The FHA Refinance Authorization form serves as a critical tool in the refinancing process for homeowners seeking to take advantage of advantageous loan conditions under the Federal Housing Administration program. One of the key components of this form is the identification of the loan number, which aids in tracking the refinancing application effectively. Additionally, borrowers must provide their Social Security numbers, including those of co-borrowers if applicable, which ensures accurate record-keeping and eligibility verification. The form also requests the FHA case numbers for both the new refinance application and the mortgage being paid off, facilitating a seamless transition from the old mortgage to the new one. Moreover, an expected closing month is specified, which helps lenders manage timelines and expectations for all parties involved. Overall, the FHA Refinance Authorization form is designed to streamline the refinancing process while ensuring compliance with FHA regulations.

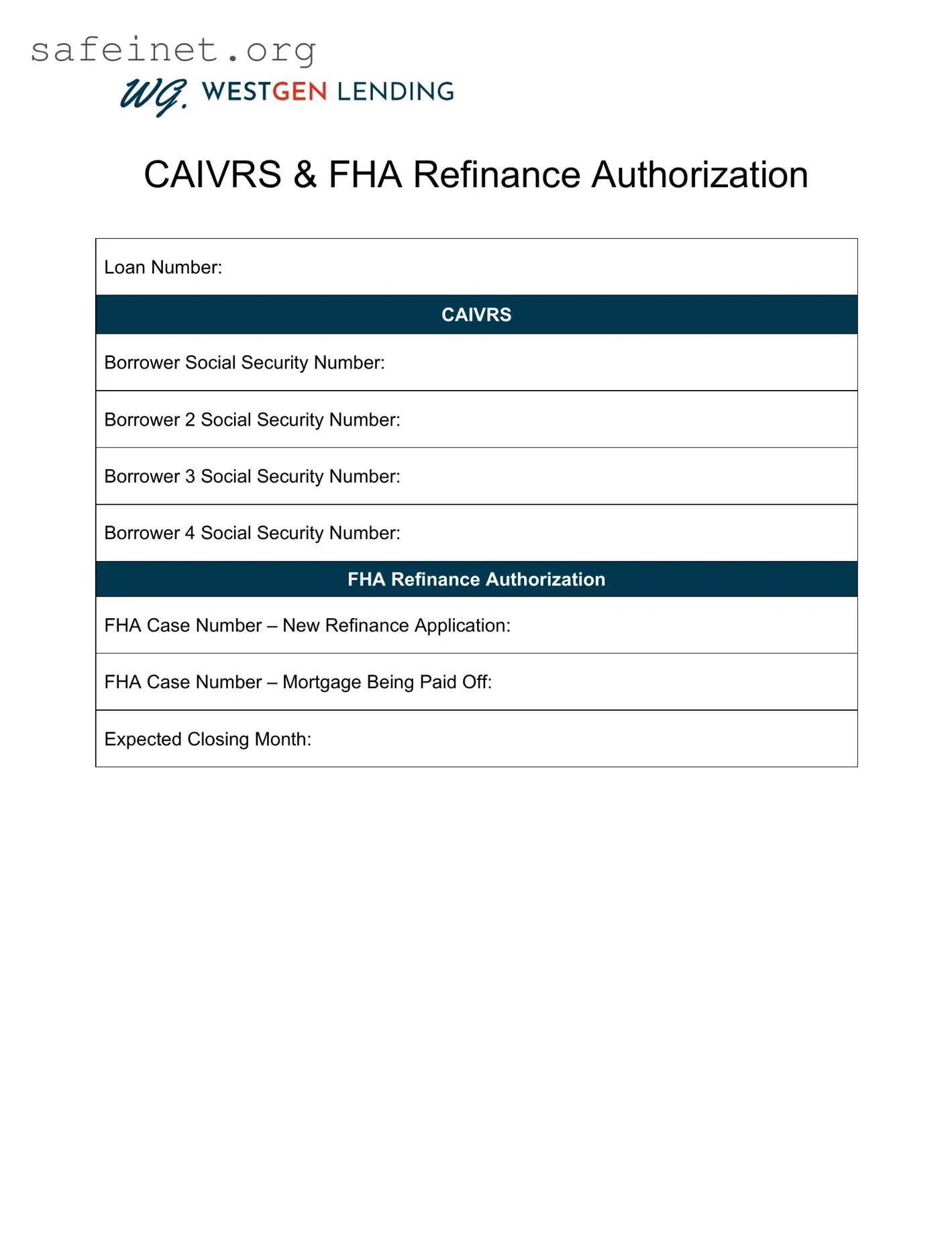

CAIVRS & FHA Refinance Authorization

Loan Number:

CAIVRS

Borrower Social Security Number:

Borrower 2 Social Security Number:

Borrower 3 Social Security Number:

Borrower 4 Social Security Number:

FHA Refinance Authorization

FHA Case Number – New Refinance Application:

FHA Case Number – Mortgage Being Paid Off:

Expected Closing Month:

| Fact Name | Description |

|---|---|

| Loan Number | The unique identifier for the refinance transaction, essential for tracking and processing the loan. |

| CAIVRS | This refers to the Credit Alert Verification Reporting System, which checks for federal delinquency status. |

| Borrower Social Security Numbers | The form requires Social Security Numbers for up to four borrowers, vital for identification and credit checks. |

| FHA Case Number – New Refinance Application | This unique number identifies the new refinance application with the FHA, essential for processing. |

| FHA Case Number – Mortgage Being Paid Off | This number points to the mortgage that the refinance will pay off, linking the transactions. |

| Expected Closing Month | This indicates when the borrower anticipates the closing of the refinancing transaction will occur. |

| Governing Laws | Specific FHA regulations and guidelines govern the form, primarily federal laws concerning refinancing. |

Filling out the FHA Refinance Authorization form requires careful attention to specific details. It is essential to ensure that all necessary information is provided accurately, as this will be used in the refinancing process. Follow the steps below to complete the form effectively.

What is the FHA Refinance Authorization form?

The FHA Refinance Authorization form is a document required when you are looking to refinance your existing FHA loan. This form gives your lender permission to obtain information, such as your credit report and the status of your current mortgage, which is necessary for processing the refinancing application.

Why do I need to fill out the Social Security Number section?

The Social Security Number section collects essential identification information for each borrower. This data helps lenders verify your identity and assess your creditworthiness. Providing accurate Social Security Numbers ensures a smoother process and helps avoid any delays in your refinancing application.

What is CAIVRS, and why is it mentioned in the form?

CAIVRS stands for the Credit Alert Verification Reporting System. It is a database that includes information about borrowers who have defaulted on federal loans. Your lender will use this information to determine your eligibility for refinancing. If you’re listed in CAIVRS, it may affect your ability to get a new FHA loan.

What are the FHA Case Numbers mentioned in the form?

The form requires two FHA Case Numbers: one for the new refinance application and one for the mortgage you are paying off. The new FHA Case Number is assigned when you start the refinancing process, while the mortgage being paid off refers to the existing loan you want to replace. Both numbers are crucial for tracking your loan and ensuring the refinancing goes through without issues.

How does the 'Expected Closing Month' section work?

This section allows you to provide an estimate of when you plan to close on the new loan. It helps lenders plan and streamline the refinancing process. When you fill this out, make sure to consider any factors that might affect your closing timeline, such as home inspections or appraisal scheduling.

Can I complete the FHA Refinance Authorization form electronically?

Yes, many lenders now allow borrowers to complete the FHA Refinance Authorization form electronically. This can save time and make the process more convenient. Just ensure you securely submit the form and follow your lender's specific instructions for electronic submissions.

What happens if I do not complete the authorization form?

If you choose not to fill out the FHA Refinance Authorization form, your lender will be unable to request the necessary information required for your refinancing application. This could delay or even halt your refinancing process, so it’s essential to complete this form promptly and accurately.

Who should I contact if I have questions about the form?

If you have questions about the FHA Refinance Authorization form, your first point of contact should be your lender or mortgage broker. They can provide guidance specific to your situation and help clarify any uncertainties you may have about filling out the form.

How long does it take to process the refinancing after submitting the form?

The processing time can vary depending on several factors, including the lender's workload and your specific financial situation. Typically, it may take anywhere from a few weeks to a couple of months. Staying in contact with your lender for updates can help you stay informed about your application’s progress.

Failing to provide accurate Social Security Numbers for all borrowers involved in the refinancing process. It is essential to include correct numbers to ensure proper identification.

Leaving out the FHA Case Number for the new refinance application. This number is critical for processing the loan.

Omitting the FHA Case Number for the mortgage being paid off. This detail helps to confirm which existing loan is being refinanced.

Not specifying the Expected Closing Month. This information is important for the timeline of the refinancing process.

Incorrectly identifying the loan number. Ensure this number reflects the correct loan being refinanced to avoid any processing errors.

Missing signatures or failing to date the authorization form. All required signatures must be present with appropriate dates to validate the submission.

Submitting incomplete or illegible forms. Make sure all entries are clear and filled out completely to prevent delays.

Neglecting to verify that all information is current and accurate before submission. Outdated information may lead to complications in processing.

Not reviewing the entire form for consistency. Any discrepancies between fields can cause confusion and slowdown in approval.

When considering the FHA Refinance Authorization form, it is essential to recognize that several other documents may accompany it during the refinancing process. Each of these documents plays a vital role in ensuring a smooth and transparent transaction. Below is a list of some commonly used forms that often go hand-in-hand with the FHA Refinance Authorization form.

Understanding these accompanying documents is essential for borrowers as they navigate the refinancing process. Each form will contribute to a coherent loan structure, promoting clarity and confidence in the decision-making journey. By familiarizing oneself with these documents, borrowers can better prepare for the responsibilities and opportunities that come with an FHA refinance.

The FHA Loan Application is a document that borrowers complete to apply for a home loan insured by the Federal Housing Administration. Like the FHA Refinance Authorization form, it collects essential information, such as the borrower's financial details and property information. Both forms require identification numbers, including Social Security numbers, and involve FHA case numbers, which track the loan throughout the financing process.

The Loan Estimate is another essential document that borrowers receive after applying for a loan. Similar to the FHA Refinance Authorization, it provides crucial information about loan terms, projected payments, and closing costs. Both forms aim to keep the borrower informed about the financial implications of their loan, facilitating better decision-making for refinancing or purchasing a home.

The Credit Authorization form permits lenders to check a borrower's credit history. This document is similar to the FHA Refinance Authorization since it often requires Social Security numbers and personal identifiers. Both forms serve to assess the borrower’s eligibility for financing, ensuring that lenders have the necessary information to make sound lending decisions.

The Loan Commitment letter outlines the terms and conditions of a mortgage loan approved by a lender. Like the FHA Refinance Authorization, it includes specific details related to the borrower’s financial profile and loan structure. Both documents are crucial for finalizing the loan process, providing assurance to borrowers that they have secured financing under agreed-upon conditions.

The Borrower's Affidavit is a sworn statement about the borrower's financial situation. Just as the FHA Refinance Authorization requires verification of borrower information, the Borrower's Affidavit serves to confirm the accuracy of the details provided to the lender. Both documents aim to protect against fraud while establishing the legitimacy of the application process.

The Good Faith Estimate (GFE) has been replaced by the Loan Estimate but served a similar purpose. It gave borrowers a breakdown of expected costs associated with their loans, similar to the information found in the FHA Refinance Authorization form. Both documents aided borrowers in understanding the financial implications of refinancing or taking a new loan.

The Mortgage Application form collects comprehensive personal and financial data from the borrower. Much like the FHA Refinance Authorization, it seeks to assess the borrower's ability to repay a loan by gathering relevant information. Both documents establish a foundation for lender review and approval, facilitating the mortgage process.

The Closing Disclosure is provided to borrowers three days before closing on a mortgage. Like the FHA Refinance Authorization, it provides a summary of final loan terms and costs. Both documents ensure borrowers fully understand their financial obligations, allowing for informed financial decisions before entering into a mortgage agreement.

The Verification of Employment (VOE) form confirms a borrower's employment status. This document, like the FHA Refinance Authorization, must be filled out with accurate identifiers, including Social Security numbers. Both forms help lenders assess a borrower's ability to repay the loan by evaluating employment stability and income information.

The Form 4506-T, Request for Transcript of Tax Return, allows lenders to verify a borrower’s income through tax returns. Similar to the FHA Refinance Authorization, this form includes personal identifiers to ensure accuracy. Both documents are critical in evaluating a borrower’s financial situation and risk, which helps in determining loan approval for refinancing or new purchases.

When filling out the FHA Refinance Authorization form, there are certain practices to adopt and others to avoid. The following list outlines the essential do's and don'ts:

The FHA Refinance Authorization form is often misinterpreted. Below are some common misconceptions and clarifications regarding this important document.

This is incorrect. The FHA Refinance Authorization form is applicable to any homeowner seeking to refinance, regardless of whether they have previously purchased a home.

All borrowers listed on the loan must sign and complete the FHA Refinance Authorization form to ensure compliance with FHA guidelines.

The Social Security numbers of all borrowers are required on the form. This information is vital for the FHA to verify identity and credit history.

The loan number is essential for tracking the refinance request. Without it, processing may be delayed.

The expected closing month should be as accurate as possible. This information aids in scheduling and processing your refinance efficiently.

This assumption is false. Including the FHA case number of the existing mortgage is critical to ensure proper application of funds.

Multiple case numbers can be processed, contingent upon the terms of the refinancing. Each transaction will need its own authorization.

This is untrue. The FHA Refinance Authorization form must be submitted prior to closing, so that all compliance checks can be completed.

All signatures must be present when submitting the form. Incomplete forms will likely lead to delays in processing.

This misconception is critical. The form is essential for the FHA to track the refinance process and maintain proper records, making it a vital part of the refinancing procedure.

Understanding the FHA Refinance Authorization form is crucial for a successful refinancing process. Here are some key takeaways: