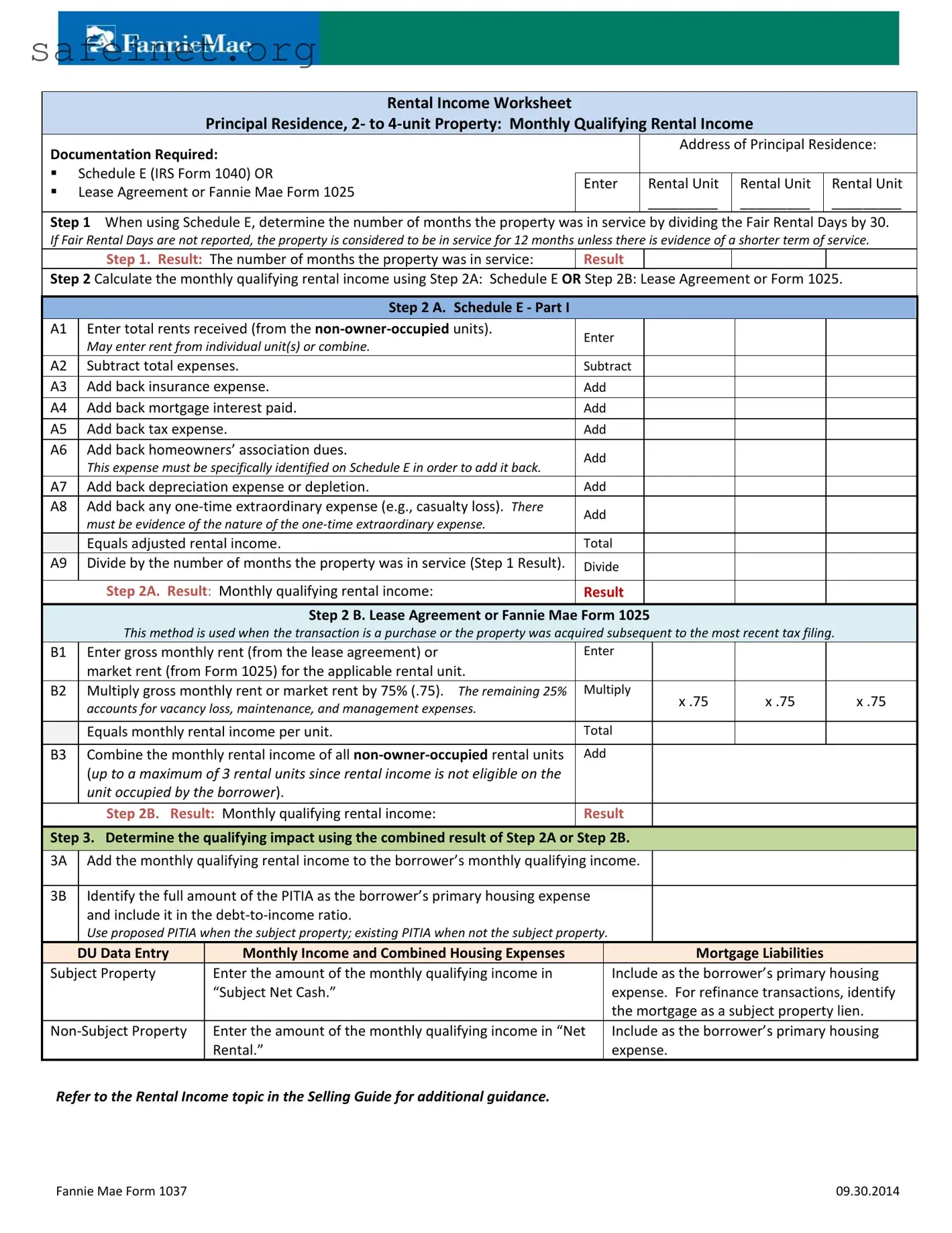

The Fannie Mae 1037 form is a critical tool for anyone looking to document rental income for a principal residence or a property with two to four units. This form serves to establish the monthly qualifying rental income that borrowers can use to support their mortgage applications. You’ll find that the form guides users through various steps for calculating this income, using either Schedule E from the IRS Form 1040 or a lease agreement. To get started, you’ll need information like the address of the principal residence and the rental unit details. The form emphasizes the importance of determining how long the property has been rented and calculating income after deducting allowable expenses. Additional allowances can also be considered, such as insurance, mortgage interest, and taxes, which can help in adjusting the rental income amount. If using a lease agreement or Fannie Mae Form 1025, you can directly determine the gross monthly rent, adjust it for potential vacancies and other expenses, and then sum the income from multiple rental units. By following these steps, you can efficiently assess the impact this income has on the borrower's overall debt-to-income ratio, making the Fannie Mae 1037 form a vital aspect of the mortgage process for property owners.

Rental Income Worksheet

Principal Residence, 2- to

Documentation Required: |

|

Address of Principal Residence: |

||||

|

|

|

|

|||

Schedule E (IRS Form 1040) OR |

|

|

|

|

||

Enter |

Rental Unit |

Rental Unit |

Rental Unit |

|||

|

Lease Agreement or Fannie Mae Form 1025 |

|||||

|

_________ |

_________ |

_________ |

|||

|

|

|

||||

Step 1 When using Schedule E, determine the number of months the property was in service by dividing the Fair Rental Days by 30. If Fair Rental Days are not reported, the property is considered to be in service for 12 months unless there is evidence of a shorter term of service.

Step 1. Result: The number of months the property was in service: |

Result |

|

|

|

Step 2 Calculate the monthly qualifying rental income using Step 2A: Schedule E OR Step 2B: Lease Agreement or Form 1025.

|

|

|

Step 2 A. Schedule E - Part I |

|

|

|

|

|

|

|

|

A1 |

Enter total rents received (from the |

Enter |

|

|

|

|

|

|

|

|

May enter rent from individual unit(s) or combine. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2 |

Subtract total expenses. |

Subtract |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A3 |

Add back insurance expense. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A4 |

Add back mortgage interest paid. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A5 |

Add back tax expense. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A6 |

Add back homeowners’ association dues. |

Add |

|

|

|

|

|

|

|

|

This expense must be specifically identified on Schedule E in order to add it back. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A7 |

Add back depreciation expense or depletion. |

Add |

|

|

|

|

|

|

|

A8 |

Add back any |

Add |

|

|

|

|

|

|

|

|

must be evidence of the nature of the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equals adjusted rental income. |

Total |

|

|

|

|

|

|

|

A9 |

Divide by the number of months the property was in service (Step 1 Result). |

Divide |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2A. Result: Monthly qualifying rental income: |

Result |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2 B. Lease Agreement or Fannie Mae Form 1025 |

|

|

|

|

||

|

|

|

This method is used when the transaction is a purchase or the property was acquired subsequent to the most recent tax filing. |

|

|

||||

|

|

B1 |

Enter gross monthly rent (from the lease agreement) or |

Enter |

|

|

|

|

|

|

|

|

market rent (from Form 1025) for the applicable rental unit. |

|

|

|

|

|

|

|

|

B2 |

Multiply gross monthly rent or market rent by 75% (.75). The remaining 25% |

Multiply |

x .75 |

|

x .75 |

|

|

|

|

|

accounts for vacancy loss, maintenance, and management expenses. |

|

x .75 |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equals monthly rental income per unit. |

Total |

|

|

|

|

|

|

|

B3 |

Combine the monthly rental income of all |

Add |

|

|

|

|

|

|

|

|

(up to a maximum of 3 rental units since rental income is not eligible on the |

|

|

|

|

|

|

|

|

|

unit occupied by the borrower). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2B. Result: Monthly qualifying rental income: |

Result |

|

|

|

|

|

Step 3. Determine the qualifying impact using the combined result of Step 2A or Step 2B.

Step 3. Determine the qualifying impact using the combined result of Step 2A or Step 2B.

3A Add the monthly qualifying rental income to the borrower’s monthly qualifying income.

3B Identify the full amount of the PITIA as the borrower’s primary housing expense and include it in the

Use proposed PITIA when the subject property; existing PITIA when not the subject property.

|

|

DU Data Entry |

Monthly Income and Combined Housing Expenses |

|

Mortgage Liabilities |

|

|

|

|

|

|||

|

|

Subject Property |

Enter the amount of the monthly qualifying income in |

|

Include as the borrower’s primary housing |

|

|

|

|

“Subject Net Cash.” |

|

expense. For refinance transactions, identify |

|

|

|

|

|

|

the mortgage as a subject property lien. |

|

|

|

|

|

|

|

|

|

|

Enter the amount of the monthly qualifying income in “Net |

|

Include as the borrower’s primary housing |

|

|

|

|

|

Rental.” |

|

expense. |

|

Refer to the Rental Income topic in the Selling Guide for additional guidance.

Fannie Mae Form 1037 |

09.30.2014 |

| Fact Name | Details |

|---|---|

| Purpose | The Fannie Mae 1037 form is a Rental Income Worksheet used to calculate monthly qualifying rental income for principal residences of 2- to 4-unit properties. |

| Documentation Needed | Borrowers must provide either the Schedule E from IRS Form 1040, a Lease Agreement, or Fannie Mae Form 1025 to support rental income claims. |

| In-Service Calculation | To determine how many months a property was in service, divide Fair Rental Days by 30. If Fair Rental Days are not available, assume 12 months in service unless evidence suggests otherwise. |

| Monthly Qualifying Rental Income Steps | Calculating rental income involves two potential methods: using Schedule E (Step 2A) or the Lease Agreement/Form 1025 (Step 2B). |

| Adjustment Process | Various expenses can be added back to the total rental income, including mortgage interest, insurance, and homeowners' association dues, to arrive at adjusted rental income. |

| Vacancy Loss Consideration | When using the Lease Agreement or Form 1025, the gross monthly rent is reduced by 25% to account for vacancy loss and maintenance costs. |

| Debt-to-Income Ratio | The calculated monthly qualifying rental income is included in the borrower’s debt-to-income ratio, impacting mortgage eligibility assessments. |

| State-Specific Variations | In some states, additional local laws may influence rental income documentation and calculation requirements. Check with local authorities for specifics. |

Completing the Fannie Mae 1037 form requires careful attention to financial details related to rental income for a principal residence. Gather the necessary documentation and follow these steps to accurately fill out the form.

What is the purpose of the Fannie Mae 1037 form?

The Fannie Mae 1037 form is designed to help lenders calculate the monthly qualifying rental income for properties that serve as a principal residence and contain two to four units. It details the necessary documentation and steps required to determine the rental income that can be used in qualifying a borrower for a mortgage. By using this form, lenders ensure they accurately assess rental income based on updated agreements or tax documentation, thereby providing a clearer picture of a borrower's financial situation.

What documentation is needed to complete the Fannie Mae 1037 form?

To properly complete the Fannie Mae 1037 form, you will need either Schedule E from the IRS Form 1040 or a lease agreement. If using Schedule E, it facilitates the calculation of rental income from non-owner-occupied units. For those using a lease agreement, the specified gross monthly rent must be provided. Additionally, if the form relies on specific expenses such as insurance or mortgage interest, those must also be documented adequately. This ensures that the estimated qualifying rental income is comprehensive and reflects the property’s financial performance accurately.

How do you calculate monthly qualifying rental income using the Fannie Mae 1037 form?

Calculating monthly qualifying rental income involves a systematic process. First, determine how many months the property was in service, typically calculated using Fair Rental Days. Then, either summarize the net rental income using Schedule E with adjustments for specific expenses or apply the gross rent from a lease agreement and adjust it to 75% to account for vacancy, maintenance, and management expenses. The resulting figures from these calculations yield the monthly rental income, which plays a critical role in evaluating the borrower’s financial viability.

What is the significance of including rental income in a borrower's debt-to-income ratio?

Including rental income in a borrower’s debt-to-income (DTI) ratio is significant because it helps lenders assess the borrower's capacity to manage monthly obligations in relation to their income. The rental income, when calculated accurately, can bolster the borrower's financial profile, making them a more attractive candidate for loan approval. It is essential to distinguish between qualifying rental income from non-owner-occupied units and the primary housing expenses associated with the borrower's principal residence, ensuring a precise DTI evaluation for a comprehensive assessment of financial health.

Neglecting to provide accurate rental documentation: Many applicants fail to attach the required documents, such as Schedule E or the lease agreement, which can lead to approval delays.

Miscalculating service months: When determining how long the property has been in service, some forget to divide Fair Rental Days by 30 or mistakenly assume they qualify for 12 months without supporting evidence.

Overlooking expenses on Schedule E: It's crucial to correctly list total rents received and to subtract relevant expenses. Failure to do this can inflate the adjusted rental income.

Ignoring the vacancy and maintenance adjustment: When using the lease agreement method, some overlook the 25% deduction for vacancy loss and management expenses, leading to an inaccurate rental income calculation.

Confusing primary housing expenses: Applicants often misidentify PITIA as primary housing expenses. It's essential to include the right figures to avoid misrepresenting the debt-to-income ratio.

Not reconciling qualifying income: Applicants sometimes fail to combine the monthly qualifying rental income with their primary income accurately. This step is vital for assessing financial eligibility.

The Fannie Mae 1037 form is used to document rental income for individuals who own properties and are looking to qualify for a mortgage. Along with this form, there are several other documents that play a crucial role in providing the necessary financial information and ensuring compliance with lending requirements. Each of these documents serves a unique purpose in the overall rental income verification process.

Collectively, these documents support the validation of rental income claimed on the Fannie Mae 1037 form. They help lenders make informed decisions, ensuring that borrowers are adequately assessed based on their financial capabilities and the income potential of their rental properties.

The Fannie Mae 1037 form has similarities to the IRS Schedule E form, which is used for reporting rental income and expenses from real estate that is rented or leased. Similar to the Fannie Mae 1037, Schedule E allows the taxpayer to list all sources of rental income and deduct associated expenses. Both documents require the identification of rental units and the calculation of net rental income after expenses, providing a method of establishing qualifying rental income for potential financing purposes.

An additional document that parallels the Fannie Mae 1037 is the Lease Agreement. This legal document outlines the terms under which a rental property is leased to tenants. In terms of rental income documentation, both the Lease Agreement and the Fannie Mae 1037 require specified amounts of monthly rent that can be projected as qualifying income. While the 1037 may also consider market rent based on standardized forms, the Lease Agreement provides concrete terms directly related to the tenancy, ensuring clear expectations between landlord and tenant.

Fannie Mae Form 1025 shares a close relationship with the 1037 form. Form 1025 is specifically utilized for reporting the income potential of multiple-unit properties and includes a methodology for calculating market rents. The incorporation of Form 1025 in the qualitative assessment of rental income aligns with the strategy employed in the Fannie Mae 1037 for establishing accurate revenue estimates. This allows for comparable income evaluations for properties undergoing financing assessments.

The 1040 form can also be likened to the Fannie Mae 1037. This individual income tax return includes supplemental schedules such as Schedule E for reporting rental income. The 1040 form as a whole provides comprehensive financial information that can substantiate the overall income and ability to repay loans or mortgages. Both documents integrate aspects of rental income into a broader financial framework needed for qualifying for different types of financing arrangements.

Lastly, the HUD-1 Settlement Statement serves a similar purpose by detailing all charges and credits involved in the closing of a real estate transaction, including rental income considerations. While primarily focused on settlement-related expenses, this document also outlines the financial obligations of the borrower and can reflect how rental income factors into debt calculations. The HUD-1 and Fannie Mae 1037 both enhance understanding of financial viability in real estate transactions, ensuring that comprehensive assessments are considered for qualified lending purposes.

When filling out the Fannie Mae 1037 form for rental income, attention to detail is crucial. Here’s a helpful list of dos and don’ts to ensure you complete the form accurately.

Misconceptions about the Fannie Mae 1037 Form

Filling out the Fannie Mae 1037 form requires careful attention to detail. Here are key takeaways to consider: