The Financial Planning Worksheet for Career Transition serves as an essential tool for individuals navigating significant career changes. This comprehensive form facilitates a thorough assessment of one's financial situation, helping users to strategize effectively for their future. To complete the worksheet, individuals must gather various documents including their current Leave and Earnings Statement (LES), bank and mortgage statements, credit reports, and details on living expenses. The form prompts users to calculate their net worth, itemizing assets and liabilities, and provides sections to evaluate monthly income and expenses. Key components include a listing of all income sources, various expense categories, and a comprehensive overview of indebtedness. By clearly outlining financial responsibilities, the worksheet encourages users to develop actionable plans aimed at increasing income, decreasing expenses, and managing debts more effectively. Importantly, it also highlights the necessity of setting short- and long-term financial goals, allowing individuals to chart their target costs and achieve their desired milestones systematically.

Financial Planning Worksheet for Career Transition

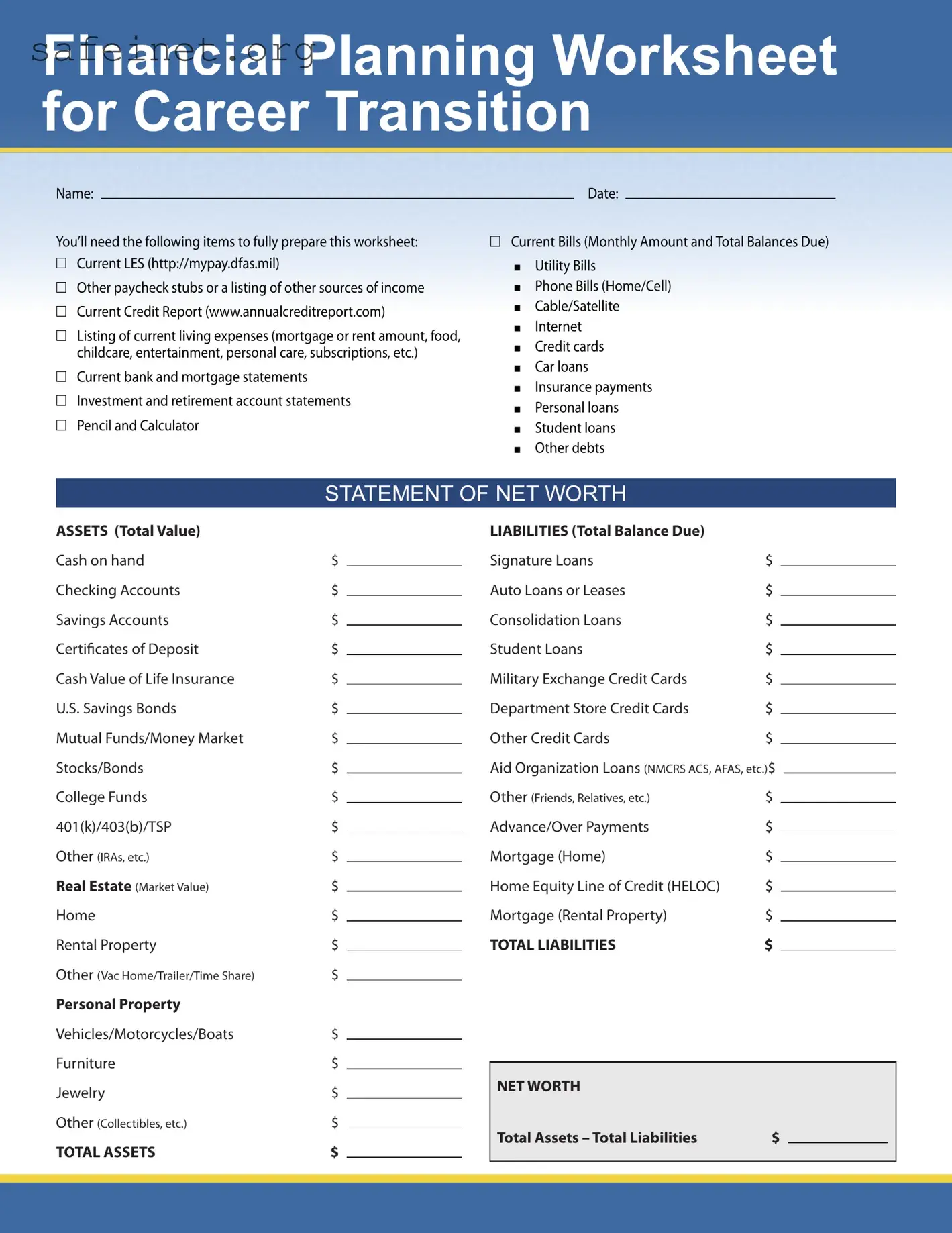

Name:

You’ll need the following items to fully prepare this worksheet: PP Current LES (http://mypay.dfas.mil)

PP Other paycheck stubs or a listing of other sources of income PP Current Credit Report (www.annualcreditreport.com)

PP Listing of current living expenses (mortgage or rent amount, food, childcare, entertainment, personal care, subscriptions, etc.)

PP Current bank and mortgage statements

PP Investment and retirement account statements PP Pencil and Calculator

Date:

PP Current Bills (Monthly Amount and Total Balances Due)

OO Utility Bills

OO Phone Bills (Home/Cell) OO Cable/Satellite

OO Internet

OO Credit cards OO Car loans

OO Insurance payments OO Personal loans

OO Student loans OO Other debts

STATEMENT OF NET WORTH

ASSETS (Total Value) |

|

Cash on hand |

$ |

Checking Accounts |

$ |

Savings Accounts |

$ |

Certificates of Deposit |

$ |

Cash Value of Life Insurance |

$ |

U.S. Savings Bonds |

$ |

Mutual Funds/Money Market |

$ |

Stocks/Bonds |

$ |

College Funds |

$ |

401(k)/403(b)/TSP |

$ |

Other (IRAs, etc.) |

$ |

Real Estate (Market Value) |

$ |

Home |

$ |

Rental Property |

$ |

Other (Vac Home/Trailer/Time Share) |

$ |

Personal Property |

|

Vehicles/Motorcycles/Boats |

$ |

Furniture |

$ |

Jewelry |

$ |

Other (Collectibles, etc.) |

$ |

TOTAL ASSETS |

$ |

LIABILITIES (Total Balance Due) |

|

Signature Loans |

$ |

Auto Loans or Leases |

$ |

Consolidation Loans |

$ |

Student Loans |

$ |

Military Exchange Credit Cards |

$ |

Department Store Credit Cards |

$ |

Other Credit Cards |

$ |

Aid Organization Loans (NMCRS ACS, AFAS, etc.)$

Other (Friends, Relatives, etc.) |

$ |

Advance/Over Payments |

$ |

Mortgage (Home) |

$ |

Home Equity Line of Credit (HELOC) |

$ |

Mortgage (Rental Property) |

$ |

TOTAL LIABILITIES |

$ |

NET WORTH |

|

Total Assets – Total Liabilities |

$ |

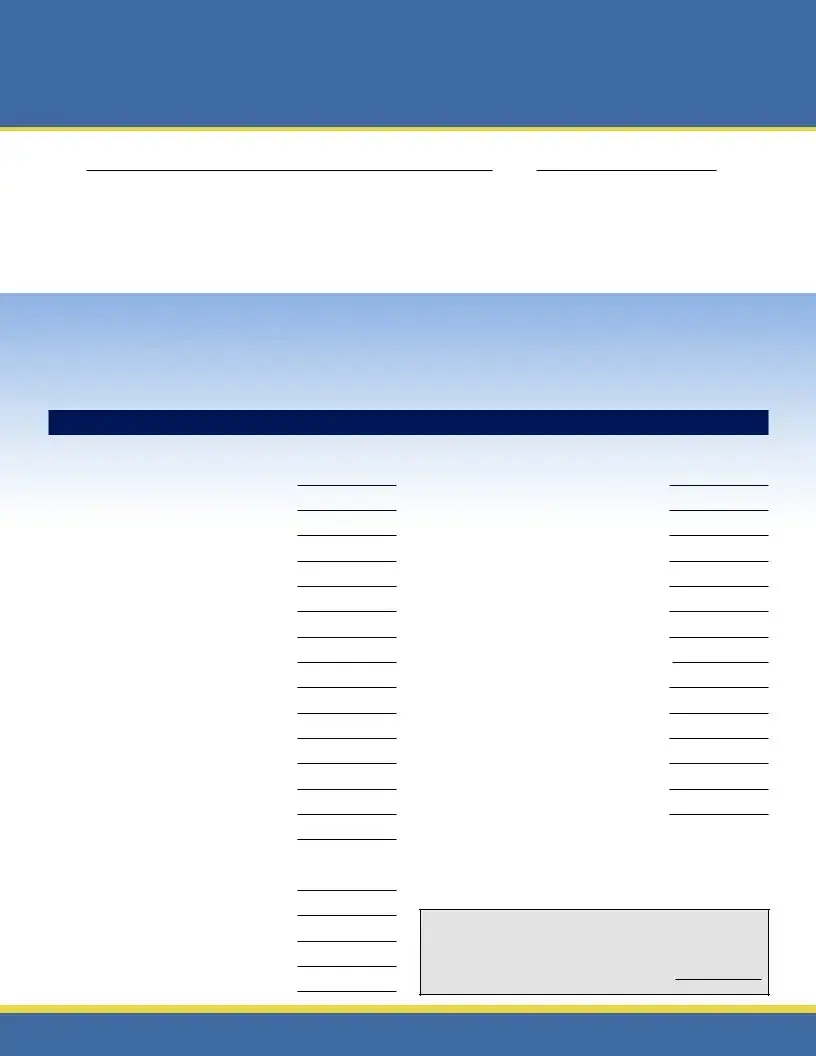

MONTHLY INCOME

ENTITLEMENTS |

|

ACTUAL |

PROJECTED 1 |

PROJECTED 2 |

|

|

|

|

|

|

|

* |

Base Pay |

|

|

|

|

|

Basic Allowance for Housing |

|

|

|

|

|

|

|

|

|

|

|

Overseas Housing Allowance |

|

|

|

|

|

|

|

|

|

|

|

Basic Allowance for Subsistence (BAS) |

|

|

|

|

|

|

|

|

|

|

|

Family Separation Allowance (FSA) |

|

|

|

|

|

|

|

|

|

|

* |

Special Pay |

|

|

|

|

* |

Special Pay |

|

|

|

|

* |

Special Pay |

|

|

|

|

* |

Special Pay |

|

|

|

|

|

*Other Taxable Pay |

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

TOTAL MILITARY COMPENSATION |

(A) |

|

|

|

|

|

|

|

|

|

DEDUCTIONS |

|

ACTUAL |

PROJECTED 1 |

PROJECTED 2 |

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

Family SGLI (For Spouses) |

|

|

|

|

|

|

|

|

|

|

|

Servicemembers’ Group Life Insurance (SGLI) |

|

|

|

|

|

|

|

|

|

|

|

Uniform Services TSP |

|

|

|

|

|

|

|

|

|

|

|

MGIB |

|

|

|

|

|

|

|

|

|

|

|

FITW Filing Status Actual |

|

|

|

|

|

|

|

|

|

|

|

FICA (Social Security) |

|

|

|

|

|

|

|

|

|

|

|

FICA (Medicare) |

|

|

|

|

|

|

|

|

|

|

|

State Income Tax |

|

|

|

|

|

|

|

|

|

|

|

AFRH (Armed Forces Retirement Home) |

|

|

|

|

|

|

|

|

|

|

|

TRICARE Dental Plan (TDP) |

|

|

|

|

|

|

|

|

|

|

|

Advance Payments |

|

|

|

|

|

|

|

|

|

|

|

Overpayments |

|

|

|

|

|

|

|

|

|

|

|

TOTAL DEDUCTIONS |

(B) |

$ |

$ |

|

|

|

|

|

|

|

CALCULATE NET INCOME |

|

ACTUAL |

PROJECTED 2 |

PROJECTED 2 |

|

|

|

|

|

|

|

|

Service Member’s Take Home Pay |

$ |

$ |

|

|

|

|

|

|

|

|

|

Service Member’s Other Earnings (less taxes) |

|

|

|

|

|

|

|

|

|

|

|

Spouse’s Earnings (less taxes) |

|

|

|

|

|

|

|

|

|

|

|

Child Support/Alimony (Received/Income) |

|

|

|

|

|

|

|

|

|

|

|

Other Income (e.g., SSI, Rental Income) |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

ALLOTMENT |

|

|

|

|

|

|

|

|

|

|

|

Family SGLI (For Spouses) |

|

|

|

|

|

|

|

|

|

|

|

Servicemembers' Group Life Insurance (SGLI) |

|

|

|

|

|

|

|

|

|

|

|

Uniform Services TSP |

|

|

|

|

|

|

|

|

|

|

|

MGIB |

|

|

|

|

|

|

|

|

|

|

|

TRICARE Dental Plan (TDP) |

|

|

|

|

|

|

|

|

|

|

|

Advance Payments |

|

|

|

|

|

|

|

|

|

|

|

Overpayments |

|

|

|

|

|

|

|

|

|

|

|

MONTHLY NET INCOME |

|

$ |

$ |

$ |

*Note: Pay Entitlements are taxable. Allowance Entitlements are

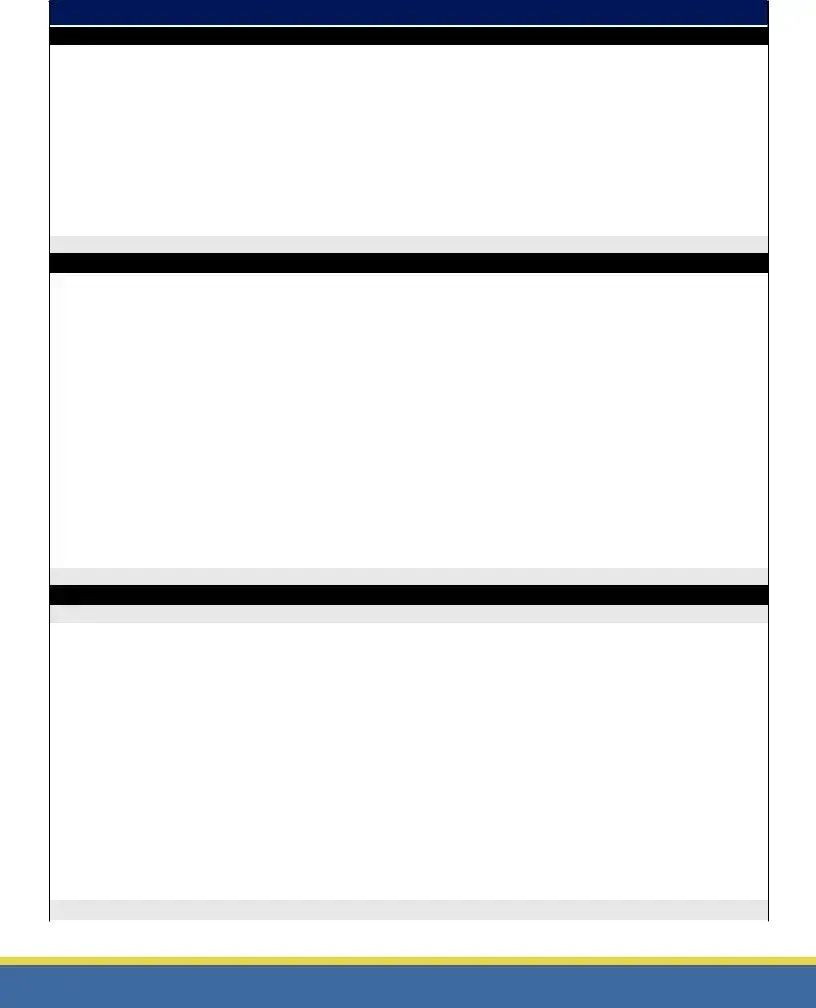

MONTHLY SAVINGS AND LIVING EXPENSES

SAVINGS |

|

ACTUAL |

PROJECTED 1 |

PROJECTED 2 |

|

|

|

|

|

|

|

|

Emergency Fund |

|

|

|

|

|

Reserve Fund |

|

|

|

|

|

|

|

|

|

|

|

Investments/IRAs/TSP/etc. |

|

|

|

|

TOTAL SAVINGS AND |

INVESTMENTS |

$ |

|

$ |

|

|

LIVING EXPENSES |

|

ACTUAL |

PROJECTED 1 |

PROJECTED 2 |

|

|

|

|

|

|

|

|

|

HOUSING |

Furnishings |

|

|

|

|

|

|

Maintenance/Repairs |

|

|

|

|

|

|

Mortgage/Rent |

|

|

|

|

|

|

Taxes/Fees |

|

|

|

|

|

FOOD |

Dining Out |

|

|

|

|

|

|

Groceries |

|

|

|

|

|

|

Lunches |

|

|

|

|

|

|

Vending Machines |

|

|

|

|

|

|

Meal Deductions from military pay |

|

|

|

|

|

UTILITIES |

Cable/Satellite TV |

|

|

|

|

|

|

Cellular/Pagers/Phone Cards |

|

|

|

|

|

|

Electricity |

|

|

|

|

|

|

Internet Service |

|

|

|

|

|

|

Natural Gas/Propane |

|

|

|

|

|

|

Telephone |

|

|

|

|

|

|

Water/Garbage/Sewage |

|

|

|

|

|

CHILD CARE |

Allowances |

|

|

|

|

|

|

Daycare |

|

|

|

|

|

|

Child Support/Other Dependent Care |

|

|

|

|

|

AUTOMOBILE |

Gasoline |

|

|

|

|

|

|

Maintenance/Repairs |

|

|

|

|

|

|

Other |

|

|

|

|

|

CLOTHING |

Laundry/Dry Cleaning |

|

|

|

|

|

|

Purchases ($50 monthly per person) |

|

|

|

|

|

INSURANCE |

Automobile |

|

|

|

|

|

|

Health |

|

|

|

|

|

|

Life |

|

|

|

|

|

|

Homeowners/Renters |

|

|

|

|

|

|

SGLI/FSGLI |

|

|

|

|

|

|

Dental Insurance |

|

|

|

|

|

HEALTHCARE |

Dental Expenses |

|

|

|

|

|

|

Eye Care |

|

|

|

|

|

|

Hospital/Physician |

|

|

|

|

|

|

Prescriptions |

|

|

|

|

|

EDUCATION |

Books |

|

|

|

|

|

|

Fees (Other/Room & Board) |

|

|

|

|

|

|

Tuition |

|

|

|

|

|

|

MGIB |

|

|

|

|

|

CONTRIBUTIONS |

Charities |

|

|

|

|

|

|

Club Dues/Association Fees |

|

|

|

|

|

|

Religious |

|

|

|

|

|

LEISURE |

Athletic Events/Sporting Goods |

|

|

|

|

|

|

Books/Magazines |

|

|

|

|

|

|

Computer Products (Software/Hardware) |

|

|

|

|

|

|

DVD/VHS & Video Games Rentals |

|

|

|

|

|

|

DVD’s & CD’s |

|

|

|

|

|

|

Entertainment |

|

|

|

|

|

|

Lessons |

|

|

|

|

|

|

Toys & Games |

|

|

|

|

|

|

Travel/Lodging |

|

|

|

|

|

PERSONAL |

Beauty Shop/Nails |

|

|

|

|

|

|

Barber Shop |

|

|

|

|

|

|

Cigarettes/Other Tobacco |

|

|

|

|

|

|

Vending Machines |

|

|

|

|

|

|

Liquor/Beer/Wine |

|

|

|

|

|

|

Other (Toiletries, Supplements, etc.) |

|

|

|

|

|

GIFTS |

Holidays |

|

|

|

|

|

|

Birthdays/Anniversaries |

|

|

|

|

|

PET CARE |

Food/Supplies |

|

|

|

|

|

|

Veterinarian/Service (Boarding/Grooming) |

|

|

|

|

|

MISCELLANEOUS |

ATM Fees/Stamps/etc. |

|

|

|

|

|

|

Other |

|

|

|

|

|

TOTAL MONTHLY LIVING EXPENSES |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

INDEBTEDNESS

|

|

|

BALANCE |

CURRENT |

|

|

CREDITOR |

PURPOSE |

APR % |

(From Page |

MONTHLY |

PROJECTED 1 |

PROJECTED 2 |

|

|

|

One) |

PAYMENT |

|

|

1. US Govt. |

Advance Pay |

|

|

|

|

|

|

|

|

|

|

|

|

2. US Govt. |

Over Payments |

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

|

|

|

|

|

|

|

|

|

|

|

|

|

15. |

|

|

|

|

|

|

|

|

|

|

|

|

|

16. |

|

|

|

|

|

|

|

|

|

|

|

|

|

17. |

|

|

|

|

|

|

|

|

|

|

|

|

|

18. |

|

|

|

|

|

|

|

|

|

|

|

|

|

19. |

|

|

|

|

|

|

|

|

|

|

|

|

|

20. |

|

|

|

|

|

|

|

|

|

|

|

|

|

21. |

|

|

|

|

|

|

|

|

|

|

|

|

|

22. |

|

|

|

|

|

|

|

|

|

|

|

|

|

23. |

|

|

|

|

|

|

|

|

|

|

|

|

|

24. |

|

|

|

|

|

|

|

|

|

|

|

|

|

25. |

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL

SUMMARY

ACTUAL |

PROJECTED 1 |

PROJECTED 2 |

NET INCOME (Bottom of Page 2)

SAVINGS & INVESTMENTS (Page 3) |

– |

|||

|

|

|

|

|

LIVING EXPENSES (Page 3) |

– |

|||

|

|

|

|

|

AMOUNT LEFT TO PAY DEBTS |

= |

|

|

|

|

|

|

|

|

TOTAL MONTHLY DEBT PAYMENTS (Page 4) |

– |

|||

|

|

|

|

|

SURPLUS OR DEFICIT |

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Total Monthly Debt Payments ÷ Net Income x 100 =

ACTION PLAN

INCREASE INCOME

1. �����������������������������������������������������������������������

2. �����������������������������������������������������������������������

3. �����������������������������������������������������������������������

4. �����������������������������������������������������������������������

DECREASE LIVING EXPENSES

1. �����������������������������������������������������������������������

2. �����������������������������������������������������������������������

3. �����������������������������������������������������������������������

4. �����������������������������������������������������������������������

DECREASE INDEBTEDNESS

1. �����������������������������������������������������������������������

2. �����������������������������������������������������������������������

3. �����������������������������������������������������������������������

4. �����������������������������������������������������������������������

ADDITIONAL INFORMATION NEEDED

1. �����������������������������������������������������������������������

2. �����������������������������������������������������������������������

3. �����������������������������������������������������������������������

4. �����������������������������������������������������������������������

TRANSITION GOALS

GOAL |

COST |

DATE WANTED |

MONTHLY SAVINGS TO REACH GOAL |

1.

2.

3.

4.

5.

6.

| Fact Name | Description |

|---|---|

| Purpose | The Financial Planning Worksheet for Career Transition helps individuals assess their current financial situation and plan for a successful transition. |

| Required Documents | To complete this worksheet, gather documents such as paycheck stubs, credit reports, and living expenses. |

| Assets Listing | The form requires a detailed listing of assets, including bank accounts, real estate, and personal property. |

| Liabilities Listing | Users must also provide a complete overview of their liabilities, including loans and credit card debts. |

| Net Worth Calculation | The worksheet calculates net worth by subtracting total liabilities from total assets. |

| Monthly Income Assessment | Individuals project actual and future income from various sources, including military compensation and other earnings. |

| Government Compliance | This worksheet adheres to various regulations governing financial planning in the United States, such as the Fair Credit Reporting Act. |

| Action Plan | Users can develop an action plan for increasing income, decreasing expenses, and managing debt. |

Filling out the Financial Planning Worksheet for Career can help organize your financial situation, making it easier to make informed decisions. Before starting, gather the necessary documents and information. This preparation will assist in creating an accurate picture of your financial health. Here are the steps to complete the form:

What is the purpose of the Financial Planning Worksheet for Career Transition?

The Financial Planning Worksheet for Career Transition serves as a comprehensive tool to assist individuals in assessing their financial situation as they transition into a new career. By evaluating income, expenses, assets, and liabilities, users can create a clear picture of their financial health and make informed decisions for future planning.

What information is needed to complete the worksheet?

To fully prepare the worksheet, gather several critical documents, including your current Leave and Earnings Statement (LES), paycheck stubs, credit reports, and bank statements. Additionally, have a complete list of living expenses, current bills, and records of investment and retirement accounts at hand. A pencil and calculator are also essential for calculations throughout the worksheet.

How does the worksheet help with budgeting?

The worksheet outlines both monthly income and expenses, which helps users identify where their money goes each month. By detailing fixed expenses such as housing and variable costs like entertainment and groceries, you can see clearly areas to adjust spending. This structured approach leads to improved budgeting and financial awareness.

What is ‘Net Worth,’ and why is it important?

Net Worth is the difference between total assets (what you own) and total liabilities (what you owe). Calculating your net worth is crucial because it provides insight into your overall financial health. A positive net worth suggests you're financially secure, while a negative net worth may indicate a need to reevaluate spending and saving habits.

Can this worksheet assist with debt management?

Yes, the worksheet includes a section for detailing indebtedness, which captures all debts and their respective payments. By organizing this information, users can devise strategies to reduce liabilities and manage debt more effectively. Tracking monthly payments and projecting future financial obligations will help with planning and staying on track.

What are the projected income and expense sections for?

Projected income and expense sections allow users to estimate future financial situations based on changing circumstances. By filling out these projections, such as anticipated salary changes or varying expenses, individuals can better prepare for shifts in their financial landscape. This forward-looking approach enhances preparedness and informed decision-making.

How can I set financial goals using this worksheet?

The worksheet provides a dedicated section for outlining transition goals, including specific desired costs and timelines for achieving those goals. Users can evaluate how much needs to be saved monthly to reach each financial target. This structured goal-setting creates accountability and a clear pathway towards financial success during and after the career transition.

Rushing through the form: Filling out the Financial Planning Worksheet in haste can lead to careless mistakes. Take your time to ensure accuracy.

Omitting necessary documents: People often forget to gather all the required items, such as bank statements or paycheck stubs, which can affect the validity of their financial picture.

Incorrectly estimating income: Some individuals do not project their income accurately, which can result in either overestimating or underestimating their resources.

Neglecting living expenses: A common oversight is failing to list all living expenses. This can create a misleading view of financial health.

Ignoring existing debts: People sometimes underestimate or forget to include all liabilities, such as student loans or credit card debt, leading to an incomplete assessment.

Not calculating net worth: Some fail to compute their net worth, which is essential for understanding overall financial status. This calculation is simply total assets minus total liabilities.

Failing to update figures: Using outdated information can result in a distorted view of one's financial situation. Make sure to use the most current data available.

Neglecting potential lifestyle changes: Some do not account for upcoming changes in their lifestyle or expenses, like moving or changing jobs, which can drastically alter their financial planning.

Ignoring the importance of savings: Many individuals overlook budgeting for savings or emergency funds, which is crucial for long-term financial stability.

Not creating an action plan: Finally, failing to develop an action plan based on the worksheet's findings can leave individuals without a clear path forward for achieving their financial goals.

In preparing for a career transition, various supporting documents and forms are essential to ensure a comprehensive understanding of one’s financial situation. Each document offers unique insights or assists in organizing financial information effectively. Below are several key forms commonly used alongside the Financial Planning Worksheet for Career.

Compiling these documents alongside the Financial Planning Worksheet creates a comprehensive view of one’s financial landscape. This preparation facilitates informed decision-making during a career transition, ultimately leading to a more strategic approach toward financial well-being.

The Career Change Assessment Form is an essential document similar to the Financial Planning Worksheet for Career Transition. It provides individuals with tools to evaluate their current job satisfaction and identify transferable skills. By breaking down personal and professional attributes, users can gain insights into potential career changes. This assessment encourages focused reflection on one's strengths, weaknesses, and passions, allowing for informed decisions about future career directions.

The Budget Planning Template is another useful resource that parallels the Financial Planning Worksheet for Career Transition. This document enables individuals to create a comprehensive monthly budget, listing income sources and expenses in a structured manner. It assists users in tracking their spending habits and identifying areas for savings. By visualizing income against expenses, the Budget Planning Template fosters a proactive approach to financial management during career transitions.

Similarly, the Income & Expenses Tracker serves a critical role in personal finance management. It offers a streamlined way to document and monitor all income and expenses over time. Users can categorize their earnings and spending, aiding in the assessment of financial health. Like the Financial Planning Worksheet, it helps individuals understand budgetary constraints and encourages smarter financial choices, especially when navigating career changes.

The Personal Financial Statement is another document that aligns with the Financial Planning Worksheet for Career Transition. This statement summarizes an individual's assets, liabilities, and net worth, providing a clear snapshot of their financial situation. By documenting financial standing, users can make educated decisions regarding potential job opportunities or investments. This transparency is crucial during transitioning phases when individuals evaluate their financial readiness for change.

The Retirement Planning Checklist also bears similarities to the Financial Planning Worksheet for Career Transition. It allows individuals to assess their readiness for retirement by mapping out financial goals, accounts, and investments over time. While the Financial Planning Worksheet focuses on immediate career transitions, the Retirement Planning Checklist encourages long-term financial health, making it a critical tool for planning ahead as one contemplates career shifts.

Lastly, the Debt Management Plan is an important document that resonates well with the Financial Planning Worksheet for Career Transition. It focuses on understanding and overcoming debt to pave the way for future financial stability. Users can list debts, create payment strategies, and track progress, much like how the Financial Planning Worksheet organizes financial information. Addressing debt is vital for those considering career transitions, as it enables individuals to pursue opportunities without financial constraints holding them back.

Filling out the Financial Planning Worksheet for Career Transition is an important step in managing your finances. Adhering to certain dos and don’ts can help ensure that you complete the form accurately and effectively. Here’s a helpful list to guide you through the process:

The Financial Planning Worksheet for Career Transition is a valuable tool for individuals preparing for a career change or financial assessment. However, several misconceptions surround its use. Here are some of the most common misunderstandings:

Understanding these misconceptions can help individuals utilize the Financial Planning Worksheet more effectively. It is a comprehensive tool that supports financial literacy and strategically prepares for career transitions.

Gather all relevant financial documents before starting the worksheet. This includes your paycheck stubs, credit report, and bank statements.

List your current living expenses accurately. Detail every expense from housing to entertainment to present a complete picture of your financial situation.

Clearly outline all debts and their balances. This includes loans, credit cards, and any other financial obligations you may have.

Calculate your net worth by subtracting total liabilities from total assets. This figure indicates your overall financial health.

Utilize both actual income and projected income figures. Being realistic about your current financial situation helps in planning for the future.

Identify areas where you can increase your income or decrease living expenses. For example, consider additional job opportunities or reducing discretionary spending.

Use the summary section to assess your financial balance. It allows you to see the relationship between your income and expenses at a glance.

Develop a clear action plan based on your findings. Whether it’s to increase savings or decrease debt, concrete steps can help you achieve your financial goals.