The Dr 0100 form is an essential document for retailers in Colorado, as it provides a structured way to report retail sales and remit the appropriate sales taxes. Every retailer, regardless of sales volume, is required to file this form for each specified filing period, even if no transactions have taken place. The filing frequency is typically monthly, but this can vary based on specific guidelines set forth in the Colorado Sales Tax Guide. It's important for retailers to remember that separate returns must be submitted for each business location. Failure to file can lead to estimated tax situations where the Department of Revenue issues a notice based on their own calculations. The form offers various electronic filing options as well, making it easier for retailers to submit their returns. Payment can be made via electronic funds transfer or a paper check, providing flexibility. Detailed instructions assist retailers in filling out the form correctly, ensuring they report not just state tax but also local taxes for different jurisdictions. Additional resources are available to avoid common mistakes and ensure compliance. Understanding the Dr 0100 form is crucial for any retailer to successfully navigate the tax landscape in Colorado.

*DO*NOT*SEND*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Colorado Retail Sales Tax Return

General Information

Retailers must file a sales tax return for every filing period, even if the retailer made no sales during the period and no tax is due. Typically, returns must be filed on a monthly basis. See Part 7: Filing and Remittance in the Colorado Sales Tax Guide for additional information regarding filing frequency.

A separate return must be filed for each business site or location at which a retailer makes sales. If a retailer fails to file a return for any filing period, the Department will estimate the tax due and issue to the retailer a written notice of the estimated tax due. The Department may deactivate the sales tax account of a retailer who fails to file returns for successive filing periods.

Electronic Filing Information

The Department offers multiple electronic filing options that retailers may use as an alternative to filing paper returns.

•Revenue Online – Retailers must first create a Revenue Online account to file returns through Revenue Online. Retailers who file returns through Revenue Online must file separate returns for each of the retailer’s business sites or locations. Revenue Online can be accessed at

Colorado.gov/RevenueOnline.

•XML Filing – Retailers may file returns electronically in an XML (Extensible Markup Language) format using any of the approved software options listed online at

Retailers do not need to obtain any special approval from the Department to file using an approved software option.

•Spreadsheet Filing – Retailers may file electronically using an approved Microsoft Excel spreadsheet. Each retailer must obtain approval from the

Department before filing returns with an Excel spreadsheet. Information can be found online at

Payment Information

The Department offers retailers several payment options for remitting sales taxes.

Electronic Payments

Regardless of whether they file electronically or with a paper return, retailers can remit payment electronically using one of two payment methods. Retailers who remit electronic payments should check the appropriate box on line 18 of the return to indicate their electronic payment.

•EFT Payment – Retailers can remit payment by electronic funds transfer (EFT) via either ACH debit or ACH credit. There is no processing fee for EFT payments. Retailers must register prior to making payments via EFT and will not be able to make payments via EFT until

•Credit Card and

Paper Check

Regardless of whether they file electronically or with a paper return, retailers can remit payment with a paper check. Retailers should write “Sales Tax,” the account number, and the filing period on any paper check remitted to pay sales tax

*DO*NOT*SEND*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

to ensure proper crediting of their account.

•Paper Return – Retailers who file a paper return can mail a paper check with the return to pay the tax reported on the return.

•Electronic Filing Through Revenue Online – A retailer who files electronically through Revenue Online can remit payment by paper check. Once the electronic return has been submitted, the retailer can select “Payment Coupon” for the payment option to print a payment processing document to send along with their paper check.

Physical And

A retailer is required to obtain a sales tax license and file separate sales tax returns for each separate place of business at which the retailer makes sales (a “physical site”). Additionally, if a retailer delivers taxable goods or services to a purchaser at any location other than the retailer’s place of business, the retailer must register with the Department a

Filing A Paper Return

Retailers electing to file a paper return must sign, date, and mail the return, along with their payment, if applicable, to:

Colorado Department of Revenue

Denver CO

Retailers are required to keep and preserve for a period of three years all books, accounts, and records necessary to determine the correct amount of tax.

Items Removed From Inventory

Any tangible personal property a retailer purchased for resale, but subsequently removed from inventory for the retailer’s own use, is subject to consumer use tax. A Consumer Use Tax Return (DR 0252) is required to report and remit any consumer use tax a retailer owes.

Additional Resources

Additional sales tax guidance and filing information can be found online at Tax.Colorado.gov. These resources include:

•Colorado Sales Tax Guide

•Sales tax classes and videos available online at

Tax.Colorado.gov/education.

•The Customer Contact Center, which can be contacted at (303)

Form Instructions

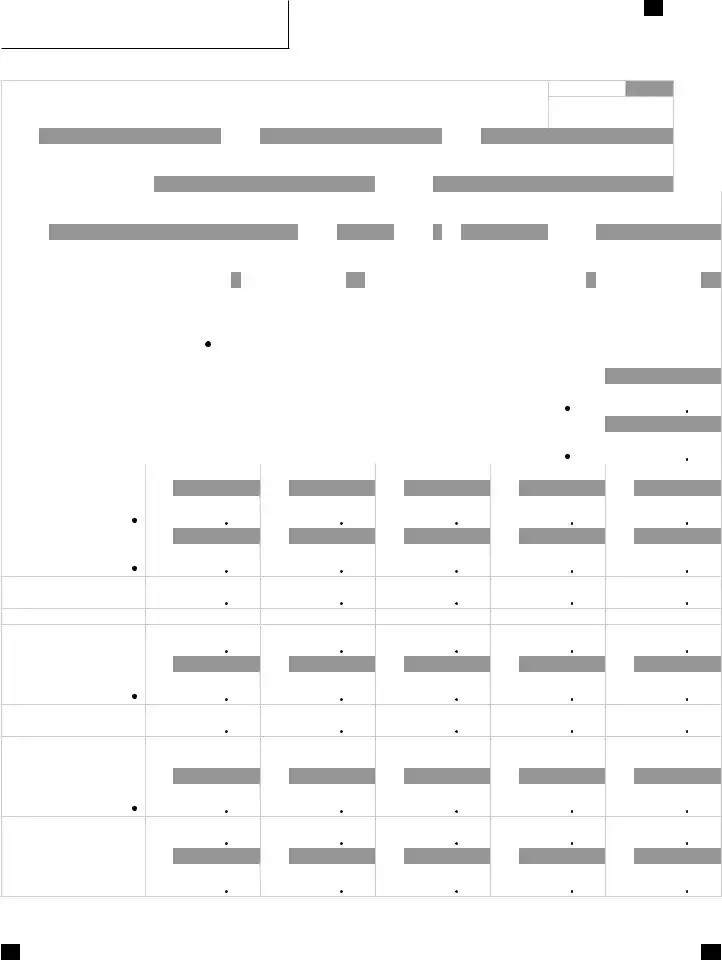

In preparing a sales tax return, a retailer must include its identifying information (such as name and account number), the filing period and due date, and information about sales and exemptions in order to calculate the tax due. Specific instructions for preparing sales tax returns appear below and on the following pages.

SSN and FEIN

Retailers must provide a valid identification number, issued by the federal government, when filing a sales tax return. If the retailer is a corporation, partnership, or other legal entity, this will generally be a Federal Employer Identification Number (FEIN). If the retailer is a sole proprietorship, a Social Security number (SSN) will generally be used instead.

Colorado Account Number

Retailers must enter their Colorado account number on each return, including both their

If you have applied for your license, but do not have your account number, please contact the Customer Contact Center at (303)

Period

Retailers must indicate the filing period for each return. The filing period is defined by the first and last months in the filing period and entered in a

•For a monthly return for January 2020, the filing period would be

•For a quarterly return for the first quarter (Jan. through March) of 2020, the filing period would be

•For an annual return filed for 2020, the filing period would be

Location Juris Code

Retailers must enter the

Due Date

Retailers must enter the due date for the return. Returns are due the 20th day of the month following the close of the filing period. If the 20th is a Saturday, Sunday, or legal holiday, the return is due the next business day.

*DO*NOT*SEND*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Monthly Returns: due the 20th day of the month following the reporting month.

Quarterly Returns:

1st quarter (January – March): due April 20

2nd quarter (April – June): due July 20

3rd quarter (July – September): due October 20

4th quarter (October – December): due January 20 Annual Returns: (January – December): due January 20

Amended Returns

If a retailer is filing a return to amend a previously filed return, the retailer must mark the applicable box to indicate that the return is an amended return. A separate amended return must be filed for each filing period and for each site/location. The amended return replaces the original return in its entirety and must report the full corrected amounts, rather than merely the changes in the amount of sales or tax due. If the amended return reduces the amount of tax reported on the original return, the retailer must file a Claim for Refund (DR 0137) along with the amended return to request a refund of the overpayment. If the amended return is filed after the due date and reports an increase in the amount of tax due, penalties and interest will apply.

State and

The Colorado Retail Sales Tax Return (DR 0100) is used to report not only Colorado sales tax, but also sales taxes administered by the Colorado Department of Revenue for various cities, counties, and special districts in the state. The sales taxes for different local jurisdictions are calculated and reported in separate columns of the DR 0100. Local sales taxes reported on the DR 0100 include:

•RTD/CD – Sales taxes for the Regional Transportation District (RTD) and the Scientific and Cultural Facilities District (CD) are reported in the RTD/CD column of the DR 0100.

•Special District – Special district sales taxes reported in the Special District column include sales taxes for any Regional Transportation Authority (RTA), Multi- Jurisdictional Housing Authority (MHA), Public Safety Improvements (PSI), Metropolitan District Tax (MDT), or Health Services District (HSD). Sales taxes for Mass Transportation Systems (MTS) and Local Improvement Districts (LID) are not reported in the Special District column, but are instead reported in the County/MTS and City/LID columns, respectively.

•County/MTS – County and Mass Transportation Systems (MTS) sales taxes administered by the Department are reported in the County/MTS column.

•City/LID – City and Local Improvement Districts (LID) sales taxes administered by the Department are reported in the City/LID column.

Many

cannot be reported and remitted with the DR 0100. Retailers must report such taxes directly to the applicable city.

See Department publication Colorado Sales/Use Tax Rates (DR 1002) for tax rates, service fee rates, and exemption information for state and

Avoiding Common Filing Errors

You can avoid several common errors by reviewing your return before filing it to verify that:

•You completed all applicable lines of the return.

•You completed all three pages of the return, including Schedule A and Schedule B. You must complete and submit all three pages when filing your return, even if you have no deductions or exemptions to report on Schedule A or Schedule B.

•You used the correct version of the form, depending on the filing period. There are different versions of the sales tax return for each year 2016 through 2020.

•You entered your account number and site number correctly on your return.

•You used the correct tax rate for each jurisdiction reported on your return. See

Additional information about common filing errors can be found online at

Specific Line Instructions

Retailers must complete all applicable lines, including lines 1, 2, 3, 4, 14, and 18, entering 0 (zero), if applicable. Retailers must also include Schedules A and B for each site/location.

Line 1. Gross sales of goods and services for this site/ location only

Enter the gross sales of goods and services made during the filing period. Include only sales sourced pursuant to state law to the site/location indicated on the return. See Part 7: Retail Sales in the Colorado Sales Tax Guide for additional information regarding sourcing.

For small retailers subject to origin sourcing rules, include all sales made from the retailer’s physical site/location, regardless of whether the property or service is delivered to the purchaser at another location.

For all other retailers who are subject to destination sourcing rules, do not include on a return for any physical site any sales delivered to the purchaser and sourced for sales tax purposes to another location. For

Include all sales of goods and services, whether taxable or not, and the collection during the filing period of any bad debts deducted on a return filed for a previous filing period.

*DO*NOT*SEND*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Line 6. Tax rate

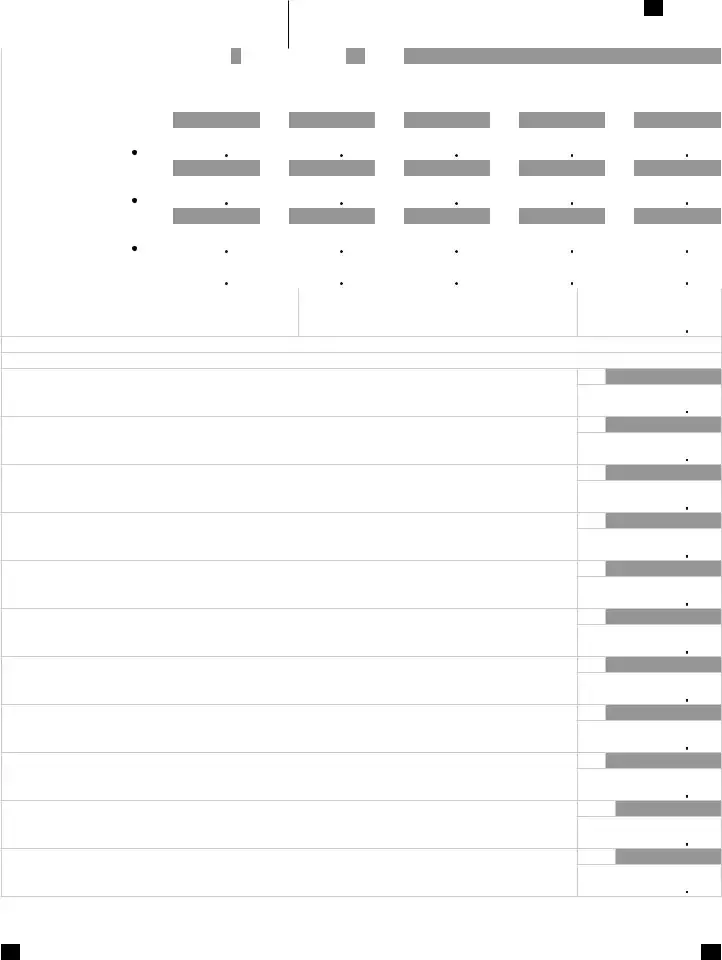

Enter the applicable state, city, county, and/or special district tax rate in each column of the return. The Colorado state sales tax rate is 2.9%. The sales tax rates for each city, county, and special district can be found in Department publication Colorado Sales/Use Tax Rates (DR 1002) or online at Colorado.gov/RevenueOnline.

Line 8. Excess tax collected

Enter any tax collected in excess of the tax due as computed on line 7. For example, if the retailer collected $50 of county sales tax during the filing period, but only $45 of tax is calculated in the County/MTS column of the return, the excess $5 of tax collected must be reported on this line.

Line 10. Service fee rate

Enter the applicable service fee rate in each column of the return. The Colorado state service fee rate is 4%. Service fee rates for each city, county, and special district can be found in Department publication Colorado Sales/Use Tax Rates (DR 1002).

Line 11. Service fee

The service fee is calculated by multiplying the amount on line 9 by the rate on line 10. The full amount calculated should be entered on line 11, unless the return is filed after the due date or possibly if the return is an amended return. Both of these situations are addressed in the following instructions.

If the amount in the state column, line 5 (net taxable sales) is $1,000,000 or greater, enter $0.

Retailers with multiple sites must add the amounts in the state column, line 5 for all sites. If the sum is greater than $1,000,000, enter $0.

Timely payment of tax

If the tax calculated on the return is paid by the return due date, enter on line 11 the service fee calculated by multiplying the amount on line 9 by the service fee rate on line 10, regardless of whether the return is an original or amended return. If the return is an original return and the tax is not paid by the due date for the return, and therefore no service fee is allowed, enter $0 on line 11.

Amended returns

If the return is an amended return and the tax reported on the original return was not paid by the due date for the return, the allowable service fee on the amended return is $0.

If the tax reported on the original return was paid by the due date and the amended return reports an increase of the tax due, the allowable service fee on the amended return is equal to the service fee allowed on the original return. Enter on line 11 of the amended return the service fee allowed on the original return. No additional service fee is allowed for the additional tax reported on the amended return.

If the tax reported on the original return was paid by the due date and the amended returns reports a decrease of the tax due, enter on line 11 the amount calculated by multiplying the amount on line 9 of the amended return by the service fee rate on line 10.

Limit on state service fee

The total combined Colorado state service fee allowed to a retailer for any given filing period is limited to $1,000. The retailer should enter on line 11 the full amount calculated by multiplying the amount on line 9 times the rate on line 10, but if the combined Colorado state service fee calculated on the retailer’s sales tax returns for all sites/locations for the filing period exceeds $1,000, the retailer must complete the State Service Fee Worksheet (DR 0103). The worksheet is used to determine what amount, if any, the retailer must pay in addition to the total balance due calculated on line 18 of the retailer’s returns. The amount of additional tax calculated on the State Service Fee Worksheet (DR 0103) should not be entered anywhere on the retailer’s Colorado Retail Sales Tax Return (DR 0100).

Beginning January 1, 2022, a retailer with total state net taxable sales (Column 1, line 5 or the sum of Column 1, line 5 across all sites), greater than $1,000,000 is not eligible to retain the state vendor's fee.

Line 13. Credit for tax previously paid

If a retailer overpaid tax on any previously filed return for a different filing period, and a refund claim for such overpayment is not barred by the statute of limitations, the retailer may claim a credit against tax calculated on the current return for such prior overpayment. Credit may be claimed only for tax overpayments for the same site/location and the same state or local jurisdiction. No credit may be claimed for an overpayment reflected in Department records either because the retailer filed an amended return or the Department adjusted the tax for the prior filing period.

Line 15. Penalty

If any retailer does not, by the applicable due date, file a return, pay the tax due, or correctly account for tax due, the retailer will owe a penalty. The penalty is 10% of the tax plus 0.5% of the tax for each month the tax remains unpaid, not to exceed a total of 18%. The minimum penalty amount is $15.

Line 16. Interest

If the tax is not paid by the applicable due date, the retailer will owe interest calculated from the due date until the date the tax is paid. See FYI General 11 for interest rates and information about interest calculation.

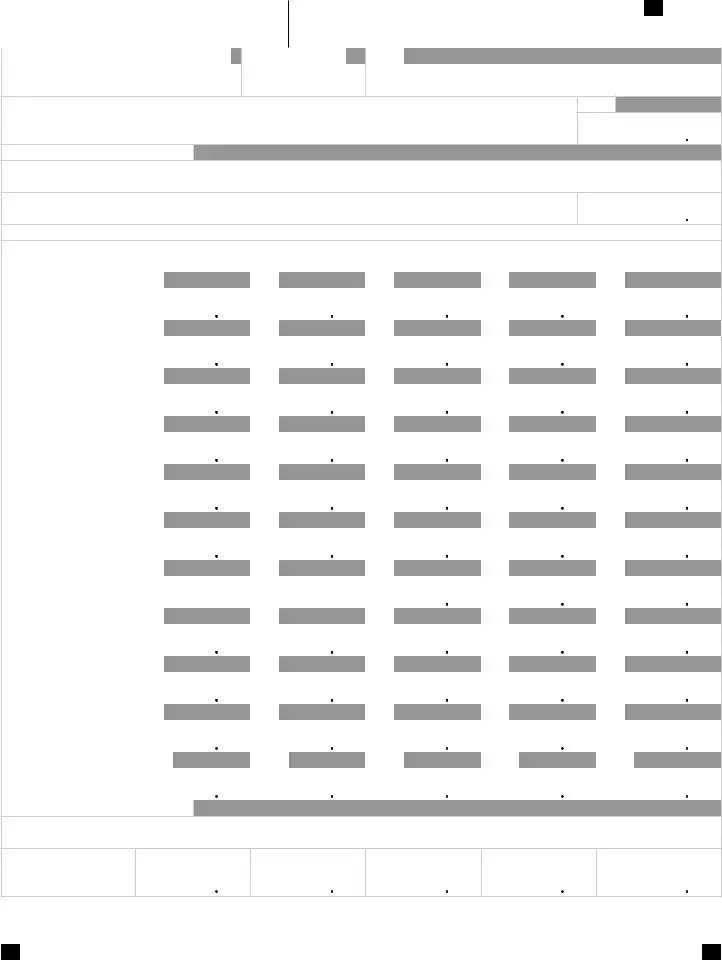

Schedule A and Schedule B

Schedule A and Schedule B are used to report various deductions and exemptions. Any amounts entered on lines 2 or 4 of the return may be disallowed if Schedules A and B for each site/location are not completed and included with the return. In general, Schedule A includes deductions and exemptions that are not optional for state- administered local jurisdictions and Schedule B includes exemptions that are optional for local jurisdictions. See the Supplemental Instructions available online at

*190100==19999*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Colorado Retail Sales Tax Return

Signature (Signed under penalty of perjury in the second degree).

Date (MM/DD/YY)

SSN 1 |

|

|

|

|

|

|

SSN 2 |

|

|

|

|

|

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Last Name or Business Name |

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP |

|

|

|

Phone |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Colorado Account Number |

|

Period |

|

Location Juris Code (Refer to form DR 0800) |

|

Due Date (MM/DD/YY) |

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Mark here if this is an Amended Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1. Gross sales of goods and services for this site/location only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2. Total from line 13 of Schedule A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

State |

|

|

RTD/CD |

|

Special District |

County/MTS |

|

|

|

City/LID |

|||||||||||||||

3. Subtract line 2 from line 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

and enter the result in each |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

applicable column |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

4.Total from line 12 of

Schedule B

5.Net taxable sales:

Subtract line 4 from line 3

6.Tax rate

7.Tax on net taxable sales:

Multiply line 5 by line 6

|

|

8. Excess tax collected

9.Add lines 7 and 8

10.Service fee rate

|

|

11. Service fee: Multiply line 9 by line 10

12.Net tax due: Subtract line 11 from line 9

|

|

13.Credit for tax previously paid

Attention: Continue to pages 2 and 3 to complete your return.

Page 1

*190100==29999*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Colorado Account Number |

|

|

Period |

|

Name |

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

|

RTD/CD |

|

|

Special District |

County/MTS |

|

|

City/LID |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

14. |

Subtract line 13 from |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

line 12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

15. |

Penalty |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

16. |

Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17. |

Add lines 14, 15, and 16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The State may convert your check to a |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Your bank account may be debited as early as the same day received by the |

18. Balance due: Add |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

||||||||||||||

State. If converted, your check will not be returned. If your check is rejected due |

amounts from line 17 |

|

Paid by EFT |

|

|

|

||||||||||||||

to insufficient or uncollected funds, the Department of Revenue may collect the |

|

$ |

|

|

||||||||||||||||

|

|

|

||||||||||||||||||

payment amount directly from your bank account electronically. |

|

|

|

in each column |

|

|

(355) |

|

|

|||||||||||

Schedule A (see instructions)

This schedule is required if any amount is entered on line 2 of Form DR 0100.

1.Wholesale sales, including wholesale sales of ingredients and component parts

2.Sales made to nonresidents or sourced to locations outside of Colorado

3.Sales of nontaxable services

4.Sales to exempt entities and organizations

5.Sales of gasoline, dyed diesel, and other exempt fuels

6.Sales of exempt drugs and medical devices

7.Fair market value of property received in exchange and held for resale

8.Bad debts

9.Cost of exempt utilities upon which tax was previously paid (restaurants must complete and attach Form DR 1465)

10.Exempt agricultural sales, not including farm and dairy equipment

11.Sales of computer software that is not taxable

Page 2

*190100==39999*

DR 0100 (09/27/21)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Colorado Account Number |

Period |

Name |

|

–

12.Other exempt sales (see instructions and identify type(s) of exemption(s) claimed below)

Type(s) of other exemption(s) claimed:

13.Add lines 1 through 12. Enter the total on line 2 of Form DR 0100.

Schedule B (see instructions)

This schedule is required if any amount is entered on line 4 of Form DR 0100.

1. |

Sales of food for domestic |

|

|

State |

|

|

RTD/CD |

|

Special District |

|

County/MTS |

|

|

|

City/LID |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

home consumption and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

food sold through vending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

machines |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

2. |

Sales of machinery and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

machine tools |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

3. |

Sales of electricity and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

fuel for residential use |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

4. |

Sales of farm and dairy |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Sales of medium and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

heavy duty |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

vehicles and associated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

parts and power sources |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

Exempt sales made |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

by schools, school |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

organizations, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

charitable organizations |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

7. |

Sales of cigarettes |

|

|

N/A |

|

|

|

N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

8. |

Sales of renewable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

energy components |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

9. |

Sales of property for use |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

in space flight |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. Sales of retail |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

marijuana and retail |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

marijuana products |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. Other exempt sales (see |

|

|

|

|

|

|

|

|

|

|||||||||||

|

instructions and identify |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

type(s) of exemption(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

claimed below) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type(s) of other exemption(s) claimed:

12.Add lines 1 through 11 of each column. Enter the total on line 4 of Form

DR 0100.

Page 3

| Fact Name | Details |

|---|---|

| Filing Requirement | All retailers must file a sales tax return for each filing period, regardless of sales. This includes periods with no sales. |

| Filing Frequency | Returns are typically filed monthly. Specific filing frequency can vary, and details can be found in the Colorado Sales Tax Guide. |

| Separate Returns | A separate return is needed for each business site where sales are made. |

| Electronic Filing | Retailers can file electronically through methods like Revenue Online, XML, or approved spreadsheets for convenience. |

| Payment Methods | Retailers can remit taxes electronically via EFT, credit card, electronic check, or by mail with a paper check. |

| License Requirement | Retailers must obtain a sales tax license and file separate returns for physical and non-physical delivery sites. |

| Due Date | Returns are due on the 20th of the month following the reporting period. If that date falls on a weekend or holiday, the return is due the next business day. |

| Amended Returns | If correcting a previously filed return, an amended return must be marked and submitted for each relevant period. |

| Sales Tax Reporting | The form is used to report Colorado state sales tax as well as local sales taxes for various jurisdictions, organized by column on the return. |

| Common Errors | It’s key to check for completion of all necessary lines and to ensure correct versions of the form are used for accurate filing. |

Completing the DR 0100 form is an essential process for retailers in Colorado to report their sales tax obligations. Once filled out, this form can be submitted to the Colorado Department of Revenue along with any required payments. Following the steps below will assist in ensuring that the form is completed correctly and accurately.

Once the form is filled, review it carefully to avoid common errors. The completed form should be mailed to the Colorado Department of Revenue along with any payment, if applicable. Proper recordkeeping is crucial, as retailers should retain all pertinent documents for a three-year period to demonstrate compliance and accuracy in their reporting.

What is the DR 0100 form?

The DR 0100 form is the Colorado Retail Sales Tax Return that retailers must complete and submit to report sales tax collections. This form is necessary regardless of whether a retailer made any sales during the filing period. It ensures all retailers comply with state tax laws by filing returns either monthly, quarterly, or annually, depending on their specific situation.

When is the DR 0100 form due?

The due date for the DR 0100 form depends on the type of return you are filing. Monthly returns are due on the 20th day of the month following the reporting month. Quarterly returns are due on April 20, July 20, October 20, and January 20 for their respective quarters. Annual returns are due on January 20 of the following year. If the due date lands on a weekend or holiday, the deadline extends to the next business day.

What happens if I fail to file the DR 0100 form?

If a retailer does not file the DR 0100 form for any period, the Colorado Department of Revenue may estimate the tax due and issue a notice to the retailer. Continued failure to file could result in the deactivation of the retailer’s sales tax account. Thus, it’s crucial to submit the form on time to avoid complications.

How do I file the DR 0100 form?

Retailers can file the DR 0100 form electronically or via paper submission. Electronic filing can be done through the Revenue Online platform, where separate returns are required for each business site. For paper submissions, retailers must mail the completed form and any associated payments to the Colorado Department of Revenue. Always ensure all necessary fields are filled out correctly to prevent rejection.

Can I amend a previously filed DR 0100 form?

Yes, if a retailer needs to amend a previous return, they can do so by checking the amended return box on the form. It's important to file a separate amended return for each period and each site or location. The amended return must report the correct amounts and not just the changes. If an overpayment has occurred, a Claim for Refund must be filed alongside the amended return.

What payment options are available for the taxes reported on the DR 0100?

Retailers have several options to remit payment for the taxes reported on the DR 0100. Electronic payments can be made via Electronic Funds Transfer (EFT) without a processing fee, or through credit card and e-check, which do have a processing fee. Payments can also be mailed as a paper check alongside the completed form, ensuring all necessary details are specified to guarantee correct crediting.

What information do I need to complete the DR 0100 form?

When completing the DR 0100 form, retailers must provide their identification information such as name, Colorado account number, and the filing period. It's also essential to report gross sales, applicable tax rates for each jurisdiction, and any credits or exemptions. Schedules A and B must accompany the return if applicable, providing deductions or exemptions for each site/location.

Not Completing All Required Lines: A common mistake is failing to fill out all applicable lines of the return, especially lines 1, 2, 3, and 4. Each section contributes to an accurate calculation of taxes owed.

Forgetting to File for Multiple Locations: Retailers often overlook that separate returns are necessary for each business site. You cannot lump all sales together in one return, even if the same retailer owns multiple places.

Incorrect Account and Juris Codes: Many people misenter their Colorado account number or the location jurisdiction code. This can lead to misallocated taxes and unnecessary delays.

Missing the Due Date: It's easy to forget that returns are due on the 20th day following the end of the filing period. Missing this deadline can result in penalties and interest accruing on the unpaid amounts.

Each of these mistakes can complicate the filing process significantly, but with careful attention, they can be easily avoided. Always double-check your entries before submitting to ensure compliance and accuracy.

The DR 0100 form is a crucial document for retailers in Colorado as it relates to the filing of retail sales tax returns. Several other forms and documents often accompany the completion of the DR 0100 to ensure compliance and facilitate accurate tax reporting. Below are five commonly used forms and documents that might be necessary in this process.

Using these forms and documents alongside the DR 0100 can help retailers navigate the complexities of tax compliance in Colorado. Each form serves a distinctive purpose that aids in facilitating accurate tax reporting and adherence to state regulations.

The Colorado Consumer Use Tax Return (DR 0252) is similar to the DR 0100 form as it is used to report tax owed on items that a retailer bought for resale but later used for personal purposes. Both forms require the identification of the entity along with the appropriate tax calculations. Like the DR 0100, it necessitates the reporting of gross sales, applicable tax rates, and payment information. However, while the DR 0100 focuses primarily on sales tax collected on retail sales, the DR 0252 specifically targets use tax obligations, often arising from items that were not sold but consumed by or used within the business.

The Colorado Claim for Refund form (DR 0137) serves a purpose similar to that of the DR 0100 in that it is filed when a business seeks to recover overpaid taxes. This form requires relevant details about the overpayments and the activities leading to them. Both forms also demand accuracy in reporting periods and account numbers. However, the Claim for Refund primarily addresses situations involving prior overpayments or excess tax collected, whereas the DR 0100 is more centered on the current sales and tax amounts due.

The Federal Employer Identification Number (FEIN) Application (Form SS-4) is another document that shares characteristics with the DR 0100. While the DR 0100 includes space for the FEIN to identify the retailer, the SS-4 is used to apply for that identification number. Both forms are essential for tax reporting and compliance, as the FEIN helps the IRS and other governmental agencies track tax obligations for business entities. They each require identifying information and situational context about the taxpayer’s operations.

The Colorado Sales Tax License Application (DR 100) resembles the DR 0100, as it is critical for retailers who wish to operate legally and remit sales tax. Both forms are integral to understanding a retailer's tax responsibilities and require details such as business name and location. However, while the DR 0100 is used for filing returns after sales have occurred, the DR 100 is an initiation form that allows businesses to obtain a sales tax license in the first place.

The IRS Form 1040, or the U.S. Individual Income Tax Return, is akin to the DR 0100 in that it is a required document for reporting income and tax obligations. Both forms involve precise calculations related to tax due and necessitate accurate identification of the taxpayer. However, the Form 1040 is a personal income tax form, while the DR 0100 focuses specifically on sales tax collected from retail transactions.

The Colorado Annual Report form for corporations and LLCs is comparable to the DR 0100 in its requirement for consistent reporting to the state. Both documents require essential business information and the payment of relevant taxes or fees. However, an annual report typically reflects a broader overview of the business’s activities and finances for the entire year, while the DR 0100 centers on specific sales tax obligations during a defined filing period.

The IRS Form 941, which is used to report payroll taxes withheld from employees, is similar to the DR 0100 in that both forms necessitate regular filing with governmental authorities. They require accurate reporting of taxes due, along with identifying information for the business. Despite serving different tax categories, they both hold companies accountable for timely tax remittance and are tied to adherence to respective tax regulations.

The Colorado Withholding Tax Return (Form DR 1094) represents another document similar to the DR 0100, as both involve state taxes that businesses are required to report. Each form has associated deadlines and requirements for payment and filing. While the DR 0100 pertains to collected sales tax, the DR 1094 specifically addresses tax withheld from employees. Thus, while they both serve vital functions in tax reporting, their respective scopes differ.

The Business Personal Property Report (Form DR 201) is similar to the DR 0100 in that it requires detailed reporting of tax liabilities associated with owned business assets. Both documents involve specific deadlines and demand accurate identification of the filing entity. However, while the DR 0100 focuses on sales tax from goods sold, the DR 201 addresses the property taxes applicable to business-owned equipment and fixtures.

The Colorado Business Registration (Form CR 0100) can be compared to the DR 0100 as it also requires essential business information and is crucial for compliance. Both forms necessitate accurate and timely submissions to ensure proper functioning within state regulations. However, the CR 0100 is focused on business formation and registration, while the DR 0100 deals specifically with remitting sales tax collected from retail sales.

When filling out the DR 0100 form for Colorado Retail Sales Tax Return, it is essential to approach the process with care. The following list outlines important dos and don’ts to ensure accuracy and compliance.

Many retailers believe that if they made no sales during a filing period, they can skip filing the DR 0100. This is incorrect. The Colorado Department of Revenue requires all retailers to file a sales tax return for every period, regardless of sales activity. Even when no tax is due, it's essential to submit the return to remain compliant.

Some retailers think they can file a single return for all their business locations. However, each physical site or separate business location requires its own return. Failure to file separately for each location can lead to complications and possible penalties.

A common belief is that electronic payments are straightforward and do not require any specific actions on the return. Retailers must indicate their choice of electronic payment on their return. It’s important to ensure that they check the correct box on line 18 to indicate an electronic payment method. Missing this step can result in confusion regarding payment processing.

Many retailers assume that if they need to correct a previous return, they can just file an amended return without further considerations. While it's true that amendments are allowed, they require a separate return for each filing period and site. Moreover, the amended return replaces the original entirely and must report all corrected amounts, not just the changes. This step is crucial to avoid potential penalties.

Retailers must file the DR 0100 form for every filing period, even if no sales occurred.

Returns typically need to be filed on a monthly basis, but there are variations based on the retailer's sales volume and location.

A separate return is required for each business site or location where sales are made.

Failure to file a return will lead to estimated taxes imposed by the Colorado Department of Revenue.

Retailers have various electronic filing options available, including using Revenue Online, XML filing, or spreadsheet filing.

When paying taxes, retailers can choose between electronic payments through EFT, credit card, e-check, or traditional paper checks.

It is crucial to maintain accurate records for a minimum of three years to ensure compliance and for tax verification.

Both physical and non-physical sites require their own sales tax licenses and respective returns.

Careful attention is needed when reporting local sales taxes, as these vary by jurisdiction and must be itemized in the return.

Penalties may apply for late filings, with specifics regarding interest accruing on unpaid taxes after the due date.