The Hawaii Promissory Note form serves as a crucial legal document in the realm of lending and borrowing, providing a clear framework for the terms of a loan agreement. This form outlines the borrower's promise to repay a specified amount of money to the lender, detailing essential elements such as the principal amount, interest rate, repayment schedule, and any applicable late fees. It also includes provisions regarding default, which specify the consequences if the borrower fails to meet their obligations. Furthermore, the form typically requires the signatures of both parties, thereby solidifying the agreement and ensuring that both lender and borrower are aware of their rights and responsibilities. Understanding this document is vital for anyone engaging in financial transactions in Hawaii, as it not only protects the interests of the lender but also provides clarity and security for the borrower. With its structured approach, the Hawaii Promissory Note form plays an essential role in fostering trust and accountability in financial dealings.

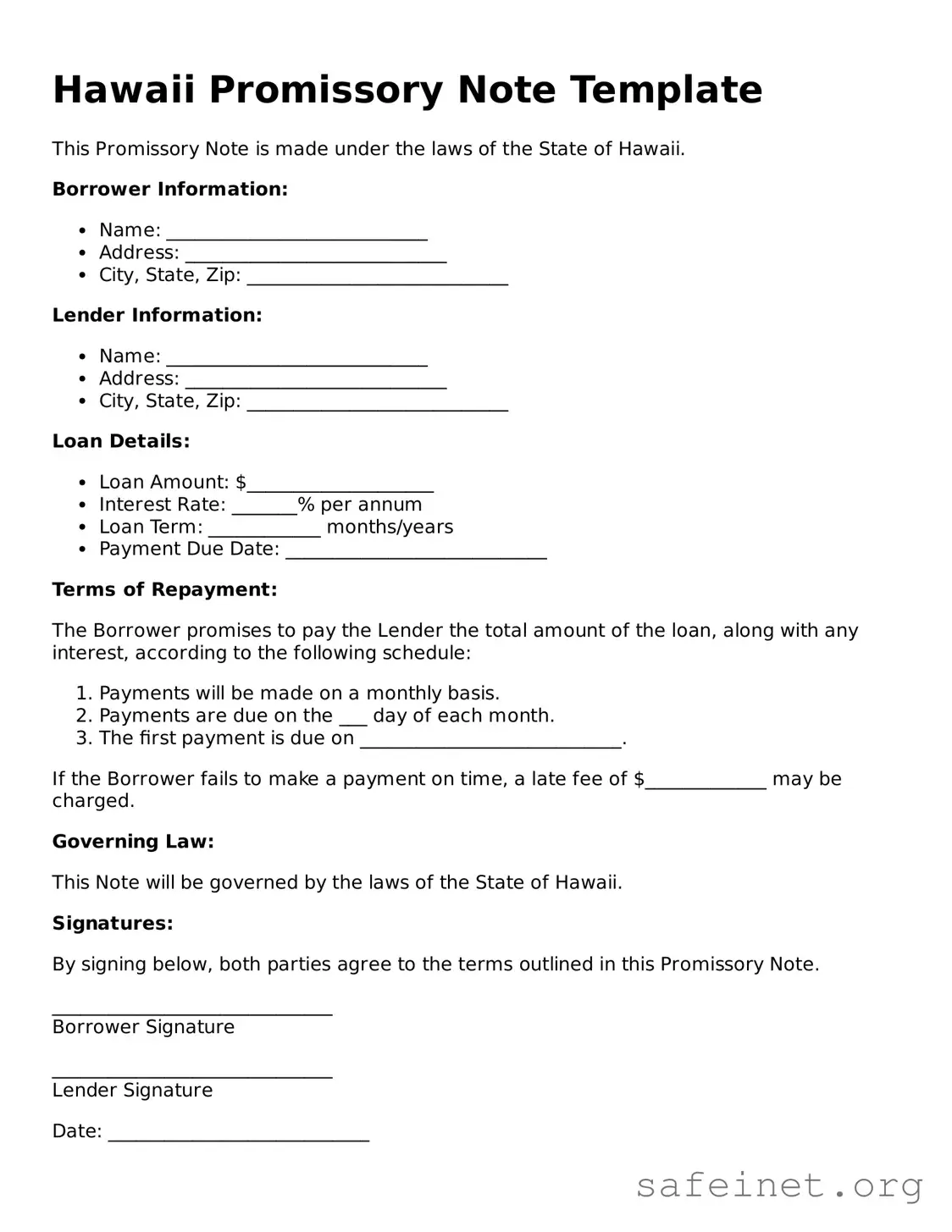

Hawaii Promissory Note Template

This Promissory Note is made under the laws of the State of Hawaii.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower promises to pay the Lender the total amount of the loan, along with any interest, according to the following schedule:

If the Borrower fails to make a payment on time, a late fee of $_____________ may be charged.

Governing Law:

This Note will be governed by the laws of the State of Hawaii.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower Signature

______________________________

Lender Signature

Date: ____________________________

| Fact Name | Description |

|---|---|

| Definition | A Hawaii Promissory Note is a written promise to pay a specific amount of money at a designated time. |

| Governing Law | The note is governed by Hawaii Revised Statutes, Chapter 478. |

| Parties Involved | The note typically involves a borrower (maker) and a lender (payee). |

| Interest Rate | Interest rates can be fixed or variable, as agreed upon by the parties. |

| Payment Terms | Payment terms, including due dates and installment amounts, should be clearly outlined. |

| Default Clauses | Default provisions specify the actions that can be taken if the borrower fails to make payments. |

| Signatures | Both parties must sign the note for it to be legally binding. |

| Notarization | While not required, notarization can add an extra layer of authenticity to the document. |

After completing the Hawaii Promissory Note form, you will need to ensure that all parties involved understand their obligations and rights under the agreement. It is crucial to keep a copy of the signed document for your records. Follow these steps to fill out the form accurately.

What is a Hawaii Promissory Note?

A Hawaii Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It specifies the amount borrowed, the interest rate, repayment schedule, and any other terms agreed upon by both parties. This document serves as evidence of the debt and can be used in court if necessary.

Who can use a Promissory Note in Hawaii?

Any individual or entity can use a Promissory Note in Hawaii. This includes individuals borrowing money from friends or family, businesses securing loans from banks, or even real estate transactions where one party agrees to pay another over time. It is essential for both parties to understand the terms before signing.

What are the key components of a Hawaii Promissory Note?

A typical Hawaii Promissory Note includes the following components: the names of the borrower and lender, the principal amount, interest rate, repayment terms, due dates, and any penalties for late payments. It may also include clauses related to default and remedies available to the lender.

Is a Promissory Note legally binding in Hawaii?

Yes, a Promissory Note is legally binding in Hawaii as long as it meets the necessary requirements. Both parties must agree to the terms, and the document should be signed and dated. It is advisable to have the document notarized to add an extra layer of authenticity and enforceability.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is best to document any modifications in writing and have both parties sign the updated agreement. This ensures that all parties are on the same page regarding the new terms.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has several options. They may choose to negotiate a new payment plan, pursue legal action to recover the owed amount, or initiate foreclosure proceedings if the loan is secured by collateral. The specific actions depend on the terms outlined in the Promissory Note and applicable state laws.

Do I need a lawyer to create a Promissory Note in Hawaii?

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A lawyer can ensure that the document complies with Hawaii laws and adequately protects your interests. For simple loans, individuals often use templates available online.

Where can I find a template for a Hawaii Promissory Note?

Templates for Hawaii Promissory Notes can be found online through legal websites, state government resources, or local law libraries. It is essential to choose a template that is specific to Hawaii laws and customize it to fit the specific terms of your agreement.

Failing to include the borrower's name clearly. This can lead to confusion about who is responsible for the debt.

Not specifying the loan amount accurately. It's crucial to state the exact figure to avoid disputes later.

Omitting the interest rate. The note should clearly outline how much interest will be charged, if any.

Neglecting to include payment terms. This includes the schedule for repayments and the due date for the final payment.

Using vague language. Clear and precise wording helps prevent misunderstandings.

Not signing the document. A signature is essential for the note to be legally binding.

Forgetting to date the note. A date is important for establishing when the agreement was made.

Leaving out consequences for default. It's important to specify what happens if the borrower fails to make payments.

Not having a witness or notary present. While not always required, having a third party can add an extra layer of credibility.

When engaging in a loan agreement in Hawaii, a Promissory Note is often accompanied by several other important documents. Each of these documents serves a specific purpose in outlining the terms and protecting the interests of both the borrower and the lender.

Understanding these documents is crucial for both parties involved in a loan transaction. They provide clarity, protect rights, and ensure that all parties are aware of their responsibilities throughout the life of the loan.

The Hawaii Promissory Note form shares similarities with a Standard Promissory Note. Both documents serve as written promises to repay a specific amount of money, usually with interest, within a defined period. They outline the borrower’s obligations and the lender’s rights, ensuring clarity in the repayment terms. The structure typically includes details such as the principal amount, interest rate, payment schedule, and consequences of default.

Another document similar to the Hawaii Promissory Note is the Secured Promissory Note. This type of note includes collateral to secure the loan, providing additional protection for the lender. If the borrower defaults, the lender has the right to seize the collateral. Like the Hawaii Promissory Note, it specifies repayment terms but adds a layer of security for the lender.

The Installment Loan Agreement also resembles the Hawaii Promissory Note. Both documents detail the terms of a loan that is to be repaid in installments. However, the Installment Loan Agreement may include more comprehensive terms regarding the loan’s use, fees, and potential penalties for late payments. This agreement ensures both parties understand the payment structure and obligations involved.

A Loan Agreement is another document that shares characteristics with the Hawaii Promissory Note. While a promissory note is a simple promise to pay, a Loan Agreement typically includes more detailed terms and conditions. It often outlines the purpose of the loan, payment methods, and the rights of both the lender and borrower, ensuring a mutual understanding of the loan's terms.

The Demand Note is also similar, as it allows the lender to demand repayment at any time. Like the Hawaii Promissory Note, it requires the borrower to repay the principal and interest. However, the key difference lies in the lender's ability to call for immediate payment, making it a more flexible option for lenders who may need quick access to funds.

A Commercial Promissory Note is another related document. This type is often used in business transactions and is tailored for commercial purposes. Like the Hawaii Promissory Note, it outlines the repayment terms and interest but may also include provisions specific to business lending, such as the use of funds and business-related covenants.

The Personal Loan Agreement is akin to the Hawaii Promissory Note in that it involves a borrower receiving funds from a lender, with a promise to repay. It typically covers personal loans, which can be for various purposes, such as medical expenses or home improvements. This agreement ensures that both parties are aware of the terms and conditions surrounding the loan.

A Real Estate Promissory Note is similar as it is often used in real estate transactions. It serves as a promise to repay a loan used to purchase property. While it shares the basic structure of the Hawaii Promissory Note, it may also include specific terms related to the real estate transaction, such as property descriptions and conditions related to the sale.

The Student Loan Agreement is another document that bears resemblance to the Hawaii Promissory Note. This agreement outlines the terms under which a student borrows money for educational expenses. Like the promissory note, it specifies the repayment terms, interest rates, and any grace periods, ensuring students understand their obligations once they graduate.

Finally, a Mortgage Note is similar to the Hawaii Promissory Note in that it is a written promise to repay borrowed money used to purchase real estate. It includes terms regarding the loan amount, interest rate, and repayment schedule, just like the Hawaii Promissory Note. The key distinction is that a Mortgage Note is secured by the property itself, giving the lender rights to the property if the borrower defaults.

When filling out the Hawaii Promissory Note form, it is essential to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Following these guidelines will help ensure that your Promissory Note is processed smoothly and efficiently.

Misconception 1: A Hawaii Promissory Note is only for large loans.

Many people believe that promissory notes are only necessary for significant amounts of money. In reality, they can be used for any loan amount, whether it's a few hundred dollars or several thousand. The form serves to document the terms of the loan, regardless of size.

Misconception 2: You don’t need a promissory note if you’re lending money to a friend.

Some think that informal agreements between friends or family members don’t require documentation. However, having a written promissory note can help clarify the terms and protect both parties in case of misunderstandings or disputes.

Misconception 3: A verbal agreement is sufficient.

While verbal agreements can be binding, they are often difficult to enforce. A Hawaii Promissory Note provides clear evidence of the loan terms, including the amount, interest rate, and repayment schedule, making it easier to resolve any issues that may arise.

Misconception 4: The note needs to be notarized to be valid.

Many people assume that notarization is required for a promissory note to be legally binding. In Hawaii, notarization is not necessary, although it can add an extra layer of authenticity and may be beneficial in certain situations.

Misconception 5: Once signed, the terms cannot be changed.

It’s a common belief that a promissory note is set in stone once signed. However, the terms can be modified if both parties agree to the changes. It’s essential to document any amendments in writing to avoid future disputes.

Filling out and using the Hawaii Promissory Note form is an important process for both lenders and borrowers. Here are some key takeaways to keep in mind:

By following these key points, individuals can navigate the process of using the Hawaii Promissory Note form more effectively and with greater confidence.