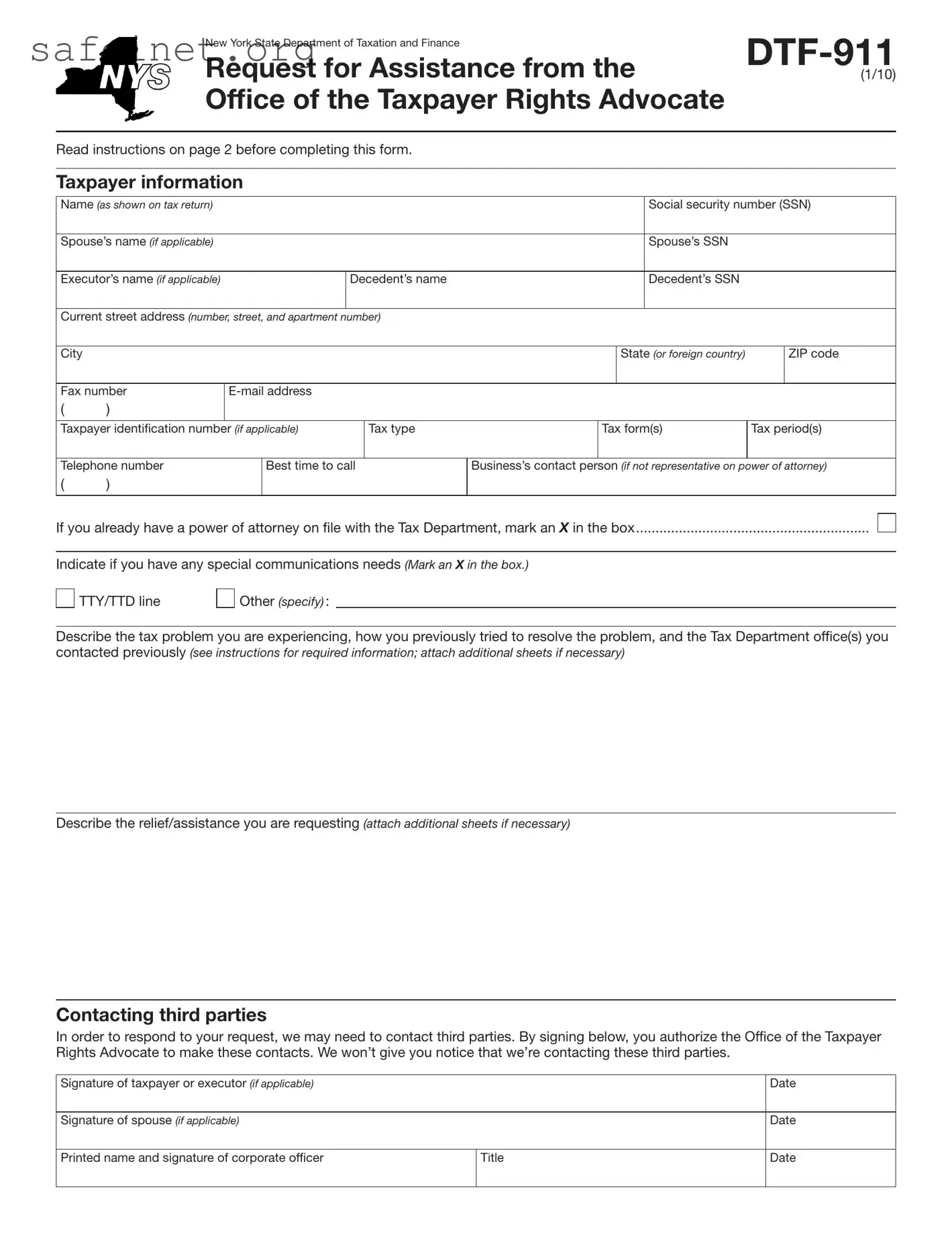

The DTF-911 form, officially known as the Request for Assistance from the Office of the Taxpayer Rights Advocate, serves as a vital resource for New York State taxpayers encountering significant challenges with tax matters. This form is designed for individuals who find themselves facing immediate adverse actions, such as asset seizures, or those who believe they are experiencing undue economic harm due to tax issues. Furthermore, it may also protect taxpayers who have endured substantial delays or unfair treatment by the Tax Department, ensuring that their rights are upheld. The form requires essential personal information such as taxpayer identification numbers, specific tax types, and a detailed account of the issue at hand, including the steps already taken to seek resolution. In addition, it empowers the Office of the Taxpayer Rights Advocate to communicate with third parties as necessary, aiming to expedite assistance. Instructions on how to properly fill out the form emphasize the importance of providing a clear and comprehensive description of the tax problem, as well as necessary documentation, ensuring that every aspect is addressed efficiently. This form remains a crucial tool for those in need of guidance and intervention in navigating the complexities of the tax system.

|

New York State Department of Taxation and Finance |

|

|

|

|

||||||

|

|

|

|

|

|

|

|||||

|

Request for Assistance from the |

(1/10) |

|||||||||

|

Office of the Taxpayer Rights Advocate |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

Read instructions on page 2 before completing this form. |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer information |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Name (as shown on tax return) |

|

|

|

|

|

|

|

Social security number (SSN) |

|||

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s name (if applicable) |

|

|

|

|

|

|

|

Spouse’s SSN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Executor’s name (if applicable) |

|

|

Decedent’s name |

|

|

|

Decedent’s SSN |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Current street address (number, street, and apartment number) |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

|

State (or foreign country) |

|

ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

Fax number |

|

|

|

|

|

|

|

|

|||

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer identiication number (if applicable) |

|

Tax type |

|

Tax form(s) |

Tax period(s) |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

Telephone number |

|

Best time to call |

Business’s contact person (if not representative on power of attorney) |

||||||||

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If you already have a power of attorney on ile with the Tax Department, mark an X in the box............................................................

Indicate if you have any special communications needs (Mark an X in the box.)

TTY/TTD line

Other (specify) :

Describe the tax problem you are experiencing, how you previously tried to resolve the problem, and the Tax Department ofice(s) you contacted previously (see instructions for required information; attach additional sheets if necessary)

Describe the relief/assistance you are requesting (attach additional sheets if necessary)

Contacting third parties

In order to respond to your request, we may need to contact third parties. By signing below, you authorize the Ofice of the Taxpayer Rights Advocate to make these contacts. We won’t give you notice that we’re contacting these third parties.

Signature of taxpayer or executor (if applicable) |

|

Date |

|

|

|

Signature of spouse (if applicable) |

|

Date |

|

|

|

Printed name and signature of corporate oficer |

Title |

Date |

|

|

|

Page 2 of 2

Instructions

The Ofice of the Taxpayer Rights Advocate (OTRA) is an independent organization within the New York State Department of Taxation and Finance. OTRA was created to safeguard taxpayer rights and to assist taxpayers who are experiencing problems with the Tax Department.

When to use this form

Use this form if you are experiencing any of the following problems:

•You are facing a threat of immediate adverse action

(e.g., seizure of an asset) for a debt you believe is not owed or where the action is, in your view, unwarranted, unfair, or illegal.

•You are experiencing undue economic harm or are about to suffer undue economic harm because of your tax problem.

•You believe there has been an undue delay by the Tax

Department in providing a response or resolution to your problem or inquiry.

•You believe the tax laws, regulations, or policies are being administered unfairly or have impaired (or will impair) your rights.

•You believe a Tax Department system or procedure has failed to operate as intended, or has failed to resolve your problem or dispute.

•You believe that the unique facts of your case or compelling public policy reasons warrant assistance.

When not to use this form

•If you haven’t exhausted all reasonable efforts to obtain timely relief through normal Tax Department channels.

•To seek legal or tax return preparation advice.

•To seek review of an unfavorable administrative law judge, Tax Appeals Tribunal, or judicial determination.

Specific instructions

Taxpayer information

Taxpayer identification — Enter your taxpayer identiication number if this request involves a business or

Tax type — Enter the tax type (for example, personal income tax, corporation tax, sales tax, etc.) that relates to this request.

Tax form(s) — Enter the form number(s) that relates to this request. For example, an individual taxpayer with an income tax issue might enter FORM

Tax period(s) — Enter the quarterly, annual, or other tax period(s) that relates to this request. For example, if this request involves an income tax issue, enter the calendar or iscal year; if an employment tax issue, enter the calendar quarter.

Business contact person — If a business entity is iling this form, enter the name of the person to contact about the request. This may be the corporate oficer signing the request, or another person authorized to discuss the matter.

Power of attorney

If you choose to have a representative act on your behalf, you must complete a power of attorney form.

Businesses: use Form

Individuals: use Form

Estates: use Form

You can get these forms from our Web site at www.nystax.gov.

Include the power of attorney form when you submit this form.

Describe the tax problem you are experiencing

Enter any detailed information necessary to describe the tax problem you are experiencing. If you have been involved with a Bureau of Conciliation and Mediation Services conference, a small claims hearing, the Tax Appeals Tribunal, a courtesy conference, an administrative law judge, an Offer in Compromise, or an audit or other collection action, include the dates of such activity, as well as the following information (if applicable):

•BCMS number

•DTA number

•audit case number

•assessment or collection case number

•formal or informal protest number

Where to file

Send your completed Form

By mail — NYS TAX DEPT

OTRA

W A HARRIMAN CAMPUS

ALBANY NY 12227

By fax — (518)

Privacy notification — The Commissioner of Taxation and Finance may collect and maintain personal information pursuant to the New York State Tax Law, including but not limited to, sections

This information will be used to determine and administer tax liabilities and, when authorized by law, for certain tax offset and exchange of tax information programs as well as for any other lawful purpose.

Information concerning quarterly wages paid to employees is provided to certain state agencies for purposes of fraud prevention, support enforcement, evaluation of the effectiveness of certain employment and training programs and other purposes authorized by law.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Manager of Document Management, NYS Tax Department, W A Harriman Campus, Albany NY 12227; telephone (518)

| Fact Name | Description |

|---|---|

| Form Purpose | The DTF-911 form is used to request assistance from the Office of the Taxpayer Rights Advocate in New York State. |

| Governing Body | This form is governed by the New York State Department of Taxation and Finance. |

| Who Should Use This Form | Taxpayers facing immediate adverse action or those experiencing undue economic harm should consider using this form. |

| Special Circumstances | The form addresses unique circumstances that warrant assistance due to the tax system's unfair administration. |

| Prior Efforts | Taxpayers must demonstrate that they have exhausted all reasonable efforts to resolve their issues through regular channels before using this form. |

| Contact Information | The DTF-911 form requires specific taxpayer details, including names, SSNs, contact numbers, and email addresses. |

| Power of Attorney | If someone represents the taxpayer, a power of attorney form must be includes, such as Form POA-1 or POA-1-IND. |

| Filing Method | The completed DTF-911 must be sent by mail or fax to the specified office at NYS Department of Taxation and Finance. |

| Privacy Notification | Personal information provided may be collected under various laws and is used to determine and administer tax liabilities. |

| Submission Requirements | Attachments may be necessary and the form must be completed as per the instructions provided on the second page. |

Filling out the DTF-911 form is a step toward seeking assistance from the Office of the Taxpayer Rights Advocate. This form requires personal information and details about the tax problem you are encountering. Ensure you have all necessary documents handy as you go through the steps below.

After completing the form, it is important to submit it along with any required attachments. You can send it by mail or fax as indicated in the instructions. Make sure to keep copies of everything for your records.

What is the DTF-911 form?

The DTF-911 form, also known as the Request for Assistance from the Office of the Taxpayer Rights Advocate, is a document provided by the New York State Department of Taxation and Finance. It is designed to assist taxpayers who are facing serious issues with the Tax Department that have not been resolved through standard procedures. This form allows individuals to formally request help when they believe their taxpayer rights are being compromised.

Who should use the DTF-911 form?

This form is intended for taxpayers who are experiencing immediate adverse actions regarding debts they believe are unwarranted, or undue economic harm due to tax-related issues. It is appropriate to use this form if you believe there has been an undue delay in resolving your problem, or if you consider that tax laws are being unfairly administered. Specific circumstances warranting this form include complications from disputes, undue delays, or failures in the Tax Department process.

What is considered an "immediate adverse action"?

An immediate adverse action refers to any measure taken by the Tax Department that negatively impacts the taxpayer without due cause. This includes actions such as asset seizures or other enforcement tactics, particularly when the taxpayer contests the legitimacy of the debt owed. If you find yourself in such a situation, submitting the DTF-911 can help you seek assistance.

What information do I need to provide on the DTF-911 form?

When filling out the DTF-911 form, you must supply various pieces of information, including your name, Social Security number, contact details, and a description of the tax problem. Additionally, outline any attempts you have made to resolve the issue through standard channels. Be as detailed as possible to help the Taxpayer Rights Advocate understand your situation.

Can I use the DTF-911 form if I have not exhausted other options?

No, the DTF-911 form is not suitable for use unless you have already made reasonable efforts to resolve your issues via other Tax Department channels. It's essential to demonstrate that all standard procedures have been attempted before resorting to this form for assistance.

Is there a way to authorize someone to represent me while submitting this form?

Yes, you can designate a representative by completing a power of attorney form. For businesses, use Form POA-1, while individuals should utilize Form POA-1-IND. If you are dealing with an estate, use Form ET-14. Make sure to include this power of attorney form alongside your DTF-911 submission.

How do I submit the DTF-911 form?

You can submit the completed DTF-911 form either by mail or by fax. If mailing, send it to the NYS Tax Department, OTRA, W A Harriman Campus, Albany, NY 12227. If choosing to fax it, the number is (518) 435-8532. Be sure to retain copies of your submissions for your records.

What will happen after I submit the DTF-911 form?

Upon submission, your request will be reviewed by the Office of the Taxpayer Rights Advocate. They may need to contact third parties to gather more information regarding your case. You will not receive prior notice of these communications. The objective is to assess your situation and provide the necessary assistance as expediently as possible.

Incomplete Personal Information: Failing to provide full names, Social Security numbers, or addresses can delay processing. Ensure all sections detailing personal information are filled out accurately.

Missing Tax Identification Number: If applicable, neglecting to include a taxpayer identification number can result in confusion. Always include this if your request involves a business or non-individual entity.

Not Specifying Tax Type: Leaving out the type of tax related to the issue, such as personal income or sales tax, can lead to difficulties in identifying the problem. Specify the relevant tax type to streamline the process.

Omitting Tax Form Numbers: Failing to enter the appropriate form number associated with your request complicates the processing. Identify the form that relates to the tax issue being raised.

Ignoring Required Details: Not providing detailed information about the tax issue may result in longer resolution times. Include specifics about prior attempts to resolve the issue and any involved tax department offices.

Forgetting Attachments: Neglecting to attach necessary documents, such as additional sheets with information, can hinder the review process. Prepare and include all relevant documents before submission.

Neglecting to Authorize Third-Party Contact: Failing to sign where permission is granted to contact third parties may lead to a lack of follow-up. Ensure you sign this section if applicable.

Not Providing Communication Preferences: Leaving out indications of special communication needs limits the ability of the Tax Department to assist effectively. Clearly mark any such needs.

Choosing Incorrect Submission Method: Submitting the form via fax when mail is required can delay processing. Review submission methods and choose the most appropriate one.

Missing Signatures: Omitting necessary signatures of the taxpayer, spouse, or executor can render the form invalid. Verify all required signatures are provided before submission.

When dealing with tax issues, various forms and documents may be required alongside the DTF-911 form to properly address your concerns. Below is a list of commonly used forms and documents that may facilitate your interactions with the tax authorities. Each has a specific purpose and may be essential for your request.

Ensure that you have all relevant forms and documents ready when submitting the DTF-911 form. This preparation can significantly affect your case and assist in expediting the resolution process. Addressing tax issues can be complex, and having the right information at hand will help safeguard your rights as a taxpayer.

The IRS Form 911, also known as the Request for Taxpayer Advocate Service Assistance, serves a purpose similar to the DTF-911 form. Taxpayers experiencing difficulties with the IRS can use this form when they believe their problems have not been addressed through regular channels. Much like the DTF-911, Form 911 seeks to advocate for taxpayer rights and ensures that individuals receive the assistance they need without facing undue hardship. The form requires a detailed explanation of the issue, previous resolutions attempted, and what specific help the taxpayer is requesting.

Another document similar to the DTF-911 is the IRS Form 2848, Power of Attorney and Declaration of Representative. This form allows taxpayers to grant another individual, such as a tax professional, the authority to act on their behalf. While the DTF-911 focuses primarily on resolving tax-related issues, Form 2848 establishes a representative who can handle various tax matters. It requires details about the taxpayer, the representative, and the scope of authority granted, making it essential for anyone needing representation in tax dealings.

The California Form 3530, Request for Assistance from the Taxpayer Advocate, mirrors the DTF-911 form in its purpose. This form assists California taxpayers who face difficulties with the state’s tax department and have not received timely or fair treatment. Similar to the DTF-911, it requires a description of the taxpayer's issue and any efforts made to resolve it. California's form ultimately aims to protect taxpayer rights and ensure that individuals receive the attention they need in a complicated tax environment.

The IRS Form 1040-X is another related document, particularly when it involves amending a tax return. Taxpayers who believe they submitted incorrect information can use this form to correct their returns. While it does not provide direct assistance like the DTF-911, it helps address tax issues that may lead to the need for further support. The process encourages taxpayers to rectify their situations, potentially avoiding larger problems with tax authority communications.

The New York State Form IT-201, Resident Income Tax Return, also shares similarities with the DTF-911. While Form IT-201 focuses on filing income taxes for residents, it can be pivotal for those experiencing issues that prompt the use of DTF-911. Errors or disputes arising from the income tax return can lead to situations where a taxpayer seeks assistance through the DTF-911. Therefore, while the two forms serve different functions, they can overlap in instances involving unresolved tax issues stemming from an income tax return.

The Form 8822, Change of Address, is another document relevant to taxpayers. While it does not specifically serve to resolve tax issues, it is important for individuals facing tax difficulties due to outdated contact information. Keeping the tax department updated on address changes can prevent further complications or misunderstandings in communication, thus indirectly supporting the goal of the DTF-911 to improve taxpayer experiences. Accurate information keeps lines of communication open and ensures timely responses from tax authorities.

Lastly, the IRS Form 4506, Request for Copy of Tax Return, has a useful role as well in relation to the DTF-911. When taxpayers are experiencing issues, having access to past tax returns can provide crucial information to resolve disputes. The DTF-911 assists when there are current problems with the tax department, but having accurate records from forms like 4506 can support taxpayer claims or provide clarity about past filings, facilitating the resolution process.

When completing the DTF-911 form, it is important to follow certain guidelines to ensure accuracy and efficiency. Below is a list of things to do and things to avoid during this process.

Following these guidelines can facilitate a smoother process when addressing your tax concerns with the Office of the Taxpayer Rights Advocate.

Many people have misunderstandings about the DTF-911 form, which can lead to confusion when seeking assistance with tax-related issues. Here are four common misconceptions:

The DTF-911 form is specifically designed for taxpayers who face urgent problems, such as imminent adverse actions or undue economic harm. It is not appropriate for general inquiries or unresolved disputes already addressed through other channels.

While the form connects you with the Office of the Taxpayer Rights Advocate, there is no promise of speedy resolution. Each case is assessed individually, and the timeline can vary based on the complexity of the issue.

You do not need legal representation to fill out and submit the DTF-911 form. Individuals can complete it on their own. However, those who prefer assistance may wish to consult a tax professional.

While personal information is safeguarded under privacy laws, you authorize the Taxpayer Rights Advocate to contact third parties as part of the process when you sign the form. Therefore, be mindful of the information you include.

Filling out the DTF-911 form can be essential for those facing tax-related issues in New York. Here are key takeaways to consider:

By following these guidelines, you can facilitate the process of obtaining the necessary assistance for your tax concerns.