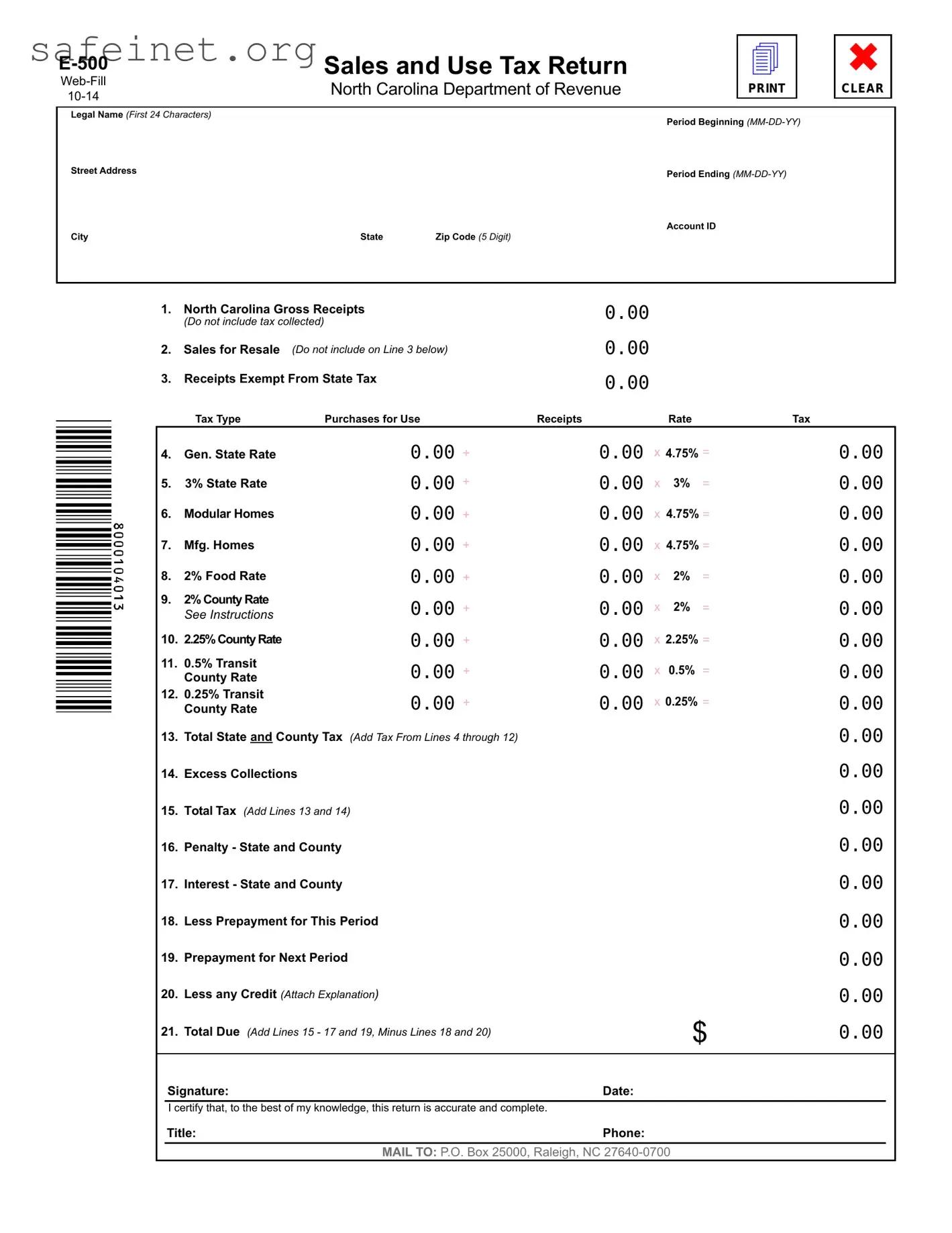

The E 500 form plays a crucial role for businesses in North Carolina in relation to sales and use taxes. Designed specifically for the state's Department of Revenue, this form requires businesses to report their gross receipts, sales for resale, and any exemptions from state tax. By accurately filling out this form, businesses can ensure that they comply with state tax laws and maintain good standing with the government. The E 500 form includes several key sections, such as an account ID, legal name, and address, along with a detailed breakdown of taxable purchases based on different rates. Completing the E 500 involves calculating total taxes accrued for the reporting period, accounting for any excess collections or credits, and determining the total amount due. Proper submission of this form is essential, as inaccuracies can lead to penalties or interest charges. Thus, understanding the importance of the E 500 form and its related components is vital for any business operating in North Carolina.

Sales and Use Tax Return |

|

North Carolina Department of Revenue |

|

4

✖

CLEAR

Legal Name (First 24 Characters) |

|

Period Beginning |

|

|

|

Street Address |

|

Period Ending |

|

|

Account ID |

City |

State |

Zip Code (5 Digit) |

|

|

|

1.North Carolina Gross Receipts

(Do not include tax collected)

2.Sales for Resale (Do not include on Line 3 below)

3.Receipts Exempt From State Tax

0.00

0.00

0.00

Tax Type |

Purchases for Use |

Receipts |

Rate |

Tax |

4. |

Gen. State Rate |

0.00 + |

5. |

3% State Rate |

0.00 + |

6. |

Modular Homes |

0.00 + |

7. |

Mfg. Homes |

0.00 + |

8. |

2% Food Rate |

0.00 + |

9. |

2% County Rate |

0.00 + |

|

See Instructions |

|

10. |

2.25% County Rate |

0.00 + |

11. |

0.5% Transit |

0.00 + |

|

County Rate |

|

12. |

0.25% Transit |

0.00 + |

|

County Rate |

13.Total State and County Tax (Add Tax From Lines 4 through 12)

14.Excess Collections

15.Total Tax (Add Lines 13 and 14)

16.Penalty - State and County

17.Interest - State and County

18.Less Prepayment for This Period

19.Prepayment for Next Period

20.Less any Credit (Attach Explanation)

21.Total Due (Add Lines 15 - 17 and 19, Minus Lines 18 and 20)

0.00 |

x 4.75% = |

0.00 |

||

0.00 |

x |

3% |

= |

0.00 |

0.00 |

x 4.75% = |

0.00 |

||

0.00 |

x 4.75% = |

0.00 |

||

0.00 |

x |

2% |

= |

0.00 |

0.00 |

x |

2% |

= |

0.00 |

0.00 |

x 2.25% = |

0.00 |

||

0.00 |

x |

0.5% |

= |

0.00 |

0.00 |

x 0.25% = |

0.00 |

||

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

|

|

0.00 |

|

|

$ |

0.00 |

|

Signature: |

Date: |

I certify that, to the best of my knowledge, this return is accurate and complete.

Title: |

Phone: |

|

MAIL TO: P.O. Box 25000, Raleigh, NC |

| Fact Name | Description |

|---|---|

| Form Title | The form is known as the E-500 Sales and Use Tax Return. |

| Governing Authority | This form is governed by the North Carolina Department of Revenue. |

| Purpose | It is used to report and pay sales and use tax for businesses operating in North Carolina. |

| Frequency | The E-500 form is typically filed on a monthly basis, but it can be filed quarterly depending on the business's tax obligations. |

| Due Date | Returns are generally due on the 20th day of the month following the end of the reporting period. |

| Account ID | Businesses must include their unique Account ID assigned by the North Carolina Department of Revenue on the form. |

| Exempt Sales | Sales for resale and exempt receipts should not be included in gross receipts on the form. |

| Tax Calculation | The total state and county tax is calculated by adding up various tax lines from the form, including state rates and county rates. |

| Signature Requirement | A signature and date are required to certify the accuracy of the return before submission. |

| Filing Address | Completed forms should be mailed to P.O. Box 25000, Raleigh, NC 27640-0700. |

After completing the E 500 form, ensure that all information is accurate before submitting. This process involves several key steps to properly fill out the form.

What is the purpose of the E 500 form?

The E 500 form is utilized by businesses in North Carolina to report their sales and use tax. This step is essential for compliance with state tax laws. The form collects information about gross receipts from sales, purchases made for use, and various tax categories. After filling it out, businesses submit the form to the North Carolina Department of Revenue to ensure they are paying the correct amount of taxes owed.

Who needs to file the E 500 form?

Any business registered in North Carolina that makes taxable sales, leases, or rentals of tangible personal property or services must file the E 500 form. This includes retailers, wholesalers, and manufacturers. If your business collects sales tax from customers or incurs use tax on purchases, you are required to file this form regularly, based on your sales volume and tax obligations.

How do I properly complete the E 500 form?

Completing the E 500 form involves providing specific details such as your legal name, address, and account ID. You will need to input gross receipts, sales for resale, and any exempt receipts. Be sure to include the appropriate figures for various rates across state and county taxes. After calculating total tax and any applicable penalties or interests, you will arrive at the total amount due. Thoroughly review the instructions provided with the form to avoid mistakes.

What happens if I don't file the E 500 form on time?

Failure to file the E 500 form by the due date can result in penalties and interest. The North Carolina Department of Revenue may impose a fine based on the amount due and the duration of the delay. Additionally, failing to file can jeopardize your business's standing with the state, potentially leading to further enforcement actions. Therefore, timely submission of this form is critical to maintaining compliance and avoiding unnecessary additional costs.

Failing to accurately report the North Carolina Gross Receipts. This amount should reflect total income received without the inclusion of any tax collected. Missing or incorrect figures can lead to discrepancies and potential penalties.

Omitting Sales for Resale on Line 3. It's essential to only list sales that are intended for resale in this section. Including them here incorrectly impacts the tax calculation and might result in audits.

Not providing sufficient details regarding Receipts Exempt From State Tax. This section needs clear documentation to justify any exempt sales and ensure compliance with state regulations. Lack of information can cause complications when the form is reviewed.

Incorrectly calculating the Total Due. This figure is crucial as it determines the amount payable to the state. Mistakes in adding lines 15-17 and subtracting lines 18 and 20 can lead to overpayments or penalties for underpayment.

The E-500 form is a key document used for reporting sales and use tax in North Carolina. However, it is often accompanied by several other forms and documents that help ensure compliance with state tax regulations. Below is a list of common documents that may be needed alongside the E-500 form.

Understanding and preparing these accompanying forms can significantly streamline the tax filing process for businesses in North Carolina. Organizing these documents in advance contributes to accuracy and compliance, reducing the likelihood of errors or audits.

The E-500 form, which serves as the Sales and Use Tax Return for North Carolina's Department of Revenue, bears similarities to the IRS Form 1040, which is used for individual income tax returns. Both forms require accurate reporting of financial information, including income and taxable expenses. However, while the E-500 focuses on sales and use tax specific to North Carolina, Form 1040 centers around federal income tax. Both forms also necessitate the taxpayer's signature, certifying the accuracy of the data provided.

Another document comparable to the E-500 is the IRS Form 941, which employers use to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Like the E-500, Form 941 requires periodic submission based on a set timeframe, generally quarterly. Each form collects specific financial data to determine tax obligations: the E-500 deals with sales and use tax liabilities, while Form 941 handles federal payroll taxes. Both documents must be filed to ensure compliance with relevant tax regulations.

The E-500 also shares characteristics with a state-specific sales tax exemption certificate, such as North Carolina's ST-3. This document allows buyers to purchase items without paying sales tax under certain circumstances. Exemption certificates, like the E-500, require particular details about the buyer and the nature of the exempt purchase. Both forms emphasize the necessity of accurate record-keeping to substantiate claims made when dealing with state tax authorities.

In addition, the E-500 is similar to the Form 1065, which partnerships use to report income, deductions, gains, and losses. Both documents detail financial activity over a specified period. The Form 1065, however, pertains to business entities, while the E-500 relates specifically to tax owed on sales transactions, highlighting unique aspects of revenue generation and tax liability within their respective frameworks.

The E-500 also resembles the IRS Form 1120, which is utilized by corporations to report income tax. Both forms are essential for determining tax obligations and include comprehensive information about revenue receipt. Nevertheless, the primary distinction lies in the type of entity each form represents—the E-500 targets sales in North Carolina, while Form 1120 focuses on corporate income generation at the federal level.

Another relevant document is the North Carolina Form D-400, which individuals use for income tax purposes. Like the E-500, it requires taxpayers to report certain financial figures based on a defined period. The E-500, on the other hand, specifically addresses sales and use tax collection, appealing to businesses rather than individual income earners. Both serve as crucial tools in ensuring that taxpayers fulfill their obligations to the state.

The E-500 form can also be compared to the IRS Form 720, which is used to report and pay federal excise taxes. While both documents require detailed financial reporting, the E-500 focuses on sales and use tax at the state level, whereas Form 720 deals with various federal excise taxes related to specific goods and activities. Both document types require periodic reporting and payment of taxes, but they cover different areas of financial obligations.

Furthermore, the E-500 is akin to the IRS Form 1099, which businesses use to report various types of payments made to contractors. Just as the E-500 collects information about sales transactions, Form 1099 captures payment information for services rendered. While both forms require accurate reporting, they pertain to distinct financial activities—sales versus payments for services—within the tax framework.

Lastly, the E-500 shares similarities with the North Carolina Corporate Income and Franchise Tax Return (Form CD-405), used by corporations to report their tax obligations. Both forms require precise financial information about revenue and tax rates applicable over a specified timeframe. However, the E-500 specifically targets sales and use tax, while Form CD-405 encompasses corporate income tax, depicting the broader landscape of tax liability for different types of entities in North Carolina.

When filling out the E-500 form for sales and use tax in North Carolina, it's important to follow specific guidelines to ensure accuracy and compliance. Here are ten things to keep in mind:

By following these guidelines, you can help ensure a smooth filing process for your E-500 return.

Misconceptions about the E 500 form can create confusion for businesses and taxpayers in North Carolina. Below is a list of ten common misconceptions, along with clarifications for each.

Understanding these misconceptions can help taxpayers correctly navigate the filing process and avoid potential issues. Accurate filing is essential for compliance with state tax laws.

When filling out and using the E 500 form for Sales and Use Tax in North Carolina, these key takeaways are essential to ensure accuracy and compliance:

Following these steps can help ensure the form is completed correctly and submitted in a timely manner.