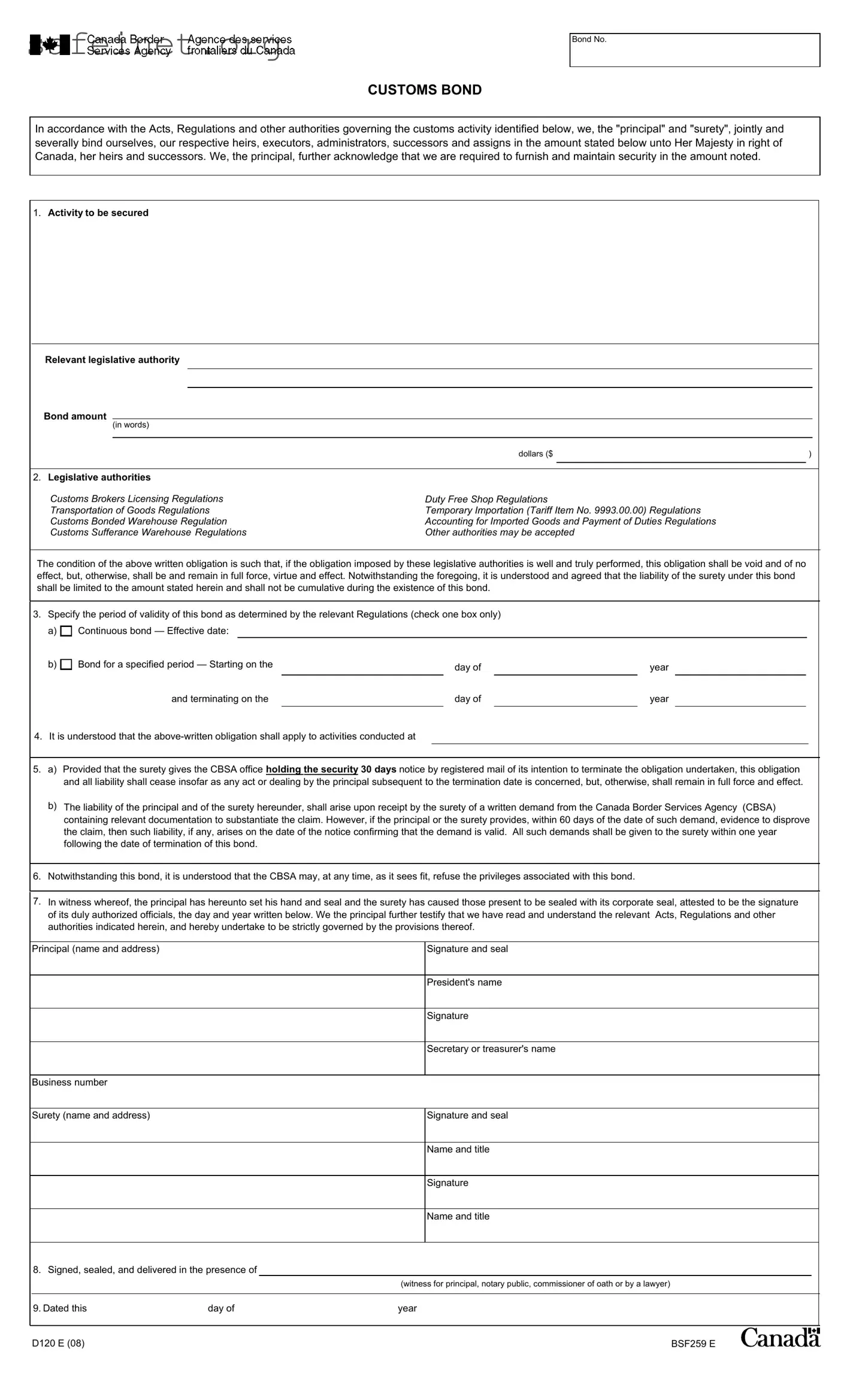

The D120 E form plays an essential role in facilitating customs activities between businesses and the Canada Border Services Agency (CBSA). This document is primarily a Customs Bond, a financial guarantee that ensures compliance with various legislative authorities. It establishes a binding agreement among the principal—typically the business—and the surety, who agrees to cover any obligations should the principal fail to meet them. This form specifies crucial details including the bond amount, relevant legislative authorities, and the duration of the bond’s validity. Business owners must select whether their bond is continuous or for a specific period, which can affect how they manage their customs activities over time. Additionally, the bond clarifies the responsibilities of both the principal and the surety, stating that any liability will arise only under specific conditions, such as upon receiving a written demand from the CBSA. Notably, this bond is also subject to the CBSA’s discretion, which means that the agency retains the right to refuse any privileges associated with the bond. By signing the D120 E form, individuals confirm they have read the relevant regulations and commit to adhering to them, thus underscoring the importance of understanding both the obligations and protections embedded within this crucial customs document.

Bond No.

CUSTOMS BOND

In accordance with the Acts, Regulations and other authorities governing the customs activity identified below, we, the "principal" and "surety", jointly and severally bind ourselves, our respective heirs, executors, administrators, successors and assigns in the amount stated below unto Her Majesty in right of Canada, her heirs and successors. We, the principal, further acknowledge that we are required to furnish and maintain security in the amount noted.

1.Activity to be secured

Relevant legislative authority

Bond amount

(in words)

|

|

|

|

|

|

|

|

dollars ($ |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Legislative authorities |

|

|

|

|

|

Customs Brokers Licensing Regulations |

Duty Free Shop Regulations |

|

|

||

Transportation of Goods Regulations |

Temporary Importation (Tariff Item No. 9993.00.00) Regulations |

|

|

||

Customs Bonded Warehouse Regulation |

Accounting for Imported Goods and Payment of Duties Regulations |

|

|

||

Customs Sufferance Warehouse Regulations |

Other authorities may be accepted |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

The condition of the above written obligation is such that, if the obligation imposed by these legislative authorities is well and truly performed, this obligation shall be void and of no effect, but, otherwise, shall be and remain in full force, virtue and effect. Notwithstanding the foregoing, it is understood and agreed that the liability of the surety under this bond shall be limited to the amount stated herein and shall not be cumulative during the existence of this bond.

3.Specify the period of validity of this bond as determined by the relevant Regulations (check one box only) a)  Continuous bond — Effective date:

Continuous bond — Effective date:

b) |

|

Bond for a specified period — Starting on the |

|

day of |

|

year |

|

|

|

|

|

||

|

|

and terminating on the |

|

day of |

|

year |

|

|

|

|

|||

|

|

|

|

|

|

|

4.It is understood that the

5.a) Provided that the surety gives the CBSA office holding the security 30 days notice by registered mail of its intention to terminate the obligation undertaken, this obligation and all liability shall cease insofar as any act or dealing by the principal subsequent to the termination date is concerned, but, otherwise, shall remain in full force and effect.

b)The liability of the principal and of the surety hereunder, shall arise upon receipt by the surety of a written demand from the Canada Border Services Agency (CBSA) containing relevant documentation to substantiate the claim. However, if the principal or the surety provides, within 60 days of the date of such demand, evidence to disprove the claim, then such liability, if any, arises on the date of the notice confirming that the demand is valid. All such demands shall be given to the surety within one year following the date of termination of this bond.

6.Notwithstanding this bond, it is understood that the CBSA may, at any time, as it sees fit, refuse the privileges associated with this bond.

7.In witness whereof, the principal has hereunto set his hand and seal and the surety has caused those present to be sealed with its corporate seal, attested to be the signature of its duly authorized officials, the day and year written below. We the principal further testify that we have read and understand the relevant Acts, Regulations and other authorities indicated herein, and hereby undertake to be strictly governed by the provisions thereof.

Principal (name and address)

Signature and seal

President's name

Signature

Secretary or treasurer's name

Business number

Surety (name and address)

Signature and seal

Name and title

Signature

Name and title

8. Signed, sealed, and delivered in the presence of

(witness for principal, notary public, commissioner of oath or by a lawyer)

9. Dated this |

day of |

year |

D120 E (08) |

BSF259 E |

| Fact Name | Fact Description |

|---|---|

| Bond Type | The D120 E form is a Customs Bond, ensuring compliance with customs regulations. |

| Governing Bodies | This bond is governed by the Canada Border Services Agency (CBSA) and related Canadian customs authorities. |

| Principal and Surety | The bond requires a principal (the party seeking customs privileges) and a surety (the guarantor). |

| Bond Amount | The bond amount is specified in both words and figures, ensuring clarity in financial obligations. |

| Duration of Validity | The bond can be continuous or for a specified period, as outlined in the relevant regulations. |

| Termination Notice | A 30-day notice by registered mail is needed to terminate obligations of the bond. |

| Claims Procedure | The surety's liability arises upon receiving a claim from the CBSA, with a one-year limit to file such claims after bond termination. |

Filling out the D120 E form is a crucial step for those engaged in customs activities. This form requires careful attention to detail to ensure compliance with relevant regulations. Once the form is completed, it needs to be submitted according to the specified procedures.

What is the D120 E form?

The D120 E form is a customs bond document used in Canada. It serves as a guarantee that the principal and the surety will fulfill their obligations under customs regulations. The bond ensures that the specified amount will be available if there are any claims related to customs activities. This form is crucial for businesses engaged in international trade and helps facilitate smooth customs operations.

Who are the parties involved in the D120 E form?

There are two main parties involved in the D120 E form: the principal and the surety. The principal is typically the business or individual responsible for customs activities, while the surety is usually a bonding company or financial institution that guarantees the principal’s obligations. Both parties sign the bond, making them jointly liable for any claims made under it.

What is the purpose of the customs bond?

The purpose of the customs bond is to ensure compliance with various customs regulations. It acts as a financial safety net for the Canada Border Services Agency (CBSA) in case the principal fails to meet their tax or regulatory obligations. By providing this bond, businesses can participate in activities like importing goods, operating a bonded warehouse, or managing temporary imports.

What is the bond amount and how is it determined?

The bond amount is specified in the D120 E form and can vary depending on the nature of the customs activities being secured. Businesses should assess the financial risks involved and set an appropriate bond amount that reflects their obligations under relevant customs regulations. This ensures adequate coverage in case any claims arise.

How long is the D120 E bond valid?

The D120 E bond can be issued for a specified period or as a continuous bond. If it is a continuous bond, it remains effective until terminated by the surety, provided they notify the CBSA. For a bond for a specified period, the starting and ending dates must be clearly indicated on the form. Understanding the validity period is essential for compliance and ensuring that customs obligations are continually met.

What happens if the bond needs to be terminated?

If the surety wishes to terminate the bond, they must provide the CBSA with 30 days' notice via registered mail. This notice must include relevant documentation. Termination will not affect any obligations that were incurred before the termination date, so businesses must remain vigilant until the process is complete.

Can the CBSA refuse privileges related to the bond?

Yes, the CBSA reserves the right to refuse the privileges associated with the D120 E bond at any time. This could occur for various reasons, including non-compliance with customs regulations or failure to maintain the required bond amount. It's essential for the principal to remain compliant to prevent such refusals.

What should be included in the D120 E form?

The D120 E form requires specific information such as the activities to be secured, the bond amount, the validity period, and the signatures of both the principal and surety. It also requires witness signatures and the principal's acknowledgment of understanding customs regulations. Providing complete and accurate information is critical to avoid issues later.

How is liability determined under the D120 E bond?

Liability under the D120 E bond arises from a written demand by the CBSA, accompanied by relevant documentation supporting the claim. If the principal or surety can disprove the claim within 60 days, liability is reconsidered based on new evidence. All demands must be made within one year following the bond’s termination to be valid.

Where can I find the D120 E form?

The D120 E form can typically be found on government websites related to customs and trade, such as the Canada Border Services Agency's official site. Additionally, businesses can obtain copies through customs brokers or legal professionals who specialize in international trade and customs law.

Failing to provide the correct bond amount. It's important to write both the numeric and written amount clearly to avoid confusion.

Not selecting the proper legislative authority. Carefully choose from the listed regulations to ensure the bond meets your specific needs.

Inadequate completion of the period of validity. Ensure you accurately indicate whether it's a continuous bond or for a specified period, and double-check the dates.

Leaving out crucial signatures. Every required party must sign the form. Missing signatures can delay processing.

Ignoring the requirement for a witness. Ensure you have a qualified witness present and clearly indicated on the form to validate the signatures.

The D120 E form is a vital document used in customs procedures, particularly with the Canada Border Services Agency (CBSA). When submitting this form, there are several other forms and documents that may accompany it, each serving specific purposes essential to the overall process. Understanding these documents can enhance compliance and facilitate smoother transactions.

In summary, the successful navigation of customs processes often relies on various forms and documents in addition to the D120 E form. Each of these documents plays a crucial role in ensuring compliance with customs regulations, minimizing delays, and facilitating smooth trade operations. Understanding the purpose of each helps businesses manage their import activities effectively.

The D120 E form shares similarities with the Acknowledgment of Debt Document. Both documents outline financial obligations and parties involved in an agreement. The Acknowledgment of Debt serves as a formal recognition of a debt, detailing the amount owed and the repayment terms. Like the D120 E, the Acknowledgment ensures that all parties understand their responsibilities and provides a legal basis for enforcing the agreement should the debt remain unpaid.

Another related document is the Surety Bond Agreement. This agreement involves the same principles of securing a financial obligation, where the surety guarantees repayment if the principal defaults. The D120 E form is specifically related to customs duties and regulations, whereas the Surety Bond Agreement can apply broadly across various contexts, including construction and personal loans. Both documents provide a legal framework to ensure that obligations are met and liability is clearly defined.

The Customs Declaration Form also parallels the D120 E form in terms of customs-related activities. A Customs Declaration Form details the goods being transported across borders and the associated duties. It is required for the clearance of imported items through customs. Like the D120 E, it includes relevant legislative references and ensures compliance with regulatory standards. Both forms are critical to facilitate lawful customs operations and assess any liabilities arising from those operations.

Next, consider the Performance Bond, which is frequently used in construction contracts. A Performance Bond serves as a guarantee that a contractor will fulfill their obligations as outlined in a contract. Similar to the D120 E, this document involves the principal (the contractor), the surety (the bond provider), and the obligee (the project owner). Both documents serve to assure involved parties that contractual obligations will be upheld, creating financial security should the principal fail to perform.

The Commercial Lease Agreement also bears some resemblance to the D120 E form. This agreement outlines the responsibilities of landlords and tenants while detailing payment obligations and terms, much like the customs bond outlines obligations to customs authorities and the agreed terms between the principal and surety. Both documents are essential for establishing a clear understanding of duties, rights, and potential liabilities in a formalized structure.

Lastly, the Indemnity Agreement stands as another similar legal document. An Indemnity Agreement is designed to protect one party from any losses or damages incurred due to another party's actions. Like the D120 E, which serves to protect customs authorities against defaulted payments, the Indemnity Agreement clarifies each party's responsibility and limits liability, ensuring that parties understand their obligations in the context of a broader legal framework.

When filling out the D120 E form, it's important to pay attention to details to ensure the process goes smoothly. Here are some guidelines to help you through:

Misconceptions about the D120 E form can lead to confusion regarding its requirements and implications. Below are some common misconceptions clarified:

This is incorrect. The D120 E form is a mandatory requirement for certain customs operations, as it outlines the financial obligations of the principal and surety to the Canada Border Services Agency (CBSA).

In reality, the liability of the surety is limited to the specified bond amount outlined in the form. It does not accumulate or increase over time, regardless of the number of claims made.

This notion is false. A principal or surety may request changes to the terms or conditions of the bond, but such changes must be formally submitted and approved by the relevant authorities.

The bond indeed covers various customs activities, not limited to imports. It applies to activities governed by multiple regulations, including temporary imports and customs bonded warehouses.

Contrary to this belief, the principal’s liability ceases after the bond is terminated, provided proper notice is given to the CBSA, although liabilities incurred before termination still apply.

This is misleading as the CBSA retains the authority to refuse privileges at its discretion, regardless of whether a bond has been issued. Compliance with regulations is essential to maintain those privileges.

Ensure **accurate information**: When completing the D120 E form, provide precise details about the bond amount, the principal, and the surety. Any errors can lead to processing delays.

**Understand the obligations**: Read the obligations laid out in the form carefully. Acknowledge what is required from both the principal and the surety to maintain compliance with relevant regulations.

Be mindful of **notice requirements**: Should you wish to terminate the bond, the surety must provide the Canada Border Services Agency (CBSA) with 30 days' notice via registered mail. Understand that termination does not absolve existing liabilities related to the bond.

**Validity period** is critical: Choose the bond's validity period correctly, whether it's continuous or for a specified term. Misunderstanding this can affect your level of coverage and obligations.