When it comes to securing a loan or establishing a payment agreement, the Delaware Promissory Note form serves as a vital tool for both lenders and borrowers. This legal document outlines the terms of a loan, detailing the amount borrowed, interest rates, and repayment schedule. It is designed to protect the interests of both parties involved in the transaction. By clearly defining the obligations of the borrower and the rights of the lender, the form helps prevent misunderstandings and disputes down the line. Additionally, it includes provisions for late payments and default, ensuring that both parties are aware of the consequences of failing to meet the agreed-upon terms. Whether you are an individual lending money to a friend or a business extending credit to a customer, understanding the nuances of the Delaware Promissory Note form is essential for a smooth and legally sound financial arrangement.

Delaware Promissory Note Template

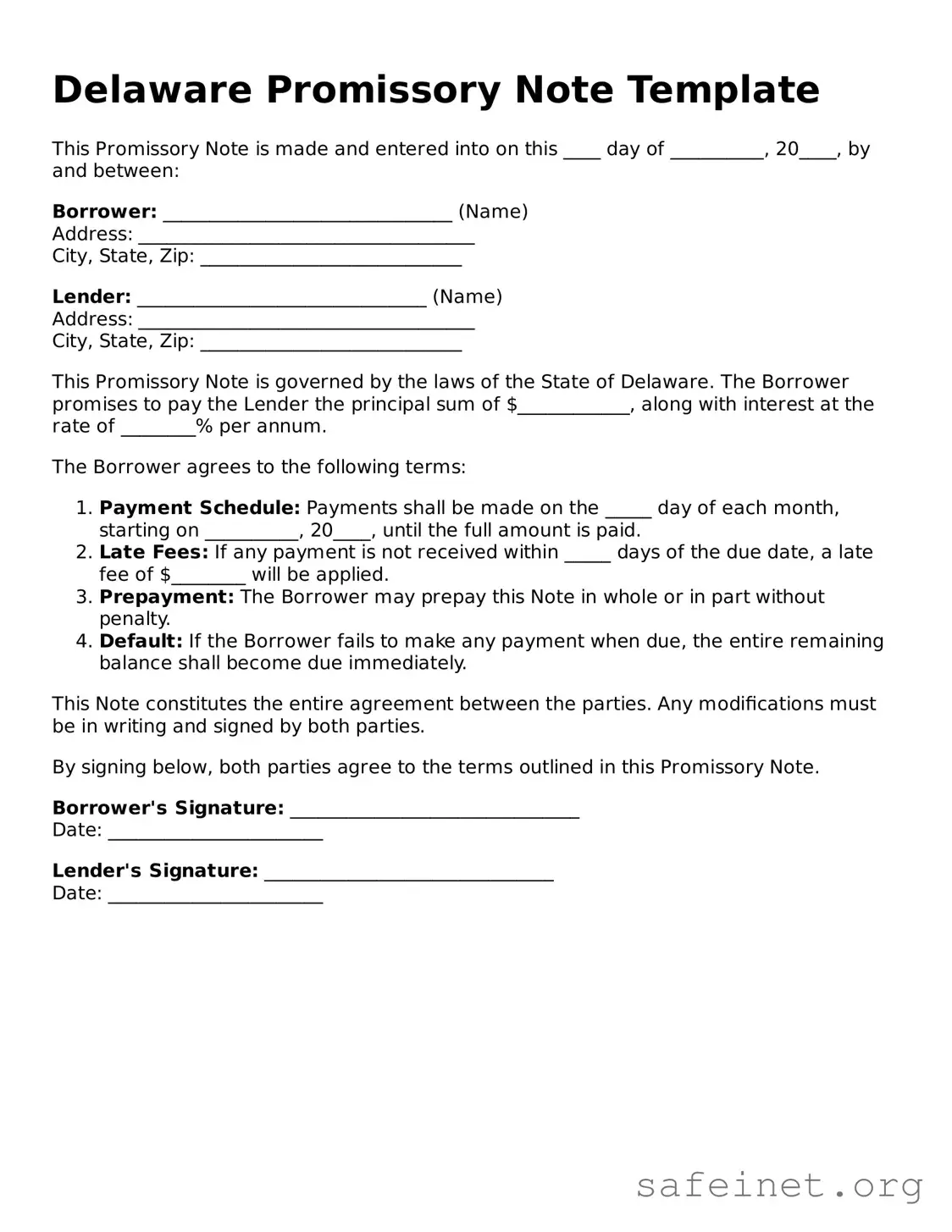

This Promissory Note is made and entered into on this ____ day of __________, 20____, by and between:

Borrower: _______________________________ (Name)

Address: ____________________________________

City, State, Zip: ____________________________

Lender: _______________________________ (Name)

Address: ____________________________________

City, State, Zip: ____________________________

This Promissory Note is governed by the laws of the State of Delaware. The Borrower promises to pay the Lender the principal sum of $____________, along with interest at the rate of ________% per annum.

The Borrower agrees to the following terms:

This Note constitutes the entire agreement between the parties. Any modifications must be in writing and signed by both parties.

By signing below, both parties agree to the terms outlined in this Promissory Note.

Borrower's Signature: _______________________________

Date: _______________________

Lender's Signature: _______________________________

Date: _______________________

| Fact Name | Description |

|---|---|

| Definition | A Delaware Promissory Note is a written promise to pay a specified amount of money to a designated party at a specified time. |

| Governing Law | The Delaware Uniform Commercial Code (UCC) governs promissory notes in Delaware. |

| Parties Involved | The note involves at least two parties: the maker (borrower) and the payee (lender). |

| Interest Rate | The interest rate may be fixed or variable, and it should be clearly stated in the note. |

| Payment Terms | Payment terms, including the due date and payment method, must be explicitly outlined. |

| Signatures | Both the maker and the payee should sign the note to validate the agreement. |

| Enforceability | For the note to be enforceable, it must meet certain legal requirements, including clarity and mutual consent. |

| Default Clause | A default clause may be included to specify the consequences of non-payment or late payment. |

After obtaining the Delaware Promissory Note form, it’s time to fill it out carefully. This document will require specific information about the borrower and lender, as well as the terms of the loan. Make sure you have all the necessary details at hand to ensure accuracy.

What is a Delaware Promissory Note?

A Delaware Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a future date or on demand. This document serves as a legal agreement between the borrower and the lender, outlining the terms of the loan, including the interest rate, repayment schedule, and any collateral involved. It is important because it provides clarity and protection for both parties involved in the transaction.

What are the key components of a Delaware Promissory Note?

Several essential elements make up a Delaware Promissory Note. First, it must clearly state the amount of money being borrowed. Next, it should specify the interest rate, which can be fixed or variable. The repayment terms are crucial; they should outline when payments are due and how they will be made. Additionally, the note should include the names and addresses of both the borrower and lender, as well as any provisions regarding default or late payments. Lastly, both parties should sign the document to make it legally binding.

Do I need to have the Delaware Promissory Note notarized?

While notarization is not strictly required for a Delaware Promissory Note to be enforceable, it is highly recommended. Having the document notarized adds an extra layer of protection, as it verifies the identities of the parties involved and confirms that they signed the document willingly. This can be particularly useful in case of any disputes in the future, as it serves as evidence that the agreement was made in good faith.

What happens if the borrower defaults on the loan?

If the borrower defaults, meaning they fail to make the required payments, the lender has several options. The Promissory Note typically includes provisions that outline what constitutes a default and the steps the lender can take in such an event. Common remedies may include demanding immediate repayment of the full loan amount, pursuing legal action to recover the debt, or seizing any collateral specified in the agreement. It is essential for both parties to understand these terms before entering into the agreement to avoid potential misunderstandings down the line.

Incomplete Information: Many individuals fail to fill out all required fields. Leaving sections blank can lead to confusion and potential disputes later on.

Incorrect Dates: Entering the wrong date can create issues regarding the repayment timeline. Always double-check that the date of signing and the due date are accurate.

Wrong Amount: Some people mistakenly write the loan amount incorrectly. Ensure that both the numerical and written amounts match to avoid misunderstandings.

Missing Signatures: Forgetting to sign the document is a common oversight. Both the borrower and lender must sign to validate the agreement.

Improper Witnessing: In certain cases, a witness may be required. Not having a witness sign can make the note unenforceable in some situations.

Vague Terms: Using unclear language can lead to misinterpretation. Clearly define the terms of repayment, including interest rates and payment schedules.

Neglecting to Include Collateral: If the loan is secured, it’s essential to specify the collateral. Omitting this information can affect the lender's rights.

Ignoring State Laws: Each state has specific requirements for promissory notes. Failing to comply with Delaware laws can render the document invalid.

Not Keeping Copies: After filling out the form, it’s crucial to keep copies for both parties. This helps in maintaining a record of the agreement.

The Delaware Promissory Note is an important document for outlining the terms of a loan. However, it is often used in conjunction with other forms and documents that help clarify the agreement and protect the interests of both parties involved. Below is a list of commonly associated documents.

These documents work together to create a comprehensive framework for the loan agreement. They help ensure that all parties understand their rights and responsibilities, fostering a smoother transaction process.

A Loan Agreement is similar to a Delaware Promissory Note because both documents outline the terms of a loan between a borrower and a lender. A Loan Agreement typically includes details about the loan amount, interest rates, repayment schedule, and any collateral involved. While a Promissory Note serves as a simple promise to repay, a Loan Agreement provides a more comprehensive framework that covers additional terms and conditions, making it a more detailed document.

A Mortgage is another document that shares similarities with a Promissory Note. In a Mortgage, the borrower secures a loan by using real property as collateral. The Promissory Note in this case outlines the borrower's promise to repay the loan, while the Mortgage document gives the lender a legal claim to the property if the borrower fails to repay. Both documents work together to protect the lender's interests.

A Secured Note is akin to a Delaware Promissory Note but includes specific collateral backing the loan. This means that if the borrower defaults, the lender has the right to claim the collateral. Like a Promissory Note, a Secured Note outlines the borrower's obligation to repay the loan, but it adds an extra layer of security for the lender by clearly identifying the collateral involved.

An Unsecured Note is similar in that it is also a promise to repay a loan, but it does not involve collateral. This means that if the borrower defaults, the lender cannot claim specific assets. Both the Unsecured Note and the Promissory Note outline the repayment terms, but the Unsecured Note carries a higher risk for the lender due to the absence of collateral.

A Demand Note is closely related to a Promissory Note, as both involve a borrower's promise to repay a loan. However, a Demand Note allows the lender to request repayment at any time. In contrast, a Promissory Note usually has a fixed repayment schedule. This flexibility can be beneficial for lenders who want the option to call in their loan sooner than expected.

A Personal Guarantee is similar to a Promissory Note in that it involves a commitment to repay a debt. In this case, an individual agrees to be responsible for a loan taken out by a business. While a Promissory Note focuses on the borrower’s obligation, a Personal Guarantee adds a layer of accountability by making an individual liable for the debt, which can provide additional security for the lender.

An IOU (I Owe You) is a less formal document that serves as a simple acknowledgment of a debt. Like a Promissory Note, it indicates that one party owes money to another. However, an IOU typically lacks the detailed terms found in a Promissory Note, such as interest rates and repayment schedules. It is often used for smaller, informal loans between friends or family.

A Credit Agreement is similar to a Promissory Note as it outlines the terms of borrowing money. However, a Credit Agreement often involves a line of credit rather than a fixed loan amount. It details the terms under which the borrower can draw funds, repayment terms, and interest rates. While both documents serve to formalize a borrowing arrangement, a Credit Agreement provides more flexibility in how funds can be accessed.

A Subordination Agreement can also be compared to a Promissory Note. In this case, it establishes the order of claims on collateral in the event of a default. While a Promissory Note specifies the borrower's repayment obligation, a Subordination Agreement clarifies which creditors have priority over others. This is particularly important in situations where multiple loans are secured by the same collateral.

Finally, a Loan Modification Agreement is similar to a Promissory Note in that it involves changes to the terms of an existing loan. If a borrower is struggling to meet repayment terms, they may negotiate a Loan Modification to adjust the interest rate, payment schedule, or other conditions. While a Promissory Note remains the original document of obligation, the Loan Modification Agreement serves to update those terms to better suit the borrower’s current situation.

When filling out the Delaware Promissory Note form, it's essential to approach the task with care. Here are ten important guidelines to follow, including what you should and shouldn't do.

By following these guidelines, you can help ensure that your Delaware Promissory Note is completed correctly and serves its intended purpose effectively.

Understanding the Delaware Promissory Note form can be challenging, and several misconceptions often arise. Here are five common misconceptions explained:

When using the Delaware Promissory Note form, it is essential to understand its key components to ensure its effectiveness and legality. Here are four important takeaways:

By keeping these points in mind, you can create a Delaware Promissory Note that serves its intended purpose effectively.