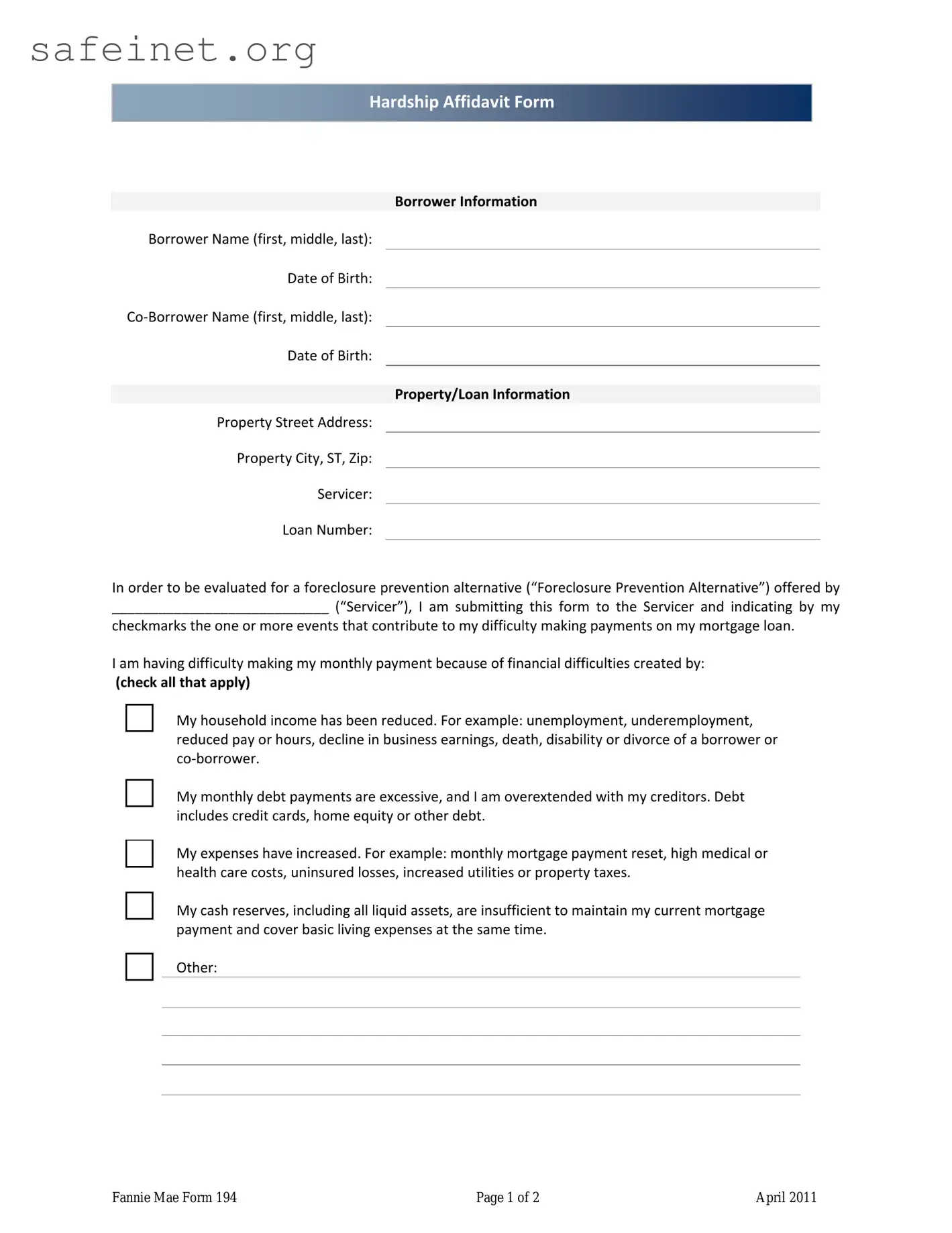

The Fannie Mae Form 194, often referred to as the Hardship Affidavit, plays a crucial role in the realm of mortgage assistance and foreclosure prevention. This form allows borrowers facing financial difficulties to outline their situations clearly and concisely. When submitting this affidavit to their mortgage servicer, individuals provide key personal information, including their names, dates of birth, and property details. The form also prompts borrowers to identify specific hardship events that have impacted their ability to make mortgage payments. These events can range from reduced household income due to job loss or underemployment, to excessive monthly debt burdens, increasing living expenses, or insufficient cash reserves. By checking the relevant boxes, borrowers indicate the factors contributing to their financial struggles. Additionally, the affidavit includes a series of acknowledgments and agreements, where borrowers certify the truthfulness of their claims and consent to potential investigations into their financial status. This underscores the seriousness of the affidavit and the responsibility borrowers assume when seeking assistance. Ultimately, Form 194 serves not only as a vital tool for individual homeownership stability but also as a mechanism for servicers to evaluate eligibility for various foreclosure prevention alternatives.

Hardship Affidavit Form

Borrower Information

Borrower Name (first, middle, last):

Date of Birth:

Co‐Borrower Name (first, middle, last):

Date of Birth:

Property/Loan Information

Property Street Address:

Property City, ST, Zip:

Servicer:

Loan Number:

In order to be evaluated for a foreclosure prevention alternative (“Foreclosure Prevention Alternative”) offered by

____________________________ (“Servicer”), I am submitting this form to the Servicer and indicating by my

checkmarks the one or more events that contribute to my difficulty making payments on my mortgage loan.

I am having difficulty making my monthly payment because of financial difficulties created by:

(check all that apply)

My household income has been reduced. For example: unemployment, underemployment, reduced pay or hours, decline in business earnings, death, disability or divorce of a borrower or co‐borrower.

My monthly debt payments are excessive, and I am overextended with my creditors. Debt includes credit cards, home equity or other debt.

My expenses have increased. For example: monthly mortgage payment reset, high medical or health care costs, uninsured losses, increased utilities or property taxes.

My cash reserves, including all liquid assets, are insufficient to maintain my current mortgage payment and cover basic living expenses at the same time.

Other:

Fannie Mae Form 194 |

Page 1 of 2 |

April 2011 |

Hardship Affidavit Form

Borrower/Co‐Borrower Acknowledgement and Agreement

1.I certify that all of the information in this Hardship Affidavit is truthful and the event(s) identified above has/have contributed to my need for a Foreclosure Prevention Alternative relating to my mortgage loan.

2.I understand and acknowledge the Servicer may investigate the accuracy of my statements, may require me to provide supporting documentation, and that knowingly submitting false information may violate Federal law.

3.I understand the Servicer may pull a current credit report on all borrowers obligated on the note relating to my mortgage loan.

4.I understand that if I have intentionally defaulted on my existing mortgage, engaged in fraud or misrepresented any fact(s) in connection with this Hardship Affidavit, or if I do not provide all of the required documentation, the Servicer may cancel a Foreclosure Prevention Alternative and may pursue foreclosure on my home.

5.I certify that I have not received a condemnation notice on my property.

6.I certify that I am willing to provide all requested documents and to respond to all Servicer communication in a timely manner. I understand that time is of the essence.

7.I understand that the Servicer may use this information to evaluate my eligibility for a Foreclosure Prevention Alternative, but the Servicer is not obligated to offer me assistance based solely on the representations in this Hardship Affidavit.

8.I understand that the Servicer may collect and record personal information, including, but not limited to, my name, address, telephone number, social security number, credit score, income, payment history, and information about account balances and activity. I understand and consent to the disclosure of my personal information and the terms of any Foreclosure Prevention Alternative offered by the Servicer to any investor, insurer, guarantor or servicer that owns, insures, guarantees or services my first lien or subordinate lien (if applicable) mortgage loan(s).

_________________________ ___________ |

_________________________ ____________ |

||

Borrower Signature |

Date |

Co‐Borrower Signature |

Date |

Fannie Mae Form 194 |

Page 2 of 2 |

April 2011 |

| Fact Name | Description |

|---|---|

| Purpose of the Form | The Fannie Mae 194 form is designed to collect information from borrowers facing financial hardships. It assists servicers in evaluating the borrowers' eligibility for foreclosure prevention alternatives. |

| Borrower Information Required | Borrowers must provide their names and dates of birth, along with information about any co-borrowers. This helps the servicer to accurately identify and evaluate each case. |

| Hardship Identification | Borrowers are required to check applicable reasons for their financial difficulties, such as reduced income or excessive debt. This section emphasizes the specific circumstances affecting the borrower’s ability to make payments. |

| Legal Acknowledgments | The form includes legal acknowledgments where borrowers certify the truthfulness of their information, understand potential consequences of false statements, and consent to credit checks. |

| States Governed by Specific Laws | In states like California, the form is governed by the California Civil Code, which outlines the obligations and protections for distressed homeowners in foreclosure situations. |

Carefully completing the Fannie Mae 194 form is an important step toward addressing mortgage payment difficulties. This document assesses your financial situation and is required for consideration of various foreclosure prevention alternatives. Following the steps outlined will ensure that you provide all necessary information accurately.

What is the purpose of the Fannie Mae 194 form?

The Fannie Mae 194 form, also known as the Hardship Affidavit, is designed for borrowers experiencing difficulties in making their mortgage payments. It allows borrowers to disclose the specific hardships they face, which may qualify them for foreclosure prevention alternatives offered by their loan servicer. Submitting this form is a crucial step in seeking assistance and helps lenders understand the financial circumstances impacting the borrower.

Who should complete the Fannie Mae 194 form?

Both the primary borrower and co-borrower should complete the Fannie Mae 194 form if applicable. This ensures that all parties involved in the mortgage are on the same page regarding their financial hardships. Accurate and full disclosure is essential for the servicer to evaluate the borrower’s situation effectively.

What information is required on the Fannie Mae 194 form?

The form requires information about the borrower's and co-borrower's names and dates of birth, as well as details about the property such as the address, city, state, and loan number. Additionally, borrowers must indicate the specific financial hardships they are facing by checking relevant boxes, such as reduced income or increased expenses.

How does a borrower submit the Fannie Mae 194 form?

To submit the Fannie Mae 194 form, borrowers typically send it directly to their loan servicer. This can often be done via email, mail, or a secure online platform provided by the servicer. It’s essential to follow any specific submission guidelines provided by the servicer to ensure timely processing.

What happens after the Fannie Mae 194 form is submitted?

After submission, the servicer will review the information provided to assess the borrower's eligibility for various foreclosure prevention alternatives. The servicer may contact the borrower for additional documentation or clarification. It’s important for the borrower to respond promptly to any requests for information.

Can falsifying information on the Fannie Mae 194 form lead to legal issues?

Yes, submitting false information on the Fannie Mae 194 form can lead to serious legal ramifications. If a borrower is found to have intentionally misrepresented their circumstances, they could face foreclosure or other legal actions. Servicers have the right to investigate the accuracy of the information provided.

What types of hardships can be reported on the Fannie Mae 194 form?

Borrowers can report various hardships on the form, including reduced household income, excessive monthly debt, increased expenses such as medical bills, and insufficient cash reserves. There is also an option for borrowers to describe any other hardships that may not be specifically listed.

Is there a deadline for submitting the Fannie Mae 194 form?

While there may not be a formal deadline for submitting the Fannie Mae 194 form, borrowers are encouraged to act quickly. Timely submission is crucial because it can affect the options available to the borrower regarding foreclosure prevention. It’s beneficial to submit the form as soon as difficulties in making payments arise.

What should borrowers do if they have questions while completing the Fannie Mae 194 form?

If borrowers have questions while filling out the Fannie Mae 194 form, they should reach out to their loan servicer. Most servicers have customer service representatives who can provide guidance. Understanding the form is vital, and servicers are there to assist throughout the process.

Incomplete Personal Information: Borrowers often neglect to fill in all sections, such as both the borrower and co-borrower's names and dates of birth. This omission can delay processing.

Failure to Specify Hardship: Many individuals either do not check any boxes or select too many options without providing specific details. Clear identification of the reason for financial difficulty is essential.

Inaccurate Information: Misrepresentation of facts, whether intentional or accidental, can lead to severe consequences. All statements must reflect the true circumstances of the borrower's situation.

Neglecting Documentation Requests: Borrowers sometimes forget to submit supporting documents as requested by the Servicer. This can thwart the evaluation process for Foreclosure Prevention Alternatives.

Ignoring Timeliness: Time-sensitive responses are critical. Many borrowers underestimate the importance of responding promptly to communications from the Servicer.

Signature Errors: Failing to sign the affidavit correctly, or overlooking the date of signature, can render the form invalid. Always ensure that all required signatures are present.

Assuming Eligibility Guarantees: Some borrowers mistakenly believe that completing the form guarantees a Foreclosure Prevention Alternative. It is crucial to understand that submission does not ensure assistance.

The Fannie Mae 194 form, also known as the Hardship Affidavit, is commonly used by borrowers facing financial difficulties to communicate their situation to their mortgage servicer. Along with this form, several other documents are typically required to assist in processing requests for foreclosure prevention alternatives. Below is a list of relevant forms and documents that borrowers may encounter during this process.

Each of these documents plays a crucial role in the evaluation of foreclosure prevention alternatives. By presenting accurate and complete information, borrowers can better communicate their needs and explore potential solutions with their servicer.

The Fannie Mae 194 form, known as the Hardship Affidavit, is designed to help borrowers communicate their financial difficulties to servicers. A similar document is the HUD-92070, often referred to as the Request for a Mortgage Assistance. Like the Fannie Mae 194, this form serves as a way for borrowers to disclose their financial hardships. It specifically facilitates the process of applying for assistance under various government programs. The HUD-92070 also emphasizes the importance of honesty and transparency, requiring borrowers to list specific financial difficulties that impact their ability to make mortgage payments. Both documents function as critical tools in the foreclosure prevention landscape, aiming to aid homeowners in distress by enabling them to explore available alternatives.

Another similar document is the FNMA 1040, which is typically used in conjunction with loan applications. This document is focused on disclosing relevant financial information, like income and debt obligations, to establish a borrower’s financial situation. While both the FNMA 1040 and the Fannie Mae 194 require borrowers to provide detailed accounts of their financial circumstances, the 1040 is driven more by the initial qualification process for new loans. Nevertheless, both documents underscore the necessity of accurate financial reporting to ensure that borrowers receive appropriate assistance based on their unique situations.

The Mortgage Assistance Application, often utilized by state and local agencies, bears similarities to the Fannie Mae 194 form as well. This application provides a comprehensive overview of a borrower's financial position. By outlining hardships and providing supporting documentation, borrowers can advocate for assistance from local and state programs. Just as the Fannie Mae 194 is intended to facilitate communication of financial distress, so does this document help in applying for localized support. Both documents serve as vital resources, aiming to prevent foreclosure and help families sustain homeownership.

Lastly, the Form 4506-T, which is used to request a tax transcript, also shares some connection to the Fannie Mae 194. Inability to provide adequate financial documentation can severely hinder the chances of securing assistance. While the Fannie Mae 194 aims to capture immediate hardships and necessary disclosures, the 4506-T serves as a verification tool. It allows servicers to cross-check income details against IRS records, ensuring the accuracy of the information submitted. Both forms highlight the critical role of documentation in the process of obtaining mortgage relief and draw attention to the necessity for honesty when communicating financial realities.

Things to Do When Filling Out the Fannie Mae 194 Form:

Things to Avoid When Filling Out the Fannie Mae 194 Form:

Understanding the Fannie Mae 194 form can be complicated. Here are six common misconceptions regarding this form:

Educating yourself about these misconceptions can help in making informed decisions regarding mortgage assistance.

Here are key takeaways for correctly filling out and using the Fannie Mae 194 form: