The Fannie 1084 form, also known as the Cash Flow Analysis, plays a crucial role in evaluating the income of self-employed borrowers. This tool is designed to assess the stability and continuity of a borrower’s income, which is essential for qualifying for loans. The Fannie 1084 form requires detailed information from various IRS tax documents, including Form 1040 and various schedules that pertain to personal and business income sources. Borrowers must provide information on self-employment income, rental income, capital gains, and various business expenses. Notably, the form also accounts for income from partnerships and S corporations through Schedule K-1, highlighting the importance of documentation to verify income distribution and business liquidity. Each section guides lenders through the necessary calculations to ensure accurate income representation, thereby facilitating informed lending decisions. This thorough evaluation not only assists lenders but also helps borrowers in demonstrating their financial capability to meet loan obligations.

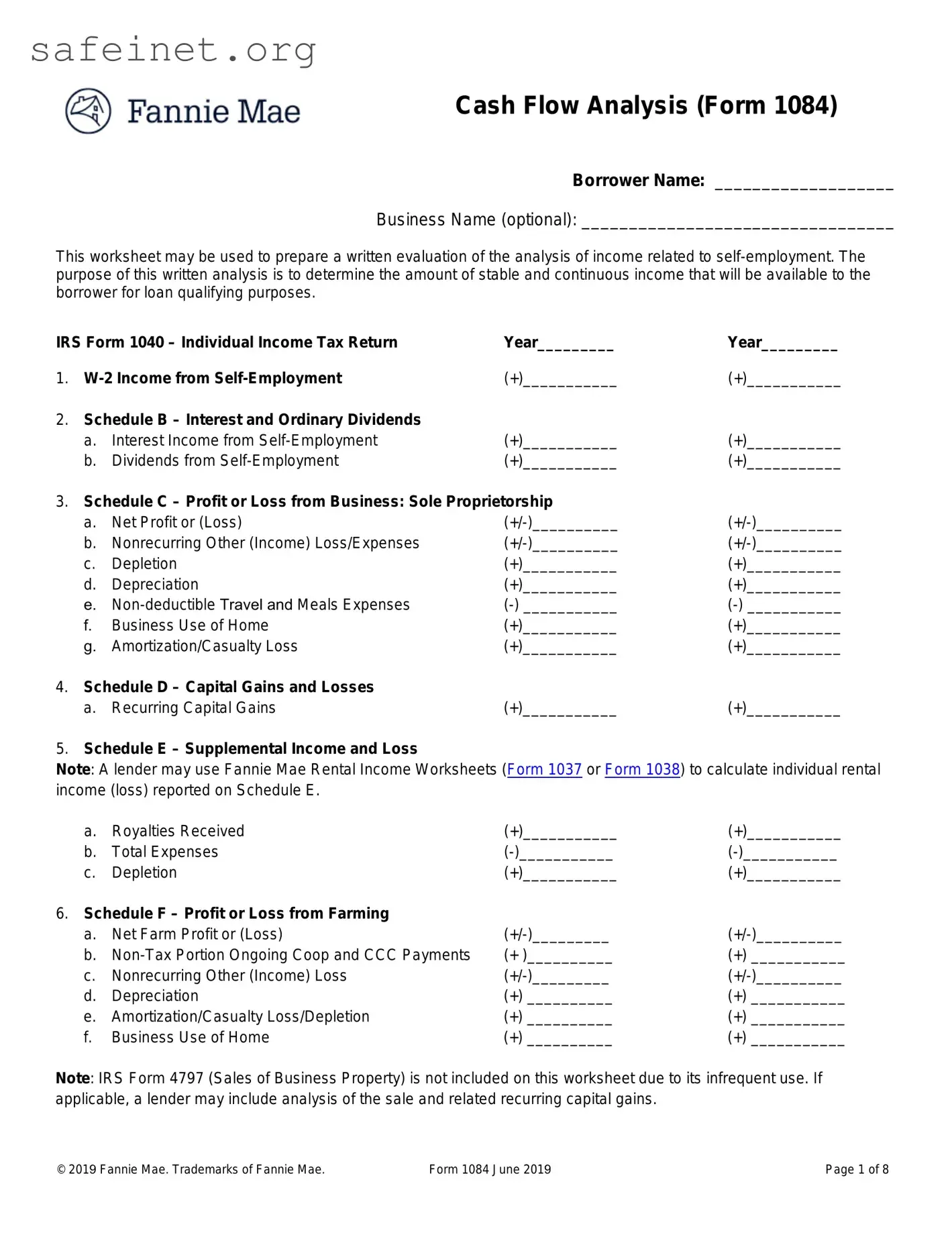

Cash Flow Analysis (Form 1084)

Borrower Name: ___________________

Business Name (optional): _________________________________

This worksheet may be used to prepare a written evaluation of the analysis of income related to

IRS Form 1040 – Individual Income Tax Return |

Year_________ |

Year_________ |

||

1. |

(+)___________ |

(+)___________ |

||

2. |

Schedule B – Interest and Ordinary Dividends |

|

|

|

|

a. |

Interest Income from |

(+)___________ |

(+)___________ |

|

b. |

Dividends from |

(+)___________ |

(+)___________ |

3.Schedule C – Profit or Loss from Business: Sole Proprietorship

a. Net Profit or (Loss) |

|||

b. Nonrecurring Other (Income) Loss/Expenses |

|||

c. |

Depletion |

(+)___________ |

(+)___________ |

d. |

Depreciation |

(+)___________ |

(+)___________ |

e. |

|||

f. |

Business Use of Home |

(+)___________ |

(+)___________ |

g. |

Amortization/Casualty Loss |

(+)___________ |

(+)___________ |

4.Schedule D – Capital Gains and Losses

a. Recurring Capital Gains |

(+)___________ |

(+)___________ |

5.Schedule E – Supplemental Income and Loss

Note: A lender may use Fannie Mae Rental Income Worksheets (Form 1037 or Form 1038) to calculate individual rental income (loss) reported on Schedule E.

a. |

Royalties Received |

(+)___________ |

(+)___________ |

b. |

Total Expenses |

||

c. |

Depletion |

(+)___________ |

(+)___________ |

6.Schedule F – Profit or Loss from Farming

a. Net Farm Profit or (Loss) |

|||

b. |

(+ )__________ |

(+) ___________ |

|

c. Nonrecurring Other (Income) Loss |

|||

d. |

Depreciation |

(+) __________ |

(+) ___________ |

e. |

Amortization/Casualty Loss/Depletion |

(+) __________ |

(+) ___________ |

f. |

Business Use of Home |

(+) __________ |

(+) ___________ |

Note: IRS Form 4797 (Sales of Business Property) is not included on this worksheet due to its infrequent use. If applicable, a lender may include analysis of the sale and related recurring capital gains.

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 1 of 8 |

Partnership or S Corporation

A

the income was actually distributed to the borrower, or

the business has adequate liquidity to support the withdrawal of earnings. If the Schedule

Note: See the Instructions for additional guidance on documenting access to income and business liquidity.

IRS Form 1065 - Partnership |

Income |

|

|

|

7. Schedule |

– Partner’s Share of Income |

Year__________ |

Year__________ |

|

a. |

Ordinary Income (Loss) |

|||

b. Net Rental Real Estate; Other Net Income (Loss) |

||||

c. |

Guaranteed Payments to Partner |

(+)____________ |

(+) ___________ |

|

8.Form 1065 - Adjustments to Business Cash Flow

a. Ordinary (Income) Loss from Other Partnerships |

|||

b. Nonrecurring Other (Income) Loss |

|||

c. |

Depreciation |

(+) __________ |

(+) ___________ |

d. |

Depletion |

(+) __________ |

(+) ___________ |

e. |

Amortization/Casualty Loss |

(+) __________ |

(+) ___________ |

f. Mortgages or Notes Payable in Less than 1 Year |

|||

g. |

|||

h. |

Subtotal |

____________ |

_____________ |

i. |

Total Form 1065 |

____________ |

_____________ |

|

(Subtotal multiplied by % of ownership) |

||

IRS Form 1120S – S Corporation Earnings |

Year__________ |

Year__________ |

9.Schedule

a. |

Ordinary Income (Loss) |

||

b. |

Net Rental Real Estate; Other Net Rental Income (Loss) |

||

10.Form 1120S - Adjustments to Business Cash Flow

a. Nonrecurring Other (Income) Loss |

|||

b. |

Depreciation |

(+)__________ |

(+)___________ |

c. |

Depletion |

(+)__________ |

(+)___________ |

d. |

Amortization/Casualty Loss |

(+)__________ |

(+)___________ |

e. Mortgages or Notes Payable in Less than 1 Year |

|||

f. |

|||

g. |

Subtotal |

____________ |

_____________ |

h. |

Total Form 1120S |

|

|

|

(Subtotal multiplied by % of ownership) |

____________ |

_____________ |

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 2 of 8 |

IRS Form 1120 – Regular Corporation

Corporation earnings may be used when the borrower(s) own 100% of the corporation.

11. Form 1120 – Regular Corporation |

Year_________ |

Year_________ |

|

|

|

||

a. |

Taxable Income |

____________ |

_____________ |

b. |

Total Tax |

||

c. |

Nonrecurring (Gains) Losses |

||

d. Nonrecurring Other (Income) Loss |

|||

e. |

Depreciation |

(+)__________ |

(+)___________ |

f. |

Depletion |

(+)__________ |

(+)___________ |

g. |

Amortization/Casualty Loss |

(+)__________ |

(+)___________ |

h. Net Operating Loss and Special Deductions |

(+)__________ |

(+)___________ |

|

i. Mortgages or Notes Payable in Less than 1 Year |

|||

j. |

|||

k. |

Subtotal |

____________ |

_____________ |

l. Less: Dividends Paid to Borrower |

|||

m. Total Form 1120 |

____________ |

_____________ |

|

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 3 of 8 |

CASH FLOW ANALYSIS (Fannie Mae Form 1084)

Instructions

Guidance for documenting access to income and business liquidity

If the Schedule

If the Schedule

IRS Form 1040 – Individual Income Tax Return

1.

2.Schedule B – Interest and Ordinary Dividends

Line 2a - Interest Income from

Line 2b - Dividends from

3.Schedule C – Profit or Loss from Business: Sole Proprietorship

Line 3a - Net Profit or Loss: Record the net profit or (loss) reported on Schedule C.

Line 3b - Nonrecurring Other (Income) Loss/ Expense: Other income reported on Schedule C represents income that is not directly related to business receipts. Deduct other income unless the income is determined to be recurring. If the income is determined to be recurring, no adjustment is required. Other loss may be added back when it is determined that the loss will not continue.

Line 3c - Depletion: Add back the amount of the depletion deduction reported on Schedule C.

Line 3d - Depreciation: Add back the amount of the depreciation deduction reported on Schedule C. Vehicle depreciation included as part of the standard mileage deduction may be added back by multiplying the business miles driven by the depreciation factor for the respective year.

Line 3e -

Line 3f - Business Use of Home: Add back the expenses deducted for the business use of home.

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 4 of 8 |

Line 3g - Amortization/Casualty Loss: Add back the expense deducted for amortization along with the expense associated with

4.Schedule D – Capital Gains and Losses

Line 4a - Recurring Capital Gains: Identify the amount of recurring capital gains. Schedule D may report business capital gains passed through to the borrower on Schedule

Note: Business capital losses identified on Schedule D do not have to be considered when calculating income or liabilities, even if the losses are recurring.

5.Schedule E – Supplemental Income and Loss

Note: Use Fannie Mae Rental Income Worksheets (Form 1037 or Form 1038) to evaluate individual rental income (loss) reported on Schedule E. Refer to Selling Guide,

Partnerships and S corporation income (loss) reported on Schedule E is addressed below.

Line 5a - Royalties Received: Include royalty income which meets eligibility standards.

Line 5b - Total Expenses: Deduct the expenses related to royalty income used in qualifying the borrower.

Line 5c - Depletion: Add back the amount of the depletion deduction related to royalty income used in qualifying the borrower.

6.Schedule F – Profit or Loss from Farming

Line 6a - Net Farm Profit or (Loss): Record the net farm profit or (loss) reported on Schedule F.

Line 6b -

Line 6c - Nonrecurring Other (Income) Loss: Other income reported on Schedule F represents income received by a farmer that was not obtained through farm operations. Deduct other income unless the income is determined to be recurring. If the income is determined to be recurring, no adjustment is required. Other loss may be added back when it is determined that the loss will not continue.

Line 6d - Depreciation: Add back the amount of the depreciation deduction reported on Schedule F.

Line 6e - Amortization/Casualty Loss/Depletion: Add back the expense deducted for amortization/depletion along with the expense associated with

Line 6f - Business Use of Home: Add back the expenses deducted for the business use of home.

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 5 of 8 |

Partnership or S Corporation

IRS Form 1065 – Partnership Income

7.Schedule

Line 7a - Ordinary Income (Loss): Record the amount of ordinary income (loss) reported to the borrower in Box 1 of Schedule

Line 7b - Net Rental Real Estate; Other Net Income (Loss): Record the amount of net rental real estate; other net income (loss) reported to the borrower in Box 2 and/or 3 of Schedule

Line 7c - Guaranteed Payments to Partner: Add guaranteed payments to partner when the borrower has a two- year history of receipt.

8.Adjustments to Business Cash Flow – Form 1065

When business tax returns are obtained by the lender, the following adjustments to business cash flow should be made.

Line 8a - Ordinary income (loss) from other Partnerships: In order to consider ordinary income from other partnerships, the lender must obtain additional documentation to confirm the income passed through from the other partnership to the borrower’s business meets partnership income eligibility standards. Deduct ordinary income passed through to the borrower’s business from other partnerships unless this additional action is taken. Losses passed through to the borrower’s business may be added back when the lender determines

Line 8b - Nonrecurring Other (Income) Loss: Other income reported on Form 1065 generally represents income that is not directly related to business receipts. Deduct other income unless the income is determined to be recurring. If the income is determined to be recurring, no adjustment is required. Other loss may be added back when it is determined that the loss will not continue.

Line 8c - Depreciation: Add back the amount of the depreciation deduction reported on Form 1065 and/or on Form 8825.

Line 8d - Depletion: Add back the amount of the depletion deduction reported on Form 1065.

Line 8e - Amortization/Casualty Loss: Add back the expense deducted for amortization/depletion along with the expense associated with

Line 8f - Mortgage or Notes Payable in Less than 1 Year: Subtract the amount of mortgage or note obligations payable in less than one year, as reported in Schedule L of Form 1120S, end of year column. This deduction is not required for lines of credit or if there is evidence that these obligations roll over regularly and/or the business has sufficient liquid assets to cover them.

Line 8g -

Line 8h - Subtotal: Total lines 8a – 8g.

Line 8i - Form 1065 Total: To arrive at the borrower’s proportionate share of adjustments to business cash flow, multiply the subtotal (line 8h) by the borrower’s percentage of ownership (the borrower’s ending percentage of capital ownership as reported on the Schedule

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 6 of 8 |

IRS Form 1120S – S Corporation Earnings

9.Schedule

Line 9a - Ordinary Income (Loss): Record the amount of ordinary income (loss) reported to the borrower in Box 1 of Schedule

Line 9b - Net Rental Real Estate; Other Net Income (Loss): Record the amount of net rental real estate; other net income (loss) reported to the borrower in Box 2 and/or 3 of Schedule

10.Adjustments to Business Cash Flow – Form 1120S

When business tax returns are obtained by the lender, the following adjustments to business cash flow should be made.

Line 10a - Nonrecurring Other (Income) Loss: Other income reported on Form 1120S generally represents income that is not directly related to business receipts. Deduct other income unless the income is determined to be recurring. If the income is determined to be recurring, no adjustment is required. Other loss may be added back when it is determined that the loss will not continue.

Line 10b - Depreciation: Add back the amount of the depreciation deduction reported on Form 1120S and/or or Form 8825.

Line 10c - Depletion: Add back the amount of the depletion deduction reported on Form 1120S.

Line 10d - Amortization/Casualty Loss: Add back the expense deducted for amortization/depletion along with the expense associated with

Line 10e - Mortgage or Notes Payable in Less than 1 Year: Subtract the amount of mortgage or note obligations payable in less than one year, as reported in Schedule L of Form 1120S, end of year column. This deduction is not required for lines of credit or if there is evidence that these obligations rollover regularly and/or the business has sufficient liquid assets to cover them.

Line 10f -

Line 10g - Subtotal: Total lines 10a – 10f.

Line 10h - Form 1120S Total: To arrive at the borrower’s proportionate share of adjustments to business cash flow, multiply the subtotal (line 10g) by the borrower’s percentage of stock for tax year reported on the Schedule

IRS Form 1120 – Regular Corporation

11.Regular Corporation – Form 1120

When business tax returns are obtained by the lender, the following adjustments to business cash flow should be made.

Line 11a - Taxable Income: Record the taxable income reported by the business on the first page of Form 1120.

Line 11b - Total Tax: Deduct the corporation‘s tax liability identified on page 1 of Form 1120.

Line 11c - Nonrecurring Other (Gains) Losses: Deduct gains unless it is determined that the gains are likely to continue. Losses may be added back when it can be determined that the loss is a

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 7 of 8 |

Line 11d - Nonrecurring Other (Income) Loss: Other income reported on Form 1120 generally represents income that is not directly related to business receipts. Deduct other income unless the income is determined to be recurring. If the income is determined to be recurring, no adjustment is required. Other loss may be added back when it is determined that the loss will not continue.

Line 11e - Depreciation: Add back the amount of the depreciation deduction reported on Form 1120.

Line 11f - Depletion: Add back the amount of the depletion deduction reported on Form 1120S.

Line 11g - Amortization/Casualty Loss: Add back the expense deducted for amortization/depletion along with the expense associated with

Line 11h - Net Operating Loss and Special Deductions: Add back the full amount of the deduction related to net operating loss and/or special deductions.

Line 11i - Mortgage or Notes Payable in Less than 1 Year: Subtract the amount of mortgage or note obligations payable in less than one year, as reported in Schedule L of Form 1120S, end of year column. This deduction is not required for lines of credit or if there is evidence that these obligations roll over regularly and/or the business has sufficient liquid assets to cover them.

Line 11j -

Line 11k - Subtotal: Total lines 11a – 11j.

Line 11l - Dividends Paid to Borrower: Dividends paid to stockholders are reported on Schedule

Line 11m - Form 1120 Total: Subtract 11l from 11k to determine the adjustments to business tax flow that may be considered when the borrower(s) own 100% of the corporation and the business has adequate liquidity to support the withdrawal of earnings.

© 2019 Fannie Mae. Trademarks of Fannie Mae. |

Form 1084 June 2019 |

Page 8 of 8 |

| Fact Name | Description |

|---|---|

| Purpose | The Fannie 1084 form is designed to evaluate income for self-employed borrowers, determining stable income for loan qualification. |

| IRS Forms Used | This form references multiple IRS forms, including 1040, 1065, 1120, and 1120S, to analyze various income sources. |

| Income Sources | Borrowers can assess income from various sources like W-2 self-employment income, Schedule C profits, and partnership earnings. |

| Document Requirements | Lenders must obtain verifiable documentation, such as Schedule K-1, to confirm income distributions for partnerships or S Corporations. |

| Stable Income Evaluation | The analysis identifies recurring income. Nonrecurring items may be adjusted during review, particularly when they do not reflect ongoing earnings. |

| State-Specific Applicability | Form 1084 may be governed by state lending laws, which may vary by jurisdiction. Always consult local regulations for compliance. |

After gathering the necessary information, it’s important to carefully fill out the Fannie 1084 form to calculate your cash flow analysis related to self-employment income. Each section requires specific details from your financial records to ensure accurate assessment and documentation for loan qualification purposes.

What is the purpose of the Fannie 1084 form?

The Fannie 1084 form is designed to assist in the cash flow analysis of self-employed borrowers. This form serves to evaluate the income related to a borrower's self-employment, allowing lenders to determine the amount of stable and continuous income available for loan qualifying purposes. Essentially, it provides a structured way to document various income sources and expenses while following guidelines set forth by Fannie Mae.

What types of income should be reported on the Fannie 1084 form?

The Fannie 1084 gathers various types of income, including W-2 income from self-employment, interest and dividends, business profits, rental income, and farm earnings, among others. It incorporates data from IRS forms such as Schedule C for sole proprietorships, Schedule E for supplemental income, and Schedule F for farming income. Each section allows for a detailed accounting of all relevant income that can contribute to the borrower’s overall cash flow.

How can business expenses affect the cash flow calculation?

Business expenses play a crucial role in the cash flow analysis outlined in the Fannie 1084 form. The form provides areas to deduct non-deductible expenses and nonrecurring losses while allowing for the addition of certain deductions back into the cash flow. For instance, depreciation and expenses related to business use of the home can be added back. This approach enables a more accurate representation of the income available for loan qualification by adjusting for expenses that may not reflect ongoing cash flow realities.

What documentation is required to support income reported on the Fannie 1084 form?

To use the income reported on the Fannie 1084, supporting documentation is essential. This may include various IRS forms such as Schedule K-1 for partnerships or S corporations, Form 1065 for partnerships, and Form 1120S for S corporations. It’s important that lenders obtain verification that any income reported has been consistently distributed to the borrower. If the borrower’s income history does not reflect consistency, lenders must also confirm that the business maintains adequate liquidity to support the income being used for qualification purposes.

What is the importance of accurately reporting income on the Fannie 1084 form?

Accurate reporting of income on the Fannie 1084 form is vital in determining a borrower's eligibility for a loan. Misrepresenting income or failing to provide complete information can lead to loan denial or complications during the underwriting process. The detailed breakdown encourages transparency and provides lenders with a comprehensive view of a borrower’s financial situation, aiding in making informed lending decisions. This accuracy not only affects the borrower’s ability to secure financing but can also influence the overall relationship with the lender.

Failure to Complete All Required Fields: One common mistake is neglecting to fill in all pertinent sections of the Fannie 1084 form. Each segment, including borrower and business names, must be completed accurately to avoid delays.

Inaccurate Reporting of Income: Individuals often misreport their income from self-employment. Ensure that the amounts entered for W-2 income, dividends, and business profits precisely reflect what is reported on associated tax forms, such as the IRS Form 1040 and Schedules B and C.

Omitting Nonrecurring Income and Losses: Some borrowers fail to correctly address nonrecurring income or losses. Understanding which income is stable and can be counted towards cash flow is crucial for accurate assessment.

Ignoring Relevant Documentation: Lenders require documentation like Schedule K-1 forms to confirm income distribution from partnerships or S corporations. Neglecting to provide this documentation can result in a denial or delay in processing the application.

Improperly Accounting for Depreciation: Borrowers may incorrectly handle depreciation expenses by failing to add back the correct amounts that should be considered for cash flow calculations. This can significantly skew the financial picture presented to lenders.

Not Differentiating Between Business and Personal Expenses: Mixing personal expenses with business ones often leads to inaccuracies. It is essential to clearly segregate these expenses to provide an honest representation of business profitability.

The Fannie Mae Form 1084, or the Cash Flow Analysis form, plays a crucial role in evaluating a borrower’s income from self-employment for loan qualification. However, this form is often accompanied by several other documents that provide essential information about the borrower’s financial situation. Understanding these related forms can help paint a more complete picture of a borrower’s ability to repay a loan. Below is a list of these documents and a brief description of each.

Each document contributes valuable information that informs a lender’s decision-making process. Collectively, they help establish a borrower’s financial health, ensuring decisions are made based on a thorough understanding of the borrower’s income and the sustainability of that income over time.

The IRS Form 1040, or the Individual Income Tax Return, bears similarities to the Fannie 1084 form in that both aim to assess an individual's income for financial and lending purposes. The 1040 summarizes a taxpayer's annual earnings, detailing various income sources and providing deductions and credits that impact taxable income. Lenders often refer to this form to evaluate a borrower's financial health, especially when determining eligibility for loans. Just like the Fannie 1084, the Form 1040 facilitates a comprehensive understanding of an individual's earnings and their capacity to repay debt, making it a key document in the income analysis process.

The IRS Schedule C, which reports the Profit or Loss from Business, is another critical document that closely aligns with the Fannie 1084. Self-employed individuals complete Schedule C to detail income and expenses linked to their business activities. This form is pivotal in demonstrating a borrower's income stability and continuity. Similar to the Fannie 1084’s focus on cash flow analysis, Schedule C provides insights into the operational profits or losses of a business, making it an essential tool for lenders to assess self-employed borrowers' financial situations accurately.

IRS Form 1065, Partnership Income, shares commonalities with the Fannie 1084 as it substantiates the income earned by partnerships. Similar to the analysis provided in the 1084 form, Form 1065 breaks down a partnership's financial performance, allowing some of that income to flow through to partners, which the lender can consider when evaluating their loan application. By reviewing Form 1065, lenders can ascertain the financial viability of a partnership and its capacity to support distributions to its partners, just as the Fannie 1084 requires proof of stable income for qualifying purposes.

Similarly, Schedule K-1 from Form 1065, which details a partner's share of income, loss, deductions, and credits, is also comparable to the Fannie 1084. This document further clarifies a partner's financial interest in the business and specifies any distributions received. Lenders use this information to confirm that self-employed borrowers have stable income from partnerships and assess whether these earnings can be counted toward qualifying for loans, echoing the Fannie 1084's objective of analyzing cash flow.

IRS Form 1120S, used for S Corporations, parallels the Fannie 1084 form by detailing the corporate income that flows through to its shareholders. This form informs lenders about the earnings retained by S Corporations and those distributions available to shareholders, similar to how the Fannie 1084 evaluates income sources. Both documents serve as critical resources for understanding the potential cash flow that borrowers may access, thereby influencing their loan eligibility.

Also worth mentioning is Schedule K-1 from Form 1120S, which outlines a shareholder’s share of income, deductions, and credits from an S Corporation. Like the data compiled in the Fannie 1084, this form provides important indicators of the income that shareholders can utilize. Lenders often analyze this document to understand the borrower’s financial health better and ascertain whether the income reported can be reliably counted for loan qualification purposes.

Finally, IRS Form 1120, the corporate income tax return for Regular Corporations, is analogous to the Fannie 1084 in its role of presenting corporate financial performance. This form shows the taxable income, which can be essential for understanding the overall financial health of a business and the income potentially accessible to shareholders. Both the 1120 and the 1084 are utilized by lenders to evaluate the financial standing of a borrower in relation to their debts, ensuring a thorough assessment of their cash flow position before making lending decisions.

When filling out the Fannie Mae Form 1084 for Cash Flow Analysis, it’s essential to be meticulous in your approach. Here’s a guide on what to do and what to avoid while completing this form.

Successfully completing the Fannie Mae Form 1084 involves careful attention to detail and accurate representation of financial data. Following these guidelines can simplify the process and enhance your eligibility for loan approval.

Misconception 1: The Fannie 1084 form is exclusively for sole proprietors.

This is not accurate. While the form caters to sole proprietorships, it also accommodates income reporting from partnerships and S corporations. Documentation like Schedule K-1 allows for a wider range of income sources to be analyzed.

Misconception 2: Only profit is considered in cash flow analysis.

This is misleading. The form takes into account not only profits but also losses and nonrecurring incomes or losses. Adjustments are made to ensure an accurate picture of the borrower's financial situation.

Misconception 3: The form does not require supporting documentation.

This is incorrect. For income to be eligible for cash flow analysis, lenders must obtain necessary documentation, such as IRS forms, that verify income sources. The form relies heavily on structured records for accurate analysis.

Misconception 4: All business-related expenses can be deducted.

This is not true. Only certain expenses can be deducted, and some, like non-deductible travel and entertainment expenses, need to be factored back into the analysis. Attention to detail is critical to ensure accurate calculations.

Misconception 5: The Fannie 1084 form guarantees loan approval.

This is misleading. The form is a tool that assists lenders in understanding a borrower’s cash flow, but loan approval depends on various factors beyond just the analysis from this form. Other criteria also play a significant role in the lending decision.

Gather the relevant financial documents before starting the Fannie 1084 form. This includes completing IRS Forms 1040, 1065, 1120, and 1120S, as well as obtaining Schedule K-1s as applicable.

Clearly identify all sources of income on the form. Include W-2 income, dividends, interest, and any net profits or losses from self-employment. Accurate reporting is crucial for loan qualification.

Ensure that any nonrecurring income or expenses are adjusted appropriately. If income is deemed recurring, no adjustment is necessary; otherwise, deductions should be made for nonrecurring items.

Check for business liquidity documentation. If the distributions of income are confirmed by Schedule K-1, further documentation may not be needed. Ensure verification of access to income where necessary.

Regularly reassess the information provided. Income and expenses can change; thus, it is essential to continually monitor business financial health to maintain accuracy for future assessments.