The Family Chore Chart form serves as a practical tool designed to encourage financial literacy and responsibility among tweens. This form not only lays the groundwork for managing an allowance system but also integrates various elements aimed at enhancing savings habits. At its core, the form prompts families to establish a chore chart that tracks completed tasks, thereby ensuring children earn the money they receive. Additional incentives, such as extra earnings for completing seasonal chores, are encouraged to teach the value of hard work. Furthermore, the form advocates for setting a regular pay day, allowing tweens to develop budgeting skills as they plan their spending and saving around these intervals. Incorporating a monthly calendar also provides a visual aid for tracking financial goals and wish list items, fostering proactive financial planning. Engaging trusted adults to impart financial wisdom further enriches the child's learning experience, ensuring that important lessons about money management resonate beyond the confines of family discussions. Ultimately, the Family Chore Chart form highlights the importance of instilling a sense of financial responsibility early in life, equipping children with the necessary tools to make informed financial choices as they grow.

M ney Talks To Tweens

ney Talks To Tweens

and their families

Brought to you by your local bank and the ABA Education Foundation

Quick Tips to Help

Your Tween

Save Money!

1 If your tween has spending money, have him write a list of the things he’d like to purchase. Prioritize the list and discuss the choices, even research the lowest prices.

2 Help your tween earn extra money by suggesting he start a paper route or a

3 Set up an automatic savings plan for college or other expenses for your child. Putting away $5 a week over 18 years is $4680 — even more with interest earned if the money is in a bank account.

4 Have your tween wait at least

48 hours before buying an impulse purchase. If he still wants to buy the video game or CD a couple of days or a week later, you can be confident about it too.

It’s Pay Day!

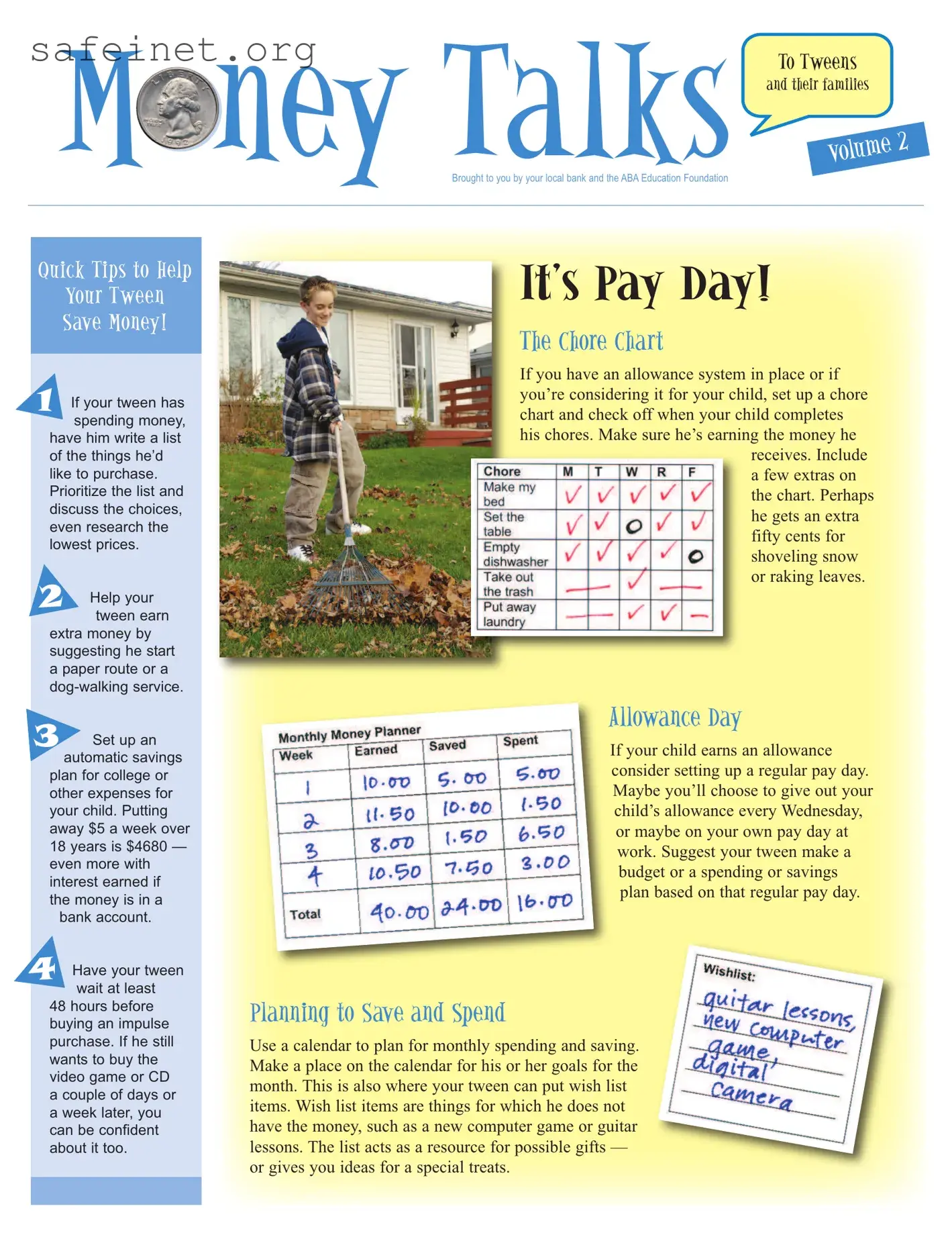

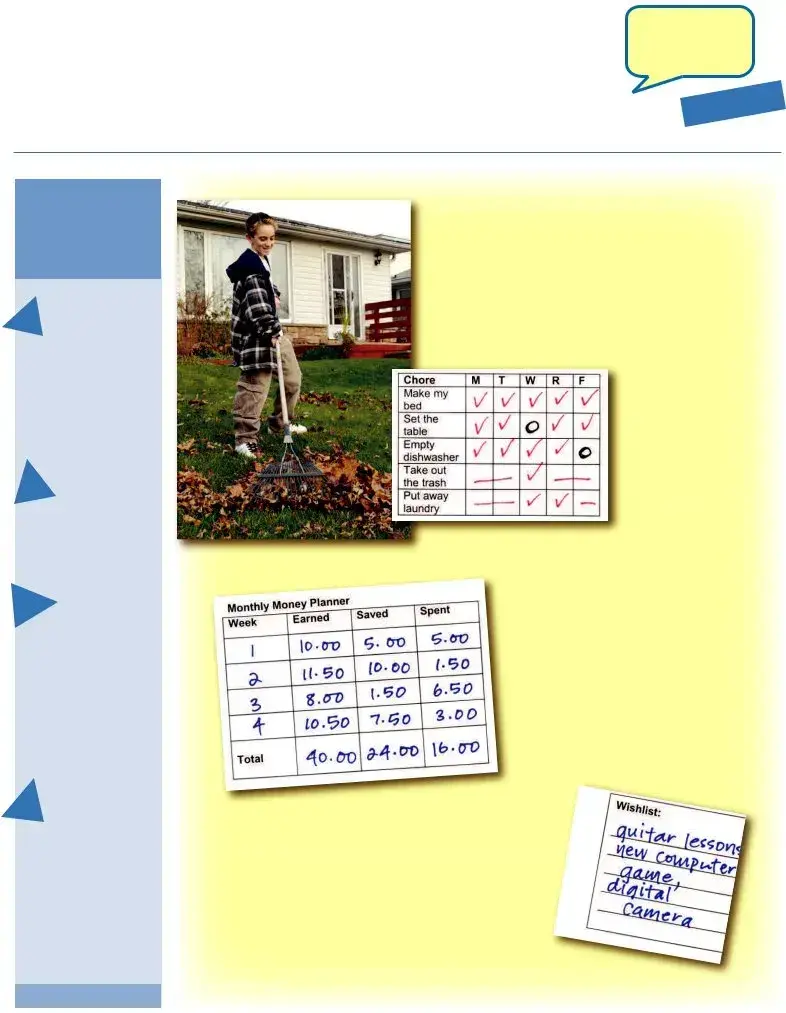

The Chore Chart

If you have an allowance system in place or if you’re considering it for your child, set up a chore chart and check off when your child completes his chores. Make sure he’s earning the money he

receives. Include a few extras on the chart. Perhaps he gets an extra fifty cents for shoveling snow or raking leaves.

Allowance Day

If your child earns an allowance consider setting up a regular pay day. Maybe you’ll choose to give out your child’s allowance everyWednesday, or maybe on your own pay day at work. Suggest your tween make a budget or a spending or savings plan based on that regular pay day.

Planning to Save and Spend

Use a calendar to plan for monthly spending and saving. Make a place on the calendar for his or her goals for the month.This is also where your tween can put wish list items.Wish list items are things for which he does not have the money, such as a new computer game or guitar lessons.The list acts as a resource for possible gifts — or gives you ideas for a special treats.

Enlist Someone Cool

Enlist Someone Cool

Parents,guardiansandgrandparentsknowthattothetweenintheirlife,adults

If all of your talking about the importance ofsavingandplanningforthefuturedoesn’t seemtobesinkinginwithyourtween spender,enlistsomeoneheorshethinksis cool.Maybeit’syourdaughter’sbabysitter, alifeguardatthepool,oryourson’ssoccer coach.Asksomeonewithwhomyourchild hasaconnection.

Encouragethatspecialpersoninyour child’slifetodiscussafewbasicmessages aboutsavingandbudgeting.Perhapsyour daughter’sbabysitterwillshareherstoryof savingforherschooltrip.Yourson’ssoccer coachmighthaveagreatstoryabouthowhe

madeextramoneydoingneighbors’chores.Thelifeguardatthepoolmightbe abletoshareacautionarystoryabouthowsheblewlastyear’ssummerwages onatriptothebeach,whenhewassupposedtousehissavingsforadown paymentonacar.WhetherthetalesarebasedonwhattodoorwhatNOTto do,theywillbeinstructive.

Check Out These Books!

Visit your local library or bookstore …

Earning Money: How

Economics Works

By Patricia J. Murphy

This book details how to earn money, either by

requesting an allowance or starting a

Money Sense for Kids

By Hollis Page Harman

This book introduces different types of U.S. currency, an explanation of the complicated path

that money takes from the mint to banks to the consumer, how to earn money and how to make it grow by investing in stocks and bonds. Clear,

Click Your Mouse Here

http://pbskids.org/dontbuyit

(Corporation for Public Broadcasting and Public Broadcasting Service)

Yet another site developed specifically for tweens, Don’t Buy It: Get Media Smart is a media literacy Web site for young people that encourages users to think critically about media and become smart consumers. Activities on the site are designed to provide users with some of the skills and knowledge needed to question, analyze, interpret and evaluate media messages.

www.plasticforkdiaries.com (Maryland Public Television)

This Web site especially for tweens follows six middle school students as they experience

The ABA Education Foundation, a

© 2007 American Bankers Association Education Foundation, Washington, DC. Permission to reprint granted.

| Fact Name | Description |

|---|---|

| Purpose | The Family Chore Chart helps families organize and track chore completion by children, allowing for an effective allowance system. |

| Connection to Financial Literacy | This chart promotes financial literacy by encouraging tweens to earn money through chores and make responsible spending choices. |

| Pay Day Flexibility | Families can set a regular allowance pay day that best suits their schedules, whether it's weekly or on a designated pay day. |

| Incentives | Parents can add incentives to the chore chart, such as additional payments for extra tasks, to motivate children further. |

| Goal Setting | The chart allows tweens to incorporate goal-setting in planning their spending and savings, fostering a sense of responsibility and planning. |

The Family Chore Chart is designed to help families organize chores and track allowances effectively. By following the steps below, those involved can create a functional and motivating chart for managing household responsibilities.

What is the Family Chore Chart, and how does it work?

The Family Chore Chart serves as a visual aid to help children manage their responsibilities and, in return, earn an allowance. Parents can set up a chore list—assigning tasks that must be completed for payments to be made. Each time a chore is finished, it can be checked off the list. This system not only teaches children accountability but also rewards their efforts with tangible benefits, like extra money for additional tasks, such as shoveling snow or raking leaves.

How can I effectively implement an allowance system using the chore chart?

To implement an allowance system effectively, decide on a regular pay day. For example, some families choose Wednesdays, while others might align it with their own pay schedule. It's crucial to ensure that the allowance reflects the chores completed by the child. By connecting the allowance directly to work done, you teach the importance of earning instead of simply receiving. To deepen understanding of budgeting, encourage your child to create a spending or savings plan based on their allowance, fostering early financial literacy.

What are some tips for helping my tween develop good financial habits?

There are several strategies to instill sound financial habits in your tween. Begin by discussing spending priorities; ask them to list items they want and rank them. This dialogue opens the door for discussions about making wise choices and researching prices. Additionally, consider setting up an automatic savings plan for future expenses like college. Recommend a waiting period for impulse buys—suggest that your child waits 48 hours before deciding whether to purchase something. This strategy can help reduce frivolous spending and promote thoughtful decision-making.

How can I encourage my tween to talk about money management with trusted adults?

Engaging your tween in conversations about money management can be enhanced by involving other trusted adults. Identify someone your tween looks up to—perhaps an older sibling, a teacher, or a coach. Ask them to share their experiences related to saving and budgeting. Hearing personal stories from role models can make the lessons more relatable and impactful. Such shared experiences often resonate more than parental advice alone, reinforcing the importance of making financial decisions wisely.

Failing to read all instructions thoroughly can lead to confusion and incomplete submissions.

Omitting family members' names results in a lack of clarity regarding responsibilities.

Leaving chore descriptions vague does not provide enough detail for proper execution.

Not assigning values to each chore can cause misunderstandings about allowance amounts.

Forgetting to update the chart regularly can lead to ineffective tracking of completed chores.

Neglecting to discuss chores as a family may leave some members unaware of expectations.

Underestimating the importance of setting realistic expectations can lead to frustration.

Failing to include some fun or rewarding activities can discourage participation in chores.

Not reviewing the chart together can lead to a lack of motivation and accountability.

Ignoring input from children on preferred chores may result in disengagement from the process.

The use of the Family Chore Chart form is often accompanied by various other documents and resources that can aid in teaching children about responsibility, budgeting, and financial literacy. Below is a list of documents that complement the chore chart, each serving a unique purpose in family management and education.

By utilizing these additional documents and resources, families can create a comprehensive framework for teaching valuable life skills. Together, they work to foster a sense of responsibility and financial awareness in children, preparing them for future success.

The Family Chore Chart is reminiscent of a behavior modification chart used in various educational settings. Both tools are designed to encourage and track the performance of specific tasks or behaviors. In schools, such charts often reward students for completing academic assignments or demonstrating good behavior, much like a chore chart rewards children for completing household tasks. The focus is on accountability and tangible rewards, reinforcing positive habits over time.

Another similar document is a daily or weekly planner. Both a chore chart and a planner help individuals organize their tasks and responsibilities. While the planner serves a broader purpose by allowing for scheduling of appointments, assignments, and personal goals, the chore chart specifically tracks household duties. Each encourages time management and prioritization, promoting a structured approach to completing necessary activities.

Bullet journals share similarities with the Family Chore Chart as well. Both serve as creative outlets for tracking progress and responsibilities. With bullet journals, users customize layouts and designs, making tracking enjoyable. The chore chart’s straightforward design focuses primarily on chores, but both documents encourage consistency and reflection on completed tasks, fostering a sense of achievement.

Goal-setting worksheets are another comparable document. A Family Chore Chart can include specific goals related to household responsibilities, similar to how goal-setting worksheets outline personal, educational, or professional aspirations. Both tools encourage individuals to define objectives and monitor their progress toward achieving them, enhancing motivation and accountability.

The concept of a family calendar also aligns with the Family Chore Chart. While a family calendar outlines events, appointments, and special occasions, it can also incorporate chore schedules. Both documents serve to keep family members informed about responsibilities and commitments, fostering communication and cooperation within the home.

Similar to the Family Chore Chart, a rewards system or incentive chart is used to motivate children to complete tasks. Parents might design a rewards chart that allows children to earn points or stickers for chores completed, redeemable for desired rewards. Both systems promote responsibility and create a positive association with completing tasks, encouraging continued participation.

Visual aids, such as charts or infographics illustrating chores and responsibilities, are also related to the Family Chore Chart. These visuals simplify complex information, making it easier for children to understand what is expected of them. Just like the chore chart, these visual aids serve to engage family members and promote a sense of ownership over their responsibilities.

Lastly, a weekly meal plan shares similarities with the Family Chore Chart. Both documents aim to organize and simplify family life. A meal plan outlines meals for the week, ensuring that dietary needs are met while a chore chart outlines household duties, ensuring that the home remains organized and clean. Both encourage planning ahead, establishing routines, and maximizing efficiency in daily life.

When filling out the Family Chore Chart form, it’s essential to follow certain guidelines to ensure clarity and effectiveness. Here’s a list of dos and don’ts to keep in mind:

Misconceptions about the Family Chore Chart form can lead to misunderstandings about its purpose and effectiveness. Here are five common misconceptions:

Filling out and using the Family Chore Chart can significantly improve financial literacy and responsibility among tweens. Here are ten key takeaways to consider:

Implementing these strategies can foster a sense of financial responsibility and encourage healthy money habits in your tween.