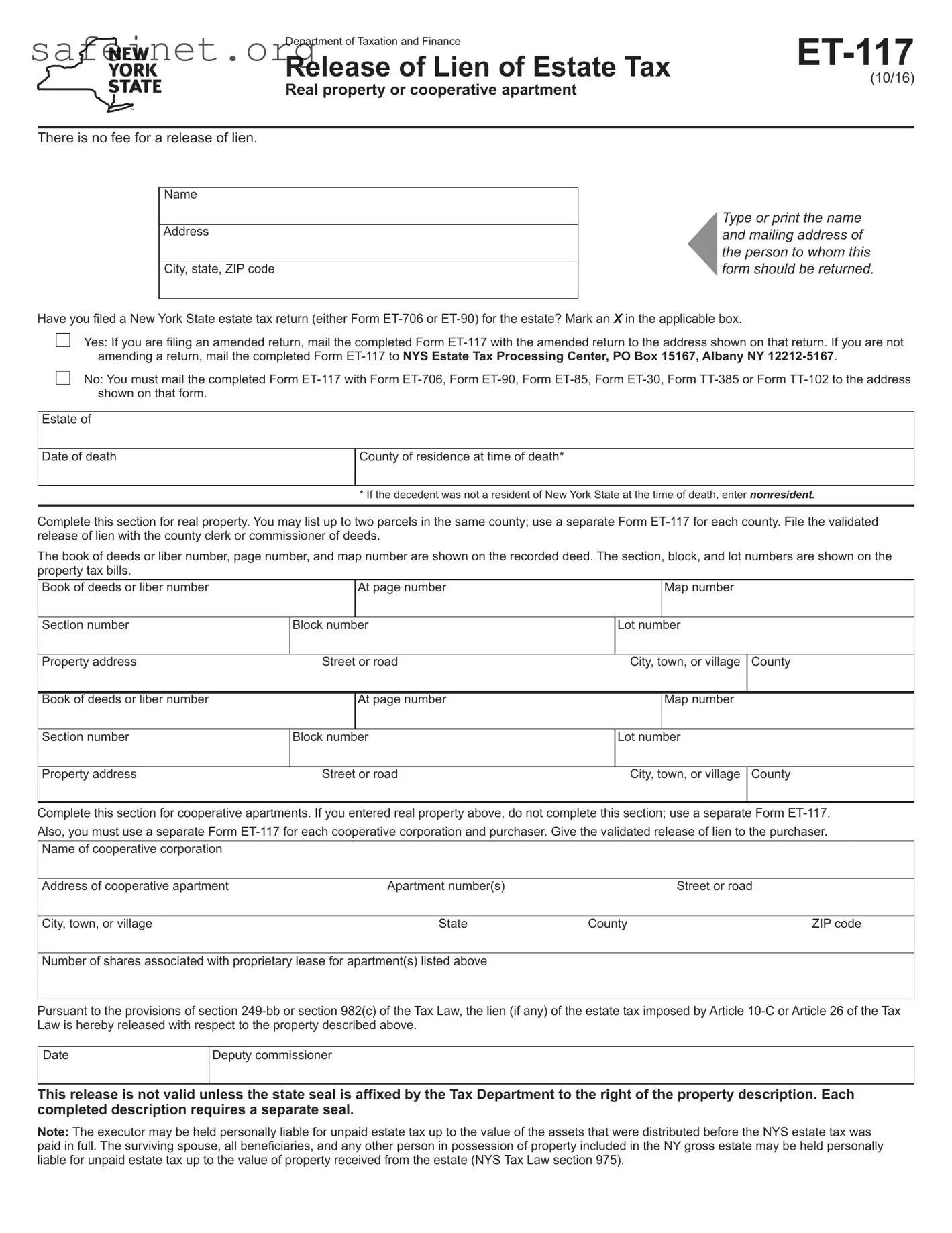

The ET-117 form is an essential document in the estate tax process in New York State, specifically designed to facilitate the release of a lien on real property or cooperative apartments. When a decedent passes away, their estate may incur outstanding estate taxes, which can result in a lien on their property. This lien remains until the estate taxes are settled. The ET-117 form allows executors or administrators of estates to formally request the release of such liens, ensuring that property can be transferred or sold without legal complications. Importantly, there is no fee associated with filing this form. When completing the ET-117, individuals must specify whether they have filed an estate tax return, such as Form ET-706 or ET-90. If they have not filed a return, the ET-117 must be submitted along with these forms. The application requires detailed information, including property descriptions, addresses, and pertinent identification numbers for ease of processing. It is crucial for those involved to understand that filing the ET-117 does not eliminate the responsibility to pay estate taxes fully; rather, it helps clear the way for property transactions while still adhering to state tax laws. Furthermore, liability for unpaid estate taxes may extend to spouses, beneficiaries, and others who possess property from the estate, emphasizing the importance of meticulous adherence to procedural requirements outlined in the ET-117 filing process.

Department of Taxation and Finance |

||

Release of Lien of Estate Tax |

||

(10/16) |

||

|

Real property or cooperative apartment

There is no fee for a release of lien.

Name

Address

City, state, ZIP code

Type or print the name and mailing address of the person to whom this form should be returned.

Have you iled a New York State estate tax return (either Form

Yes: If you are iling an amended return, mail the completed Form

No: You must mail the completed Form

Estate of

Date of death

County of residence at time of death*

* If the decedent was not a resident of New York State at the time of death, enter NONRESIDENT.

Complete this section for real property. You may list up to two parcels in the same county; use a separate Form

The book of deeds or liber number, page number, and map number are shown on the recorded deed. The section, block, and lot numbers are shown on the property tax bills.

Book of deeds or liber number |

|

At page number |

|

Map number |

|

|

|

|

|

|

|

Section number |

Block number |

Lot number |

|

||

|

|

|

|

|

|

Property address |

Street or road |

City, town, or village |

County |

||

|

|

|

|

|

|

Book of deeds or liber number |

|

At page number |

|

Map number |

|

|

|

|

|

|

|

Section number |

Block number |

Lot number |

|

||

|

|

|

|

||

Property address |

Street or road |

City, town, or village |

County |

||

|

|

|

|

|

|

Complete this section for cooperative apartments. If you entered real property above, do not complete this section; use a separate Form

Name of cooperative corporation

Address of cooperative apartment |

Apartment number(s) |

|

Street or road |

|

|

|

|

City, town, or village |

State |

County |

ZIP code |

|

|

|

|

Number of shares associated with proprietary lease for apartment(s) listed above |

|

|

|

Pursuant to the provisions of section

Date

Deputy commissioner

This release is not valid unless the state seal is afixed by the Tax Department to the right of the property description. Each completed description requires a separate seal.

Note: The executor may be held personally liable for unpaid estate tax up to the value of the assets that were distributed before the NYS estate tax was paid in full. The surviving spouse, all beneiciaries, and any other person in possession of property included in the NY gross estate may be held personally

liable for unpaid estate tax up to the value of property received from the estate (NYS Tax Law section 975).

| Fact Name | Detail |

|---|---|

| Form Purpose | The ET-117 form is used to release a lien on estate tax for real property or cooperative apartments in New York State. |

| Filing Fee | There is no fee for submitting the ET-117 form. |

| Return Address | The completed form should be mailed to the appropriate address based on whether you are filing an amended return or not. |

| Estate Tax Return Requirement | You must have filed either Form ET-706 or ET-90 to be eligible to use ET-117. |

| Non-residents | If the decedent was not a resident of New York at the time of death, indicate "NONRESIDENT" on the form. |

| Multiple Properties | You can list up to two parcels in the same county on the ET-117; separate forms must be used for different counties. |

| Cooperative Apartments | A separate ET-117 must be completed for cooperative apartments if real property details have been filled out. |

| Estate Tax Liability | Executors and beneficiaries may be held personally liable for unpaid estate taxes up to the value of distributed assets. |

| Legal References | The form references New York State Tax Law sections 249-bb and 982(c) regarding the estate tax lien release. |

| State Seal Requirement | The release is not valid unless it bears the state seal affixed by the Tax Department. |

Completing the ET-117 form requires attention to detail. This form is necessary for those seeking a release of lien concerning estate tax on real property or cooperative apartments. Following the steps outlined here will ensure that you provide all the required information in a clear and concise manner. After submitting the form, it will facilitate the processing of your request, allowing for the proper management of the estate's tax obligations.

What is the purpose of the ET 117 form?

The ET 117 form, known as the Release of Lien of Estate Tax, is used to release any lien associated with the estate tax on real property or cooperative apartments in New York State. When the estate tax is paid or if certain conditions are met, this form confirms that the tax lien is no longer applicable, allowing the property to be freely transferred or sold.

Is there a fee for filing the ET 117 form?

No, there is no fee required for filing the ET 117 form. This means that you can submit the form without worrying about any associated costs, making it easier for you to manage estate-related paperwork.

Who should file the ET 117 form?

What documentation do I need to submit with the form?

How do I complete the property section on the ET 117 form?

What should I do after filing the ET 117 form?

Incomplete Information: Failing to fill out all required fields on the ET-117 form can lead to delays. Every section must be completed accurately.

Incorrect Attachment: Submitting the ET-117 without the necessary estate tax return (ET-706 or ET-90) can result in the form being returned or denied. Ensure that the correct documents are included.

Improper Mailing Address: Sending the completed form to the wrong address is a common error. Use the NYS Estate Tax Processing Center address specified in the instructions for submission.

Lack of Accurate Property Descriptions: When listing real property or cooperative apartments, it is crucial to provide precise details such as book of deeds, section, block, and lot numbers. Missing information can lead to complications in processing.

Not Following Additional Filing Requirements: Failing to use separate forms for multiple properties or cooperative corporations can create issues. Each parcel or corporation needs a distinct ET-117 for processing.

When dealing with estate taxes in New York, the ET-117 form is just one of several necessary documents. Understanding these accompanying forms can help streamline the process of releasing a lien on estate tax and ensure compliance. Below is a list of related forms that are often used in conjunction with the ET-117 form.

In understanding these forms and their purposes, individuals managing an estate can navigate the complexities of New York’s estate tax system more effectively. It is essential to file the correct forms timely to avoid complications and ensure a smooth transfer of property.

The Form ET-706, New York Estate Tax Return, is one of the primary documents related to estate tax. It is used to calculate the total estate tax liability of a decedent’s estate. Similar to the ET-117, it requires details about the decedent and the estate. Once the tax has been assessed, a lien may be placed against the estate, which the ET-117 can later release. Both forms require specific property details and share a common purpose surrounding the management and distribution of estate assets.

The Form ET-90, Claim for Refund for New York Estate Tax, serves a related function. It permits individuals to request refunds on any estate tax overpayments. Like the ET-117, the ET-90 requires the filer to provide details about the decedent and the estate. In the event that a return shows excess payments, the refund process begins, potentially leading to a release of liens similar to the ET-117. Each form plays a role in the tax lifecycle of an estate.

Form ET-85, New York State Affidavit of No Estate Tax Due, allows executors or administrators to confirm that no estate tax is owed. This document is crucial when handling assets after a death. It serves a similar purpose to the ET-117, which officially releases taxes on properties of the estate. Both forms assure interested parties that tax liabilities have been satisfied or are not present, which facilitates smoother property transactions.

The Form ET-30, New York State Estate Tax Extension Form, grants an extension for filing the estate tax return. This form encourages compliance by providing additional time for preparation. While the ET-117 is used for releasing liens on properties, the ET-30 helps to establish the timeline necessary for filing the documents associated with estate taxes. Both are essential in managing the estate's tax responsibilities.

The Form TT-385, Application for Estate Tax Exemption for Certain Multistate Estates, is also closely related to the ET-117. It is used by estates that qualify for a tax exemption under specific conditions. When completed and accepted, this form can ease the estate tax burden, similar to the lien release offered by the ET-117. Both forms require similar identification of the assets and beneficiaries involved.

Form TT-102, Application for Reinstatement of Estate Tax Exemption, works similarly by allowing estates to apply for reinstatement of tax exemptions that may have expired otherwise. This application can lead to the resolution of tax disputes related to estate tax liabilities. The ET-117 is then used to release any liens if the exemptions are granted. Each document is integral in ensuring that the estate tax obligations are properly managed.

The Form IRS 706, United States Estate (and Generation-Skipping Transfer) Tax Return, is a federal counterpart to the New York tax forms. It is necessary for reporting the value of an estate and calculating any federal estate tax owed. While the ET-117 releases property from a state lien, the IRS 706 ensures all federal obligations are addressed. Together, they streamline the process of settling an estate.

Form IRS 709, United States Gift (and Generation-Skipping Transfer) Tax Return, impacts estate planning by addressing gifts made during the lifetime of the decedent. This form allows for the appropriate accumulation of tax obligations that may influence the estate's value. The proper handling of this form may affect the claims resulting in releases on the estate’s properties, similar to what the ET-117 accomplishes.

The Form New York State Form 1040, Individual Income Tax Return, focuses on the decedent’s income tax obligations rather than estate taxes. While it serves a different purpose, it is equally important for resolving financial matters following a death. Understanding the combined implications of estate and income taxes is crucial for administering an estate effectively, tying it back to the significance of liens like those managed with the ET-117.

When filling out the ET-117 form, there are essential guidelines to follow. Proper adherence to these steps will ensure the process goes smoothly.

Understanding the ET-117 form can be challenging due to various misconceptions. Here’s a list that clarifies common misunderstandings:

Understanding the ET-117 Form is essential for efficiently managing estate tax liens. Here are key considerations: