policies |

$ |

|

|

|

13. |

Judgments |

$ |

|

|

|

14. |

Business debts (including those owed as a sole proprietor or partner) |

$ |

|

|

|

15. |

Margin debt on stocks and other debt to purchase or secured by investment assets other than real property |

$ |

|

|

|

16. |

Other liabilities (debts) not included above |

$ |

|

|

|

17. |

Total liabilities immediately before the cancellation. Add lines 1 through 16. |

$ |

Part II. Fair market value (FMV) of assets owned immediately before the cancellation (do not include the FMV of the same asset in more than one category)

|

Assets |

FMV Immediately Before |

|

|

the Cancellation |

|

|

|

18. |

Cash and bank account balances |

$ |

19.Residences (including the value of land) (can be personal residence, any additional residence, or property held for

|

investment or used in a trade or business) |

$ |

|

|

|

20. |

Cars and other vehicles |

$ |

|

|

|

21. |

Computers |

$ |

|

|

|

22. |

Household goods and furnishings (for example, appliances, electronics, furniture, etc.) |

$ |

|

|

|

23. |

Tools |

$ |

|

|

|

24. |

Jewelry |

$ |

|

|

|

25. |

Clothing |

$ |

|

|

|

26. |

Books |

$ |

|

|

|

27. |

Stocks and bonds |

$ |

|

|

|

28. |

Investments in coins, stamps, paintings, or other collectibles |

$ |

|

|

|

29. |

Firearms, sports, photographic, and other hobby equipment |

$ |

|

|

|

30. |

Interest in retirement accounts (IRA accounts, 401(k) accounts, and other retirement accounts) |

$ |

|

|

|

31. |

Interest in a pension plan |

$ |

|

|

|

32. |

Interest in education accounts |

$ |

|

|

|

33. |

Cash value of life insurance |

$ |

|

|

|

34. |

Security deposits with landlords, utilities, and others |

$ |

|

|

|

35. |

Interests in partnerships |

$ |

|

|

|

36. |

Value of investment in a business |

$ |

37.Other investments (for example, annuity contracts, guaranteed investment contracts, mutual funds, commodity accounts,

|

interest in hedge funds, and options) |

$ |

|

|

|

38. |

Other assets not included above |

$ |

|

|

|

39. |

FMV of total assets immediately before the cancellation. Add lines 18 through 38. |

$ |

Part III. Insolvency

40.Amount of Insolvency. Subtract line 39 from line 17. If zero or less, you are not insolvent.

$

Page 6 |

Chapter 1 Canceled Debts |

| Fact Name | Details |

|---|---|

| Purpose of the Form | The Insolvency Worksheet helps individuals determine their financial status by calculating total liabilities and fair market value of assets before debt cancellation. |

| Components of Liabilities | It includes various debts such as credit card debt, mortgages, car loans, medical bills, student loans, and more, ensuring no liability is counted more than once. |

| Asset Valuation | Individuals must assess the fair market value of their assets, including cash, real estate, vehicles, and personal belongings, prior to debt cancellation. |

| Calculation of Insolvency | Insolvency is determined by subtracting the total fair market value of assets from total liabilities. A result of zero or less indicates that the individual is not insolvent. |

| Governing Law | Insolvency laws vary by state. For example, in California, the governing law is the California Uniform Commercial Code, while in New York, it falls under the New York Debtor and Creditor Law. |

Filling out the Insolvency IRS form involves collecting financial information about your debts and assets. This process is essential to determine your financial status before any debt cancellation. Follow these steps carefully to complete the form accurately.

What is the Insolvency IRS form?

The Insolvency IRS form is a worksheet used to determine your financial status when a debt is canceled. It helps you assess whether you are insolvent, meaning your total liabilities exceed your total assets. This information is crucial for tax purposes, particularly when dealing with canceled debts that may be considered taxable income.

Why do I need to fill out this form?

Filling out the Insolvency IRS form is important if you have had any debts canceled. It allows you to establish whether you qualify for insolvency, which can help you avoid tax liability on the canceled debt. If your liabilities exceed your assets, you may not have to report the canceled debt as income.

What information do I need to provide?

You will need to provide details about your total liabilities immediately before the cancellation of the debt. This includes various types of debts, such as credit card debt, mortgages, vehicle loans, medical bills, and more. Additionally, you will need to list the fair market value of your assets, including cash, property, vehicles, and investments.

How do I calculate my total liabilities?

To calculate your total liabilities, list each type of debt you owe and its corresponding amount. Add these amounts together to get your total liabilities immediately before the cancellation. Be sure not to double-count any liabilities in different categories.

What is fair market value (FMV) and how do I determine it?

Fair market value (FMV) is the price that an asset would sell for on the open market. To determine FMV, consider recent sales of similar items or properties, or consult with a professional appraiser. It’s important to provide accurate values to ensure your insolvency calculation is correct.

What happens if my total liabilities exceed my total assets?

If your total liabilities exceed your total assets, you are considered insolvent. In this case, you may not have to report the canceled debt as income on your tax return. It’s essential to document your findings clearly on the form.

What if my assets equal my liabilities?

If your assets equal your liabilities, you are not considered insolvent. This means you may need to report the canceled debt as taxable income. It is crucial to keep accurate records and consult a tax professional if you are unsure about your situation.

How long should I keep this form?

It is advisable to keep the Insolvency IRS form and any supporting documents for at least three years after you file your tax return. This will ensure you have the necessary documentation if the IRS requests it or if you need to reference it in the future.

Can I fill out this form on my own, or do I need professional help?

You can fill out the form on your own if you feel comfortable with the information required. However, if your financial situation is complex or if you have concerns about accuracy, seeking assistance from a tax professional may be beneficial. They can provide guidance tailored to your specific circumstances.

Where can I find additional resources or help regarding the Insolvency IRS form?

You can find additional resources on the IRS website, which provides guidance on tax-related issues, including insolvency. Additionally, many tax professionals and financial advisors can offer personalized assistance and advice regarding your situation.

Neglecting to List All Liabilities: One common mistake is failing to include every liability. Each debt should be accounted for in its appropriate category. Omitting even a single liability can lead to inaccuracies in your insolvency calculation.

Double-Counting Debts: On the flip side, some individuals mistakenly list the same debt in multiple categories. This can skew the total liabilities and misrepresent your financial situation.

Inaccurate Valuation of Assets: It’s essential to provide an accurate fair market value (FMV) for each asset. Overestimating or underestimating the value can impact the insolvency determination significantly.

Missing Out on Assets: Just as it’s crucial to list all liabilities, you must also include all assets. Forgetting to mention any assets, even small ones, can affect your overall financial picture.

Using Outdated Values: When assessing the FMV of assets, using outdated or irrelevant values can lead to incorrect conclusions about your financial status. Ensure you base your values on current market conditions.

Ignoring Tax Implications: Some people overlook the tax consequences of canceled debts. Understanding how these debts impact your tax obligations is vital for accurate reporting.

Failing to Review Before Submission: Lastly, not reviewing the completed form before submission is a frequent oversight. A careful review can catch errors and ensure accuracy, preventing future complications.

When dealing with the Insolvency IRS form, several additional documents may be necessary to provide a complete picture of your financial situation. These forms can help clarify your liabilities and assets, ensuring accurate reporting and compliance with tax regulations. Below is a list of commonly used documents alongside the Insolvency form.

These documents work together to give a comprehensive view of your financial status, especially when addressing insolvency issues. Having them organized and ready can facilitate a smoother process when filing your taxes and managing your debts.

The IRS Form 982, Reduction of Tax Attributes Due to Discharge of Indebtedness, shares similarities with the Insolvency Worksheet. Both documents are used to address the impact of canceled debts on an individual’s financial situation. Form 982 allows taxpayers to reduce their tax attributes when debts are discharged, ensuring that they do not face unexpected tax liabilities. Just like the Insolvency Worksheet, it requires detailed information about liabilities and assets, helping taxpayers understand their financial standing after debt cancellation.

The Bankruptcy Petition is another document that closely resembles the Insolvency Worksheet. When individuals file for bankruptcy, they must provide a comprehensive list of their debts and assets. This petition serves to outline their financial situation and is crucial for determining the course of the bankruptcy process. Similar to the Insolvency Worksheet, it requires a thorough inventory of liabilities and assets to assess the individual’s insolvency status and eligibility for debt relief.

The Financial Statement, often used in loan applications, also mirrors the Insolvency Worksheet in its structure and purpose. This document requires individuals to detail their income, expenses, assets, and liabilities. Lenders use this information to evaluate the applicant's financial health. Like the Insolvency Worksheet, it provides a snapshot of an individual’s financial condition, making it easier to understand their ability to repay debts.

The Debt Validation Letter serves a similar function in terms of assessing liabilities. When a consumer disputes a debt, they can request validation from the creditor, which requires the creditor to provide proof of the debt. This process helps individuals clarify their financial obligations, akin to how the Insolvency Worksheet helps individuals identify their debts before cancellation. Both documents aim to ensure transparency and accuracy in financial dealings.

The Loan Modification Application also aligns with the Insolvency Worksheet by requiring detailed information about debts and assets. When homeowners seek to modify their mortgage terms, they must disclose their financial situation, including liabilities and income. This information is crucial for lenders to assess eligibility for modification. The format and information required are similar, focusing on achieving a fair assessment of financial hardship.

Finally, the Credit Counseling Intake Form resembles the Insolvency Worksheet in its purpose of evaluating an individual’s financial situation. Credit counseling often involves assessing debts and assets to create a plan for managing finances. This form helps counselors understand the individual’s financial landscape, similar to how the Insolvency Worksheet provides a comprehensive overview of liabilities and assets before debt cancellation.

When filling out the Insolvency IRS form, careful attention to detail is crucial. Here are some important dos and don'ts to consider:

Filling out the Insolvency IRS form requires careful attention to detail. Here are six key takeaways to keep in mind: