The E-585 form plays a crucial role in the financial operations of nonprofit and governmental entities in North Carolina. This form allows these organizations to claim refunds on state, county, and transit sales and use taxes they have paid on qualifying purchases. To initiate a refund process, applicants must fill out precise details, including their legal name, account ID, and the applicable tax periods. This form distinguishes between the taxes paid directly to retailers and those paid indirectly, ensuring a comprehensive approach to the refund request. Nonprofits must be aware of the specific guidelines set forth in North Carolina General Statutes, particularly regarding their eligibility and refund caps. Meanwhile, governmental entities have their own deadlines tied to the fiscal year, requiring careful timing in their submissions. Additionally, it is important to note that certain purchases, such as electricity and alcoholic beverages, do not qualify for refunds. With the correct documentation and adherence to the guidelines, entities can effectively navigate the refund process and reclaim funds that have been unjustly paid.

Do Not Include This Page

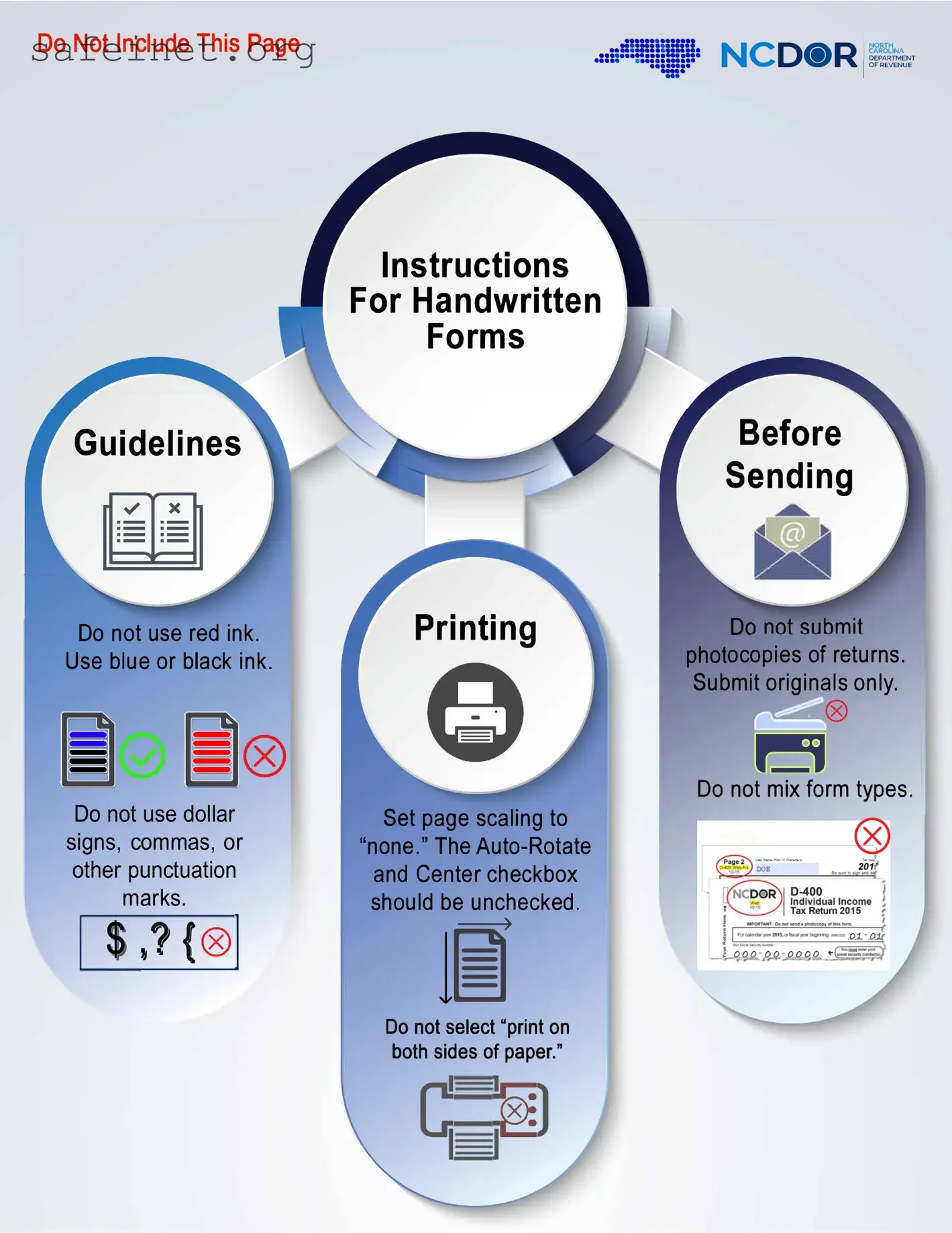

Guidelines

::::==·

. •• ··=!!!:::!:•

Instructions

For Handwritten

Forms

NCD(i)• R

Before Sending

I NORTH CAROLINA DEPARTMENT OF REVENUE

Do not use red ink. Use blue or black ink.

®

®

Do not use dollar signs, commas, or other punctuation

marks.

, 1 t®I

, 1 t®I

Printing

Set page scaling to

"none." The

1�

ocopies of returns. Submit originals only.

,,___(8)

Do not mix form types.

Do not select "print on bothc;sides of paper."

;�1

Nonprofit and Governmental Entity Claim for Refund |

|

State, County, and Transit Sales and Use Taxes |

|

Complete all of the information in this section. |

|

|

|

|

Legal Name (First 32 Characters) (USE CAPITAL LETTERS FOR YOUR NAME AND ADDRESS) |

Account ID |

|

Mailing Address

Federal Employer ID Number

City |

State |

Zip Code |

County |

Period Beginning

Name of Person We Should Contact if We Have Questions About This Claim |

Contact Telephone |

Period Ending

Fill in the circle that describes your organization.

Nonprofit or other qualified entity as defined in N.C. Gen. Stat. §

National Taxonomy of Exempt Entities Number

(Nonprofit Entity Only)

1.Name of Taxing County

(If more than one county, see instructions on page 2 and attach Form

2. Total Qualifying Purchases of Tangible Personal |

|

|

State |

||

Property and Services for Use on Which North Carolina |

||

State or Food, County & Transit Sales or Use Tax Has |

|

|

Been Paid Directly to Retailers (Do not include tax paid, |

|

|

purchases for resale, or items described in box below.) |

|

Food, County & Transit

Tax paid on any of the following items are nonrefundable:

Electricity, piped natural gas, telecommunications and ancillary services, video programming, prepaid meal plans; the purchase, lease, rental, or subscription of motor vehicles; local occupancy or local prepared food and beverage taxes; scrap tire disposal or white goods disposal taxes; reimbursements for travel expenses; alcoholic beverages; digital property

3.Amount of Sales and Use Tax Paid Directly to Retailers on Qualifying Purchases

4.Amount of Sales and Use Tax Paid Indirectly on Qualifying Purchases

5.Amount of Use Tax Paid Directly to the Department on Qualifying Purchases (Do not include tax collected

and remitted on sales made by the entity.)

6. |

Total Tax (Add Lines 3, 4, and 5. Food, County & Transit |

|

|

tax must be identified by rate on Line 8.) (For nonprofit |

|

|

entity only; annual cap applies, see General Instructions.) |

|

7. |

Total Refund Requested |

$ |

|

(Add State and Food, County & Transit tax on Line 6.) |

8.Allocation of Food, County & Transit Tax on Line 6 (Enter the Food, County & Transit tax paid at each applicable rate. If you paid more than one county’s tax, see the instructions on page 2 and attach Form

Food 2.00% Tax |

County 2.00% Tax |

County 2.25% Tax |

Transit 0.50% Tax

Durham, Mecklenburg, Orange, Wake

Signature: |

|

Date: |

I certify that, to the best of my knowledge, this claim is accurate and complete.

Title: |

|

Telephone: |

Food Tax

,

,

,

,

Refund Approved:

For Departmental Use Only

. |

, |

County 2.00% Tax |

, |

County 2.25% Tax |

||

, |

. |

, |

. |

|||

|

|

|

|

, |

State Tax |

. |

As Filed |

|

As Corrected |

, |

|||

|

|

|

|

|||

Transit Tax

,

,

,

,

.

.

Total Tax

,

,

,

,

.

.

By: |

|

Date: |

|

|

|

|

|

||

|

MAIL TO: NC Department of Revenue, P.O. Box 25000, Raleigh, NC |

|

||

Page 2, |

General Instructions |

Use blue or black ink to complete this form. An Account ID is required to process the claim.

This form is to be filed by the following entities as specified:

-Nonprofit or other qualified entities as permitted in N.C. Gen. Stat. §

For a nonprofit entity, the total State sales and use tax refund amount for both six month periods may not exceed $31,700,000 for the State’s fiscal year and the total Food, County & Transit tax refund amount for both six month periods may not exceed $13,300,000 for the State’s fiscal year.

A hospital not listed in N.C. Gen. Stat. §

-Governmental entities as permitted in N.C. Gen. Stat. §

Records must be maintained, and distinguish the following information on a county by county basis: qualifying purchases of tangible personal property and services; State, county & transit tax paid directly to retailers on qualifying purchases for use as shown on sales receipts and invoices; State, county & transit tax paid indirectly on qualifying purchases of building materials, supplies, fixtures, and equipment as shown on certified statements; and State, county & transit tax paid directly to the Department of Revenue.

Records must be maintained for qualifying direct purchases and qualifying indirect purchases as follows:

-Qualifying direct purchases - Adequate documentation for tax paid directly to the vendor is an invoice or copy of an invoice that identifies the item purchased, the date of the purchase, the cost of the item, and the amount of sales or use tax paid. Reimbursements for travel expenses to an authorized person of the entity are not considered to be a direct purchase; therefore, the sales or use tax paid on such are not refundable.

-Qualifying indirect purchases - Adequate documentation for sales or use tax paid on qualifying indirect purchases is a certified statement from the real property contractor or other person that purchased the items. The statement must indicate the date the property was purchased; the type of property purchased; the name of the person from whom the purchase was made and the invoice number of the purchase; the purchase price of property purchased and the amount of sales and use tax paid thereon; the project for which the property was used; if the property was purchased in this State, a copy of the sales receipt and the statement must include the county in which it was delivered; and if the property was not purchased in this State, the county in North Carolina in which the property was used must be included. Only sales and use taxes paid on building materials, supplies, fixtures, and equipment that become part of or annexed to a building or structure that is owned or leased by or is being erected, altered, or repaired for use by the nonprofit entity for carrying on its nonprofit activities or by the governmental entity are sales and use tax paid on qualifying indirect purchases eligible for refund.

For a claim for refund filed within the statute of limitations, the Department must take one of the following actions within six months after the date the claim for refund is filed: (1) send the taxpayer a refund of the amount shown due on the claim for refund; (2) adjust the amount of the refund shown due and send the taxpayer a refund of the adjusted amount; (3) deny the refund and send the taxpayer a notice of proposed denial; or (4) request additional information from the taxpayer. If the Department does not take one of the actions within six months, the inaction is considered a proposed denial of the requested refund. A taxpayer who objects to a proposed denial of a refund may request a Departmental review of the proposed action by filing a Form

For a full explanation of the Departmental review process, refer to the North Carolina Taxpayers’ Bill of Rights found at www.ncdor.gov or the provisions of N.C. Gen. Stat. §

If you have questions about how to complete this form, more detailed instructions can be found on our website at www.ncdor.gov or call the Department at

Line 1 - If all taxes were paid in only one county, enter the name of that county. If you made purchases and paid county & transit tax in more than one county, do not list a county on Line 1.

For Lines 2 through 6, local school administrative units and associated joint agencies should only complete the Food, County & Transit column.

Line 2 - Enter in the State column the total amount of qualifying purchases of tangible personal property and services for use on which State sales or use tax was paid to retailers. The taxable purchase price of a modular home, manufactured home, boat, or aircraft is included in the State column only. Enter in the Food, County & Transit column the total amount of qualifying purchases of tangible personal property and services for use on which food, county & transit sales or use tax was paid to retailers.

For Lines 3 through 6, State tax must be entered in the State column and food, county & transit tax must be entered in the Food, County & Transit column.

Line 3 - Enter the amount of sales and use tax paid directly to retailers on qualifying purchases for use, as shown on sales receipts or invoices. Do not include tax paid on nonrefundable purchases as described in the box on the front of claim form.

Line 4 - Enter the total amount of sales and use tax paid indirectly on qualifying purchases of building materials, supplies, fixtures, and equipment as shown on certified statements from real property contractors or other persons.

Line 5 - Enter the total amount of use tax paid to the Department by the entity on its sales and use tax returns for qualifying purchases. Do not include tax collected and paid on taxable sales made by your entity.

Line 6 - Add the amounts of tax by column on Lines 3, 4, and 5 and enter the sum.

Line 7 - Add the State and Food, County & Transit taxes on Line 6 and enter the sum. This is the total amount of refund requested for the period.

Line 8 - Allocate the amount of county and transit taxes included on Line 6 in the Food, County & Transit Tax column to the applicable rate. If county or transit tax was paid for more than one county, complete Form

For nonprofit entity only: If the total entries of food, county, & transit tax on Form

| Fact Name | Detail |

|---|---|

| Form Type | E-585 is specifically for nonprofit and governmental entities to claim refunds for State, County, and Transit Sales and Use Taxes. |

| Submission Deadline (Nonprofits) | Nonprofits must submit their claims by October 15 for the first half and April 15 for the second half of the year. |

| Submission Deadline (Governmental Entities) | Claims from governmental entities are due within six months of the close of their fiscal year. |

| Tax Exemptions | Certain purchases are nonrefundable, including items like electricity and alcoholic beverages, which are clearly listed in the guidelines. |

| Total Refund Cap (Nonprofits) | The total State sales and use tax refund amount cannot exceed $31,700,000 for the State’s fiscal year, along with limitations on Food, County, and Transit tax refunds. |

| Required Documentation | Claims require adequate documentation showing taxes paid. This includes receipts and invoices clearly detailing items purchased and taxes associated. |

| Governing Laws | The form adheres to North Carolina General Statutes §§ 105-164.14(b) and 105-164.14(c) concerning exemptions and refund qualifications. |

| Contact Information | For assistance, entities can call the NC Department of Revenue at 1-877-252-3052 or visit their website for more instructions. |

Completing the E 585 form requires careful attention to detail. This guide will help you navigate through each section effectively, ensuring that your information is accurate and your claim can be processed smoothly.

After submitting your form, the Department will review your claim. They may request additional information if necessary. Within six months, you should receive a response regarding the outcome of your request.

What is the E 585 form used for?

The E 585 form is a claim for refund of State, County, and Transit Sales and Use Taxes paid by nonprofit organizations and governmental entities in North Carolina. This form allows eligible entities to reclaim taxes they have overpaid or unnecessarily paid on qualifying purchases made during specific periods.

Who is eligible to file the E 585 form?

This form can be filed by nonprofit organizations that qualify under N.C. Gen. Stat. § 105-164.14(b) and governmental entities defined in N.C. Gen. Stat. § 105-164.14(c). Nonprofits can request refunds on purchases made in either the first or second half of the year, while governmental entities must file claims based on the fiscal year.

What is the deadline for submitting the E 585 form?

For nonprofits, the deadline to file for refunds on the first half of the year is October 15 of the same year. Claims for the second half must be filed by April 15 of the following year. Governmental entities should submit their claims within six months of their fiscal year-end.

What types of purchases qualify for a refund using the E 585 form?

The form covers qualifying purchases of tangible personal property and services on which North Carolina sales or use taxes were paid. However, refunds cannot be claimed for certain items such as electricity, alcoholic beverages, and items for resale. It is crucial to follow specific guidelines provided in the instructions.

How should the E 585 form be completed?

What happens if my E 585 form is denied?

If the North Carolina Department of Revenue denies the refund, they will send a notice explaining the reasons for the denial. Taxpayers may then request a departmental review of the proposed denial by filing a Form NC-242 within a specified period. Understanding the rejection reasons can help in preparing a stronger claim for any future submissions.

Are there limits on the refund amounts?

Yes, there are caps on the refund amounts for nonprofits. For example, the total sales tax refund cannot exceed $31,700,000 for the State’s fiscal year, while the total Food, County, and Transit tax refund is limited to $13,300,000 for the same period. These limits are in place to manage tax resources and budgetary constraints.

Where should I send the completed E 585 form?

The completed E 585 form should be mailed to the NC Department of Revenue at P.O. Box 25000, Raleigh, NC 27640-0001. It is essential to ensure that forms are mailed in time to meet the aforementioned deadlines to avoid forfeiting potential refunds.

Using Incorrect Ink Color: Many individuals fail to follow the instruction to use only blue or black ink. Utilizing red ink can lead to rejection or delays in processing.

Including Punctuation: Some people mistakenly add dollar signs, commas, or other punctuation marks in the dollar amount fields, which can cause confusion during review.

Improper Page Scaling: When printing the form, not setting the page scaling to "none" can result in a form that does not fit properly, making it unreadable or misaligned.

Originals vs. Copies: Individuals sometimes send copies instead of the original forms, which is explicitly discouraged in the instructions.

Mixing Form Types: There is a common error of mixing different form types. It’s essential to ensure that only the E-585 form is used for this claim.

Omitting Required Information: Failing to fill in all required fields, such as the legal name or Federal Employer ID Number, leads to incomplete submissions and potential delays.

Incorrect Tax Calculation: A frequent mistake involves miscalculating the total tax amounts on lines 3, 4, and 5, which could result in incorrect refund requests.

Not Following Signature Requirements: Some submitters forget to sign the form or provide an inaccurate date, both of which are necessary for processing the claim.

When filing the E 585 Form, various other documents may be required or helpful for smooth processing. Below is a list of these forms and documents, along with brief descriptions of each.

Having these documents organized and ready can significantly enhance the efficiency of the refund claim process. Always ensure that you submit the correct and complete information to avoid delays or complications.

The IRS Form 990 serves a similar purpose as the E-585 form in that it is designed for tax-exempt organizations to report on their financial activities. Nonprofits are required to file Form 990 annually, detailing their income, expenses, and activities. Like the E-585, the form provides a mechanism for nonprofits to maintain transparency and compliance with federal regulations. Both forms require accurate and complete information to reflect the organization's financial status, and both are essential for governmental oversight and public accountability.

Form W-9, which is used to provide taxpayer identification information to the IRS, is another document that shares similarities with the E-585 form. Organizations fill out the W-9 to certify their name, address, and Taxpayer Identification Number (TIN). Like the E-585, the W-9 necessitates precise information to ensure that tax-related responsibilities are fulfilled correctly. Both forms help establish clear records and facilitate transactions between organizations and the taxing authorities.

The North Carolina Sales and Use Tax Return (form E-500) is analogous to the E-585 in that it serves to report sales taxes collected and owed. While the E-585 is specifically for claiming refunds, the E-500 is used to report taxable sales and to remit tax payments. Both forms emphasize the importance of correct reporting and documentation of sales and use taxes, as inaccuracies can lead to penalties or the denial of claims. Both are essential for compliance with state tax laws.

Form 990-PF, which specifically concerns private foundations, has similarities to the E-585 due to its focus on tax-exempt entities. This form requires foundations to detail their finances, including income, expenses, and distributions. Like the E-585, it aims to ensure accountability and proper governance within tax-exempt organizations. Transparency in financial reporting is critical in both scenarios, as it helps maintain trust with the public and regulators.

The Nonprofit Registration Application is another document that parallels the E-585 form. This application typically must be submitted to state authorities when an organization seeks to operate as a nonprofit entity. Both documents underscore the organization's commitment to adhere to state regulations and tax laws. They serve as crucial tools for classification and oversight, ensuring that the proper validations and registrations are in place for nonprofit operations.

When filling out the E-585 form, it's crucial to ensure accuracy and compliance with guidelines laid out by the North Carolina Department of Revenue. Here’s a helpful list of things you should and shouldn’t do:

By adhering to these guidelines, you can help ensure that your claim is processed smoothly and efficiently.

1. The E 585 form is only for nonprofits. This form is applicable to both nonprofit organizations and governmental entities. Both types can request refunds for sales and use taxes paid.

2. All purchases qualify for a refund. Not every purchase is eligible. Purchases related to specific items like electricity, alcoholic beverages, and vehicles are nonrefundable.

3. Refunds can be claimed at any time. There are specific deadlines. Nonprofits must file claims semiannually, while governmental entities must file within six months after the fiscal year ends.

4. I can use any color of ink. This is incorrect. The form must be completed using blue or black ink only. Using red ink can lead to rejection of the form.

5. It's okay to mix form types. This is a misconception. Mixing different form types on the E 585 will result in processing delays, as each form type must be distinct.

6. You must use dollar signs and commas. This is false. The form specifies that no dollar signs, commas, or punctuation marks should be used, which simplifies the data entry process.

7. I don't need to keep records. Proper record-keeping is essential. Entities must maintain accurate documentation of qualifying purchases and taxes paid to support their claims.

8. General tax information is sufficient. The E 585 form requires detailed information. Entities must provide specific amounts related to State, county, and transit sales and use taxes to ensure accuracy and compliance.