The DR 1093 form, officially known as the Annual Transmittal of State W-2 Forms, serves as a crucial document for employers in Colorado when it comes to reporting withholding taxes. Typically filed in January, this form encompasses the details of W-2s for the previous calendar year. It's essential to note that if an employer needs to file an amended return, they must check the amended return box and submit a separate form for each year needing amendment. Importantly, the DR 1093 must accompany the total withholding statements provided to employees, and whether filing electronically or using paper forms, the completed DR 1093 must always be attached. Compliance with due dates is critical; active accounts must have the form postmarked by the end of January, while inactive accounts have a 30-day window following business closure. Employers need to accurately report total state withholdings and payments while carefully completing specific lines on the form, including penalties and interest if applicable. The Colorado Department of Revenue offers guidelines alongside this form, ensuring clarity in filing obligations and potential penalties for late submissions. Failure to adhere to these requirements could lead to complications, including delayed processing and maximum penalties. Understanding and properly completing the DR 1093 is vital for maintaining compliance and ensuring accurate tax reporting for all employees.

*DO=NOT=SEND*

DR 1093 (08/12/20)

COLORADO DEPARTMENT OF REVENUE

Tax.Colorado.gov

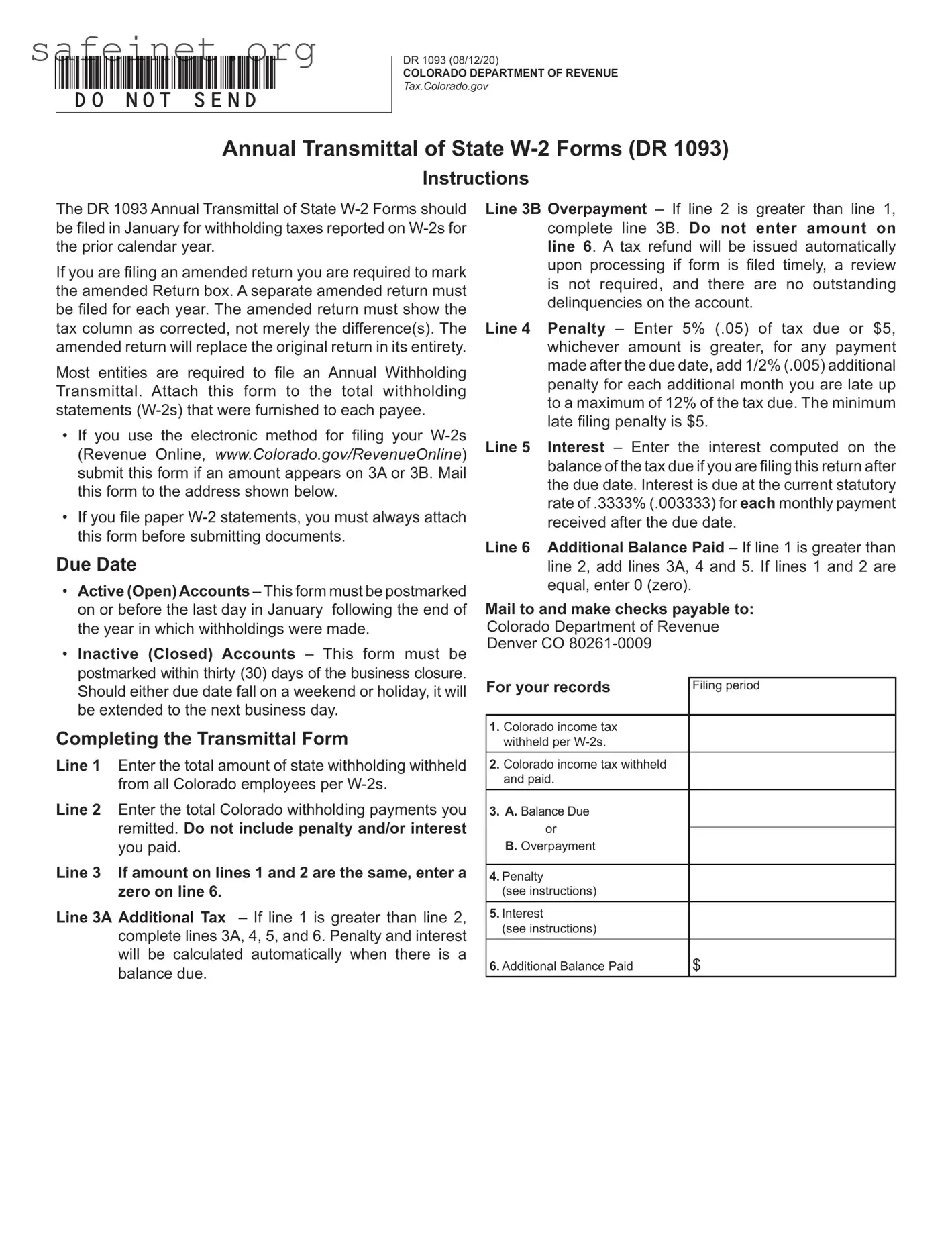

Annual Transmittal of State

Instructions

The DR 1093 Annual Transmittal of State

If you are filing an amended return you are required to mark the amended Return box. A separate amended return must be filed for each year. The amended return must show the tax column as corrected, not merely the difference(s). The amended return will replace the original return in its entirety.

Most entities are required to file an Annual Withholding Transmittal. Attach this form to the total withholding statements

•If you use the electronic method for filing your

•If you file paper

Due Date

•Active (Open)Accounts – This form must be postmarked on or before the last day in January following the end of the year in which withholdings were made.

•Inactive (Closed) Accounts – This form must be postmarked within thirty (30) days of the business closure. Should either due date fall on a weekend or holiday, it will be extended to the next business day.

Completing the Transmittal Form

Line 1 Enter the total amount of state withholding withheld from all Colorado employees per

Line 2 Enter the total Colorado withholding payments you remitted. Do not include penalty and/or interest you paid.

Line 3 If amount on lines 1 and 2 are the same, enter a zero on line 6.

Line 3A Additional Tax – If line 1 is greater than line 2, complete lines 3A, 4, 5, and 6. Penalty and interest will be calculated automatically when there is a balance due.

Line 3B Overpayment – If line 2 is greater than line 1, complete line 3B. Do not enter amount on line 6. A tax refund will be issued automatically upon processing if form is filed timely, a review is not required, and there are no outstanding delinquencies on the account.

Line 4 Penalty – Enter 5% (.05) of tax due or $5, whichever amount is greater, for any payment made after the due date, add 1/2% (.005) additional penalty for each additional month you are late up to a maximum of 12% of the tax due. The minimum late filing penalty is $5.

Line 5 Interest – Enter the interest computed on the balance of the tax due if you are filing this return after the due date. Interest is due at the current statutory rate of .3333% (.003333) for each monthly payment received after the due date.

Line 6 Additional Balance Paid – If line 1 is greater than line 2, add lines 3A, 4 and 5. If lines 1 and 2 are equal, enter 0 (zero).

Mail to and make checks payable to: Colorado Department of Revenue Denver CO

For your records |

Filing period |

|

|

|

|

1. |

Colorado income tax |

|

|

withheld per |

|

2. |

Colorado income tax withheld |

|

|

and paid. |

|

3. |

A. Balance Due |

|

|

or |

|

|

|

|

|

B. Overpayment |

|

|

|

|

4. Penalty |

|

|

|

(see instructions) |

|

5. Interest |

|

|

|

(see instructions) |

|

|

|

|

6. Additional Balance Paid |

$ |

|

*201093==19999*

DR 1093 (08/12/20)

COLORADO DEPARTMENT OF REVENUE

Tax.Colorado.gov

Page 1 of 1

Colorado Department of Revenue

Annual Transmittal of State

SSN 1 |

|

|

SSN 2 |

|

|

|

|

|

|

|

|

|

|

|

|

Account Number |

||||

FEIN |

|

|

||||

|

|

|

||||

Last Name or Business Name |

|

First Name |

|

|||

|

|

|

|

|

|

|

Middle Initial

Address

City

State

ZIP

Period (MM/YY – MM/YY) |

|

|

Due Date (MM/DD/YY) |

|

|

|

|

– |

|

|

|

|

|

|

|

|

|

Number of |

|

Phone Number |

|

|

|

|

|

|

|

|

|

Mark here if this is an Amended Return |

Paid by EFT |

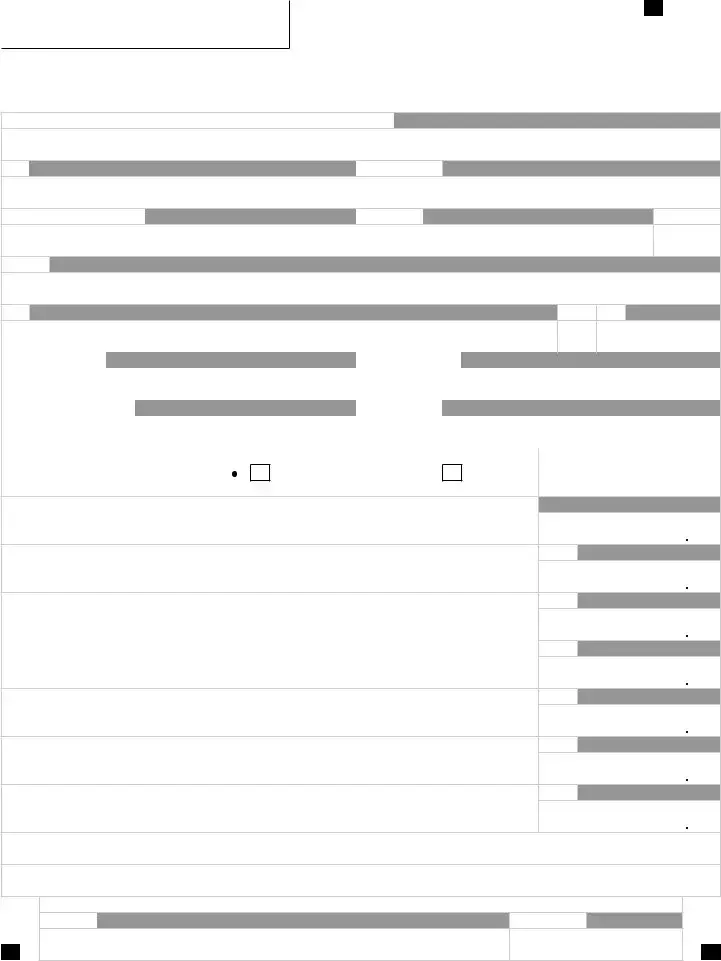

1. Total Colorado income taxes withheld per

(890)

2. Total Colorado income taxes remitted for the period indicated above.

(100)

3. A. Balance Due If line 1 is more than line 2, enter difference and (see instructions)

(415)

B. Overpayment If line 2 is more than line 1, enter the difference and (see instructions)

(200)

4. Penalty (see instructions)

(300)

5. Interest (see instructions)

(355)

6. Additional Balance Paid Add lines 3A, 4 and 5

The State may convert your check to a

Mail reconciliation with

Colorado Department of Revenue, Denver, CO

Signed under penalty of perjury in the second degree.

Signature

Date (MM/DD/YY)

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The DR 1093 is used to transmit state W-2 forms to the Colorado Department of Revenue. |

| Filing Timeline | This form should be filed in January for the previous calendar year’s withholding tax. |

| Amended Returns | If you are filing an amended return, mark the amended return box and submit a separate return for each year. |

| Due Date for Active Accounts | Postmark the form by January 31st following the year of withholdings for active accounts. |

| Due Date for Inactive Accounts | For closed accounts, the deadline is 30 days after the business closure. |

| Filing Method | Attach the DR 1093 to all W-2s when filing either electronically or on paper. |

| Late Penalties | A penalty of 5% or $5, whichever is greater, applies for late payments, with additional penalties for prolonged delays. |

| Interest on Balance | Interest at a statutory rate of 0.3333% is charged on overdue amounts. |

| Mailing Instructions | Mail the completed form and W-2s to the Colorado Department of Revenue, Denver, CO 80261-0009. |

| Electronic Payment Option | Checks may be converted to electronic transactions, which will be processed promptly upon receipt. |

You’re ready to file the DR 1093 form for your state W-2 filings. Whether you are reporting a balance due or an overpayment, it’s essential to complete the form correctly and submit it on time. Here’s a straightforward guide to help you fill out the necessary information.

Once filled out, mail the DR 1093 along with your W-2 forms to the Colorado Department of Revenue. Ensure your submission is postmarked by the appropriate deadline to avoid penalties.

What is the purpose of the DR 1093 form?

The DR 1093 form is used for the Annual Transmittal of State W-2 Forms in Colorado. Employers must file this form to report withholding taxes from employee wages for the previous calendar year. By submitting it, employers ensure that the state receives the total amount of state tax withheld from all employees’ W-2 forms. This is essential for maintaining accurate records and compliance with state tax law.

When is the DR 1093 form due?

The deadline for filing the DR 1093 form is the last day of January each year. This applies to active accounts, meaning businesses still in operation. For inactive or closed accounts, the form must be submitted within thirty days of closing the business. If the due date falls on a weekend or holiday, the deadline extends to the next business day. Meeting this deadline is crucial to avoid penalties.

How do I complete the DR 1093 form?

To complete the DR 1093, start by filling in your total Colorado income tax withheld from employee W-2s on Line 1. Then, report the total taxes you have remitted on Line 2. If the amounts differ, you must complete additional lines to report any balance due or overpayment. Make sure to follow the instructions for calculating any penalties or interest to ensure accuracy. Lastly, ensure the completed form is attached to the W-2s and mailed to the Colorado Department of Revenue.

What happens if I file the DR 1093 form late?

If you submit the DR 1093 form after the due date, penalties and interest may apply. The penalty is generally 5% of the tax due or a minimum of $5, plus an additional 0.5% for each month the payment is late, up to 12% total. Interest, calculated at the current statutory rate, will also accrue if the form is filed late. To avoid these costs, timely filing is essential.

When filling out the DR 1093 form, people often make mistakes that can lead to delays or issues with their tax reporting. Here are seven common mistakes:

Taking the time to review these areas can help ensure your filing is processed smoothly and accurately.

The DR 1093 form serves as the Annual Transmittal of State W-2 Forms in Colorado. This document must be filed annually to report withholding taxes based on W-2s for the prior calendar year. Several other forms and documents often accompany the DR 1093 to ensure compliance and accuracy in tax reporting. Below is a list of these relevant documents.

Filing the appropriate forms alongside the DR 1093 ensures that all necessary information is accurately reported to the Colorado Department of Revenue. This helps avoid penalties and streamlines the process of year-end tax compliance.

The DR 1093 form serves as an annual transmittal for state W-2 forms, much like the IRS Form 941. Businesses use Form 941 to report income taxes, Social Security tax, or Medicare tax withheld from employee's paychecks. This form is also filed quarterly, which contrasts with the annual requirement of the DR 1093. Yet, both forms ensure that the proper taxes are reported and submitted to the appropriate authority, making them fundamental to accurate payroll processing and tax compliance.

The DR 1093 is akin to Form W-3, which is the transmittal form for all W-2s issued by an employer to the Social Security Administration. While W-3 is used to summarize the individual W-2 forms for federal purposes, the DR 1093 does so at the state level. Both forms require accurate totals of the wages and withholding information and must be filed alongside their respective W-2 forms, ensuring comprehensive reporting to both federal and state agencies.

Another document similar to the DR 1093 is Form 1099-MISC, used to report payments made to independent contractors. While the DR 1093 deals with employee wages and withholdings, the 1099-MISC focuses on non-employee compensation. Nonetheless, both forms play a significant role in reporting earnings, providing detailed financial information to the IRS and ensuring compliance with tax regulations for different types of workers.

The Colorado DR 1093 also parallels Form 945, which reports federal income tax withheld from non-payroll payments like pensions and annuities. Both documents highlight the need for accurate reporting on withholdings, although they cater to different payment structures. While DR 1093 is centered on employee wages, Form 945 covers other types of income, providing tax authorities with comprehensive data on total withholding activities within a filing period.

In the realm of state taxes, the DR 1093 resembles Form ST-3, which is used for reporting sales tax withheld by businesses in some states. Though not specifically to employee wages, the purpose of accurate tax reporting remains consistent across both forms. Each facilitates the collection of state revenue and supports compliance efforts for businesses, underscoring the importance of precise accounting in different financial contexts.

Moreover, the DR 1093 can be compared to Form 660, which is utilized for reporting Colorado's state taxes withheld but is specific to contractors and certain types of payments. Both forms aim to detail withholding activities to ensure state revenue is collected appropriately. They serve distinct purposes but follow similar principles in reporting and accountability to meet tax obligations efficiently.

The DR 1093 is also similar to form CT-1, which is filed by employers covering railroad retirement tax withheld. While this document targets a specific group of employees in the railroad industry, it shares similarities with the DR 1093 in terms of being an annual summary of withholdings. Both forms maintain thorough records, contributing to the larger framework of employer responsibilities in tax reporting.

Finally, the DR 1093 has similarities with Form 1095-C, which provides information about health insurance coverage offered by large employers. While the focus is different—health care vs. wage withholdings—both forms are crucial for compliance with federal and state regulations. They share the function of serving as declarations of compliance, illustrating the breadth of information employers must report to government entities for various fiscal responsibilities.

When filling out the DR 1093 form, attention to detail is crucial to ensure compliance and avoid potential penalties. Here are four important things to remember:

Adhering to these guidelines will help streamline the process and facilitate timely handling of your submission by the Colorado Department of Revenue.

Misconceptions about the DR 1093 form can lead to confusion, especially for businesses filing their annual transmittals. Here are six common misunderstandings:

Understanding the facts surrounding the DR 1093 form is crucial for compliance and to avoid unnecessary penalties. Make sure you read the instructions carefully and submit the required documentation on time.

When handling the DR 1093 form, ensure you grasp the following key points:

By keeping these essentials in mind, you will ensure a smoother filing process and compliance with state regulations.