The Indiana Promissory Note form is a crucial document for anyone involved in lending or borrowing money in the state. This form outlines the terms of a loan agreement between a borrower and a lender, ensuring that both parties have a clear understanding of their rights and responsibilities. Key aspects of the form include the principal amount, the interest rate, and the repayment schedule, which all play a vital role in determining how and when the borrower will repay the loan. Additionally, the form may address any late fees, prepayment options, and consequences for defaulting on the loan. By using this standardized form, individuals can protect their interests and establish a legally binding agreement that can help prevent misunderstandings down the line. Understanding the Indiana Promissory Note is essential for anyone looking to navigate the lending process effectively and responsibly.

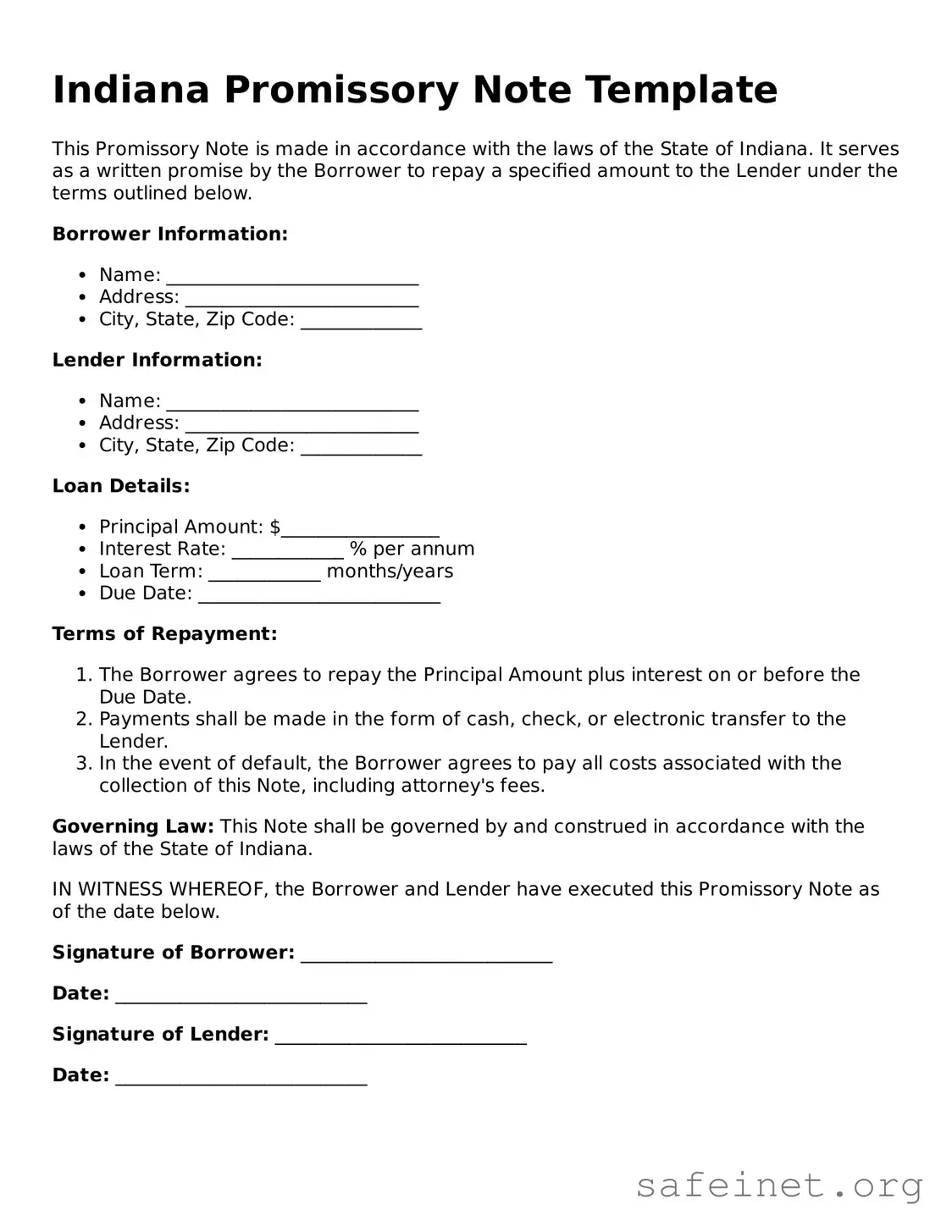

Indiana Promissory Note Template

This Promissory Note is made in accordance with the laws of the State of Indiana. It serves as a written promise by the Borrower to repay a specified amount to the Lender under the terms outlined below.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Indiana.

IN WITNESS WHEREOF, the Borrower and Lender have executed this Promissory Note as of the date below.

Signature of Borrower: ___________________________

Date: ___________________________

Signature of Lender: ___________________________

Date: ___________________________

| Fact Name | Description |

|---|---|

| Definition | An Indiana Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Governing Law | The Indiana Uniform Commercial Code (UCC) governs promissory notes in Indiana, specifically under Article 3. |

| Essential Elements | To be valid, a promissory note must include the amount owed, the interest rate (if any), the due date, and the signatures of the parties involved. |

| Types of Promissory Notes | Indiana recognizes various types of promissory notes, including secured and unsecured notes, depending on whether collateral is involved. |

| Enforceability | A properly executed promissory note is legally enforceable in Indiana, meaning the lender can take legal action if the borrower defaults. |

| Statute of Limitations | In Indiana, the statute of limitations for enforcing a promissory note is generally six years from the date of default. |

After completing the Indiana Promissory Note form, ensure that both parties retain a copy for their records. This document will serve as a formal agreement regarding the loan terms.

What is a Promissory Note in Indiana?

A Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a future date or on demand. In Indiana, this document outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any penalties for late payment. It serves as a legal contract between the borrower and the lender, ensuring that both parties understand their rights and obligations.

How do I fill out an Indiana Promissory Note?

To fill out an Indiana Promissory Note, start by entering the date of the agreement at the top of the form. Next, provide the names and addresses of both the borrower and the lender. Clearly state the principal amount being borrowed and the interest rate, if applicable. Specify the repayment terms, including how often payments will be made and the due dates. Finally, include any additional terms or conditions, such as late fees or prepayment options. It’s crucial to review the completed note for accuracy before signing.

Is it necessary to have a witness or notarization for the Promissory Note?

While Indiana law does not require a Promissory Note to be notarized or witnessed to be legally binding, having a notary public witness the signatures can add an extra layer of protection. This can help prevent disputes about the authenticity of the signatures or the terms of the agreement. It is advisable to consult with a legal professional if you have any concerns about the validity of the document.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. The lender may initiate legal action to recover the owed amount, which could involve filing a lawsuit. The Promissory Note may also specify certain remedies in the event of default, such as late fees or acceleration of the loan, which requires the borrower to pay the full balance immediately. It’s important for both parties to understand the consequences of default before signing the note.

Failing to include the borrower's name correctly. It is essential to ensure that the name matches the legal identification documents to avoid future disputes.

Neglecting to specify the loan amount. This detail must be clearly stated to prevent any misunderstandings about how much is owed.

Omitting the interest rate or not indicating if the loan is interest-free. This information is crucial for both parties to understand the financial implications of the agreement.

Not defining the repayment terms. Clear terms regarding when and how payments will be made help to establish expectations and responsibilities.

Forgetting to include a due date for the loan repayment. A specific date helps to clarify when the borrower is expected to fulfill their obligation.

Leaving out the signature of the borrower and, if applicable, the lender. Signatures validate the agreement and confirm that both parties consent to the terms.

Not having a witness or notary present when signing the document, if required. This step can lend additional credibility to the agreement.

Using vague language or legal jargon that may confuse the parties involved. Clarity is key; simple, straightforward language is more effective.

Failing to keep a copy of the signed Promissory Note for personal records. Both parties should retain copies to ensure that they have access to the terms agreed upon.

When dealing with financial transactions in Indiana, several forms and documents often accompany the Indiana Promissory Note. Each of these documents serves a specific purpose and can provide clarity and protection for both parties involved in the agreement. Below is a list of commonly used forms that complement the Promissory Note.

Understanding these documents can help both lenders and borrowers navigate their financial agreements more effectively. Each form plays a crucial role in ensuring that the terms of the loan are clear, enforceable, and mutually agreed upon.

The Indiana Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedules. While a promissory note is a simpler document that focuses on the borrower's promise to repay, a loan agreement typically includes more detailed terms, such as collateral and conditions for default. Both serve to protect the lender's interests and ensure that the borrower understands their obligations.

Another document similar to the Indiana Promissory Note is the IOU. An IOU is an informal acknowledgment of a debt, usually less detailed than a promissory note. While an IOU may state the amount owed, it often lacks specific repayment terms or interest rates. However, both documents serve the purpose of recognizing a debt and can be used as evidence in case of disputes, reinforcing the borrower's commitment to repay the loan.

The Indiana Promissory Note also resembles a Mortgage Agreement, particularly in cases where the note is secured by real property. A mortgage agreement details the terms of a loan used to purchase real estate, including the borrower's obligations and the lender's rights in case of default. Both documents establish a legal obligation to repay the borrowed amount, but a mortgage agreement typically includes additional provisions related to property ownership and foreclosure processes.

Another related document is the Secured Promissory Note. This type of note includes a security interest, meaning that the borrower pledges collateral to secure the loan. Like the Indiana Promissory Note, it outlines the borrower's promise to repay, but it adds the layer of protection for the lender by allowing them to claim the collateral if the borrower defaults. This makes both documents vital in establishing the terms of a secured loan.

Lastly, the Indiana Promissory Note can be compared to a Business Loan Agreement. This document is used when a business borrows money and includes terms specific to commercial lending. Similar to a promissory note, it outlines the loan amount, interest rate, and repayment terms. However, a business loan agreement often includes additional clauses regarding the use of funds and the responsibilities of the business, making it more complex while still serving the same fundamental purpose of documenting a loan obligation.

When filling out the Indiana Promissory Note form, it is important to follow certain guidelines to ensure accuracy and compliance. Here are ten things you should and shouldn't do:

When dealing with financial agreements, especially promissory notes, misunderstandings can arise. Here are six common misconceptions about the Indiana Promissory Note form, along with clarifications for each.

Understanding these misconceptions can help individuals navigate the complexities of promissory notes more effectively. Clarity in agreements is essential for maintaining healthy financial relationships.

When filling out and using the Indiana Promissory Note form, it is important to consider the following key takeaways:

By following these guidelines, individuals can ensure that their promissory note is legally sound and serves its intended purpose effectively.