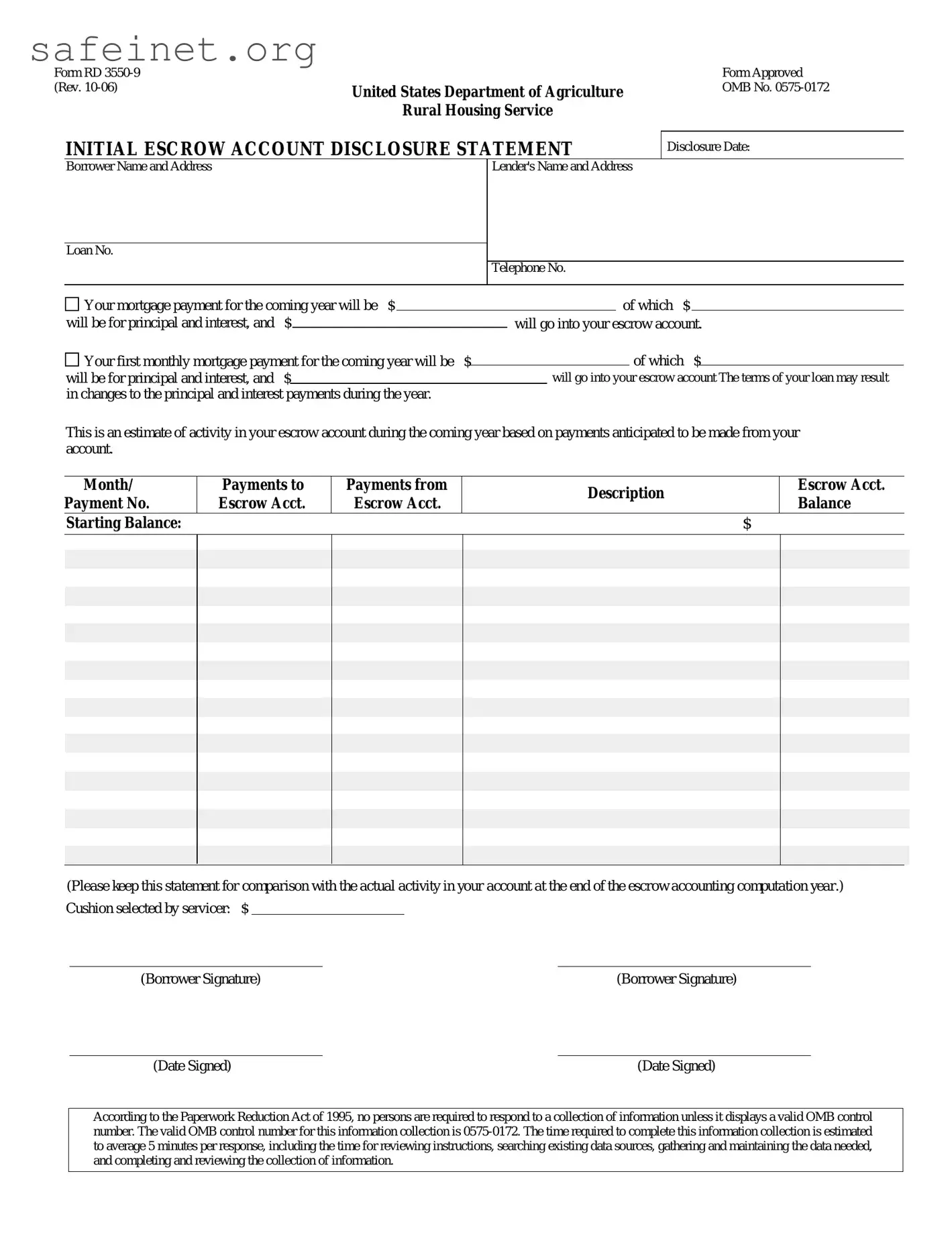

The Escrow Disclosure form is a critical document for homeowners entering into a mortgage agreement, particularly for those using USDA Rural Housing loans. This form provides borrowers with essential information about their escrow account, detailing how much of their monthly mortgage payment will go toward principal and interest, as well as what portion will be allocated to the escrow account. It outlines the total payments expected over the coming year, enabling homeowners to anticipate any changes that may arise in their loan terms. Additionally, it tracks the anticipated inflow and outflow of funds within the escrow account, including starting balances and monthly payment activities. Homeowners are advised to retain this disclosure for future reference, as it serves as a benchmark for comparing actual account activity at the end of the accounting year. The form also includes important contact information for both the borrower and lender, ensuring clear communication lines throughout the loan process. Understanding the details laid out in the Escrow Disclosure form can empower borrowers, allowing them to manage their finances more effectively and ensuring that their obligations are met without surprise costs.

Form RD

(Rev.

Rural Housing Service

INITIAL ESCROW ACCOUNT DISCLOSURE STATEMENT

Form Approved

OMB No.

Disclosure Date:

Borrower Name and Address

Lender's Name and Address

Loan No.

Telephone No.

Your mortgage payment for the coming year will be $ |

|

|

|

of which $ |

|

|

||||

will be for principal and interest, and |

$ |

|

|

will go into your escrow account. |

||||||

|

|

|||||||||

Your first monthly mortgage payment for the coming year will be $ |

|

|

|

of which $ |

|

|||||

|

|

|

|

|

|

|||||

will be for principal and interest, and |

$ |

|

|

|

|

will go into your escrow account The terms of your loan may result |

||||

in changes to the principal and interest payments during the year. |

|

|

|

|

|

|

||||

This is an estimate of activity in your escrow account during the coming year based on payments anticipated to be made from your account.

Month/ |

Payments to |

Payments from |

Description |

|

Escrow Acct. |

|

Payment No. |

Escrow Acct. |

Escrow Acct. |

|

Balance |

||

|

|

|||||

Starting Balance: |

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Please keep this statement for comparison with the actual activity in your account at the end of the escrow accounting computation year.)

Cushion selected by servicer: $

(Borrower Signature)

(Date Signed)

(Borrower Signature)

(Date Signed)

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a valid OMB control number. The valid OMB control number for this information collection is

| Fact Name | Detail |

|---|---|

| Form Identification | Form RD 3550-9 is the Initial Escrow Account Disclosure Statement. |

| Agency | This form is issued by the United States Department of Agriculture (USDA) Rural Housing Service. |

| OMB Approval | The form is approved under OMB Control Number 0575-0172. |

| Disclosure Date | The form includes a section for the disclosure date, impacting how recent the information is. |

| Estimated Payments | It outlines the borrower’s estimated mortgage payment allocation for principal, interest, and escrow. |

| Record Keeping | Borrowers should keep this form for comparison with actual account activity at the end of the escrow year. |

Completing the Escrow Disclosure form is an important step in understanding your mortgage payments and escrow account. It is essential to provide accurate information and review the details carefully to ensure everything is in order.

What is the Escrow Disclosure form?

The Escrow Disclosure form, specifically Form RD 3550-9, is a document provided by the United States Department of Agriculture's Rural Housing Service. It outlines the details of the escrow account associated with a mortgage, including expected payments into and out of the account over the coming year.

Why is the Escrow Disclosure form important?

This form is important because it helps borrowers understand how much of their monthly mortgage payment is allocated for principal and interest versus what is being saved in the escrow account. The escrow account typically covers expenses such as property taxes and homeowners insurance, providing a clear timeline for these anticipated costs.

What information is included in the Escrow Disclosure form?

The form includes details such as the borrower's name and address, lender's name and address, loan number, and a breakdown of monthly payments. It also provides an estimate of the escrow account activity for the year, including starting balance, payments expected to be made into the account, and payments anticipated from the account.

How is the escrow amount determined?

The escrow amount is typically based on the estimated annual costs of property taxes and homeowners insurance. Lenders calculate these estimates and may adjust them throughout the year based on changes in tax rates or insurance premiums.

What happens if there is a surplus or a shortage in the escrow account?

If the account has a surplus, the lender may refund the excess amount to the borrower. Conversely, if there is a shortage, the borrower might need to make a one-time payment or increase their monthly payments to cover the difference, ensuring that sufficient funds are available for upcoming expenses.

How often will I receive an escrow account statement?

Can I contest the escrow payment amounts?

Yes, if you believe the estimated payments for property taxes or insurance appear incorrect, it is important to discuss this with your lender as soon as possible. They can review your estimates and provide further clarification. You may need to provide additional documentation if you wish to contest the amounts.

What is the "cushion" in an escrow account?

The cushion is an additional amount that lenders may require to ensure there are enough funds available in the account at any given time. This is meant to cover fluctuations in costs. It helps prevent a shortage if unexpected increases in property taxes or insurance occur during the year.

How should I keep track of my escrow account?

What should I do if I have more questions about the Escrow Disclosure form?

If you have additional questions, it is advisable to contact your lender directly. They can provide specific information regarding your account and address any concerns you may have regarding the escrow account and its management.

Inaccurate Borrower Information: Filling out the borrower’s name and address incorrectly can lead to delays. It’s essential to double-check for typos or omitted details.

Missing Lender Information: Not including the lender’s name and address may cause confusion later on. Make sure this information is clear and correct.

Incorrect Payment Allocation: Misestimating the amounts for principal, interest, and escrow can complicate future payments. Review calculations carefully to ensure accuracy.

Ignoring the Cushion Amount: The cushion amount selected should reflect the servicer’s guidelines. Failing to select an appropriate cushion may affect future escrow balances.

Not Signing the Form: Forgetting to sign and date the form means it’s not valid. Be sure to include all required signatures before submission.

The Escrow Disclosure form provides vital information regarding the escrow account associated with a mortgage. However, it is often accompanied by several other documents that help clarify the terms and responsibilities related to the housing loan. Below are four essential forms that interact with the Escrow Disclosure form. They serve different purposes but are all integral to the mortgage process.

Understanding these documents is essential for anyone navigating the mortgage process. They offer important information that can help ensure a smoother experience as you manage your mortgage obligations and plan for future payments. Being well-informed can lead to better financial decisions and peace of mind for borrowers.

The Loan Estimate form serves a similar purpose to the Escrow Disclosure form by providing essential information about a borrower’s mortgage. This document lays out important details including loan terms, estimated closing costs, and the expected monthly payment. Like the Escrow Disclosure, the Loan Estimate is designed to help borrowers understand their financial obligations over the life of the loan, allowing for informed decision-making. Both forms aim to enhance transparency between lenders and borrowers, ensuring that all costs are clearly communicated right from the start.

The Closing Disclosure form closely mirrors the Escrow Disclosure form in that it provides final details about the mortgage transaction right before closing. This piece of paperwork outlines the actual costs associated with the loan, including all fees and charges. Both documents share a common goal of clarifying the financial commitments required of borrowers, but the Closing Disclosure is more comprehensive as it reflects the agreed-upon terms following the negotiation process. It serves as a final reminder of what the borrower is committing to and ensures that they are fully informed before signing the final documents.

The Truth in Lending Act (TILA) disclosure is another document that resembles the Escrow Disclosure form. TILA mandates that lenders disclose the terms and conditions of credit in a clear and understandable manner. Like the Escrow Disclosure, TILA disclosures provide crucial information about the cost of borrowing, including interest rates and payment schedules. Both documents are designed to help consumers make educated financial choices and to promote transparency in lending practices. They empower borrowers with the knowledge they need to compare different mortgage options effectively.

The Good Faith Estimate (GFE), while somewhat older, has a similar function to the Escrow Disclosure form in that it also outlines the anticipated costs associated with a mortgage. This document provides borrowers with a breakdown of various fees involved in the loan process. Notably, both the GFE and Escrow Disclosure emphasize clear communication of costs, allowing borrowers to anticipate their financial obligations accurately. Although the GFE has been replaced by the Loan Estimate in many mortgage transactions, the principles governing both documents remain aligned in promoting transparency and consumer protection.

The Annual Escrow Account Disclosure Statement is yet another similar document that complements the Escrow Disclosure form. This statement provides borrowers with a yearly summary of their escrow account, detailing how much money was paid into or withdrawn from the account over the course of a year. In this way, both documents focus on the management of the escrow account, illuminating for borrowers how their funds are being utilized. By offering a clear picture of escrow activity, these forms enhance the overall understanding of what borrowers can expect in terms of their mortgage payments.

The Mortgage Servicing Disclosure Statement provides information about the entity servicing a mortgage loan, functioning somewhat similarly to the Escrow Disclosure form. This disclosure informs borrowers about their rights regarding mortgage servicing and whom to contact for questions. Both documents prioritize transparency and delineate essential information that ensures borrowers know whom they are dealing with and what to expect in servicing their loan. Such disclosures help foster a trusting relationship between borrowers and lenders, setting the stage for responsible lending practices.

The Loan Application form also has parallels to the Escrow Disclosure by capturing essential information about the borrower and the loan they seek. This application typically includes not only personal details but also background information about income and assets. Similarly, the Escrow Disclosure provides financial details pertinent to the loan. Both documents ultimately highlight the borrower’s financial landscape and assist lenders in making decisions about loan approval and terms, thus playing a crucial role in the transactional relationship.

Finally, the Homeowner’s Insurance Disclosure closely relates to the Escrow Disclosure form since both deal with cost considerations that affect mortgage payments. This document provides key information about the homeowner's insurance required by the lender, which is often paid out of the homeowner's escrow account. While the Escrow Disclosure focuses on the specific allocations within the escrow account, the Homeowner’s Insurance Disclosure emphasizes the importance of safeguarding the property through insurance coverage. Together, they contribute to a comprehensive understanding of all financial obligations tied to homeownership.

When filling out the Escrow Disclosure form, there are important do's and don'ts to consider. Here’s a helpful list:

Misconception 1: The Escrow Disclosure form is not important.

This form is crucial as it outlines how much of your monthly mortgage payment goes into an escrow account. It helps you understand your financial obligations and ensures transparency in your loan process.

Misconception 2: The amount in the escrow account does not change.

The amount can change based on property taxes, insurance premiums, and other fees. The disclosure provides an estimate, but actual payments may vary.

Misconception 3: The escrow account only covers property taxes.

While property taxes are a primary expense, escrow accounts may also cover homeowner’s insurance and sometimes mortgage insurance premiums.

Misconception 4: Borrowers cannot access their escrow funds.

Typically, funds in the escrow account are managed by the lender and are intended for specific payments like taxes and insurance. Borrowers cannot directly withdraw these funds.

Misconception 5: The lender sets the escrow payment arbitrarily.

Escrow payments are based on estimates of future obligations. Lenders calculate these amounts based on the expected costs of taxes and insurance.

Misconception 6: You won’t receive any updates on your escrow account.

Borrowers usually receive annual statements or updates detailing the activity in their escrow account, including balances and payments made.

Misconception 7: The escrow cushion is optional and can be ignored.

The escrow cushion is a reserve intended to cover unexpected increases in payments. While it might seem unnecessary, it helps prevent shortfalls in the account.

1. Understand the Purpose: The Escrow Disclosure form provides a clear overview of your mortgage payments and anticipated escrow activity for the year.

2. Review Payment Breakdown: It details how much of your monthly payment will go toward principal and interest versus the escrow account.

3. Track Escrow Activity: The form includes a projection of payments to and from your escrow account, helping you anticipate changes and understand your financial commitments.

4. Keep for Reference: Hold onto this statement. It is essential for comparing actual activity in your escrow account at the end of the year.

5. Note the Cushion: The disclosure specifies a cushion selected by the servicer. This cushion can affect how much you may need to maintain in your escrow account.

6. Signature Requirement: Ensure both borrowers sign and date the form to validate the disclosure and acknowledge understanding.

7. OMB Control Number: The form holds an OMB control number (0575-0172), which is necessary for compliance with the Paperwork Reduction Act of 1995. This number confirms that the form is approved and that no one is required to respond unless it is displayed.