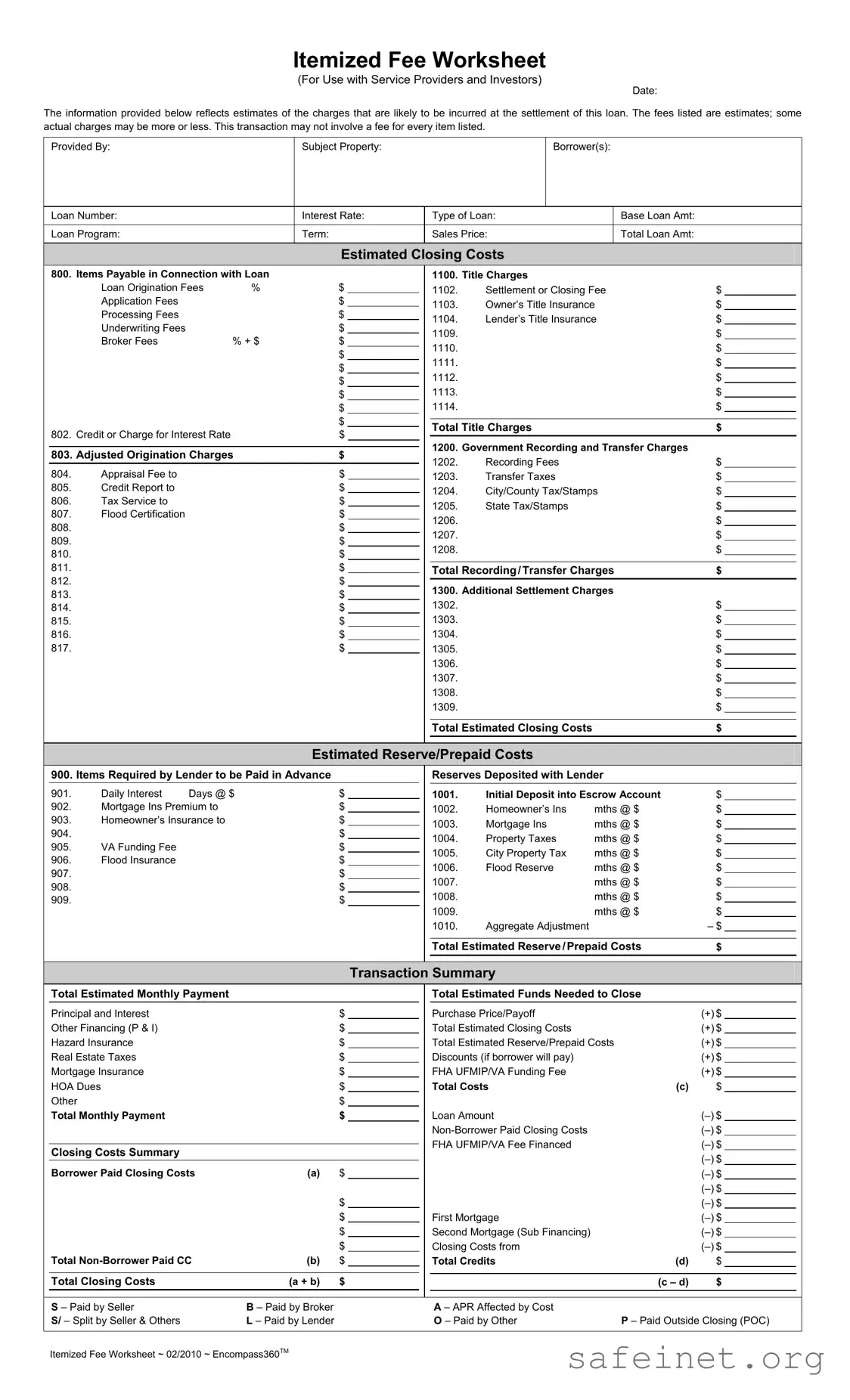

The Fee Worksheet form serves as a crucial tool in the real estate transaction process, providing a detailed breakdown of anticipated costs associated with a loan settlement. This document is designed for use by service providers and investors, allowing them to estimate various charges that may arise during the closing of a loan. It includes sections for essential information such as the date of the transaction, subject property, borrower details, loan number, interest rate, and type of loan. The form categorizes fees into several groups, including title charges, government recording and transfer charges, and additional settlement charges. Each category lists individual fees, such as loan origination fees, title insurance, appraisal fees, and more, providing transparency regarding the costs involved. Moreover, the Fee Worksheet outlines estimated closing costs and reserves required by the lender, which may include prepaid items like homeowner's insurance and property taxes. By summarizing these costs, the form helps borrowers understand their financial obligations, ensuring they are well-informed before proceeding with the transaction.

| Fact Name | Description |

|---|---|

| Purpose | The Fee Worksheet is designed to provide an itemized estimate of charges associated with the settlement of a loan. |

| Estimates | All fees listed on the worksheet are estimates; actual charges may vary at the time of settlement. |

| Provided By | The form includes fields for the service provider's name and the subject property details. |

| Governing Law | In many states, the use of this form is governed by the Real Estate Settlement Procedures Act (RESPA). |

| Closing Costs | The worksheet outlines various categories of closing costs, including title charges and government recording fees. |

| Reserve Costs | It also estimates prepaid costs and reserves required by the lender, such as mortgage insurance and property taxes. |

| Transaction Summary | A transaction summary section calculates total estimated monthly payments and funds needed to close. |

| Version | The current version of the Itemized Fee Worksheet is dated February 2010 and is associated with Encompass360™. |

Filling out the Fee Worksheet form is an essential step in preparing for your loan settlement. This form helps you estimate the various charges that may arise during the closing process. By accurately completing it, you can better understand the financial obligations associated with your loan.

What is the purpose of the Fee Worksheet form?

The Fee Worksheet form serves as a detailed estimate of the charges associated with a loan settlement. It helps borrowers understand the various costs they may incur during the closing process. By itemizing fees related to title charges, government recording, and additional settlement charges, the form provides transparency. This allows borrowers to prepare financially for the closing of their loan, ensuring they are aware of both expected and potential costs.

How are the estimated closing costs determined on the Fee Worksheet?

Estimated closing costs on the Fee Worksheet are calculated based on various factors, including the type of loan, interest rate, and specific charges associated with the transaction. Service providers and lenders typically provide these estimates. It’s important to note that while the worksheet lists potential charges, actual costs may vary. Some fees may end up being higher or lower than estimated, and not all items listed may apply to every transaction.

What should I do if my actual closing costs differ from the estimates on the Fee Worksheet?

If your actual closing costs differ from those estimated on the Fee Worksheet, it's advisable to review the final closing statement carefully. Any discrepancies should be discussed with your lender or service provider. They can explain the reasons for the differences and provide clarity on any unexpected charges. Understanding these variations can help you make informed decisions and better prepare for future transactions.

Are there any fees on the Fee Worksheet that I can negotiate?

Yes, certain fees listed on the Fee Worksheet may be negotiable. For example, you can discuss loan origination fees, broker fees, and even some title charges with your lender or service provider. It’s beneficial to shop around and compare offers from different lenders, as this may give you leverage in negotiations. Open communication about your concerns regarding fees can lead to potential savings.

Missing Information: Many people forget to fill in critical details such as the Date, Borrower(s), or Loan Number. This can lead to confusion and delays in processing.

Incorrect Fee Estimates: Some individuals underestimate or overestimate fees. Ensure that all charges, like Title Charges and Government Recording Fees, are accurately reflected to avoid surprises at closing.

Not Specifying Loan Type: Failing to indicate the Type of Loan can result in miscalculations. Different loans have different fees associated with them.

Omitting Required Charges: Some users overlook mandatory items such as Mortgage Insurance or Property Taxes. These are essential for a complete financial picture.

Confusing Total Costs: When adding up various costs, mistakes can happen. Double-check the Total Estimated Closing Costs and ensure all components are included.

The Fee Worksheet form is an essential document used in real estate transactions to estimate the costs associated with a loan. Alongside this form, several other documents are commonly utilized to provide a comprehensive overview of the financial aspects involved in closing a loan. Below is a list of these documents, each serving a specific purpose in the process.

Each of these documents plays a vital role in ensuring that the loan process is transparent and that all parties are informed of their rights and responsibilities. Proper documentation helps facilitate a smoother closing experience.

The Loan Estimate form is a document that serves a similar purpose to the Fee Worksheet. It is provided to borrowers within three business days of applying for a mortgage. This form outlines the estimated closing costs, interest rates, and monthly payments associated with the loan. Like the Fee Worksheet, it presents a detailed breakdown of various fees, making it easier for borrowers to understand the financial implications of their loan. Both documents aim to promote transparency and help borrowers make informed decisions about their financing options.

The Closing Disclosure is another document closely related to the Fee Worksheet. It is provided to borrowers three days before closing on a mortgage and includes final details about the loan, including the costs and terms. While the Fee Worksheet provides estimates, the Closing Disclosure contains actual figures that reflect the costs of the transaction. Both documents share the goal of ensuring that borrowers are fully aware of the financial obligations they are undertaking, but the Closing Disclosure finalizes the information presented in the Fee Worksheet.

The Good Faith Estimate (GFE) was a document used in the past to provide borrowers with an estimate of the costs associated with their mortgage loan. Although it has been largely replaced by the Loan Estimate, it shares similarities with the Fee Worksheet in that it aimed to provide a clear overview of expected fees and charges. Both documents were designed to help borrowers compare different loan offers and understand the financial commitments involved in their transactions, fostering informed decision-making.

The HUD-1 Settlement Statement is another document that aligns closely with the Fee Worksheet. This form was used primarily in real estate transactions to itemize all closing costs and fees associated with the settlement. Like the Fee Worksheet, the HUD-1 provided a detailed breakdown of charges, allowing both buyers and sellers to see exactly where their money was going at closing. While the HUD-1 is no longer used for most residential transactions, it shares the same intent of clarity and transparency found in the Fee Worksheet.

The Itemized Statement of Account is yet another document that bears resemblance to the Fee Worksheet. This statement is often provided by lenders to outline the various charges and credits associated with a loan. It includes a detailed list of fees, payments made, and any outstanding balances. Both the Itemized Statement of Account and the Fee Worksheet aim to provide a comprehensive view of the financial aspects of a mortgage, enabling borrowers to track their expenses and understand their financial commitments throughout the loan process.

When filling out the Fee Worksheet form, attention to detail is crucial. Here are five things to consider doing and avoiding:

Misconceptions about the Fee Worksheet form can lead to confusion for borrowers and service providers alike. Here are eight common misunderstandings explained:

Filling out and using the Fee Worksheet form is a crucial step in the loan settlement process. Here are five key takeaways to consider: