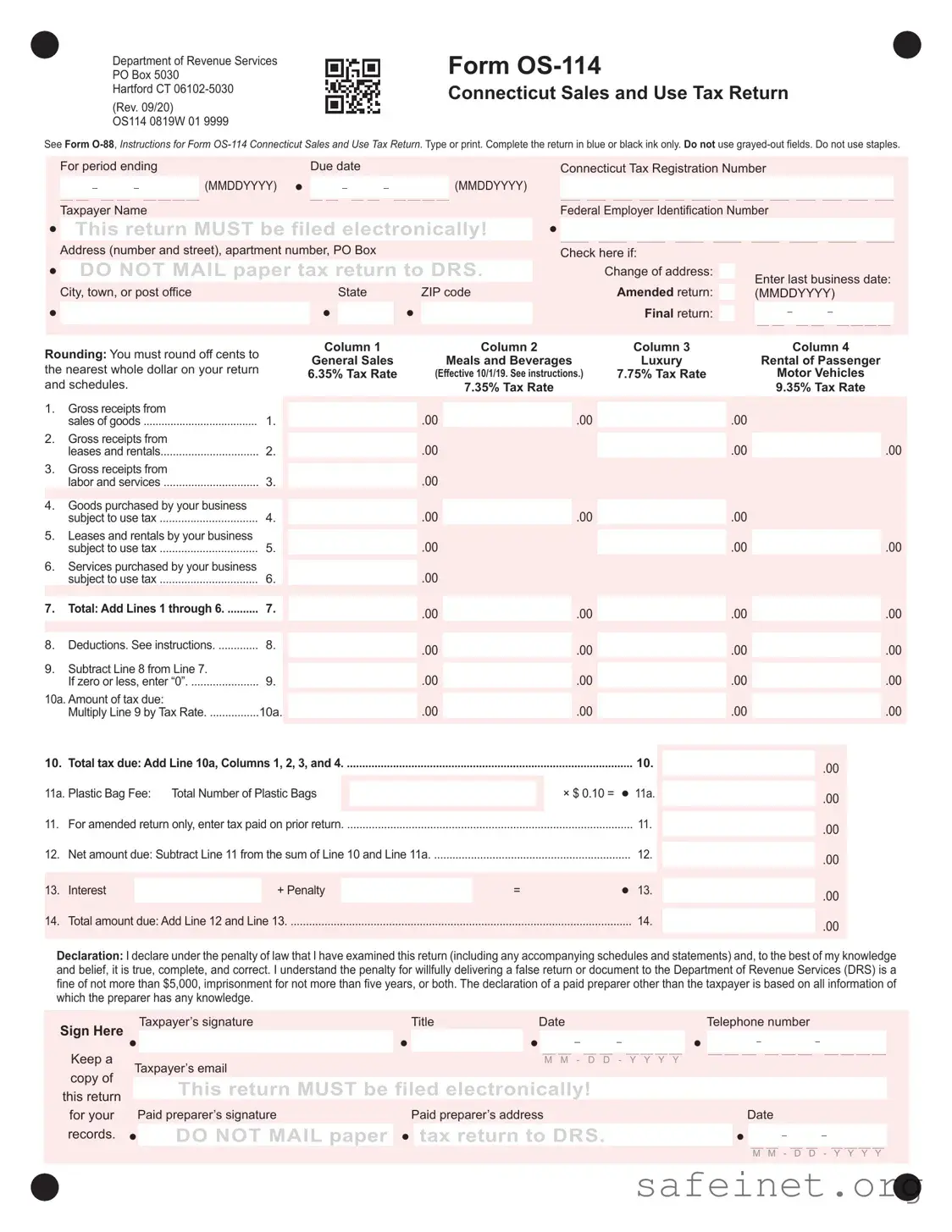

The CT OS-114 form is a crucial document for businesses operating in Connecticut, specifically for reporting sales and use tax. This form must be completed electronically and submitted by the last day of the month following the end of the reporting period. It captures various aspects of a business's operations, including gross receipts from sales of goods, leases, rentals, and services. Taxpayers must provide their Connecticut Tax Registration Number and Federal Employer Identification Number, ensuring accurate identification for tax purposes. The form also includes sections for deductions, allowing businesses to account for non-taxable sales, such as food for human consumption or sales to charitable organizations. Understanding the specific tax rates applicable to different categories—like general sales, meals and beverages, and luxury items—is essential for accurate reporting. Additionally, the CT OS-114 requires taxpayers to declare the accuracy of their information under penalty of law, emphasizing the importance of compliance. By following the instructions outlined in Form O-88, businesses can navigate the complexities of the tax return process with greater ease.

| Fact Name | Details |

|---|---|

| Form Title | Connecticut Sales and Use Tax Return (Form OS-114) |

| Filing Requirement | This return must be filed electronically. Paper returns are not accepted. |

| Due Date | The return is due on the last day of the month following the end of the reporting period. |

| Tax Rates | Various tax rates apply: 6.35% for general sales, 7.75% for meals and beverages, and 9.35% for luxury items. |

| Governing Law | Connecticut General Statutes, Title 12, Chapter 219 governs the sales and use tax in Connecticut. |

Filling out the CT OS-114 form is a crucial step for businesses in Connecticut to report their sales and use tax. After completing the form, it must be filed electronically, ensuring compliance with state regulations. Below are the steps to guide you through the process of filling out the form accurately.

What is the Ct Os 114 form?

The Ct Os 114 form is the Connecticut Sales and Use Tax Return. It is used by businesses to report and pay sales and use tax to the Connecticut Department of Revenue Services (DRS). The form must be completed electronically and is due on the last day of the month following the end of the reporting period.

Who needs to file the Ct Os 114 form?

Any business that sells goods or provides taxable services in Connecticut is required to file this form. This includes retailers, service providers, and any business that leases or rents property. If your business has a Connecticut Tax Registration Number, you must file this return.

How should I complete the Ct Os 114 form?

Complete the form using blue or black ink. You must type or print clearly. Do not use grayed-out fields, and avoid stapling any documents. Round off cents to the nearest whole dollar. Ensure all required fields are filled out accurately to avoid delays in processing.

What are the tax rates associated with the Ct Os 114 form?

The tax rates vary based on the type of goods or services. General sales are taxed at 6.35%, meals and beverages at 7.75%, luxury items at 9.35%, and the rental of passenger motor vehicles at 7.35%. Make sure to apply the correct rate based on your sales.

What is the due date for filing the Ct Os 114 form?

The form must be filed and the associated taxes paid by the last day of the month following the end of the reporting period. For example, if you are reporting for the month of January, the form is due by February 28th.

Can I file the Ct Os 114 form on paper?

No, the Ct Os 114 form must be filed electronically. The Department of Revenue Services does not accept paper returns for this form. You can file electronically through the myconneCT portal.

What should I do if I need to amend my Ct Os 114 form?

If you need to amend your return, check the box for "Amended return" on the form. Fill out the amended information accurately and submit it electronically. Be sure to include any necessary documentation related to the changes.

What happens if I do not file the Ct Os 114 form on time?

Failure to file the Ct Os 114 form on time can result in penalties and interest on the amount due. The penalties can be substantial, so it is important to file your return by the due date to avoid these additional costs.

Where can I find more information about the Ct Os 114 form?

For more details, you can refer to the instructions for Form O-88, which provide guidance on completing the Ct Os 114 form. You can also visit the Connecticut Department of Revenue Services website for additional resources and support.

Incorrect Filing Method: Many individuals mistakenly attempt to mail the OS-114 form. This form must be filed electronically. Ignoring this requirement can lead to delays and potential penalties.

Using Grayed-Out Fields: Some people fill out grayed-out fields on the form. These fields are not applicable and should be left blank. Filling them in can cause confusion and errors in processing.

Inaccurate Tax Rates: Taxpayers often miscalculate the tax due by using incorrect tax rates. Each type of sale has a specific tax rate, and failing to apply the right one can result in underpayment or overpayment.

Rounding Errors: Rounding off amounts incorrectly is a common mistake. All amounts must be rounded to the nearest whole dollar. Inaccurate rounding can affect the total tax due.

Missing Signatures: Some individuals forget to sign the declaration section of the form. A missing signature renders the return invalid and can lead to penalties.

Ignoring Deductions: Failing to account for eligible deductions is a frequent error. Taxpayers should review the instructions carefully to ensure they claim all applicable deductions to minimize their tax liability.

The Connecticut Sales and Use Tax Return, known as Form OS-114, is an essential document for businesses operating in Connecticut. It is crucial for reporting sales and use taxes owed to the state. Along with this form, several other documents are often required to ensure compliance with state tax regulations. Below is a list of these accompanying forms and documents.

Each of these forms plays a vital role in the overall tax compliance process for businesses in Connecticut. Understanding their purpose and how they interrelate with Form OS-114 can help ensure that all required information is submitted accurately and on time.

The Form CT-1040 is similar to the CT OS-114 in that both are tax forms used by individuals and businesses in Connecticut. The CT-1040 is the state income tax return for residents, while the CT OS-114 focuses on sales and use tax. Both forms require detailed information about income or sales, and they must be filed electronically. Additionally, both forms include sections for deductions and credits, which can reduce the overall tax liability. The requirement to round off cents to the nearest whole dollar is also a common feature, ensuring consistency in reporting.

The CT-1065 form is another document that shares similarities with the CT OS-114. This form is used by partnerships to report income, gains, losses, and deductions. Like the CT OS-114, it requires accurate reporting of financial information and must be filed electronically. Both forms emphasize the importance of providing correct information under penalty of law, highlighting the serious nature of tax compliance. Each form also includes a declaration section where the taxpayer affirms the accuracy of the information provided.

The CT-1120 form is the corporate income tax return for businesses in Connecticut. It is similar to the CT OS-114 in that it requires businesses to report their financial activities to the state. Both forms must be filed electronically and include sections for deductions and tax calculations. The CT-1120 also has specific tax rates that apply, much like the varying rates found in the CT OS-114 for different types of sales. Additionally, both forms require a declaration of truthfulness from the taxpayer or preparer.

The CT-941 form is a quarterly tax return used by employers to report employee wages and withholdings. Similar to the CT OS-114, it requires detailed financial information and must be filed electronically. Both forms include sections for calculating tax amounts due, and they emphasize compliance with state tax laws. Employers must ensure accuracy in reporting to avoid penalties, much like businesses filing the CT OS-114 for sales tax purposes.

The CT-990T form is used by tax-exempt organizations to report unrelated business income. This form is similar to the CT OS-114 in that both require the reporting of specific financial activities to the state. Each form must be filed electronically, and both include sections for calculating tax liabilities. The CT-990T also includes a declaration of truthfulness, reinforcing the importance of accurate reporting, akin to the CT OS-114’s declaration section.

The CT-1041 form is the fiduciary income tax return for estates and trusts in Connecticut. Like the CT OS-114, it requires detailed financial reporting and must be filed electronically. Both forms necessitate accurate calculations of tax due and provide sections for deductions. The CT-1041 emphasizes compliance with state tax laws, similar to the strict requirements found in the CT OS-114 for businesses reporting sales and use tax.

The CT-1096 form is used for reporting information returns and is similar to the CT OS-114 in that both require electronic filing and accurate reporting. The CT-1096 focuses on information related to payments made to non-employees, while the CT OS-114 focuses on sales and use tax. Both forms require a declaration of accuracy, highlighting the importance of truthful reporting in tax matters.

The CT-1120SI form is the small business income tax return in Connecticut. It shares similarities with the CT OS-114 as both forms require businesses to report financial activities and must be filed electronically. Each form includes sections for calculating tax liabilities and deductions. The CT-1120SI also emphasizes compliance with state tax laws, similar to the CT OS-114’s focus on sales tax compliance.

The CT-8862 form is used to claim the Earned Income Credit after a disallowance. It is similar to the CT OS-114 in that both forms require accurate reporting and must be filed electronically. The CT-8862 focuses on tax credits, while the CT OS-114 focuses on sales and use tax. Both forms include declarations affirming the accuracy of the information provided, underscoring the importance of compliance with tax regulations.

Filling out the Connecticut Sales and Use Tax Return, Form OS-114, can be a straightforward process if you follow some essential guidelines. Here are nine things you should and shouldn’t do to ensure your form is completed accurately.

Misconception 1: The CT OS-114 form can be filed on paper.

Many people believe they can submit the CT OS-114 form by mail. However, this form must be filed electronically. The Department of Revenue Services (DRS) does not accept paper returns for this form.

Misconception 2: All businesses can use the same tax rates.

Some individuals think that a single tax rate applies to all businesses. In reality, different tax rates apply to various categories, such as general sales, meals and beverages, and luxury items. It is important to refer to the specific rates listed on the form.

Misconception 3: The due date for filing is the same for all periods.

People often assume that the due date for filing the CT OS-114 form is constant. In fact, the due date varies depending on the filing period. The form must be submitted by the last day of the month following the end of the reporting period.

Misconception 4: You can skip rounding off cents.

Some individuals think that rounding off cents is optional. However, the form requires you to round off cents to the nearest whole dollar. This applies to all calculations on the return.

Misconception 5: The form does not require a declaration.

Many people overlook the importance of the declaration section on the form. A signed declaration is necessary to confirm that the information provided is true and complete. Failing to do so can result in penalties.

Filling out and using the Ct OS-114 form is a crucial task for businesses in Connecticut. Here are some key takeaways to keep in mind: