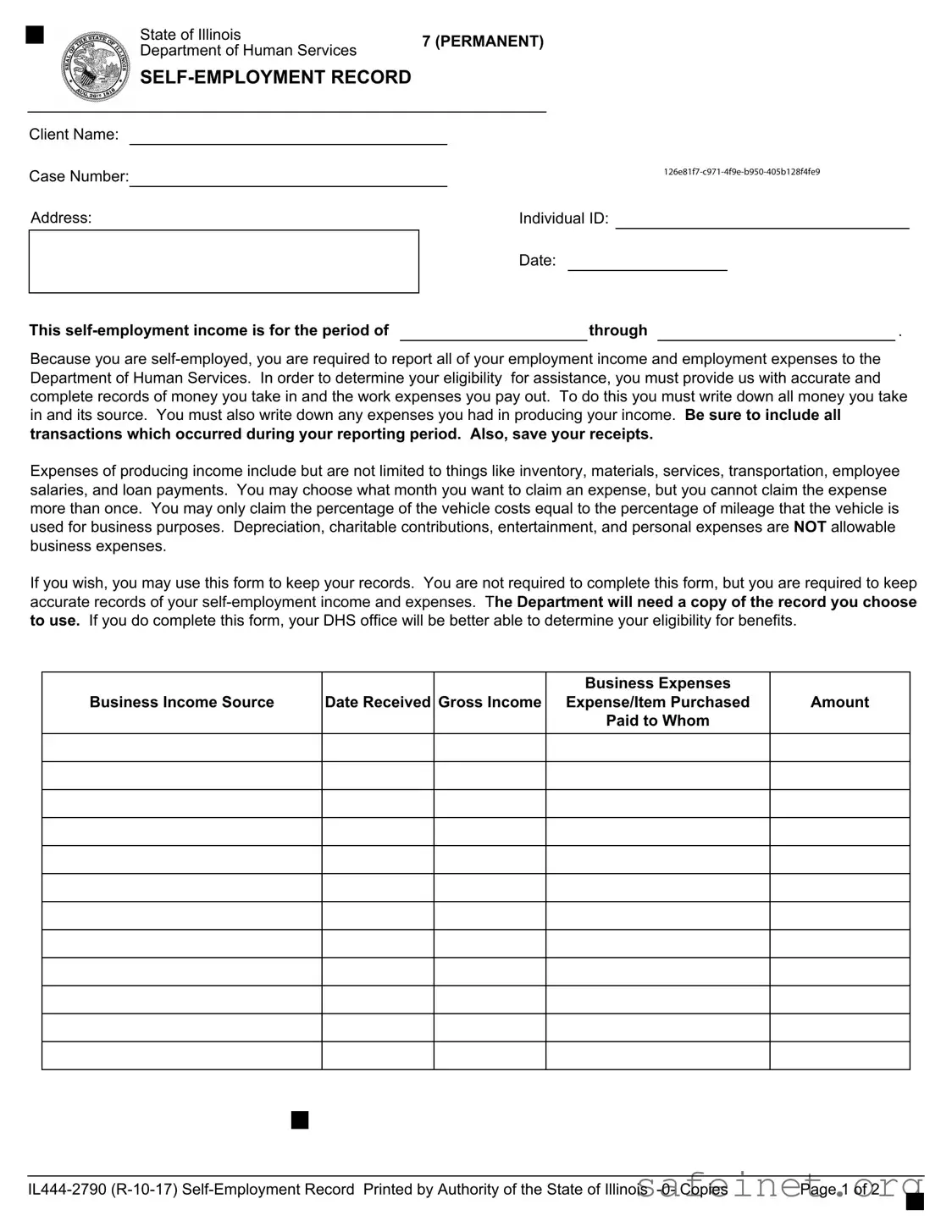

The IL 444 2790 Self Employment Record form is an essential tool for individuals in Illinois who are self-employed and seeking assistance from the Department of Human Services. This form serves as a structured way to document both income and expenses related to self-employment, which is crucial for determining eligibility for various benefits. As a self-employed individual, you must report all earnings and expenses accurately. The form requires you to list the sources of your income and the amounts received during a specified reporting period. Additionally, you will need to detail any expenses incurred while generating that income, such as costs for materials, transportation, and employee salaries. It is important to maintain thorough records, including receipts, as they support your reported figures. While the use of this form is not mandatory, completing it can streamline the process of verifying your eligibility for assistance. By providing a clear overview of your financial situation, the IL 444 2790 can help ensure that you receive the support you need.

|

|

State of Illinois |

7 (PERMANENT) |

|

|

|

||||||

|

|

|

|

|||||||||

|

|

Department of Human Services |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Client Name: |

|

|

|

|

|

|

|

|

|

|

||

Case Number: |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

||||||

Address: |

|

Individual ID: |

|

|

|

|

||||||

|

|

|

|

|

Date: |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

||||||

This |

|

|

|

|

|

through |

|

. |

||||

Because you are

Expenses of producing income include but are not limited to things like inventory, materials, services, transportation, employee salaries, and loan payments. You may choose what month you want to claim an expense, but you cannot claim the expense more than once. You may only claim the percentage of the vehicle costs equal to the percentage of mileage that the vehicle is used for business purposes. Depreciation, charitable contributions, entertainment, and personal expenses are NOT allowable business expenses.

If you wish, you may use this form to keep your records. You are not required to complete this form, but you are required to keep accurate records of your

Business Income Source

Date Received Gross Income

Business Expenses

Expense/Item Purchased

Paid to Whom

Amount

|

|

|

|

|

|

|

|

Page 1 of 2 |

|||

|

|

State of Illinois |

7 (PERMANENT) |

|

|

||||

|

|

Department of Human Services |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

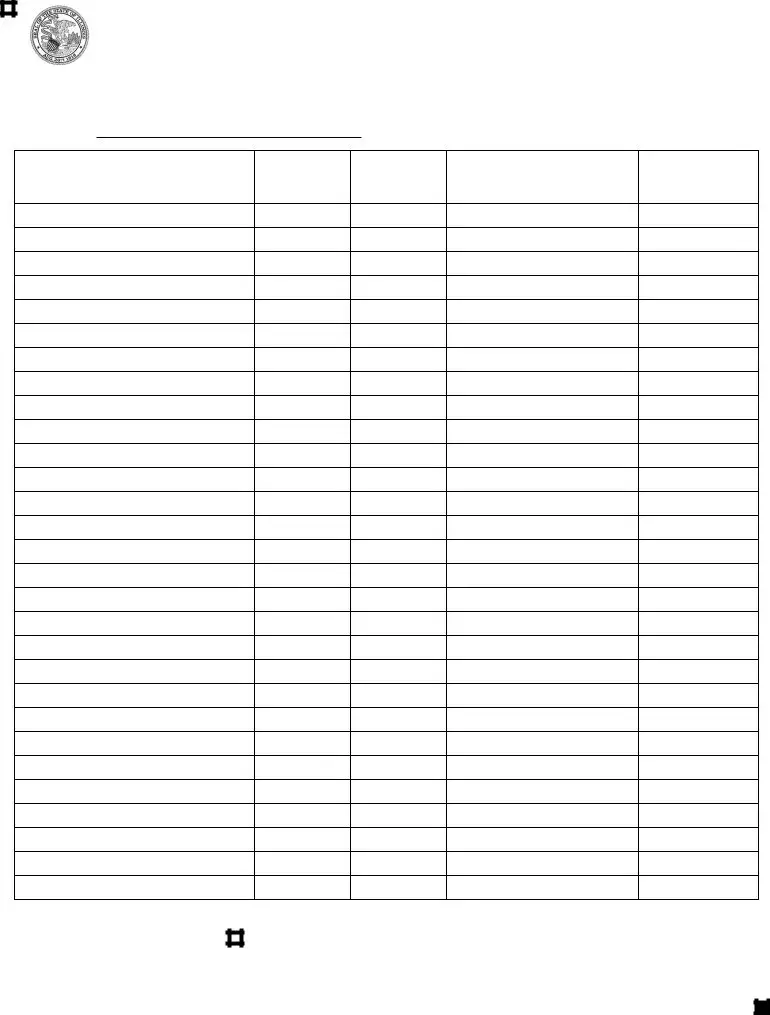

Client Name: |

|

|

|

|

Case Number: |

|

|

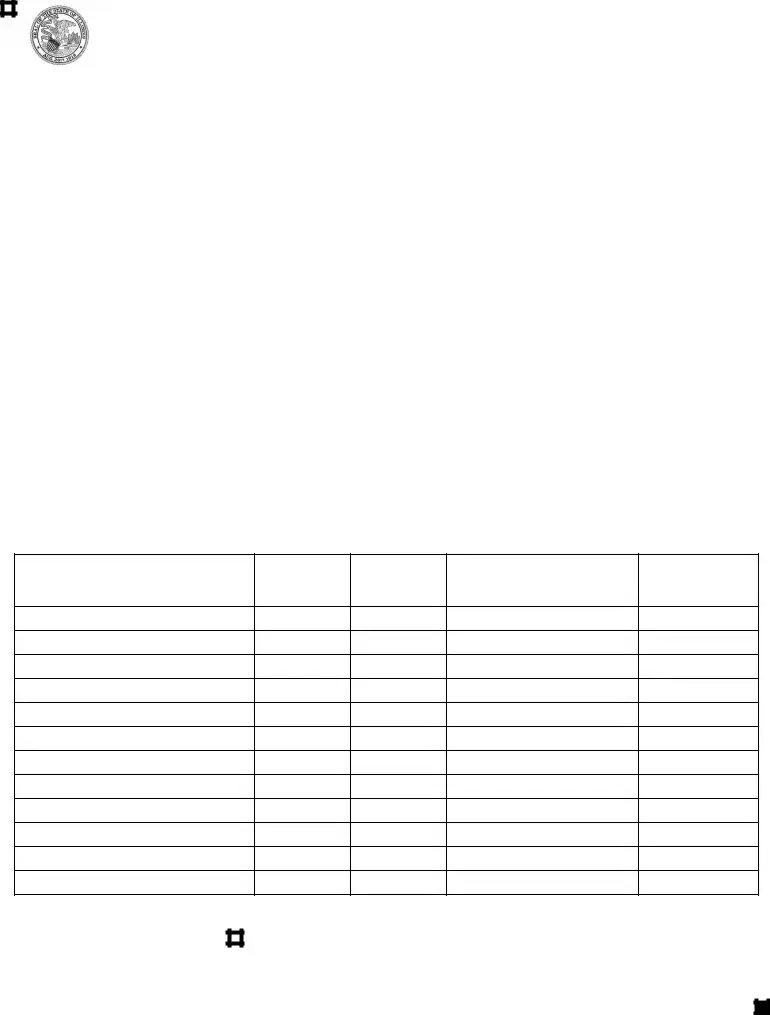

Business Income Source

Date Received Gross Income

Business Expenses

Expense/Item Purchased

Paid to Whom

Amount

|

|

|

|

|

|

|

|

Page 2 of 2 |

|||

| Fact Name | Details |

|---|---|

| Form Title | IL 444 2790 Self Employment Record |

| Governing Authority | Illinois Department of Human Services |

| Purpose | To report self-employment income and expenses for eligibility determination for assistance. |

| Reporting Requirement | All self-employment income and expenses must be accurately reported. |

| Record Keeping | Individuals are encouraged to save receipts and maintain detailed records of transactions. |

| Allowable Expenses | Expenses may include inventory, materials, transportation, and employee salaries, among others. |

| Non-Allowable Expenses | Depreciation, charitable contributions, entertainment, and personal expenses are not allowed. |

Filling out the IL 444 2790 Self Employment Record form is an important step in documenting your self-employment income and expenses. This process will help the Department of Human Services assess your eligibility for assistance. Make sure to gather all necessary information and records before you start. Here’s how to complete the form effectively.

Once you have filled out the form, review it for accuracy. It's essential that all information is complete and truthful. After reviewing, submit the form to your local Department of Human Services office along with any required documentation. This will aid in the evaluation of your eligibility for benefits.

What is the purpose of the IL 444 2790 Self Employment Record form?

The IL 444 2790 Self Employment Record form is designed to help individuals who are self-employed report their income and expenses accurately. This information is crucial for the Department of Human Services to assess eligibility for assistance programs. By keeping detailed records, you can ensure that your application reflects your financial situation accurately.

Who needs to fill out this form?

What information do I need to provide on the form?

You need to provide your name, individual ID, case number, and address. Additionally, you must record all sources of income, the dates received, gross income amounts, and any business expenses incurred during the reporting period. It's important to include details about what the expenses were for and who was paid.

What types of expenses can I claim?

You can claim expenses that are directly related to producing your income. This includes costs like inventory, materials, services, transportation, employee salaries, and loan payments. Keep in mind that you can only claim the percentage of vehicle costs that corresponds to business use. However, expenses like depreciation, charitable contributions, entertainment, and personal expenses are not allowable.

Do I have to use this form, or can I keep my records another way?

You are not required to use the IL 444 2790 form specifically. However, you must maintain accurate records of your self-employment income and expenses, regardless of the method you choose. If you do use this form, it can help the Department better assess your eligibility for benefits.

How should I handle receipts for my expenses?

It is crucial to save all receipts related to your business expenses. These documents serve as proof of your expenditures and can be requested by the Department of Human Services. Keeping organized records will make it easier for you to complete the form and verify your claims if needed.

What happens if I don’t report all my income and expenses?

Failing to report all income and expenses can lead to inaccuracies in your eligibility assessment. This may result in delays or denial of benefits. It is essential to be thorough and honest when completing the form to avoid any potential issues with your assistance application.

Can I claim the same expense more than once?

No, you cannot claim the same expense more than once. Be careful to track your expenses accurately and only claim them in the month you choose. Keeping clear and organized records will help you avoid mistakes in your reporting.

Not including all sources of income. It’s essential to report every source of income you receive from self-employment.

Failing to document expenses accurately. Make sure to write down all expenses related to your business activities during the reporting period.

Omitting the reporting period. Clearly indicate the start and end dates for the income and expenses being reported.

Claiming the same expense more than once. Each expense can only be claimed once. Be careful to track your claims accurately.

Not keeping receipts. Save all receipts related to your business expenses. They are vital for verifying your claims.

Including non-allowable expenses. Be aware that personal expenses, entertainment, and charitable contributions cannot be counted as business expenses.

Miscalculating vehicle expenses. Only claim the percentage of vehicle costs that corresponds to the business use of the vehicle.

Neglecting to sign and date the form. Ensure you complete this step to validate your submission.

Using incomplete information. Double-check that all sections of the form are filled out completely before submitting.

Not providing a copy of the record to the Department of Human Services. Make sure to submit the necessary documentation as required.

The IL 444 2790 Self Employment Record form is a crucial document for individuals in Illinois who are self-employed and seeking assistance from the Department of Human Services. Alongside this form, several other documents can help provide a comprehensive view of your financial situation. Here’s a list of those documents:

Having these documents ready will not only streamline the process of reporting your self-employment income and expenses but also strengthen your case for assistance. Accurate records are key to ensuring you receive the support you need.

The IRS Schedule C, or Form 1040, is a document used by sole proprietors to report income or loss from a business they operated or a profession they practiced. Like the IL 444 2790 Self Employment Record, it requires detailed reporting of income and expenses. Both forms emphasize the importance of keeping accurate records and receipts. The Schedule C is submitted annually with personal income tax returns, making it a crucial document for self-employed individuals to track their financial performance and tax obligations.

The Profit and Loss Statement, often referred to as an income statement, summarizes the revenues, costs, and expenses incurred during a specific period. This document serves a similar purpose to the IL 444 2790 in that it provides a clear picture of a business's financial health. Both documents require accurate reporting of income and expenses, helping individuals assess their profitability. While the Profit and Loss Statement is typically used for internal analysis or by lenders, the IL 444 2790 is geared towards determining eligibility for assistance programs.

The IRS Form 4562 is used to report depreciation and amortization. Similar to the IL 444 2790, it allows self-employed individuals to account for certain expenses over time. Both forms require individuals to maintain accurate records of their expenses, but while the IL 444 2790 focuses on current income and expenses, Form 4562 deals specifically with long-term asset costs. This distinction is important for tax reporting and financial management.

The Business Expense Log is a simple document that helps self-employed individuals track their business-related expenses. Like the IL 444 2790, it requires detailed entries of expenses incurred while generating income. Both documents emphasize the need for accuracy and completeness in reporting, ensuring that all relevant expenses are accounted for. The Business Expense Log can be a helpful tool for organizing information before filling out the IL 444 2790 or other tax-related forms.

The 1099-MISC form is used to report various types of income received by individuals who are not classified as employees. This form is similar to the IL 444 2790 in that it requires the reporting of income earned from self-employment activities. Both documents serve as important records for tax purposes, and individuals must ensure that they accurately report all income received. The 1099-MISC is often issued by clients or customers, while the IL 444 2790 is maintained by the individual for their own records.

The Personal Financial Statement is a document that outlines an individual's financial position, including assets, liabilities, and net worth. While it serves a different purpose than the IL 444 2790, it shares a commonality in requiring accurate financial reporting. Both documents help individuals understand their financial situation and can be used to assess eligibility for loans or assistance programs. The Personal Financial Statement provides a broader overview, while the IL 444 2790 focuses specifically on self-employment income and expenses.

The Cash Flow Statement tracks the flow of cash in and out of a business over a specific period. Similar to the IL 444 2790, it provides insight into the financial health of a self-employed individual. Both documents require detailed reporting of income and expenses, allowing individuals to understand their cash position. The Cash Flow Statement is often used for financial planning and analysis, while the IL 444 2790 is primarily focused on reporting for assistance eligibility.

The Business Plan is a comprehensive document that outlines the goals, strategies, and financial forecasts of a business. While it serves a broader purpose than the IL 444 2790, both documents require a detailed understanding of income and expenses. The Business Plan often includes projections based on historical data, which can be informed by the records kept in the IL 444 2790. This connection underscores the importance of maintaining accurate financial records for both operational and strategic purposes.

When filling out the IL 444 2790 Self Employment Record form, it’s important to follow certain guidelines to ensure accuracy and completeness. Here’s a list of things you should and shouldn't do:

Following these guidelines will help ensure that your form is filled out correctly and that you maintain eligibility for assistance. Accurate records are key to a smooth process.

Misconceptions about the IL 444 2790 Self Employment Record form can lead to confusion and mistakes. Here are ten common misconceptions along with clarifications to help individuals understand the requirements better.

Understanding these misconceptions can help individuals navigate the requirements of the IL 444 2790 Self Employment Record form more effectively. Accurate reporting is crucial for maintaining eligibility for assistance and ensuring compliance with regulations.

When filling out the IL 444 2790 Self Employment Record form, keep these key takeaways in mind:

By following these guidelines, you can ensure that your self-employment records are accurate and complete, helping you navigate the assistance process smoothly.